while WE slept: USTs flat ahead of HH2.0; brace for $1tril UST supply; "little bear market" (10s, BG); "Pricing of cuts under the next Fed chair has shifted materially" (DB); #TariffInflation ??

ZH: Solid 2Y Auction Stop Through Despite Weak Foreign Demand

... question now becomes if you should … or want to … #Got5s? Some context and levels …

5yy DAILY: 4.00% (TLINE) all way down to 3.50% … 55dMA 3.988, 200dMA 4.063

… momentum has become stretched and that makes sense, given some dovish / rate CUTS related commentary past few days but facts / prices / technicals remain a focus … we’re just below bullish TLINE reacting to price of OIL and cut HOPES and support just above at 200dMA (4.063) … mentioned as that level was an inflection point yesterday for 10s …

“The decline was broad-based across components, with consumers’ assessments of the present situation and their expectations for the future both contributing to the deterioration.

Consumers were less positive about current business conditions than May.

Their appraisal of current job availability weakened for the sixth consecutive month but remained in positive territory, in line with the still-solid labor market.

The three components of the Expectations Index—business conditions, employment prospects, and future income—all weakened.

Consumers were more pessimistic about business conditions and job availability over the next six months, and optimism about future income prospects eroded slightly.”

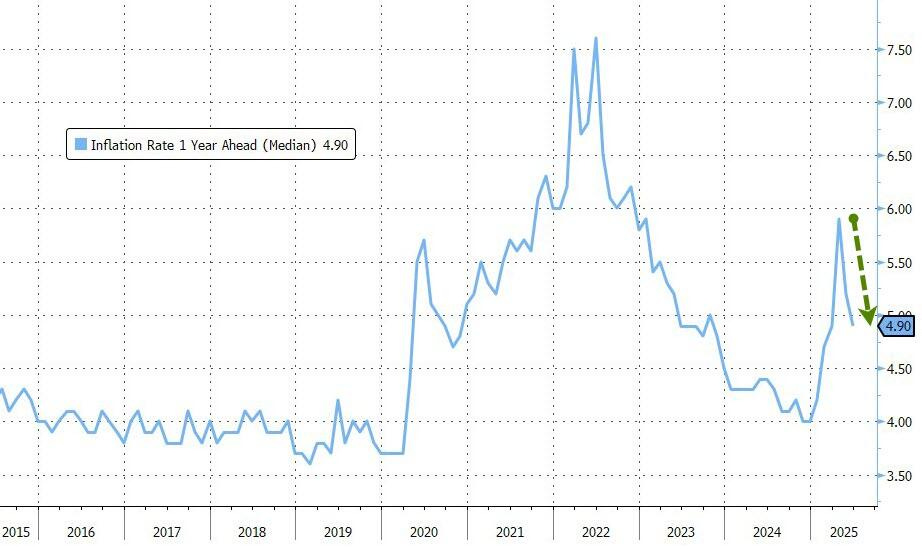

The Conference Board's Inflation Expectation index tumbled, leaving UMich alone in its partisan pathology...

Source: Bloomberg

Guichard added that:

"Tariffs remained on top of consumers’ minds and were frequently associated with concerns about their negative impacts on the economy and prices."

"Inflation and high prices were another important concern cited by consumers in June. However, there were a few more mentions of easing inflation compared to last month."

BOOOO … confidence … except that poor confidence = lower rates = yay, lower rates, housing affordability will increase … maybe? Oh, forget it. I give up. HH day 2 just ahead but first … here is a snapshot OF USTs as of 649a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: ES flat and DXY firmer into Powell Part 2, NATO summit and US supply in focus … USTs await Powell part 2 and details from the NATO summit; Bunds are pressured and currently towards session lows … USTs are essentially flat, but still remain at elevated levels following Fed Chair Powell's commentary in the prior session, where he said “many paths are possible” when questioned on a July cut. Do note that the Fed Chair is due to speak later today also. Elsewhere, data docket is fairly light so focus will be on the 5yr auction, which follows a robust 2yr outing on Tuesday. USTs are currently just off the upper-end of a 111-17+ to 111-23+ band and 1+ ticks above Tuesday’s best.

The bond market is bracing for up to $1 trillion of additional U.S. Treasuries supply in the second half of the year, likely focused in the short end, once lawmakers address the looming debt ceiling problem, possibly permanently, top rates strategists said on Tuesday. (RTRS)

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

Interesting to see Global Wall comin’ around to this way of thinking … wondering if ever MSM will, forcing hand of politico’s in Beltway …

June 25, 2025 ABN AMRO: US Watch - Why tariffs will not unleash the next inflation wave

We evaluate whether the initial tariff-induced inflationary shock could once again transform into a persistent inflation wave.

The trade war could cause supply chain disruptions again, although after the de-escalation this is less likely. Export restrictions remain a threat.

The US is already facing a negative labour supply shock, but it’s mostly absorbed by weaker demand.

The lack of stimulus from the Big beautiful bill is a blessing in disguise, as more demand-inducing spending would be inflationary.

While some circumstances are similar to those that led to the 2020-2022 inflation wave, they represent minor ripples, not the perfect storm.

We highlight two alternative channels that could lead to inflation picking up again.

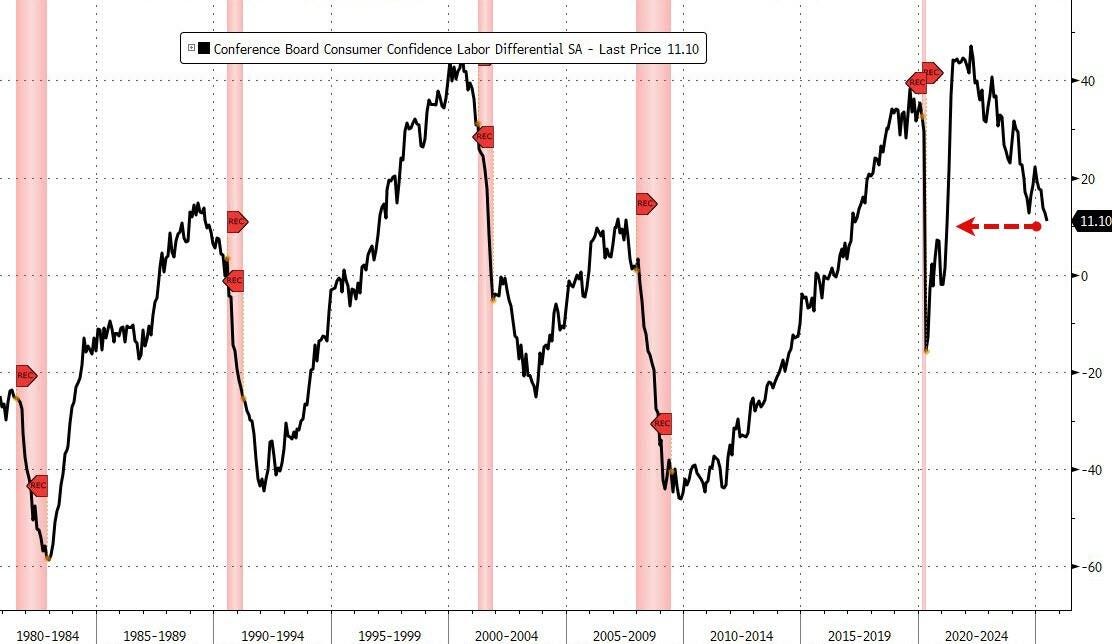

Confidence — the lack thereof — helping USTs …

24 June 2025 Barclays: Consumer confidence declines in June amid broad economic concerns

The Conference Board's consumer confidence index declined 5.4pts in June, to 93.0, reversing course after the jump seen last month. Today's drop reflects broad economic uncertainty partly stemming from geopolitical concerns about Iran, Israel, and the US.

