Good morning … A classic RISK OFF bid for USTs it was and its been awhile since it was that straight forward …

ZH: Oil Surges Over $90, Stocks Tumble After Israel Puts Embassies Around World On Maximum Alert

… To be clear there is SOME disagreement here, fundamentally, to lay full blame on Israel, it IS interesting to note this willingness for the markets to place the price of ‘Earl on top of the list of its ‘woes’ (seriously after the straight line UP?) and then to cite chapter and verse (as you’ll see below) whatever it was Neel said.

First up, ‘Earl …

… and why we all care …

… currently payin’ $3.15 / gal here in NJ so far from the ‘natl avg’ BUT with idea of full disclosure in mind and for better / worse, we’re getting full serviced (we do not yet pump ourselves here and best I reckon, we’re the last remaining state in the union with such archaic laws … i’d imagine $3.15 would be somewhat lower (but likely also having an economic impact across the region) …

‘Earl and so, gas prices, are all very important and whether you believe they are high and rising because of Bidenomics OR because of Israel and, to a lesser degree, Ka$hkari, I’ll let you decide … before I continue along with more on Ka$hkari, and with all due respect, as we all know, opinions are created equally and it’s just that some, for whatever reason, are created MORE equal than others.

#FOMC101 is where you’ll scroll and note Neel’s NOT a voter and again, with all due respect as HIS view > my view for sure … I’d only offer context along the lines that the market sees whatever it wants to see and prices however it feels is most appropriate at any given time.

Yesterday was a classic risk OFF move with USTs catching a bit of a (cleanup) bid…

… From Bloomberg.com early evening …

Bloomberg: Fed’s Kashkari Floats Possibility of No Rate Cuts This Year

… “In March I had jotted down two rate cuts this year if inflation continues to fall back towards our 2% target,” Kashkari said in a virtual event with LinkedIn on Thursday. “If we continue to see inflation moving sideways, then that would make me question whether we needed to do those rate cuts at all.”

AND … presented without much additional commentary …

ZH: Jobless Claims: Spot The Odd (Government-Supplied) One Out

… But, according to the government-supplied data...

The number of Americans filing for jobless benefits for the first time last week rose from 212k to 221k (SA) to its highest since Jan, and claims ticked modestly higher on an NSA basis...

… Continuing claims remain glued around 1.8mm Americans - where they have been for nine months...

… But, here's the thing... WARNs are soaring... and Challenger-Grey just announced that March saw the most job cuts (90,309) since January 2023...but government-supplied data on initial jobless claims continues to smoothly tick along near record lows...

… here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are just a hair cheaper this morning as global markets brace for today's US employment data amid rising geopolitical tensions. DXY is higher (+0.15%) while front WTI futures are a touch higher (+0.25%) too. Asian stocks followed NY lower, EU and Uk share markets are all heavily in the red (SX5E -1.45%) while ES futures have rebounded by +0.3% here at 7am. Our overnight US rates flows saw large lifts in TY futures in the Asian morning session with a TU block buy hitting around the London crossover. Cash volumes were muted and in London hours position squaring was a theme. We had real$ buying in the front-end and fast$ interest to add 5s30s-type steepeners. Overnight Treasury volume was ~ 75% of average.

… That 4.33% to 4.35% support zone in Tsy 5's and 10's has been pretty well-defended so far, right? I'd say impressively so, to date. That could all change today- or next week after the inflation data. We'll just have to see. In our first attachment this morning we take a look at the price set-up in Treasury 5yr yields again. The so-called Ascending Triangle (defined by the black lines) remains in place while daily momentum (lower panel) is signal-less as investors hold breath for the upcoming data. The rules of Ascending Triangles still apply, and they posit that the flat side (4.35%) will eventually be taken out to the upside.

