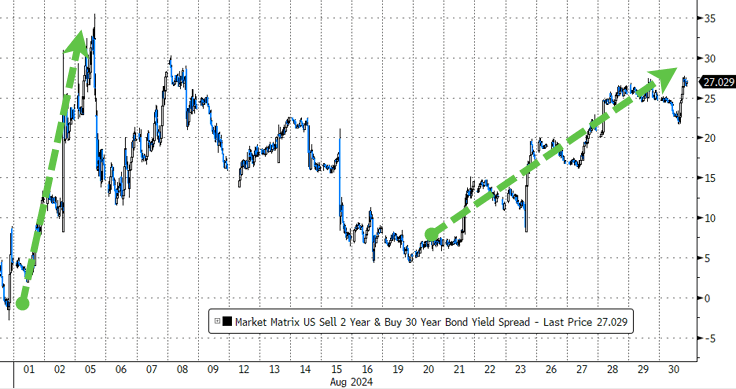

weekly observations (09.03.24): calm before NFP, staying with steepeners, getting short 2s IF and stayin' short 10s; 'Fed Pivots and Baby Aspirin' and oh, just 'throw the stick' ...

Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

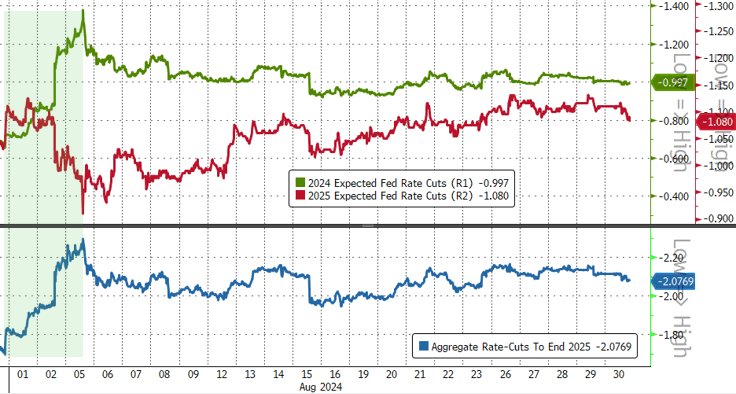

As we turn the page on August and look ahead to the beginning of the school year and end of the calendar year, rate CUT expectations and hopes continue to run pretty high.

We aren’t gonna get the 7 cuts priced as the page turned to 2024 and now we’re going to have to settle for 3 or maybe 4 (so it would seem size DOES actually matter, then? asking for a friend) …

Some will celebrate.

Others will cry foul play.

And yet others will note on this day in 2012, Bernanke (re)introduced concept of … the portfolio balance channel in JHOLE

…One mechanism through which such purchases are believed to affect the economy is the so-called portfolio balance channel, which is based on the ideas of a number of well-known monetary economists, including James Tobin, Milton Friedman, Franco Modigliani, Karl Brunner, and Allan Meltzer. The key premise underlying this channel is that, for a variety of reasons, different classes of financial assets are not perfect substitutes in investors’ portfolios.4 For example, some institutional investors face regulatory restrictions on the types of securities they can hold, retail investors may be reluctant to hold certain types of assets because of high transactions or information costs, and some assets have risk characteristics that are difficult or costly to hedge.

Imperfect substitutability of assets implies that changes in the supplies of various assets available to private investors may affect the prices and yields of those assets. Thus, Federal Reserve purchases of mortgage-backed securities (MBS), for example, should raise the prices and lower the yields of those securities; moreover, as investors rebalance their portfolios by replacing the MBS sold to the Federal Reserve with other assets, the prices of the assets they buy should rise and their yields decline as well. Declining yields and rising asset prices ease overall financial conditions and stimulate economic activity through channels similar to those for conventional monetary policy.Following this logic, Tobin suggested that purchases of longer-term securities by the Federal Reserve during the Great Depression could have helped the U.S. economy recover despite the fact that short-term rates were close to zero, and Friedman argued for large-scale purchases of long-term bonds by the Bank of Japan to help overcome Japan’s deflationary trap.5 …