Best in show offering a recap as dust settles on Global Wall from the HH testimony and fragile cease fire … NOTE the firm did engage with 10s30s flattener (tgt 45.8bps with stop at 61bps) …

June 24, 2025 BMO Close: For Hawks and Doves Alike

… Tuesday’s rally in Treasuries occurred against a backdrop of building rate cut conviction and widening concerns about the economic outlook. The move was initially triggered by an unexpected drop in Consumer Confidence, and the slide in the Labor Differential to a 4-year low contributed to the bond-bullish takeaway from the Conference Board report. Powell’s balanced approach and openness to ‘many’ scenarios for the US economy offered fodder for hawks and doves alike, although the most relevant takeaway for near-term monetary policy expectations was the Fed Chief’s indirect pushback against the odds of a rate cut on July 30th, despite his unwillingness to explicitly rule out a move next month. Notably, Powell said, “we should start to see [tariff inflation] over the summer, in the June number and the July number... if we don’t, we are perfectly open to the idea that the pass-through [to consumers] will be less than we think, and if we do that will matter for policy.” The Fed Chief further defended a wait-and-see approach in his comment that, “I don’t think we need to be in any rush because the economy is still strong.”

Powell’s emphasis on the relevance of the summer data suggests that September 17th is a better suited timeline for the resumption of rate cuts given that 3 months’ worth of inflation data is on offer between now and the lateQ3 meeting, compared to just one month of data before July 30th. The market-implied odds of a July cut slipped back below 20% on Tuesday but September cut conviction improved with a 25 bp reduction now fully priced by the next SEP meeting. 2025 cut pricing also firmed, with now 60 bp of cuts priced in by year-end compared to 45 bp in the run-up to last week’s FOMC meeting. Consistent with the recent evolution of the near-term outlook for rate cuts, 2- year yields fell to a multi-week low of 3.80% on Tuesday, bringing a test of 3.75% back onto the radar in the coming sessions.

While the plunge in oil prices, dovish Fed-speak, and an unexpected drop in consumer confidence can all be attributed to today’s rally in Treasuries, we would be remiss to not mention the role that positioning has played in adding to the squeeze further out the curve as 10-year yields broke below the 200-day moving average of 4.300% – a backdrop that helps explain the inability of the curve to steepen despite the boost to rate cut pricing. With 10-year yields reaching as low as 4.283% on Tuesday, 4.25% is the next bullish hurdle in the path toward lower rates, although it will likely take further fundamental justification for sub-4.25% 10-year rates to be durably achieved. With limited tradable information on the docket on Wednesday, the session will offer a litmus test for the near-term sustainability of 10- year yields below the 200-day moving-average of 4.300%.

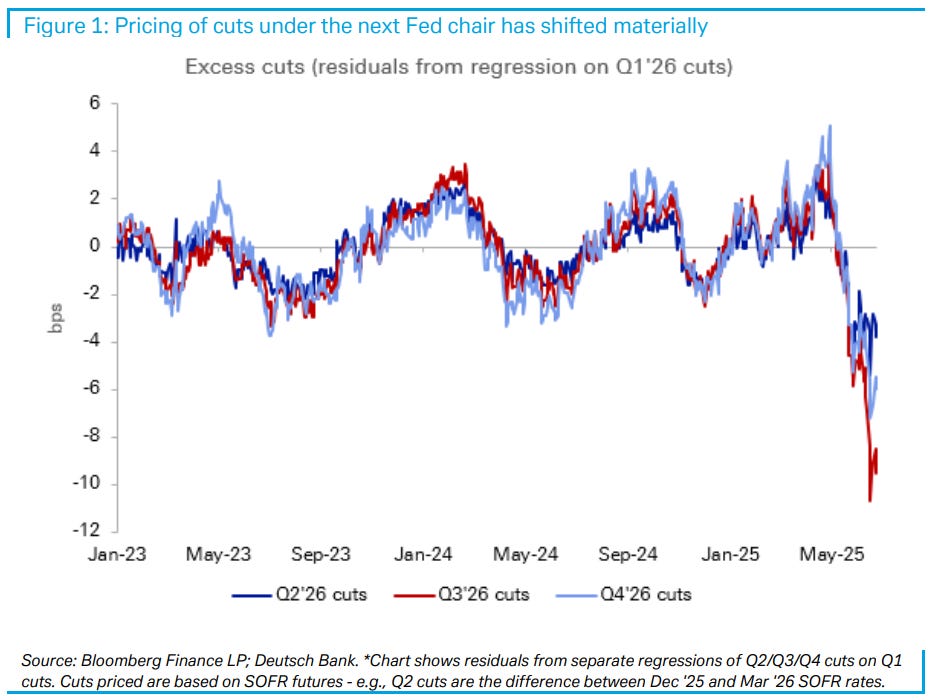

A large German bank out with a note detailing the shape shifting pricing of cuts under the next to be anointed KING of the Fed …

Since last Thursday the market has priced roughly 10bp more Fed rate cuts through year end on the heels of dovish comments from Governors Waller and Bowman and Powell’s testimony this morning. But the more notable shift over the past month is in cuts priced for the middle of next year, as the market seems to increasingly anticipate ongoing easing once the next Fed chair is in place. (Chair Powell’s term expires next May.)

To see this, the chart below shows residuals from regressions of Fed cuts priced for Q2/Q3/Q4 of next year on cuts priced for Q1. These residuals give a sense of the extent to which shifts in cuts at more distant horizons have not been “explained” by shifts in cuts priced for Q1. Over the past month the residuals have gotten significantly more negative, particularly for Q3’26, the period that corresponds to the new chair taking office. That is, the market is pricing an unusual degree of easing under the next chair relative to dynamics that have prevailed in recent years.

As we’ve noted, it takes a majority of the FOMC to set monetary policy and the next Fed chair would need to convince his or her colleagues that a different policy trajectory would be appropriate. This suggests any discontinuity in pricing around the next chair should be slight. (Broadly in line with this, even with the divergence shown below, there are still fewer cuts priced for Q2/Q3/Q4 than for Q1, so what we see is not so much expectation of a stark shift in policy as an expectation that cuts will continue for longer under the new chair than was previously anticipated.)