That said, Tuesday's and Wednesday's albeit brief forays above range supports were met with buying and covering-so we hope to learn more about how this price pattern resolves itself at today's closes. Indeed, we may have to wait until next Thursday's post PPI closes (PPI has been a notable markets-mover in recent months) for pattern resolution; who knows? The set-ups in Treasury 2yr yields and in 10yr real rates (TIPS) look predictably similar, as we show in our next two attachments with the key levels penciled in…

… THEIR BBG visuals > my TV ones but I’ll still have a go at it over weekend ‘weather’ permitting … and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Relatively contained trade into NFP as Europe catches up to geopols … Fixed income benchmarks slightly softer as they give back some of Thursday’s risk-inspired upside … USTs a touch softer but remain towards the top-end of Thursday's parameters; NFPs and Fed speak the highlights ahead where an above-forecast number could see a resumption of the earlier bear-steepening while a soft print could see this unwind further - geopolitical updates also a potential key factor …

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ … and this mornings pre NFP thoughts are a combination of NFP as well as CPI precaps and victory laps …

The correlation between change in nominal yields and equity returns is quite negative vs. history when considering the benchmark 10Y's t12m trading range. If this sustains, upward pressure on nominal yields will likely be problematic for equities, particularly as the 10Y yields approach the 5% key level.

BARCAP US CPI Inflation Preview (March 2024 CPI): A little more progress

We forecast a 0.30% m/m SA rise in headline CPI, taking the annual rate up to 3.4% y/y amid unfavorable base effects. We estimate that core price pressures decelerated modestly, rising 0.31% m/m, led by an easing in both goods and services prices. We expect the NSA index to print at 312.051.

BARCAP (EZ)Equity Market Review - Oil breakout (attempt to frame move in context of impact on CPI — short version, don’t worry. yet)

Surging oil is reviving stagflation fears, amid renewed geopolitical tensions. But we think it is also reflective of an improving cyclical backdrop. Rising oil is typically a positive for market earnings and favours cyclicals over defensives. SXEP has ~10% relative upside potential to close the gap vs. the higher oil price.

Oil demand closely tracks global growth, and market earnings move closely with oil…

BloombergBNP US March CPI preview: Easing back into a moderating trend (once again not sure how this sort of ‘research’ helps on a Thursday just ahead of NFP where they could have given us this … i dunno … over the weekend, with a NFP recap?)

KEY MESSAGES

After two strong inflation prints to start the year, we think March will begin a string of relatively more moderate price gains.

We expect core CPI to tick down to 0.3% m/m (0.4% prior, 3.7% y/y), with another month of higher gasoline prices keeping headline CPI inflation at 0.4% (3.4% y/y, NSA index 312.180).

We think start-of-year adjustments had a role in January and February’s strong core prints, and likewise see the reversal of this effect contributing to a lower March reading. Nonetheless, risks still skew to the upside, as the impact of OER methodological changes remains uncertain.

Based on our March CPI expectations, we see March PCE inflation printing 0.2% m/m, which should fall into the “good” bucket of inflation readings, according to Fed officials.

Goldilocks: Trade Deficit Widens Slightly; Initial Claims Increase; Boosting Q1 GDP Tracking to +2.5%

BOTTOM LINE: The trade deficit widened slightly in February, somewhat above consensus expectations for a narrower reading. Initial jobless claims rose by more than expected, while continuing claims were below expectations. The details of the trade balance report were somewhat firmer than our previous expectations, and we boosted our Q1 GDP tracking estimate by 0.2pp to +2.5%.

Goldilocks: March Payrolls Preview (cuz, you know, sending this last night really helps get us ready to TRADE or invest …)

We estimate nonfarm payrolls rose by 240k in March—above consensus of +213k. Our forecast reflects a continued boost from above-normal immigration, as new entrants to the labor force are matched to open positions. Big Data measures also generally indicate a solid or strong pace of job gains, and our layoff tracker indicates that the pace of layoffs remains low. We nonetheless assume a slowdown from the February payroll gain of +275k because we believe a favorable swing in the weather boosted that report by as much as 75k.