I honestly don’t care and we’ll likely learn from COVID and the Transitorians (early like Greenspan was with irrational exuberance remarks?) and I will continue on my way, lookin’ for whatever / where ever may be the ‘fat pitch’ or, as it is football season, an effective counter …

It is with that in mind, I’ll lean on one part TECHNICALS

30yy DAILY: support up nearer 4.32 (recent cheaps) and 4.40 (TLINE)

…notice the recent cheapening has been accompanied by a crossing and move in stochastics and so, ‘becoming overSOLD’ which then might very well mean a DipOrtunity…?

First up, setting the table ahead of 4pm being the new 3pm and month-end extensions and portfolio window dressing that goes on …

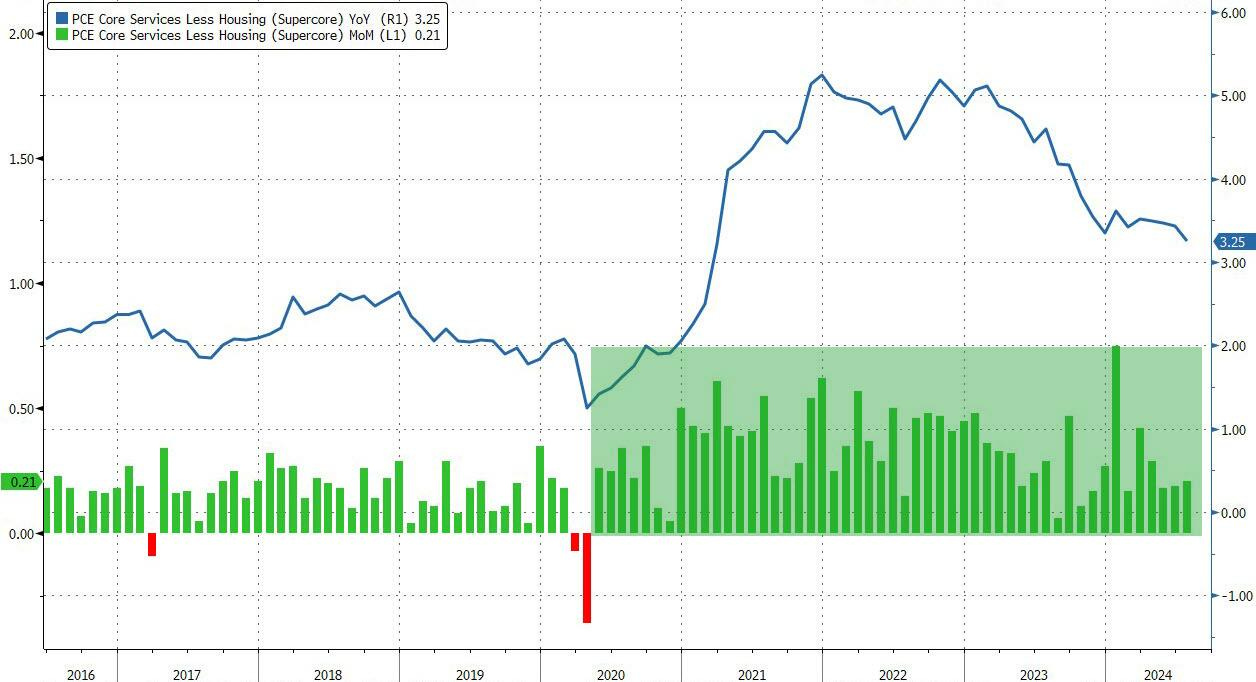

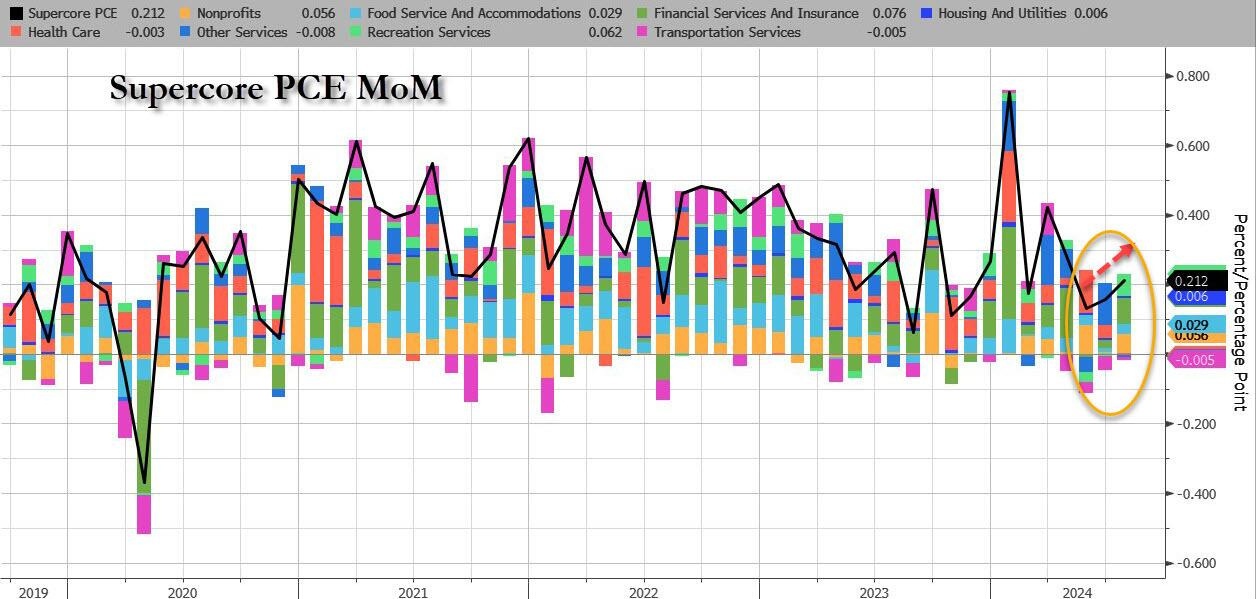

ZH: Fed's Favorite Inflation Indicator Unexpectedly Prints Soft As Savings Rate Plunges To Multiyear Low

The broadly weak trend of US macro data was jolted yesterday by the hotter than expected GDP print (hilariously driven by a surge in personal consumption at the same time as Dollar General announced the time of death of the US consumer), which prompted a hawkish shift in rate-cut expectations. However, this morning, the doves get another chance for some 'bad news' (disinflation) to support their 'we must cut in September" narrative, unveiled by Powell himself last week during Jackson Hole, when the Fed's favorite inflation indicator - Core PCE - came in line with expectations, and even missed estimates on a core YoY basis…

… Even more notably, the so-called SuperCore PCE rose 0.2% MoM, the highest in 3 months, and which pushed YoY supecore to 3.25%, which remains awkwardly stagnant at elevated levels...

… This was the 51st straight monthly rise in SuperCore prices with virtually all costs except transportation rising …

… hmmm, ‘bout that concept of transitory, again? Nevermind, lets get back to how the day and month then ENDED …

ZH: Stocks End August Flat After Early Collapse; Bonds & Gold Soar On Rate-Cut Hopes

… ...but August really spooked the markets (after payrolls - recession concerns), sparking a bloodbath in stocks to start the month, stocks (broadly speaking) rallied back to unchanged-ish on the month (flat-ish on the week and the day) with the S&P 500 leading the month while Small Caps lagged...