Fan fav stratEgerist from a large German bank …

24 June 2025 DB: The "Pennsylvania Plan"- Dealing with US Twin Deficits

…Conclusion We have been arguing for the last few months that the US has approached a tipping point in its ability to finance external deficits. In a separate report this week, we discuss what recent developments in the Middle East and the NATO summit are influencing these dynamics. In all, we conclude that in the absence of a willingness to improve the US fiscal position, the political and economic path of least resistance is for the US administration to seek greater funding of its fiscal position via domestic investors. The rest of the world can then engage in an orderly run-down of US duration exposure that will likely be accompanied by a weaker USD, upward pressure on term premium and a persistent pressure on the Fed to stay easy. In sum, all roads lead to a weaker dollar.

Same bank and another fan favored stratEgerist offers an update …

… When it comes to the last 24 hours, near-term inflation fears have rapidly diminished as the ceasefire in the Middle East led to further oil price declines. Indeed, Brent crude was down another -6.07% yesterday to $67.14/bbl, meaning that the two-day decline over Monday and Tuesday is the biggest since March 2022, at -12.82%. It’s also their lowest level since June 10, so just before fears of Israeli strikes against Iran began to surface. This fading geopolitical premium also led to a huge risk-on move across multiple asset classes, with the S&P 500 (+1.11%) seeing its best day in four weeks and closing less than 1% beneath its record high from mid-February. This morning in Asia, US equity futures are flat and oil prices (+1.36%) have edged back up, trading at $68.06/bbl …

… the key reason the market rallied so much was because lower oil prices (and hence lower inflation) are keeping the prospect of rate cuts in play this year. Indeed, futures priced in more rate cuts from the Fed in response, with the amount expected by the December meeting up +4.3bps on the day to 59bps. That’s the most rate cuts priced in six weeks, just before the US-China tariffs were slashed by 115 percentage points, which reassured markets that there wouldn’t be a downturn. This time around, lower inflation rather than growth fears have been the main driver of the repricing, and US Treasuries rallied strongly across the curve as a result. For instance, both the 2yr and 10yr yield hit their lowest level since early May, with the 2yr yield (-3.8bps) down to 3.83%, whilst the 10yr yield (-5.3bps) fell to 4.30%. That said, the decline in yields also gained considerable momentum from the Conference Board’s consumer confidence indicator, which unexpectedly fell to 93.0 in June (vs. 99.8 expected) with the share of responders who said that jobs were plentiful falling to their lowest level since the pandemic.

But even as markets were pricing in a growing chance of a rate cut this year, there was little sign of any rush from Fed Chair Powell in his latest testimony. He reiterated his message from last week’s press conference that they were “well positioned to wait to learn more about the likely course of the economy before considering any adjustments to our policy stance.” Looking forward, he also said that the tariff inflation would be evident in the June and July numbers, so that implicitly leant in favour of waiting until September before any further rate cuts. Meanwhile, Cleveland Fed President Hammack also said that it “may well be the case that policy remains on hold for quite some time”. She also said that “I would rather be slow and move in the right direction than move quickly in the wrong one.” Just after the European close NY Fed Williams' comments were similar to Powell’s with him saying that it was "entirely appropriate" to maintain the current policy stance and that it was still “early days” in terms of the impact of tariffs on inflation. Fed Governor Barr also struck a “wait and see” tone, noting the potential for “some inflation persistence” due to second-round effects.

Nevertheless, those more hawkish comments failed to halt the rally, as the market view was that the deflationary impulse from lower oil prices would bring about quicker rate cuts. So that provided a significant boost to equities on both sides of the Atlantic. The S&P 500 was up +1.11%, and tech stocks led the way as the NASDAQ advanced by a bigger +1.43% while the narrower NASDAQ 100 (+1.53%) reached a new record high.

Same large German bank with a few thoughts on where Earl goes next …

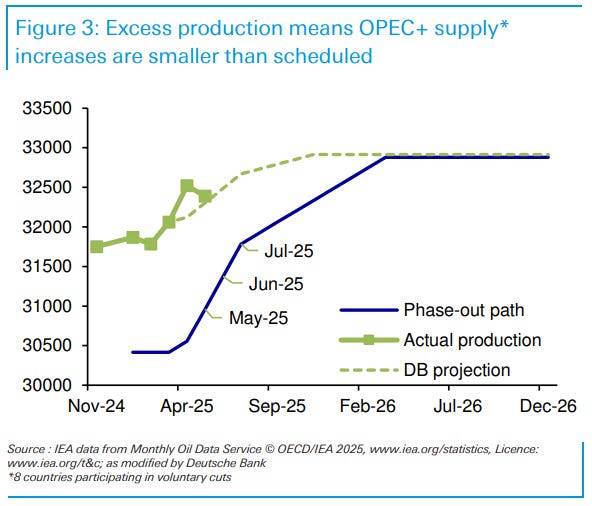

We close the front-end tactical long recommendation from May, which rested on a market under-pricing compared to our model, stronger-than-expected inventory data, and the sanctions-related downside risk to Iranian exports. However, the strategically bearish consensus may not reassert itself until Q4, as we consider fundamentals supportive of Brent at USD 68/bbl in Q3. We illustrate this with two key charts.

We do not expect current events to alter OPEC+ oil ministers' calculus at the upcoming July meeting. OPEC+ rhetoric had already been leaning in favour of continuing the May-July pace of supply increases until the end of the supply schedule. As we outlined earlier this month (Link), that accelerated schedule – if agreed – would fully reverse the eight countries' voluntary cuts by October.

In light of the rapid series of geopolitical developments over the past few days, alternating between escalation and de-escalation, we discuss the serious implications a wider conflict could have for the region, which should continue to support de-escalation efforts. Big questions remain regarding the path back to a diplomatic resolution, which suggests markets may not yet comfortably set this issue aside.