We estimate that the unemployment rate fell one tenth to 3.8%—in line with consensus. Foreign-born unemployment increased by nearly 250k over the last three months, and we assume many of the new entrants found jobs during the March payroll month. We assume a flat-to-up labor force participation rate of 62.5%. We estimate average hourly earnings rose 0.25% month-over-month, which would lower the year-on-year rate by three tenths to 4.0%—somewhat below consensus of +0.3% and +4.1% respectively. Our forecast reflects waning wage pressures but a roughly 5bp boost from calendar effects (mom sa)…

We think core CPI came down to 0.25%M in Mar-24 (0.3%M cons, 3.7%Y annual rate) after a strong print the month prior. Weak used cars and continued gradual disinflation in rents are key drivers. We see headline at 0.29%M on the back of lower energy inflation (3.4%Y, NSA Index: 312.008)

UBS (Donovan): Employment report Friday—do we care? (clearly he does not and you can even sense his dismissive, condescending tone and British accent — no offense — coming through in is written word … )

It is US employment report Friday (or “average earnings are not wages” day). Since mid-last year, the US has added almost 1.60 million jobs, and has also lost almost 0.25 million jobs depending on which bit of the employment report you read. Labor markets are changing—flexible working, changing industries like online retail, new jobs like social media influencers, the rise and fall of job hopping, side hustles and more self-employment, automation, volunteering, early retirement, and population movements. Data is not capturing these changes properly.

Rather than obsessing about employment data signals, it might be better to focus on the consequences. The US labor market is not generating fear of unemployment—important as that is one of the few things that could break US consumer hedonism. However, real wage growth remains modest and nominal wage growth is slowing. This suggests the labor market supports a soft landing with moderate inflation.

Yardeni: Loose Fed Lips Sink Stocks (he said, she said … point is NEITHER Ka$hkari NOR Dr. ED are voting members yet we seem to put some extra weight on these popular kids … on IN the FOMC and one … not so much … oh, vigilantes, where art thou…)

We are in the same camp as Federal Reserve Bank of Minneapolis President Neel Kashkari. On March 6, he said, "If we have a run rate that's very attractive, people have jobs, businesses are doing well, inflation is coming back down, why do anything?" We wrote an op-ed in the March 25 Financial Times titled, "The Fed should resist messing with success." We asked: "If the economy is doing well with the current level of interest rates, why lower them?"

Today, the stock market sank in the afternoon after Kashkari said, "If we continue to see inflation moving sideways, then that would make me question whether we needed to do those rate cuts at all."

But why did the stock market drop so sharply after he essentially reiterated his position (chart)? Investors might be finally discounting the possibility of a no-show rate cut this year. Traders might have concluded that a strong employment report tomorrow might cause more Fed officials to turn more hawkish.

And then there is the price of a barrel of Brent crude oil: It rose above $90 today (chart). According to Israeli media, Israeli diplomats serving abroad have expressed their concern that their embassies will be the target of Iranian retaliation following Monday's alleged Israeli strike on Syria, which killed senior Iranian Islamic Revolution Guard Corps (IRGC) member Mohammad Reza Zahedi.

… And from Global Wall Street inbox TO the WWW,

AllStarCharts: Bonds Tank As Commodities Soar (straight forward…except that bonds were BID today as Earl went up … but who’s countin)

… Check out our Global Benchmark Rate Composite, an equal-weight basket of Developed Market 10-year yields (Germany, UK, Canada, France, Italy, Spain, Switzerland, Japan, Australia, and the US):

Our global composite is holding well above the lower bounds of a yearlong range, catching toward the underside of a flat 200-day moving average.

Yields on sovereign debt show no signs of an imminent collapse.

Could rates roll over in the coming quarters? Absolutely!

But the data fails to support a falling interest rate thesis. In fact, the charts suggest quite the opposite…

The commodity-bond ratio resembles Developed Market rates with two exceptions: Commodities vs. bonds are trading above their long-term average and breaking above their 2022 highs.

Since this classic intermarket ratio peaked first, heading into its mirrored consolidation, perhaps it’s leading to an eventual upside resolution in global yields. ..

Bespoke: What Caused Today's Downside Reversal? (NOT what I thought I’d find — another NEEL recap / victory lap — and actually something that makes a ton of sense … EXCEPT that ‘Earl UP is NOT bullish long bonds. it just isn’t. change my mind, BESPOKE, go ahead … waiting … unless you are saying there’s war on the way? )

… Nasdaq Reversal Bulls were relishing 1%+ gains for the Nasdaq this morning, but a series of events ultimately turned the tide in dramatic fashion, and by the close, the Nasdaq was down more than 1% on the day.

