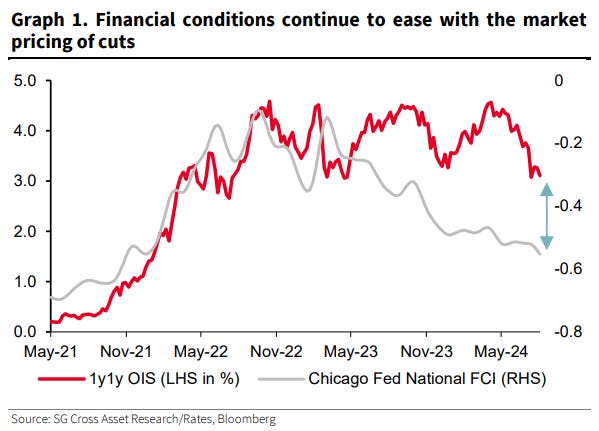

while WE slept: USTs flat ahead of mfg PMI, bunds bid, JGBs under pressure; "biggest inversion between FF1 and FF12 futures in 36 years, at -193bps. This suggests the market expects a ~2ppt cut"

Good morning … a very happy bday (albeit belated … sorry but not sorry — the Hobbit never sent ME a card on time, or at all, tbh) TO … The Dept of Treasury.

On 9/2/1789, Congress created the Treasury to manage government finances. Happy 235th birthday to the US Treasury. Hamilton was appointed at 1st Secy of Treasury by none other than George Washington …

… For better or worse, here we are and given monthly candlesticks and bars have now been finalized, a longer’ish term look at USTs

10yy MONTHLY: 5.00 to 3.75% (give or take)

… longest term avail to ME via TV is via a LINE graph and so i’ll attempt to contextualize a bit more with monthly bars (inset) …

30yy MONTHLY: 5.25% 4.00% (give or take)

… AND here is a snapshot OF USTs as of 641a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Subdued sentiment ahead of US ISM Manufacturing, JPY bid & Crude slips USTs flat ahead of key US ISM Manufacturing PMI, Bunds slightly firmer … USTs are flat as we await the return of US participants from Monday's holiday, but as focus remains on US ISM Manufacturing data later. No real follow-through from JGB pressure overnight after a relatively subdued short-dated tap. In a narrow sub-10 tick range which is at the mid-point of Monday's 113-14 to 113-30+ band.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ … in addition TO what little was noted HERE over the weekend)

… The Biggest Picture: the policy put (BoJ capitulation) & credit resilience (CDX spreads <50) have cut ‘hard landing’ fears, but watch US hiring…the last 6 times private sector share fell <40%, recession followed (Chart 2); dominance by gov’t & friends (education & health) not bullish for productivity (Chart 3); “long bonds” the best hard landing hedge…

… Flows to Know:

… Treasuries: largest inflow since Oct'23 ($8.4bn – Chart 10)

We are cognisant of the risks of higher yields and flatter curves temporarily if US data is stronger this week (as we expect it to be). Nonetheless, we retain a bullish rates bias via steepeners and US-Europe compression trades with a bias to add bullish duration exposure on pullbacks.

We explore CTA ‘pressure points’ and find that USD shorts versus EUR, GBP and CEEMEA are most vulnerable to being unwound. By contrast, global rates and commodity model positioning appears less stretched.

US equities could make new all-time highs on better US data this week, in our view.