Amsterdam on Humphrey Hawkins, day 1…

24 June 2025 ING: US Fed Chair Powell still in no hurry to lower rates

Fed Chair Jerome Powell is not only coming under pressure from the President to cut interest rates, but from members of his own team. Nonetheless, with the economy still growing and adding jobs, plus the uncertainty over the impact of tariffs on inflation, he suggests the FOMC remains in wait-and-see mode. We think they will wait until 4Q to cut

The market seems to have already moved on from Middle East tensions, with EUR rates now focusing on Germany's fiscal plans. 10y Bund yields briefly hit 2.57%, underperforming gilts and Treasuries, but very long-end yields, in particular, have come under upward pressure

An update on yesterdays HH testimony from across the pond …

24 Jun 2025 NatWEST US: Semiannual Monetary Policy Report to the Congress

As we expected, the Fed released Chairman Powell's prepared remarks in advance (8:30 EST) of his 10am EST testimony before the House Financial Services Committee. However, we didn't learn all that much new, nor did his comments alter our views for the policy outlook…

…Overall, today’s testimony was thoroughly consistent with the June FOMC meeting, so it did not change the policy outlook in our view. Our base case continues to be that the Fed will remain on hold with no cuts this year. Of course, as Chair Powell suggested various scenarios can occur so we wouldn’t rule anything out, but given our view that inflation is likely to move further away from the Fed's objective we still don't show cuts in our forecast profile. See accompanying inflation forecast table below…

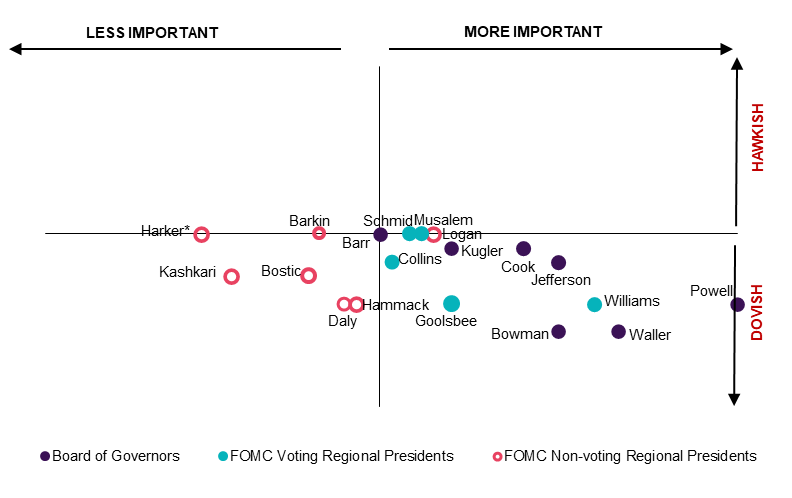

…Fed hawk-dove map (2025) *Harker will retire on June 30, 2025 and be succeeded by Anna Paulson (former research director at the Chicago Fed). Source: NatWest, Federal Reserve

Chair Powell: waiting to see the data Chair Powell's prepared remarks today (see here) hewed closely to the June FOMC meeting materials, including the Summary of Economic Projections and the prepared remarks from his press conference. The overall tone was still consistent with policy being well positioned to wait and see before needing to adjust the stance of policy despite remarks from Board members in recent days hinting at the potential for a July cut: "For the time being, we are well positioned to wait to learn more about the likely course of the economy before considering any adjustments to our policy stance." …

… There just is not a lot the funds rate can do to stop the cost-push inflation. Chair Powell highlighted the importance of keeping longer-run inflation expectations anchored and not letting a one-time price level shift from tariffs become a more persistent threat to price stability. However, even given the inflation outlook, he also said more than once if the labor market weakens, the FOMC could react to that. He said that would be one reason they might lower rates sooner rather than later. He also differentiated between what was happening in parts of the inflation basket, such as the parts unrelated to tariffs that were behaving "well." He touted the progress on inflation generally and services inflation lately…

…July rate cut not ruled out, but Chair emphasized patience …

…Still on track for September rate cut Overall, the Chair to us did not break much new ground and the testimony was consistent with an SEP that seemed to display a lot of tolerance of the tariff related inflation in order to prevent undo labor market weakness or forecast worse growth. We continue to expect the next rate cut comes at the September FOMC meeting. Based on the comments from participants, a sufficiently weak June employment report may motivate a July rate cut, but the Chair seems to prefer to wait a little longer.

In the US yesterday, Federal Reserve Chair Powell delivered a speech to members of the House of Representatives (most of whom are not economists). The main messages were: no rush to cut rates, and trade taxes create uncertainty. This will not surprise markets. There was a further softening of the data dependency mantra, as Powell focused on future inflation as a reason to keep rates unchanged for now. Powell testifies again today.

Financial markets have priced in an Iran-Israel ceasefire holding. That skews the risks if there is any further military activity. Intelligence reports suggesting the US failed to destroy Iran’s nuclear program are unlikely to impact markets directly (investors do not price extreme tail risks), but that failure probably keeps tensions high in the region (which markets do care about).

European defense spending is a focus as the NATO summit continues. In terms of economic effects what matter is not only the scale of European spending, but also the extent to which dependence on US procurement is reduced.

The Democratic primary election for the New York mayor’s race is not a market event directly. It does remind investors of the unreliability of survey/polling evidence.

Confidence — the lack thereof — helping USTs …

June 24, 2025 Wells Fargo: Confidence Slips on Renewed Concern About the Economy

Summary Today's report on consumer confidence is a mixed—but mostly negative—assessment of the mindset of consumers. The 5.4 point decline comes amid renewed concern regarding the labor market and income prospects and about the economy in general. Inflation expectations edged slightly lower.

Same shop, circles up the covered wagons as they discuss the tension in Middle East …

June 24, 2025 Wells Fargo: Middle East Global Economic Impact: Scenario Analysis

Summary Tensions between Israel and Iran escalated sharply on June 13. Tensions spilled over to U.S. intervention with U.S. military targeting three of Iran’s nuclear facilities. Last night, a tentative and fragile ceasefire was agreed to between Israel and Iran. While new confrontation marked a major geopolitical flashpoint in the Middle East and globally, we do not expect any global economic disruptions from the conflict and maintain our view that global growth prospects are improving. Our base case scenario continues to be global economic growth 2.7% for 2025, although alternative geopolitical scenarios could have modest effects on our global GDP forecast.