On the geopolitical side, US Secretary of State Anthony Blinken made a comment this morning that Ukraine would become a NATO member, and later in the day, rumors spread that various US and Israeli intelligence agencies were preparing for an imminent attack on Israeli soil from Iran. Oil prices, which began the day lower, began to surge around mid-day and ultimately closed above $90.

Along with the spike in oil prices, we got more hawkish Fedspeak this afternoon from Minneapolis Fed President Neel Kashkari. Kashkari used to be a prominent dove but is now on the much more hawkish side of the Fedspeak spectrum.

As shown in the intraday chart of the Nasdaq versus oil prices below, equities didn't immediately react negatively to the initial turn higher in oil just after noon. It wasn't until the start of Kashkari's speech that stocks ultimately began selling off, and traders continued selling all the way into the close.

Over the last 20 years, the Nasdaq has seen a 1%+ intraday gain reverse and close down more than 1% a total of 58 times. What's rare, though, is for these reversals to occur so close to a 52-week high for the Nasdaq.

Bloomberg 5 Things You Need to Know to Start Your Day: Asia (for the visual of rate cuts pricing and importance of NFP and just how GOOD would be BAD for global macro … i hate this already…”)

… US equities dropped overnight as Middle East tensions intensified, though investors may have been readier to sell than usual heading into the payrolls report due Friday. Risk assets had been holding up well until the latest Israel-Iran mutterings caused a pop in crude oil prices.