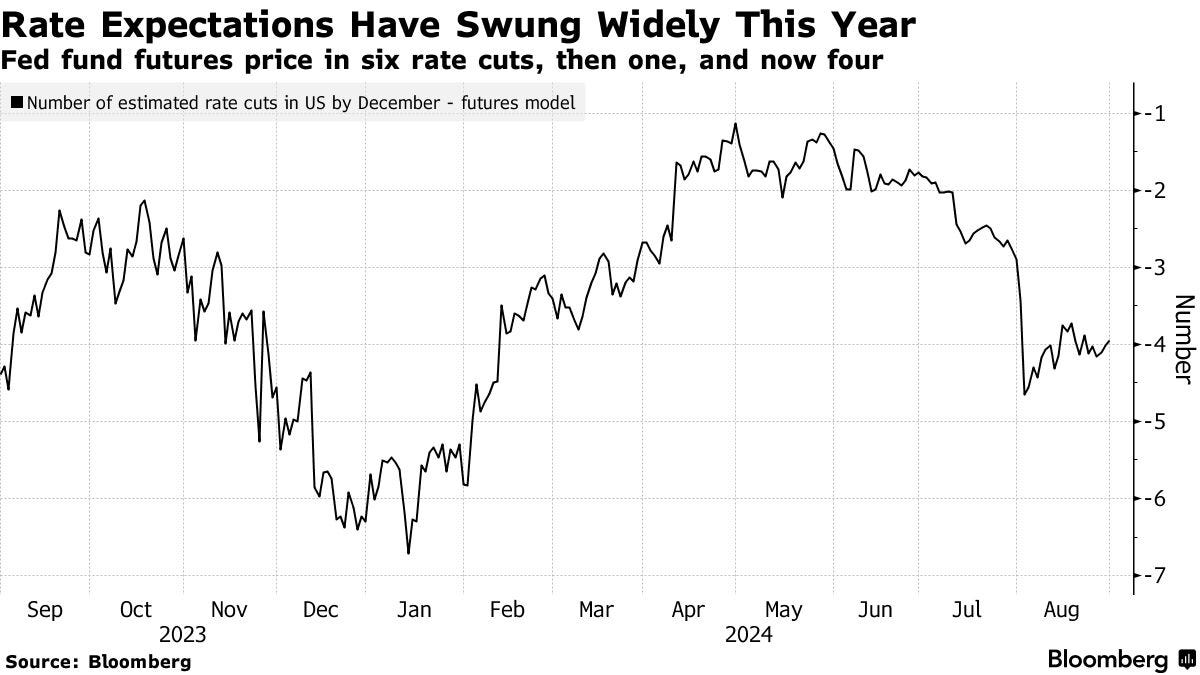

… Rate-cut expectations rose on the month - mostly driven by the early month panic...

Source: Bloomberg

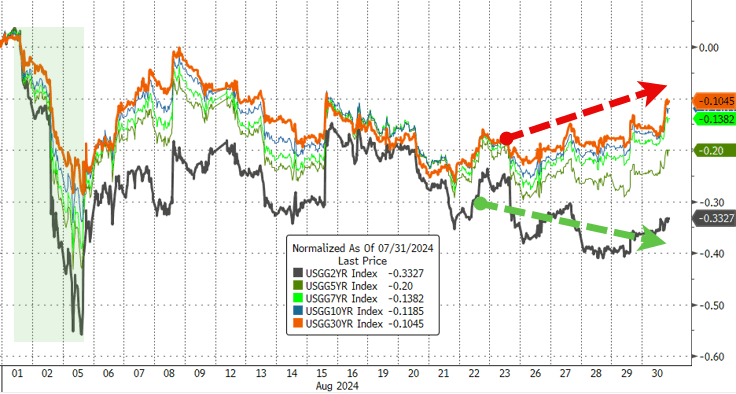

Treasuries were aggressively bid on the month led by the short-end (2Y -33bps)...

Source: Bloomberg

...which steepened the curve significantly (disinverting 2s30s)...