Finally, from Dr. Bond Vigilante …

Jun 24, 2025 Yardeni: A New Day In The Middle East

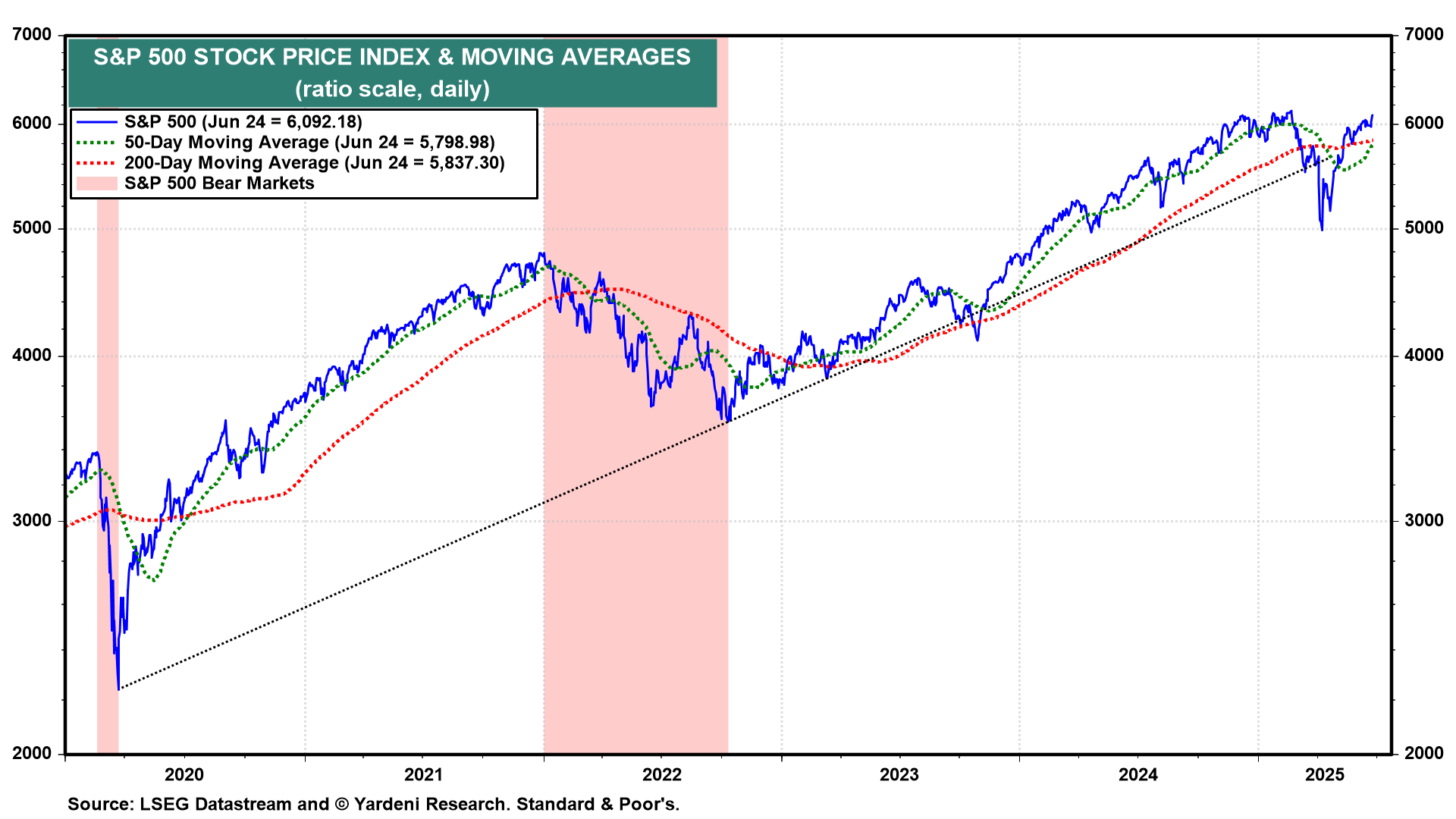

Any day with a ceasefire in the Middle East is a good day for stocks. On Monday, President Donald Trump declared that the "12-Day War" between Israel and Iran is over. The S&P 500 rose 2.1% yesterday and today on that news to 6092.18 (chart). That's only 0.9% below the February 19 record high of 6144.15. The market rose even though both Israel and Iran today accused each other of violating the ceasefire brokered by Trump, who angrily responded by dropping an F-bomb on both countries: "We basically have two countries that have been fighting so long and so hard that they don’t know what the f*** they’re doing."

The White House also went ballistic over news reports that US missile strikes did not completely destroy Iran's key nuclear sites, based on an initial assessment by the US Defense Intelligence Agency. White House Press Secretary Karoline Leavitt told NBC News in a statement that the "alleged assessment is flat-out wrong ...” and "a clear attempt to demean President Trump, and discredit the brave fighter pilots who conducted a perfectly executed mission to obliterate Iran’s nuclear program."

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

Positions matter (see BMO just above) and once again, I’d suggest a point and a click up of EBBs latest …

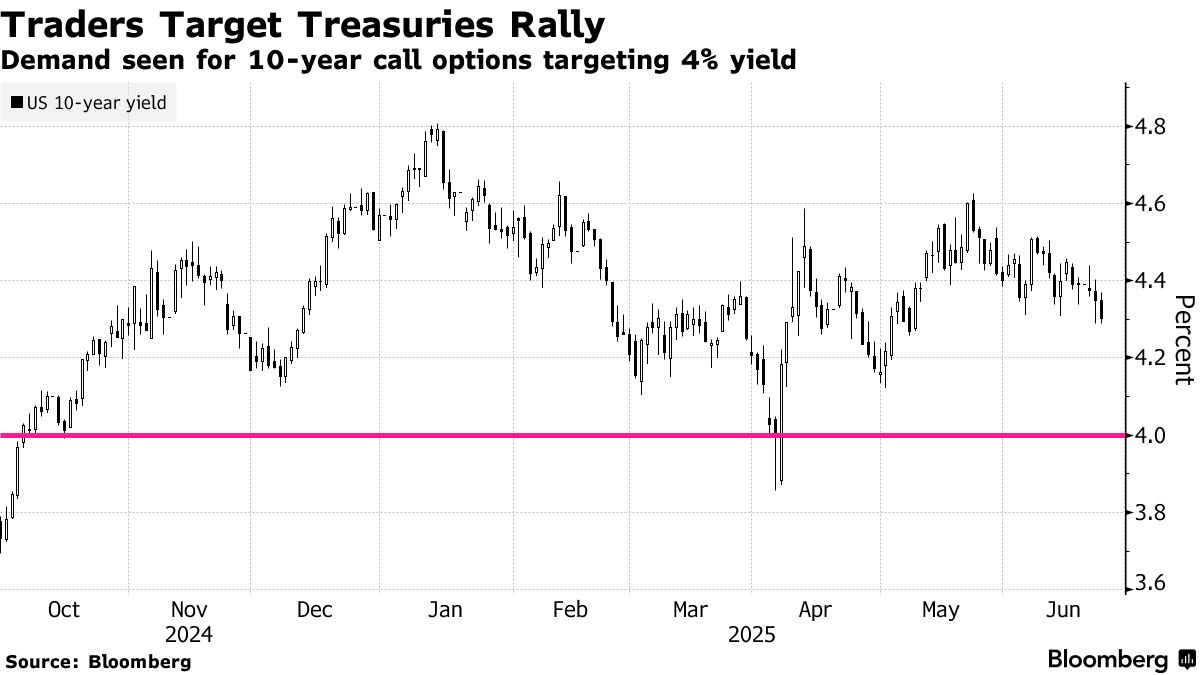

June 24, 2025 at 8:30 PM UTC Bloomberg: Bond Traders Boost Bets That US 10-Year Yield to Dive Toward 4% By Edward Bolingbroke

Traders are ramping up options wagers that 10-year Treasury yields are poised to sink to the lowest since April, amid dovish comments from Federal Reserve officials and a backdrop of simmering Mideast tensions.

The focus of the bets, which have drawn at least $38 million in premiums across Friday and Monday, has been around August calls on US 10-year options. The positions hedge against a drop in 10-year Treasury yields to 4% in the coming weeks, from roughly 4.3% now.

Such a tumble would bring them to the lowest since the market turmoil that followed President Donald Trump’s April 2 announcement of unexpectedly steep tariffs on US trading partners. It would also mark a sharp reversal from peak levels above 4.6% seen in May, when mounting worries around government spending in the US and other major economies sent long-term yields soaring.