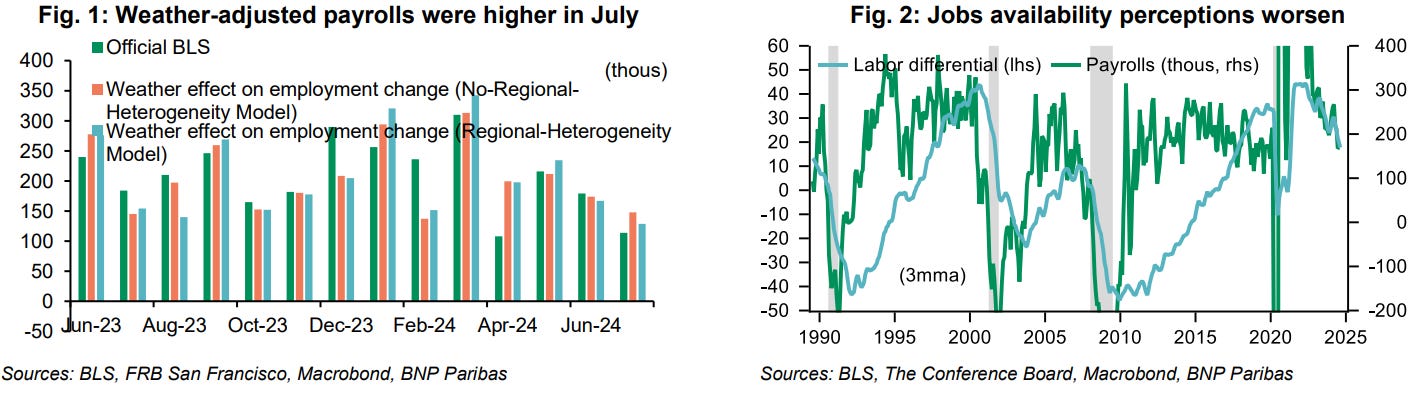

… we think weather effects exaggerated weakness in the July report and that the August report will clarify the signal versus the noise. We estimate severe weather was responsible for the roughly 30-35k gap between the reported 114k gain and the underlying pace of around 140-150k. Adding these jobs back to the August data would push the reported reading above that level, resulting in a monthly pace of around 175k, we think. For more details see US August jobs preview: Sizing September’s rate cut, dated 29 August.

Markets remain undecided between a 25bp and 50bp cut in September (pricing at the time of writing is 32bp). While a clearly weak payrolls report likely leads to a 50bp cut, Powell’s dovish stance toward the labor market in his Jackson Hole speech may have lowered the bar for a more aggressive Fed should NFPs be only modestly weak.

At a high level, the market’s reaction function to NFPs looks relatively symmetric given we are still priced for about 100bp in 2024 cuts and a 3-3.25% fed funds rate by end-2025. However, larger yield moves appear asymmetrically skewed lower. An extreme downside surprise in August NFPs (especially if followed by increasingly weak economic data) would give the market more room to price a much more aggressive Fed over the coming quarters. An upside surprise would shift market expectations toward a 25bp-per-meeting cadence for this year, but still subject to the evolution of data going forward. Based on risk–reward, our bias remains for lower rates and a steeper curve and we retain our 5s30s UST steepener even though we are cognisant of the risk of higher yields and flatter curves temporarily if our central case for better than expected data across the course of next week is realised. Signs of a more aggressive Fed would increase the likelihood of short-end forwards being out-delivered, making 2s5s and 2s10s steepener more attractive.

It might seem unfashionable to talk about inflation risk right now. After all, it’s almost back at target across the major economies and lots of central banks have begun to cut rates.

But with monetary policy now becoming looser, in many respects this is precisely the time to be cautious. Money supply growth is already picking up again in the US and the Euro Area. Many of the stickier categories of inflation have been taking longer to fall back. Heightened geopolitical risks mean that commodity price shocks could happen suddenly. And with fiscal policy more constrained by higher real yields, monetary policy is more likely to be the one providing economic stimulus from here.

Given this, we look at why markets should keep inflation on their radar…

…1. Monetary policy is now being eased globally, and money supply growth is picking up again…

…2. Stickier and more persistent categories have been the ones pushing up inflation…

3. Geopolitical shocks still have the potential to push up inflation via commodity prices…

4. Tighter constraints on fiscal policy like higher real yields mean that monetary policy is now more likely to provide economic stimulus when required…

… Steven Zeng with a chart showing the biggest inversion between FF1 and FF12 futures in 36 years, at -193bps. This suggests the market expects a ~2ppt cut from the Fed over the next 12 months, surpassing the previous peak of -185 bps before the GFC and recent inversions of -99 bps in September 2019 and -95 bps in March 2020. Is this reasonable? Pricing implies a return to neutral policy over the next 12 months, a decent baseline but also one that is likely to adjust with incoming data.