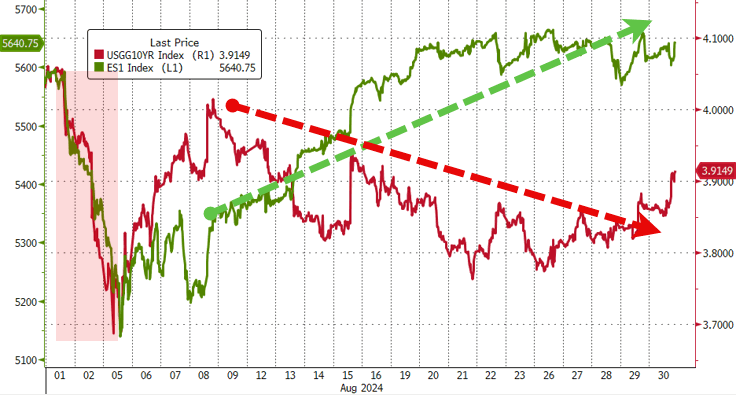

Bonds and stocks disagreed notably on the month and the recession odds...

… AND you get the point…NEXT lets deal with the reason many of you may be here … some WEEKLY NARRATIVES — SOME of THE VIEWS you might be able to use — and which Global Wall Street are selling HOPING for street cred, publicity and order FLOW … THIS WEEKEND, here a few things which stood out to ME from the inbox (which is arguably lighter than normal due to holidays and so, i’ll attempt to make something outta nuthin) …

After market volatility in response to NVIDIA earnings, the US employment report will be the next crucial milestone. We expect a solid print to cement a 25bp cut by the FOMC on 18 Sep, but a further rise in the unemployment rate could still prompt a 50bp increment. Meanwhile, Europe remains in economic and political limbo.

US Outlook: Your move, labor market The latest consumer spending estimates indicate that the virtuous cycle is intact, supported by strong household income and wealth fundamentals. The July PCE price estimates added to the recent string of benign prints, which should put inflation concerns on the back burner and shift the focus squarely on labor market data.

This week's data show consumer spending remains resilient, and revisions to Q2 data imply strong carryover effects for consumer spending into Q3. Real personal spending posted a 0.4% m/m rise in July, outpacing income gains and pulling the personal saving rate lower, to 2.9%.

As expected, PCE inflation readings appeared tame in July, with core rising 0.16% m/m (2.6% y/y), apace with June's downward revised print. Estimates for April and May were also revised lower, indicating slightly more disinflation in Q2. In all, the recent data suggest the disinflation narrative remains intact and is likely to shift the focus squarely on the upcoming labor market data.

We expect next week's highly anticipated August employment report to show a normalization in the labor market from weather-related distortions in July and firm our expectation of three 25bp rate cuts through year-end. We expect nonfarm payroll employment to strengthen to 175k in August, from 114k in July, and the unemployment rate to decline to 4.2%, unwinding temporary unemployment issues in July. However, we acknowledge risks to our call should the labor market cool more than expected….

BARCAP: PCE inflation on track to 2% target (what of disappearing base effects?)

Core PCE prices rose 0.16% m/m in July, leaving the annual rate unchanged at 2.6%. Estimates for April, May and June were revised modestly lower, indicating slightly more disinflation in Q2. The data suggest inflation is on track to hit the FOMC's 2% target. We maintain our baseline call for three Fed rate cuts this year.

BMOUS Rates Weekly: Solace from Indifference (book profits 2s10s steepener **IF** 1.5bps reached and will look to get short 2s @ 3.75 on disappointing NFP, but only IF UNR remains sub 4.5%)

… With this issue now largely resolved, the current debate regarding whether Powell is late to begin normalizing could soon be complicated by the timing of the Presidential election. While further softening in the employment data might argue for a 50 bp initial cut, Powell would need to weight such a move in the context of appearing to favor the Democrats (i.e. the party currently represented in the White House). Preserving central banking independence will be less of a consideration at the November and December meetings, which means only September's decision involves such political considerations. Ideally for the Committee, the unemployment rate shifts lower and there is solid payrolls growth, ensuring that a 25 bp cut will be the prudent approach. We remain in the 25 bp cut camp with the caveat that such an outcome would need the support of a solid employment update for August …

In the attached Weekly we discuss the signal on the outlook for the economy from newly published profits data, and we provide some thoughts on the inflation and employment data (particularly next Friday’s August jobs report) as we look ahead to the September FOMC meeting.