A big impetus for the bullish hedges came from Fed officials, including Governor Christopher Waller and Vice Chair for Supervision Michelle Bowman, appearing to support an interest-rate cut as early as July. That was after Chair Jerome Powell signaled last week that patience on additional easing was warranted while monitoring the impact of tariffs on the economy, a stance he reiterated in congressional testimony Tuesday.

Traders, however, have built additional rate cuts into the front-end of the curve. Swaps are now pricing around 4 basis points of easing into the July Fed meeting, compared with near zero before Bowman spoke, and a combined 60 basis points over the remaining four gatherings this year, up from 45 basis points a week ago.

A surprisingly weak reading on consumer confidence on Tuesday supported the options positions, pushing 10-year yields below 4.3% to the lowest since early May.

The bulk of activity in the options bets was seen Friday and Monday, when yields tumbled before Trump’s evening announcement of a ceasefire between Iran and Israel following more than a week of conflict.

Open interest, or the amount of new risk, has surged since Friday in the August 10-year call options. On Monday, one trade cost a premium of roughly $10 million for the 113.00 strike, which is equivalent to a yield of about 4%. Recent open interest data has shown the buying since Friday to be new risk, rather than covering existing positions…

Terminal dot COM offers a couple other VIEWS for your reviews …

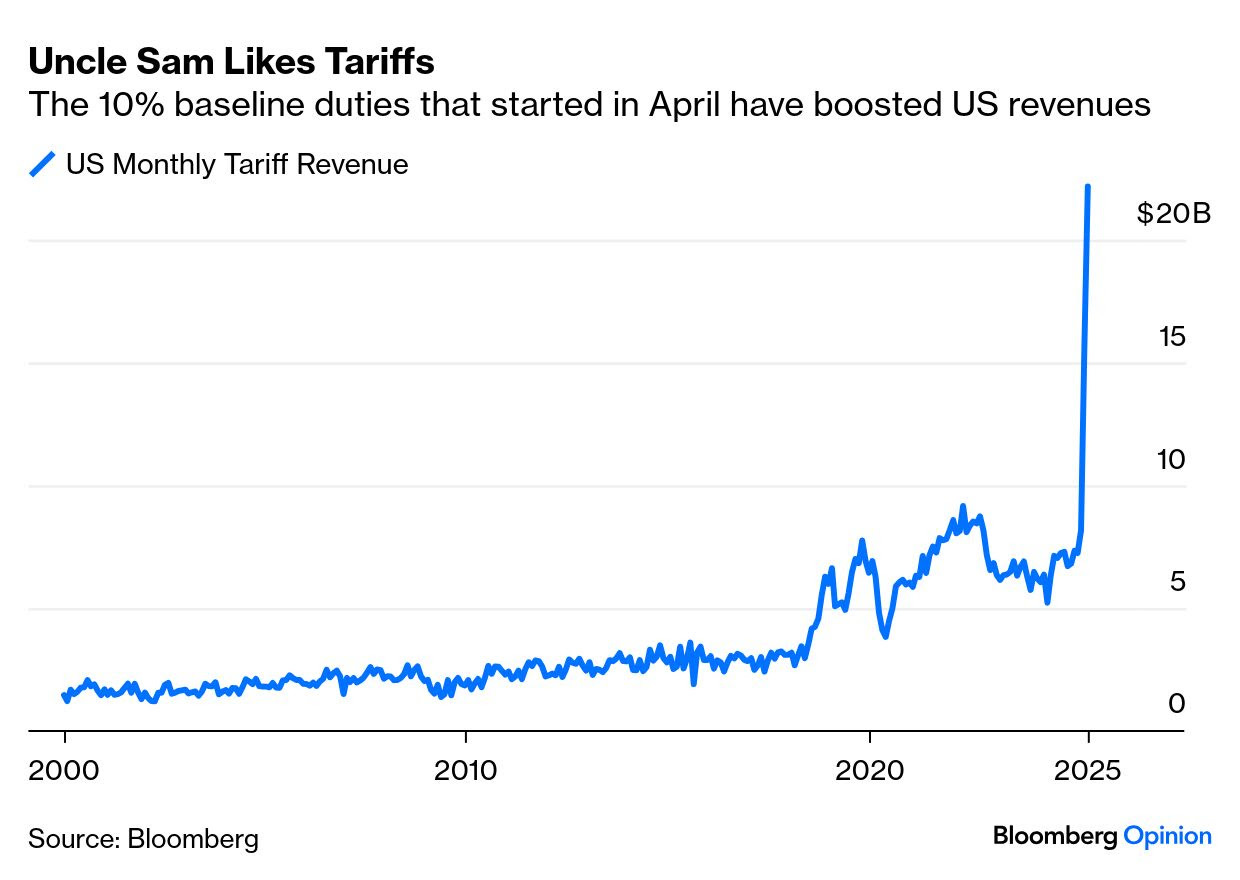

June 25, 2025 at 4:00 AM UTC Bloomberg: There's another ceasefire that's ticking Whatever Trump does on July 8, at least some tariffs are here to stay. By John Authers

…The risk that people haven’t been worrying enough about these developments can cause far more damage than those — like Iran — they’re watching obsessively. So is this degree of insouciance really justified? The pause only affected the wildly misnamed “reciprocal” tariffs, which reached as high as 44% on some unfortunate nations that run a big trade surplus with the US. The baseline 10% tariff on everyone remains in place. And that has had a massive impact on US finances. This is how monthly revenue from tariffs has moved since 2000:

Various ultimatums along the way and a brief threat to levy 50% tariffs on the EU have produced virtually nothing…