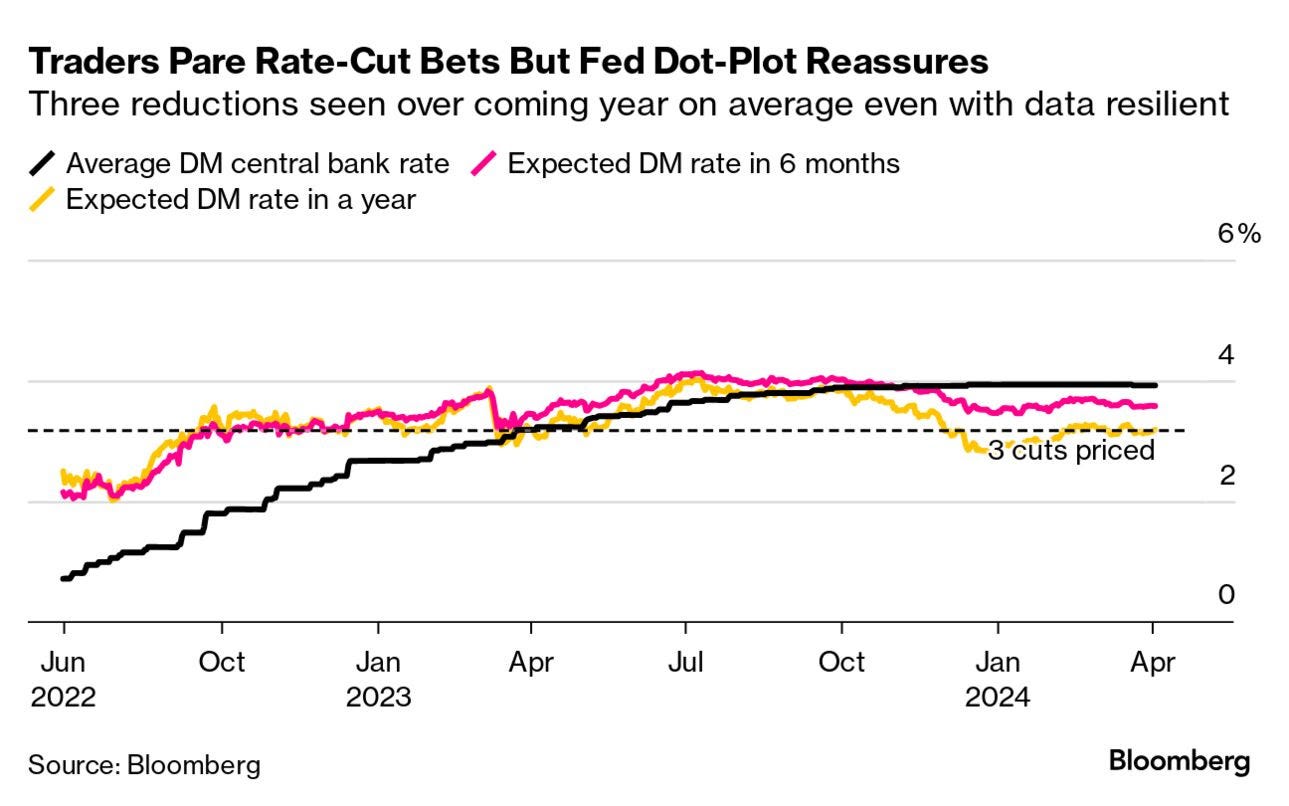

The prior calm in stock markets owed much to the steady hand of Federal Reserve Chairman Jerome Powell’s insistence — in the face of robust economic data — that interest-rate cuts are coming this year and that there are likely to be three of them. Another upside for payrolls — the past three releases beat consensus by an average of 78,000 jobs — would likely spur markets to start expressing serious doubts the Fed will be able to ease as much as it has projected.

That’s a concern for global markets. While traders have pared their expectations for policy easing across developed economies, they still see an average of one quarter-point rate cut within six months, as part of three reductions expected within a year. Another jobs blowout would threaten that consensus, and create the risk of another episode like the one that came in September-October of last year, when bonds and stocks tumbled. A surge in oil prices amid geopolitical tensions also helped fuel those moves.

Bloomberg: How Seriously You Should Take the Market Pullback (Authers OpED — claim here is that we should blame … wait for it … Israel … WTaF … safe to do now that Biden admin now seems to be turning away from support? I’m dismayed, to say the least but not at all surprised … )

Stocks were due for a retreat, but don’t read too much into it. And view non-farm payrolls with some caution.