…Chart of the day US core PCE deflator in line with consensus in July

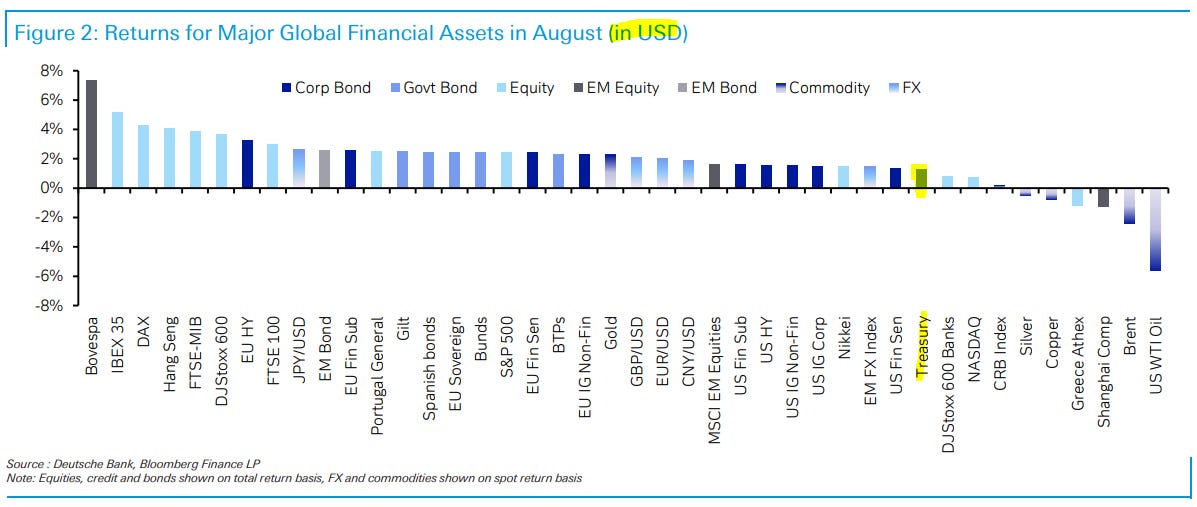

August was an incredibly tumultuous month in financial markets, with the VIX index of volatility briefly spiking to levels last seen in March 2020 during the Covid-19 market turmoil. The catalyst for that was a weak US jobs report, which raised fears that the US might be heading into a downturn. That interacted with an unwinding of the yen carry trade, and there was a massive slump in Japanese markets, with the TOPIX falling by over -12% in a single day on August 5. But calm swiftly returned, after better data and a dovish message from Fed Chair Powell at Jackson Hole helped to reassure investors. So despite everything, most equities and bonds rose in August, with both the S&P 500 and US Treasuries posting a 4th consecutive monthly advance.

… For sovereign bonds there were also gains as investors priced in more rate cuts. US Treasuries were up for a 4th consecutive month for the first time since July 2021, posting a +1.3% gain in total return terms, whilst Euro sovereigns were up +0.4%. Gold (+2.3%) was another beneficiary, since it tends to do well in a lower-rate environment given it doesn’t pay any interest itself, and prices exceeded $2,500/oz for the first time.

Which assets saw the biggest gains in August? Sovereign Bonds: With investors pricing more aggressive rate cuts, it was a strong month for sovereign bonds, and US Treasuries in particular. US Treasuries were up +1.3% over the month, and Euro sovereigns were up +0.4%.

Goldilocks: Global Markets Analyst - Lessons From G10 Cutting Cycles

With most of the G10 either having just begun or about to begin cutting policy rates, we look at the return potential of a variety of rates investment strategies during G10 cutting cycles over the last three decades to understand how to position once cuts begin

We find that outright longs generate the highest leveraged returns during cutting cycles of all types, with the 2y point consistently on average best for both total and vol-adjusted returns. 2s10s steepeners offer the best volatility-adjusted returns among curve formats. Most of the returns to longs and steepeners are generated in the months into and immediately following the initial cut.

At current levels of front-end inversion, such as 1y1y vs 1y, it would be unprecedented to generate significant positive returns to long positions in the absence of a recession. And although non-recessionary returns to steepeners are mixed, the initial flatness of the curve suggests the risk / reward to steepener positions is likely to be better.