… We see the evolution of profits as being the driver of the macro economy. Firms (by which we mean owners and CEOs) seek to make profits—this is hardly a controversial point—and in doing so must hire labor and purchase raw materials and invest in capital equipment. When profits are strong, companies invest in the future and are able to use the funds generated by those profits to invest in new capital equipment. However, when profits are squeezed, companies are forced to cut back on investment spending and cut costs, which invariably means laying off workers…

… As a share of the sector’s output, profits rose to 16.3% in the second quarter from 16.2% in the first quarter and from 16.0% a year ago (see the chart below). Recessions have been preceded by a slide in profit margins, which is simply absent in the current environment…

… Next week’s employment report for August will be an important driver of expectations for the September FOMC rate decision. We do not view this week’s data and Fed guidance as supportive of a large rate cut in September. For example, on inflation we got encouraging data on PCE prices, with headline and core prices rising 0.2% in July, which put the three-month annualized inflation rates on these measures below 2%. However, year-over-year inflation rates (on both overall and core prices) were unchanged at around 2½%, which Atlanta Fed President Bostic said this week is “still far” from the Fed objective…

DB: US Fixed Income Weekly (rehash and week in review where they got short 10s)

Bond Market Strategy Late May, we outlined the rationale behind our bias to receive the US front-end. After the significant rally that occurred early August, we argued that such rationale was no longer valid. We now follow suit on the arguments presented earlier this month and enter a short UST10Y (indicative target 4.10%, indicative stop 3.65%)

Our trade is motivated by the following observations…

ING: Fading US inflation keeps the Fed on the path of rate cuts

Inflation is on track to hit the 2% target early next year with the latest PCE deflator print giving the green light to a September rate cut. However, consumer spending remains very robust and this may make the Fed reluctant to move aggressively. Nonetheless, a soft jobs report on 6 September could still tip the odds in favour of a 50bp rate cut

MS: Friday Finish – US Economics: It’s About Labor Markets Now

The Fed is shifting focus toward the labor market. Because we expect slowing but no slump, we think the Fed resets policy lower over time. The still-strong economy and massive uncertainty about all of the “stars” suggest gradualism should carry the day…

… We think that a print around or below 100k next week will clearly put a 50bp cut on the table. And if subsequent inflation data surprise to the downside, meaning that too low inflation is a risk, even only moderately soft jobs data could prompt a bigger cut.

Over the past couple of years, we have written about how different this cycle is from other cycles. We do not think that we are “late cycle” in the sense that the economy is entering a downturn and monetary policy will cut by hundreds and hundreds of basis points to try to re-stimulate the economy. Rather, as in other “mid-cycle corrections,” the goal is to adjust the level of the stance of policy, feeling the way to the setting that will allow the economic expansion to go on … and on.

Wells Fargo: Cooling Inflation in July Amid Sustained Consumer Spending

Summary Spending still outpaced income in July, setting up for a decent Q3, and inflation continued to cool. With the 3-month annualized rate of core PCE inflation back below the Fed's 2.0% target, the case for "higher-for-longer" is not a compelling one.

…Argument for Restrictive Policy Looks Weaker Yesterday's GDP report already showed that consumer spending was stronger in the second quarter than first reported; today's personal income and spending report reveals July data and shows that the third quarter is off to a compelling start…

… Topic of the Week: That Chill in the Air Means College Football Is Upon Us

Summer is winding down and fall is just around the corner. Before the leaves change color, temperatures dip and pumpkin spice finds its way into everything, what better way to mark the transition into autumn than to dive deep into the college football season and the regional economies the top teams call home?

Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW

AllStarCharts: The Future of Bonds: Intermarket Insights

… In this kind of late-cycle environment, it is ordinary for the yield curve to come out of inversion as interest rates come down.

Apollo: Quantifying What Fed Cuts Mean for GDP and Inflation

…The bottom line is that the r-star framework is missing what “normalizing interest rates” means for the economy, and this is particularly problematic when the Fed funds rate is significantly higher than the model-calculated terminal policy rate.

Bloomberg: Once-In-Lifetime Wall Street Rally Raises Soft-Landing Stakes

Dovish Fed helps markets bounce back from early-August rout

Data on jobs, manufacturing will test faith of economic bulls

… For a sense of the tenuousness, consider the path of rate cuts priced in Fed fund futures. Back in January, when inflation fears ebbed, bond traders wagered on roughly six rate reductions for all of 2024, with the first one arriving as early as March. When inflation proved stickier than forecast, those bets were pared and by April, only one cut was expected.

Now the consensus is, the Fed will kick off its easing cycle next month, with four quarter-point reductions by December.

“The reality is both the Fed’s own guess in the dot plot and the market’s expectations are always wrong,” said James St. Aubin, chief investment officer at Ocean Park Asset Management. “I could see easily three cuts this year. Four might sound pretty extreme. It would probably only happen if the economy was really in bad shape.”…

EPB Research: A Coincident Indicator of the Labor Market

Rather than a single-factor analysis of the labor market, the EPB Coincident Employment Index provides a more robust and objective reading on the employment situation.

Hedgopia CoT: Peek Into Future Through Futures, How Hedge Funds Are Positioned (specs less short)

HUSSMAN: Fed Pivots and Baby Aspirin (i’m a sucker for L/T charts and so …)

…Treasury bonds, precious metals, and diversifying with a value-conscious, historically-informed, full-cycle discipline

In the fixed income market, we continue to view the yield on 10-year Treasury bonds as acceptable though slightly inadequate, relative to systematic benchmarks that have historically been useful in assessing the likely return/risk profile of bonds. The chart below updates this comparison. The total return of 10-year Treasuries has slightly lagged T-bills year-to-date, but they’ve outperformed T-bills since the pop in yields we observed in October 2023, when I noted that we were “finally inclined to nibble on longer maturity debt.”

But wait. Doesn’t an expected Fed pivot make long-term bonds much more attractive? Well, we can ask this question: what is the median change in the 10-year Treasury yield in the first 12 months following a Fed pivot, in a rate-cutting cycle that takes the Fed funds rate at least 150 basis points lower? The answer is zero. The largest outliers were the 1984 pivot, the first few months of the 1980 pivot, and the roller coaster that followed the 1981 pivot, which saw Treasury yields spike initially, but eventually decline by over 2% two years later. All three of these outliers started at an initial 10-year Treasury yield of about 12%. For now, with the 10-year bond yield at 3.86%, I do believe “acceptable though slightly inadequate” is the best description I can offer, despite the prospect for lower short-term interest rates.

In our own investment discipline, we generally accept risk in bonds based on the adequacy of the yields that they provide. The chart below shows the importance of yield adequacy in navigating bonds, and reflects the benchmarks shown earlier in this section.

Yahoo: A key inflation metric is back to trending below the Fed’s 2% target

… The core Personal Consumption Expenditures index showed July’s prices (excluding volatile food and energy) rose 0.2% from the prior month, in line with expectations.

With that metric confirmed, a very important thing has happened: The Fed’s preferred inflation gauge is back to trending below 2%, the Fed’s target and holy grail of the past two years.

As our Chart of the Week illustrates, the past three months of data on an annualized basis puts the key metric at just 1.8%. Since the inflation crisis began, we’ve been here twice before, in August and December of last year. But with the labor market showing healthy cooling, there’s reason to believe that this time is different.