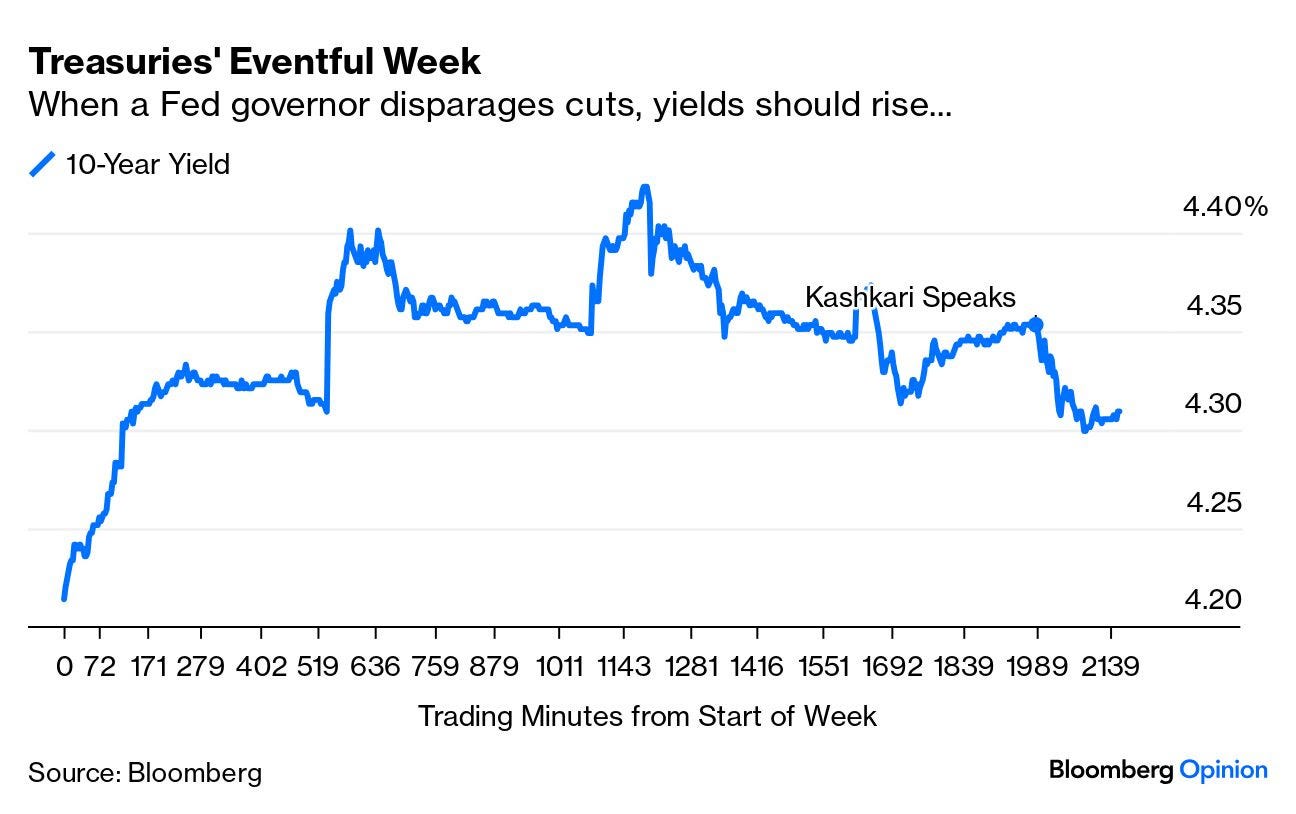

…It’s Not About Fears of Higher Rates Initial reactions blamed hawkish comments from Neel Kashkari, president of Federal Reserve Bank of Minneapolis, who said that it may not make sense to cut rates at all this year. That might be a big deal, except he’s already well established as the most hawkish of the Fed’s governors, and he doesn’t get to vote on monetary policy this year. And the 10-year Treasury yield actually fell significantly after his comments:

It’s Hard to Call This a True Risk-Off Something unusual happened during the afternoon session, and a move to buy Treasuries certainly implies safe-haven demand from people fleeing risk (most plausible from geopolitics, of which more later). If there was truly elevated concern about global risks, however, that safe-haven demand would also push up the price of gold. And yet bullion fell in the afternoon session. That’s an orthodox reaction to comments like Kashkari’s, but it’s not a safe-haven bid.

This Was Driven Primarily by the Oil Price What really did matter, evidently, was the oil price, which rushed higher, swiftly passing the round number of $90 per barrel, at the same moment that the stock market suddenly started to fall. That was at 1:40 p.m.in New York, just as the contents of the latest conversation between President Joe Biden and Israel’s Prime Minister BenjaminNetanyahu were published. With Netanyahu claiming that Israel would “hurt those who hurt us or plan to hurt us” while naming Iran, and Biden again repeating that the US wanted a ceasefire in Gaza, the meeting could be taken to increase the risks of an escalation in the conflict:

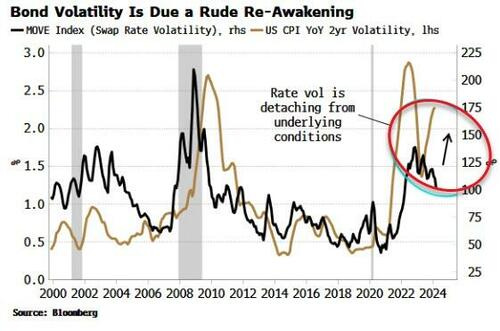

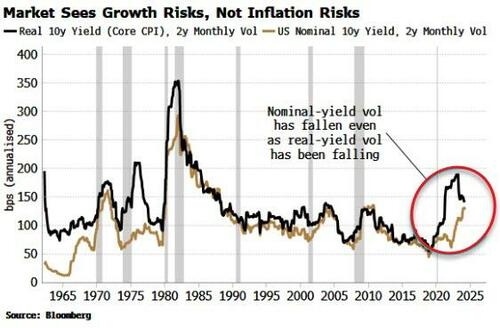

Bloomberg (via ZH): Bond Market's Eerie Calm Belies Bigger Move On Way

… Most focus has been on slowing inflation, but inflation volatility is telling a different story. It’s the variability in inflation as much as its level that’s a problem for bond volatility. Inflation’s volatility, after dipping, is rising strongly again. The MOVE is soon likely to correct higher to reflect rising inflation uncertainty.