Policy Priorities Diverge Ahead of key US data next week, signals out of the US have furthered the post-July NFP theme. Incremental inflation news has reinforced the shift in Fed focus towards the labor market, but there has been little on the activity side in recent weeks to clearly argue for heightened urgency in sizing upcoming rate adjustments. We think current pricing and the Fed’s aversion to additional labor market weakening sets up some asymmetry around the August jobs report, with a larger move in both rate level and curve likely in the event of a downside surprise. While US rates volatility appears somewhat rich and the start of cuts tends to present a good opportunity for vol selling, election uncertainty argues for waiting a bit before attempting to monetize the vol premium. The ongoing drift lower in European inflation and inflation pricing has left real rates largely unchanged despite the fall in nominal yields in recent weeks. The ECB’s still-entrenched focus on upside inflation risks—reiterated by Board member Schnabel this week—has compounded this, but we view it as an opportunity to receive. With growth data unconvincing, we continue to think the market underprices the risk of faster 2025 cuts. In the UK, growth data is reinforcing the BoE’s cautious tone—we expect two cuts this year and instead prefer long 30y Gilts through the upcoming budget and QT announcement. While the slow moderation in Australian inflation has challenged the RBA’s ability to pivot focus towards weaker growth, we expect that shift to eventually happen and see additional scope for longer-term AUD yields to catch down to global peers.

United States Payrolls to bring a resolution to the holding pattern, with asymmetric risks. US yields have remained within the broader August range despite a now consistent post-July NFP theme of signs of resilience in US activity data. We expect next Friday’s payrolls release to bring some resolution to the relative stasis, though risks to US yields are likely asymmetric given current pricing, which implies around 31bp of cuts for September and 100bp by year-end. If the report confirms or is slightly stronger than our economists’ priors that the July data somewhat overstated the extent of weakening, revealing job growth more consistent with their 160k estimate of the underlying pace of job growth (and some reversal in the rise in the unemployment rate), we expect market pricing will gravitate towards 25bp for September, with scope for incremental steepening in subsequent meeting gaps. The Fed’s stronger emphasis on avoiding further weakening in the labor market raises the bar to a more significant removal of the downside risk premium to a sequence of 25bp cuts on just a month’s worth of data. We think yields can move higher over time, but as we showed last week, the reversal in yields following a growth scare typically plays out over several months and requires the avoidance of additional material worries. Conversely, the Fed’s aversion to additional cooling suggests that even a modest miss could be sufficient for the market to quickly price in a high probability of a 50bp move in September, with increased risk of a series of larger moves to a lower implied terminal rate. While an in line or modestly firmer outcome could see some curve flattening, recent behavior has seen longer maturities move with a higher beta to the front-end in selloffs than in rallies (Exhibit 1). We ultimately think curve flattening risk should be comparatively limited versus the extent of steepening likely if there is cause for greater concern about a more evident softening; given this we continue to favor a steepening bias, with the 2s5s curve segment still comparatively flat versus the rest of the curve.

Fed and election uncertainties create opportunities to fade vol premium once easing cycle begins …

MS Sunday Start | What's Next in Global Macro: Happy "Labor" Day

The sharp correction in stocks in July/early August was due to several factors, with the most important one being softer-than-expected economic growth data that culminated in a weak employment report on August 2. In particular, the 0.2pp increase in the unemployment rate is what triggered the Sahm Rule and caused markets to worry again about a hard landing. Since then, we have received some better economic data led by jobless claims, retail sales and the ISM non-manufacturing survey (though some data have been softer, too). As a result, many equity market indices have rallied back to near all-time highs, while the bond market, yen and commodities reflect lingering suspicions that the coast might not be clear. Even equity market “internals” like cyclical versus defensive stocks have failed to rebound much at all (Exhibit 1), while lower-beta stocks continue to show very resilient performance amid the mixed data on both the macro and micro fronts…

The true test will likely come with the August jobs report on September 6. A stronger-than-expected payroll number and lower unemployment rate would likely provide markets with greater confidence that growth risks have subsided, paving the way for equity valuations to remain elevated and a potential catch-up in some other markets/stocks that have lagged. Conversely, another weak report and a further rise in the unemployment rate would likely rekindle growth fears and pressure equity valuations like last month. Our economists are looking for a better-than-expected non-farm payroll number of +185k and a fall in the unemployment rate to 4.2% (which is in line with consensus).