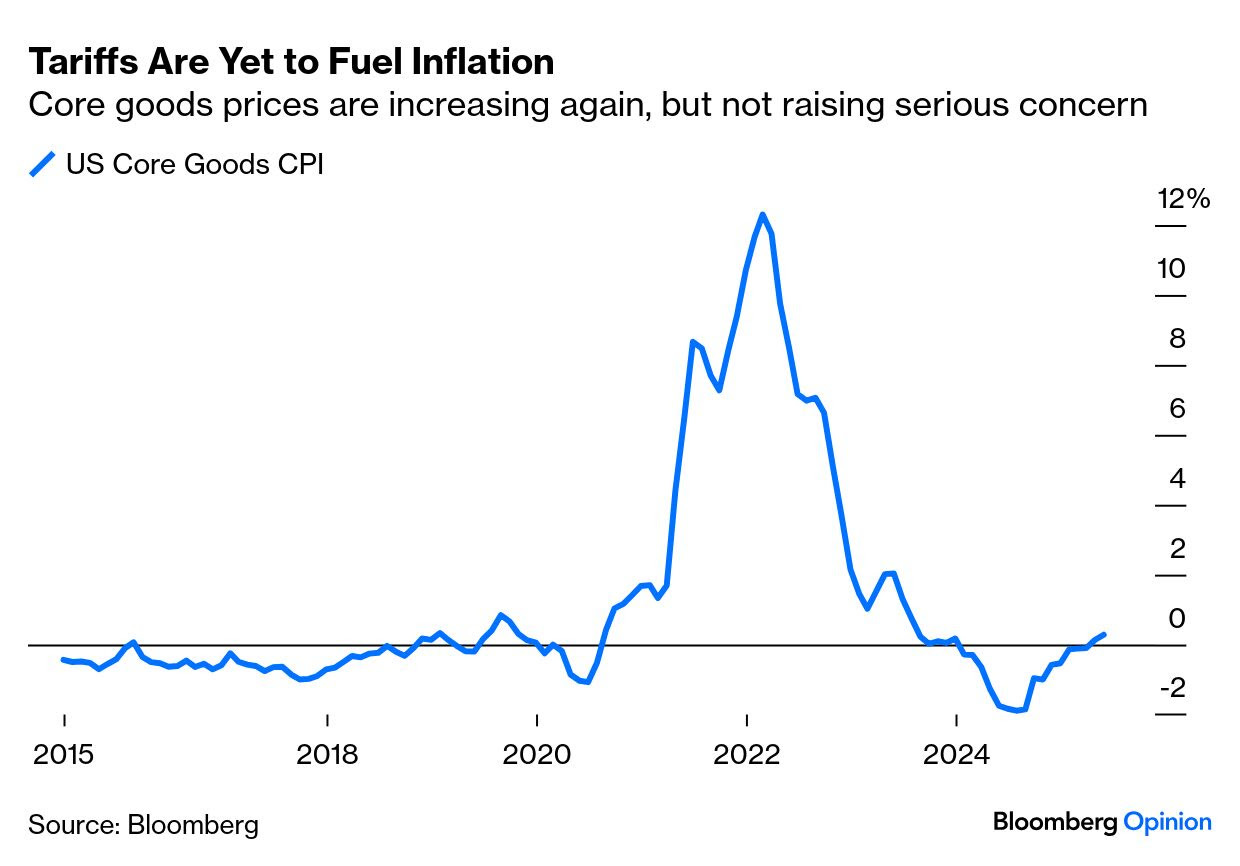

…Critically, it’s not yet had any serious negative impact. Core goods inflation is ticking up and is now slightly positive — but it hasn’t taken off in any alarming way:

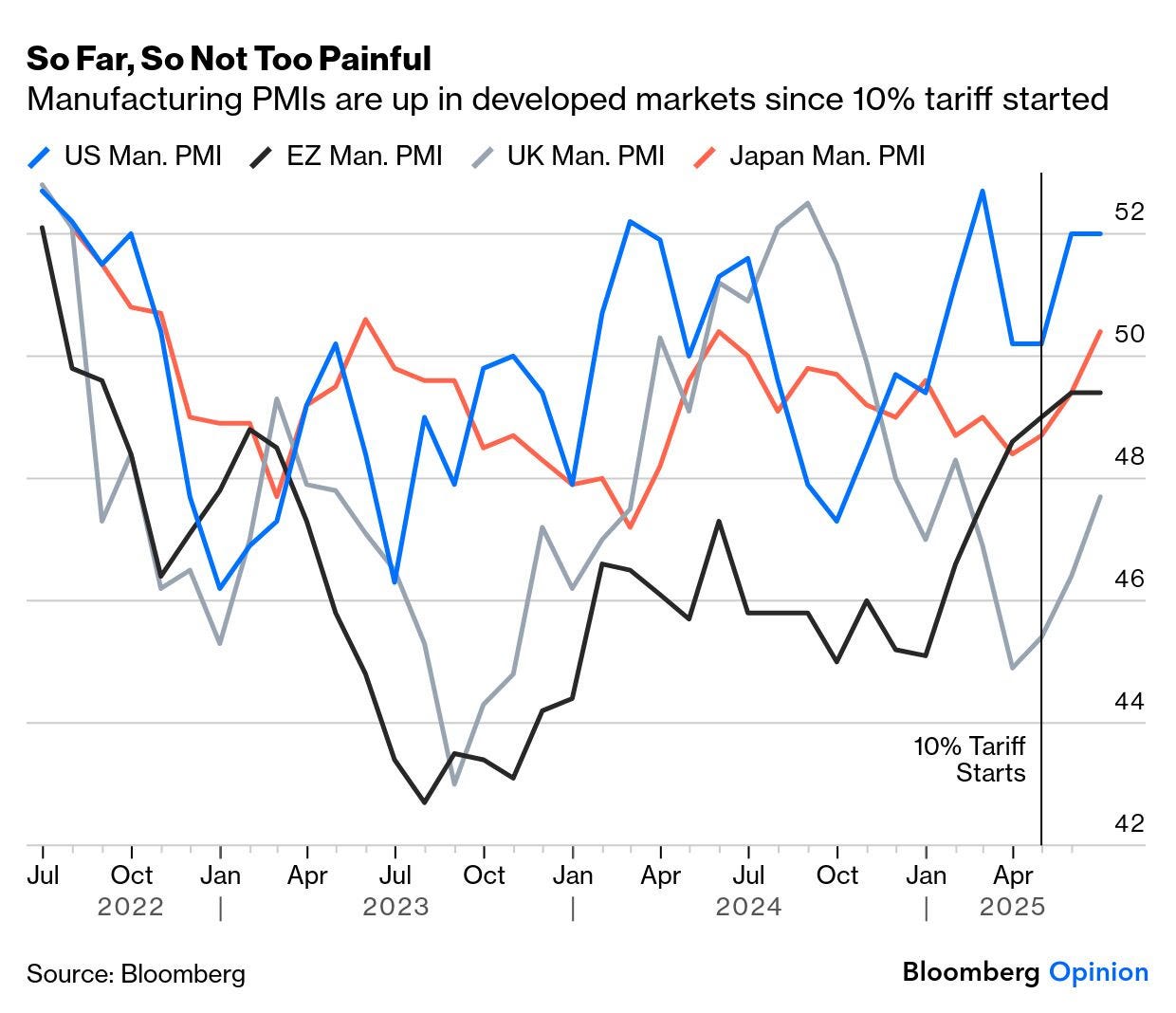

Companies brought forward production to beat the levies, which may have delayed tariff effects — but S&P Global flash manufacturing PMIs for June, the third month in which 10% was in effect, suggest global industry is living with it without difficulty. PMIs across the developed world have risen since Liberation Day:

Apollo Global’s chief economist Torsten Slok therefore argues that the president could extend the pause on reciprocal tariffs for another 12 months, and people would scarcely even notice the 10% barrier to their exports that remained in place:

Extending the deadline one year would give countries and US domestic businesses time to adjust to the new world with permanently higher tariffs, and it would also result in an immediate decline in uncertainty, which would be positive for business planning, employment, and financial markets.