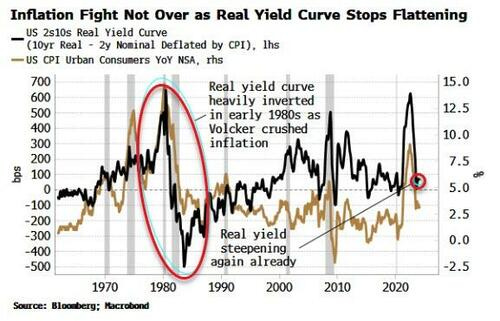

The disconnect is not confined to inflation volatility. The real yield curve, which typically flattens as inflation falls, has stopped flattening, and signally failed to invert as it did in the early 1980s when Volcker unambiguously snuffed out inflation by jacking real rates considerably higher.

…Bonds face inflation as well as upside growth risks, but markets appear to be more worried about the second than the first. Implied bond volatility might be falling, but realized volatility in nominal 10-year yields has been rising. Until early last year, volatility in real yields was also rising, but since then it has been falling.

This suggests a market expectant of upside growth risks (as leading data has been projecting, and the recent better-than-expected manufacturing ISM was a timely reminder of), but exceedingly relaxed about risks from inflation.

Bloomberg (via ZH): Gold's Defiance Of Real Yields Can't Last Unless Trouble Brewing

Gold’s surge to record highs is extraordinary — coming as it does in the face of elevated real yields that would normally bring it crashing down. That signals the metal is likely to rapidly reverse this year’s climb, unless risk assets collapse because of an economic or financial crisis.

The 10-year real yield is still around 2%, a level unseen since 2009. That should hurt a non-interest-bearing asset like gold, but it isn’t. The previous two times before the current surge when gold hit record highs were times of negative real yields — during the pandemic and in 2011-12 as Europe’s sovereign debt woes followed on the heels of the global financial crisis…

Hedgopia: Extremely Overbought Stock Market Uses Non-Voting FOMC Member Kashkari’s Hawkish Comments As Excuse To Sell Off

… This was also the fourth week in a row the bullish percent remained north of 60 percent. The last time this sentiment was as elevated was the latter months of 2020 and early 2021. Back then, for 10 consecutive weeks between November 2020 and January 2021, bulls’ count remained north of 60 percent, with the bulls-to-bears ratio well north of three percent. This bullishness got hardly unwound in 2021, as, between January and July, there were 10 weeks of bulls over 60 percent. The S&P 500 suffered a minor drop in January but went on to rally in nine of the next 11 months to finish 2021 up 26.9 percent. This was when the equity allocation jumped to 37.7 percent. And this is what ultimately gave way to the 2022 collapse in stocks.

… With one session to go, the S&P 500, down two percent this week to 5147, is now in breach of a rising trend line from last October’s low (Chart 3). A similar trend line on the Nasdaq 100 was compromised three weeks ago. Thursday’s 1.2-percent decline resulted in the S&P 500 also losing shorter-term moving averages, with the bulls unable to defend 5170s and also not able to push through 5260s. The index peaked at 5265 on March 28th.

Ironically, Thursday’s selloff was blamed – wrongly – on hawkish interest-rate comments from Neel Kashkari, Minneapolis Fed president. First, he has been hawkish for a while now. Second, he is not a voting member this year. This is an extended market looking for a reason to sell off, and there is a long way to go before the currently soapy sentiment is unwound.

WolfST: Fed’s Kashkari Says Quiet Part Out Loud: Maybe No Rate Cuts in 2024 if Inflation Continues to Move “Sideways”

Catching up, we're paying about $5 here abouts Sactown a gallon, paid $4.85 at Costco last night. But we pay over $1 per gallon in Climate Change Taxes oops meant FEES; was realizing just what a psyop Gov Gavin Newsom's 'Gas Gauging Taskforce' was/is. Full Service what's that lol! Not even offered out here but I do remember! But I'm old I remember my dad's 1969 Volvo needing Leaded Gas.

Catching up, we're paying about $5 here abouts Sactown a gallon, paid $4.85 at Costco last night. But we pay over $1 per gallon in Climate Change Taxes oops meant FEES; was realizing just what a psyop Gov Gavin Newsom's 'Gas Gauging Taskforce' was/is. Full Service what's that lol! Not even offered out here but I do remember! But I'm old I remember my dad's 1969 Volvo needing Leaded Gas.