The challenge for US equity investors is that markets already appear to be pricing in a soft landing. At 21x earnings, the S&P 500 is trading around the top decile of its historical valuation range. This is also based on consensus EPS numbers that assume 11% growth this year and 15% growth next year, well above the longer-term average of 7%. In short, I see limited upside at the index level on a 6-12-month horizon in a soft landing (our base case view) given where valuations and earnings expectations are. Conversely, in a hard landing (our bear case), there is material downside risk given well above-average valuations – i.e., there appears to be a lot riding on the upcoming labor report for equity investors…

…Finally, the big driver of US equities over the past year and a half has been the artificial intelligence theme. However, many AI winners have recently corrected by 20-40% as earnings results did not match the lofty expectations priced into stocks…

… In short, unless the Fed cuts more than the market is already expecting, the economy strengthens, and/or additional forms of policy stimulus are introduced, equity investors should expect minimal returns at the index level over the next 6-12 months and should remain up the quality curve, in our view…

We expect Friday's jobs report to set the tone for near-term price action. A strong payroll number and fall in the unemployment rate would likely pave the way for equity valuations to remain elevated, while another weak report would likely rekindle growth fears and compress valuations broadly.

… In short, unless the Fed cuts more than the market is already expecting, the economy strengthens, and/or additional forms of policy stimulus are introduced (ending QT earlier than expected, draining the RRP and/or TGA, etc.) equity investors should expect minimal returns at the index level over the next 6-12 months and should remain up the quality curve, in our view. Friday is a big day, and as usual, it may not be so much about the data itself, but how markets react to it. Happy Labor Day.

September is about to begin with a series of key data that will enable the market to fine tune its rate cut pricing. As central banks aim to ease their monetary policy stance preemptively, there is no reason to rush into aggressive rate cuts. However, they do have room to react forcefully to any contractionary shock. At this stage of the cycle, owning bonds is thus like being long volatility. In the near term, we prefer steepeners, as seasonal issuance is hitting the markets…

…United States Priced to perfection With nine 25bp rate cuts priced in by end-2025, the market is expecting a more conventional easing cycle, with fed funds reaching a terminal rate of 3% next year. With an asymmetric bias toward more cuts, it is hard to fade the market pricing of cuts, although there is little in the data to justify the need for the Fed to cut rates aggressively. With Chair Powell seemingly confident that inflation is “on a sustainable path back to 2%”, the focus is on next week’s payroll report, with a weak print increasing the probability of a 50bp cut at the September meeting, although that is not our base case. With the 2yT yield near the lows for the year, we do not see much more room for front-end yields to decline. Hence, yield curve steepening is also likely to stall until the Fed begins to cut. We expect the 10yT yield to remain in the 3.75-4% range until the US elections in November. In this context, we are neutral on duration but continue to recommend curve steepeners, as long-end yields could rise when the Fed cuts rates and we get past key risk events like the November elections. Swap spreads have declined considerably since April. There are signs that this decline may soon end, and long-end spreads started to widen in August. But with daunting fiscal deficits, it is difficult to take a strong widening view…

… ➔ We think the market is overpricing cuts, but it is hard to fade this move, as the risks are skewed towards more easing if the data disappoint. That said, we continue to expect the Fed to adopt a more gradual approach to easing, one that is based on incoming data. Thus far, there is little information in the data to justify the need for aggressive cuts…

… ➔ With the 2yT yield near the lows for the year, we do not see much more room for front-end yields to decline. Hence, the yield curve steepening is likely to stall until the Fed begins to cut rates. We expect the 10yT yield to remain in the 3.75-4% range until the November elections. In this context, we are neutral on duration but continue to recommend curve steepeners, as long-end yields could rise when the Fed cuts rates and we get past key risk events like the elections in November.