WolfST: Our Drunken Sailors Are at it Again, Not at All in the Mood for a Slowdown or a Recession

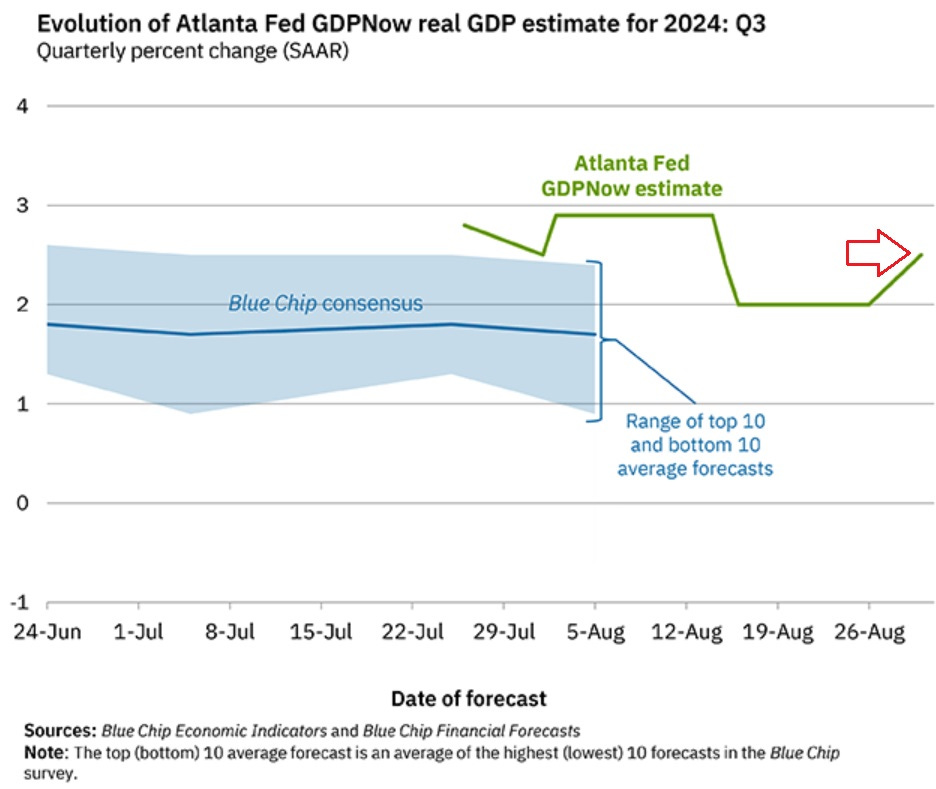

Inflation-adjusted consumer spending jumped. They splurged on durable goods. And still saved some. In response, the Atlanta Fed’s GDPNow jumped.

… What was particularly fascinating was the inflation-adjusted surge in spending on durable goods over the past three months, where a slowdown had taken place earlier in the year. But starting in May, our Drunken Sailors, as we’ve come to call them lovingly and facetiously, returned to the punch bowl.

Upon the release of this data, the Atlanta Fed’s GDPNow, which attempts to estimate Q3 growth of real GDP, jumped to 2.5% growth, up from 2.0%. The 10-year average real GDP growth for the US is about 2.0%.

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

Finally, while I spent so much time detailing various random sellside research or thinking about cuts and 2012 JHOLE, most regular people are looking ahead TO the long weekend like …

… And so, I’ll just throw the stick and wish you and yours a very happy and safe holidays … THAT is all for now …

")

")

")

https://www.zerohedge.com/political/kamala-going-drive-gold-10000

I think I have just confirmed my strategy, if the Communists take over, in November.

Sell most of my stock holdings and go to Gold or GLD.

I will be shocked, if the BLS lets the payroll number get below 100k.

I am more interested in what the Household Survey comes in at..

What a year that Aaron Judge is having!!

Wish I could Invest, like he Swings the Bat.

Thanks for your work..