This would seem like a victory for the world and yet would produce $400 billion of annual revenue for US taxpayers. Trade partners will be happy with only 10% tariffs and US tax revenue will go up. Maybe the administration has outsmarted all of us.

It’s also an elegant way for Trump to back away from a serious mistake without having to admit it.

AND those famous (last)words heard on Global Wall from time to time …

June 25, 2025 at 9:00 AM UTC Bloomberg: This Time Is Different for the US Economy Downside risks to the labor market are becoming more of a concern for Fed policymakers, with some open to a July interest rate cut. By Conor Sen

… These emergent but inconclusive labor market risks pose a challenge for the Fed, which is dealing with multiple sources of inflation uncertainty, too, from tariffs to the tax legislation going through Congress and conflicts in energy-producing regions. It’s no surprise then that Powell on Tuesday reminded senators of the need for caution with consumers still hurting from their recent experience with inflation. “We haven't fully restored price stability, and another shock, we have to be careful if there’s a meaningfully large and sustained inflation shock,” he said.

Ultimately, though, it’s downside risks from the labor and housing markets that are likely to be what’s more persistent. The Conference Board’s gauge of confidence unexpectedly declined in June, according to data Tuesday, with the share of consumers that said jobs were plentiful dropping to the smallest in more than four years. Also on Tuesday, the S&P CoreLogic Case-Shiller home price indices showed a second month of declines in April for the 20 metros tracked from the previous month.

It’s understandable that Fed policymakers want a little more time to get their arms around these short-term inflation risks, but they can't allow the labor market to deteriorate much more than it already has…

Finally, in as far as WHY no #TariffInflation …

ZH: Shocking Chart Shows Why There Has Been No Tariff Inflation

Exactly one year ago, when the dementa-ridden Joe Biden was still the presumed favorite in the upcoming presidential election and when some were speculating that tariffs under Trump (if elected) would spark runaway inflation, we said that "The Experts Are All Wrong About Inflation Under A Trump Presidency." The argument was simple: contrary to conventional wisdom, American consumers simply did not have the financial capacity to permanently absorb another round of tariffs, and at worst any inflationary hit would be transitory, one-time at which point aggregate demand would get hit and force companies to cut prices (even Goldman admitted it had been dead wrong on this as described in "Goldman Kills The Right-Tail, No Longer Expects Sustained Tariff Inflation"). Meanwhile, at best, Trump would be right and instead of US consumers or US companies forced to absorb the tariff price increases, the companies hit with the price increases would be foreign producers who - unable to pass through tariffs without losing market share in the US market - would need to slash their prices.

It turns out that Trump was right again, at least for now.

To be sure, the fat lady has yet to sign on just what the long-term impact of tariffs will be on inflation - for that we would need to wait about a year to get the full picture. But with tariffs in the pipeline for 5 months now, we have been able to see what foreign companies are doing in response and some of the observations are stunning.

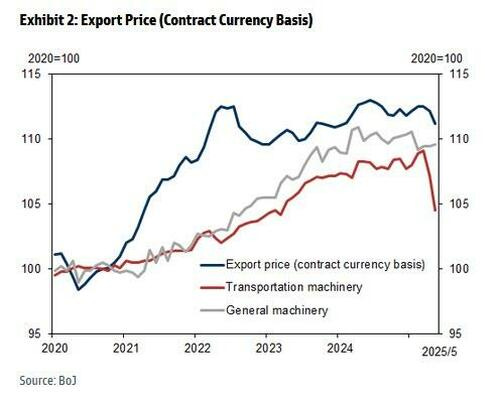

As Goldman points out in its latest report on the Japanese corporate goods price index (CGPI), there was a clear shock when looking at auto export prices, or rather auto export prices toward the US.

As Goldman's Tomohiro Ota notes (full note available to pro subscribers), export prices, which are closely watched in relation to tariffs, fell -0.7% mom in yen terms in May, continuing the decline since February, partly reflecting yen appreciation. Export prices also fell -0.9% mom in contract currency terms in May (April: -0.3%), which directly affects local sales prices in export destinations.

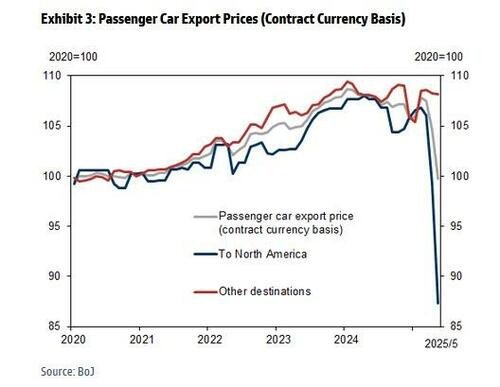

But while export prices in contract currency terms had been declining since April, the shock was the huge decline for passenger cars exported to North America (-12.0% in May; -6.5% in April). As the chart below clearly shows, Japanese passenger car exports prices to North America showed a record plunge after Trump's tariffs were instituted.

According to the Japanese strategist, after a 25% tariff was imposed on US auto imports from Japan since April, "it is possible that Japanese exporters have started to lower export prices from Japan to mitigate the impact of the tariff on local selling prices."

In a separate note frrom Goldman FX strategists Mike Cahill and Isabella Rosenberg, the duo refer to the stunning chart above and write that "mysteriously, there was a large drop prices of Japanese auto exports to North America that goes well beyond what could be explained by the stronger Yen. The data on the US side show no corresponding decline but there can be a lag between how long it takes ships with finished to get to US and they may not arrive within the same month (US import price data are collected at the beginning of the month). Data from other auto exporters like Germany and South Korea to the US are less granular and more difficult to read but the German data may also show a small decline."

The Goldman traders then add that "there are a number of possible explanations. As Chair Powell discussed in his press conference, tariffs can be spread throughout the chain between manufacturers, exporters, importers, retailers and consumers. It is also possible that firms can soften the impact in the short term by adjusting inventories, or try to avoid some of the costs by shifting profits across subsidiaries (though this would put them at risk of the FCA for undervaluing imports)." For now, Goldman writes that its (flawed) assumption is still that ultimately US businesses and consumers will ultimately pay the majority of the tariffs, as they did in the First Trade War, but the bank concedes that it is now "keenly focused on data like the Japan report because in FX we care about what side of the border pays the tariff."

Putting it all together, in order to keep the world's largest customer base happy, Japanese carmakers (and soon, all others) slashed their prices for cars sold in the US market in hopes of not only keeping their market share constant, but also capturing share from those who chose to raise their prices to keep margins flat. Call it a trade off between revenue (market share) and profits (margins), or call it a reverse game theory exercise, one where in order to capture market share from other offshore manufacturers selling to Americans, the one who cuts their prices the most, wins.

Well, that's precisely what Trump said would happen and, at least for now, he has been spot on. Again.

And as this note comes to a close, the heat presses onward, stay cool and get those bids in for 5yrs early and often … THAT is all for now. Off to the day job…