…Fixed income August was a positive month for fixed income investors, with gains across the asset class. Further indications that the Fed is poised to cut rates at its September meeting —with the possibility of a 50-basis-point easing—drove a 1.3% return from the Bloomberg US Treasury Index. The yield on the 10-year US Treasury fell from 4.10% at the start of the month to 3.91% at the end. US investment grade credit returned 1.6%, for a 3.5% gain so far this year. The Bloomberg Pan-European Average gained 0.7%.

Our view: We shifted our view on fixed income from Most Preferred to Neutral in August. Within the asset class, we also moved high grade (government) bonds from Most Preferred to Neutral. Following the 90-basis-point fall in the 10-year US Treasury yield since April, we see more limited scope for capital gains over our forecast horizon if a softlanding scenario continues to play out. We expect the 10- year Treasury yield to end the year around 3.85% in our base case, though we note that in an adverse economic scenario, it would likely decline sharply. We maintain our preference for investment grade corporate credit, where we believe yields remain attractive. We still recommend that investors shift excess cash into quality fixed income given the potential for cash rates to fall quickly as the global rate-cutting cycle advances. Investors can also consider diversified fixed income strategies—including selective exposure to higheryielding parts of the asset class—as a way of further enhancing portfolio income.

The shortened week ahead is an important one for labor market indicators. We expect them to show that August's employment continued to grow at a solid pace, and better than July's pace, which was weakened by bad weather. That should lift bond yields, the dollar, and cyclical sectors of the S&P 500. Here's more:

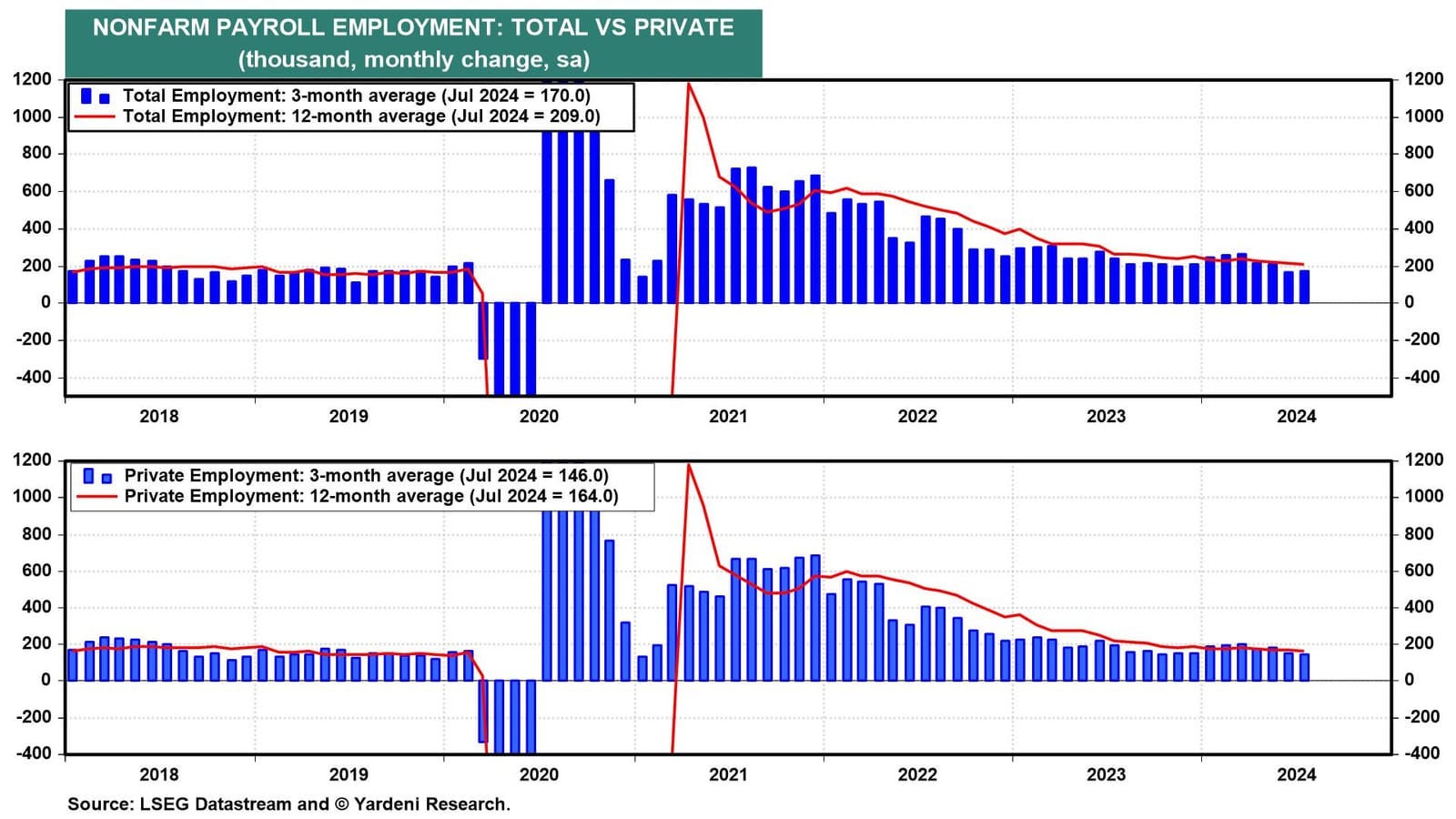

(1) Employment. August's employment report (Fri) should show payrolls rose by 200,000-225,000 to another record high and that the average workweek rebounded from July's weather-depressed reading. In any event, the average monthly increases recently suggest that the labor market has normalized back to its pre-pandemic average of roughly 170,000 per month (chart).

We expect the unemployment rate slipped to 4.2% in August from 4.3% in July, which we think was partly boosted by bad weather as evidenced by initial unemployment claims, which rose in July and eased in August.

Lacy Hunt mentioned the “long tentacles” of payrolls revisions on other upstream economic indicators.

Some of them I identified are: personal income (lower), which also means saving rate (lower), GDI (lower). Ultimately, GDP (lower).

There is this myth that GDI always get revised toward GDP. It is a myth, because turns out that GDI leads GDP in turning points of the economy (per BEA and Fed research). And GDP tends to get revised toward GDI in lead up to and during recessions…though obvious only several years later.

The discrepancy is GDP and GDI also turns out to be predictive of unemployment rate in the lead up to cyclical peaks.

Finally, why does GDI have these superior features over GDP at cyclical turning points?

You guess it…it is likely firm birth and death again!

GDI picks up the firm and death because it uses QCEW as source data…while GDP probably has non sampling data bias during these period.

This Fed paper by Jeremy Newaik has the most thorough treatment of the GDI and GDP differential that I’ve read. The former being superior during 2006-2008.

Bottomline: why do I have to spend my Friday night writing about this rather reading a nice book? I’d rather not. But people on this app put too much signal on GDP, particularly in today’s economic environment. Research would say to put more weight on GDI in turning points.

Bloomberg: Ueda Reiterates That BOJ Will Lift Rates If Outlook Realized

…Historic Divergence in Long-Term Inflation Expectations According to the recent University of Michigan Consumer Survey data, the average US consumer believes that inflation will be 6.1% over the next five to ten years. The Treasury Inflation Protected Securities (TIPS) market on the other hand indicates that CPI will be only 2.1% during that time as we show in the chart below. This shows that consumers likely do not believe that government CPI statistics reflect true inflation. Such a sentiment is understandable. We think the recent historic divergence between these two time series is a measure of government mistrust. So, if the Fed is claiming victory over long-term inflation expectations based on the TIPS market alone, we believe they have a lot more work to do. Furthermore, since the Fed has just signaled a green light for interest rate cuts we expect consumers to remain skeptical that the Fed truly has inflation under control.

… Finally, true story and a question posed here on this side …

… AND, inspired by TBP, i’ll present a video clip from SNL for your review and consideration …

1973 … think ‘bout that and as you do … THAT is all for now. I’m Off to the day job …

GDI vs GDP.... excellent thoughts

Like the SNL video.....

Politicians....ugh...