Good morning … #Got2s ?? Want some? Why NOT? I mean the war that really hadn’t even started is over.

The rather large lady who hadn’t even warmed up, not only sang, but I’m told it was beautiful and great…Last night …

… AND here we are. The ceasefire being tested early on and let’s face it, we’re not going to know in real-time if this is working. Our only metric to follow along in real-time will be various market mechanisms …

Earl, for instance, is down … just look at this (disinflationary trend back ON)chart …

CLI Weekly (for some greater context): channel levels to watch $75- $55 / bbl

… momentum mini peak suggesting lower prices = path of least resistance just ahead …

… … More on Oil below (DB, CitiFX) but for now, it’s likely I keep this commentary section short and move along as facts likely to change a couple times in the interim.

JPOW watching Earl and tariff ‘flation et al and … well, right back to you, my friend …

2yy DAILY: channel levels to watch 4.15% - 3.65% and we’ve been within this channel all year long …

… as momentum becoming overBOUGHT which poses a problem for somewhat longer-term participants — likely just means some need for ‘time at a price’ or, worst case, a(nother) dipORtunity ahead …

#Got2?

Before I move along and in as far as some of the data impacting prices yesterday …

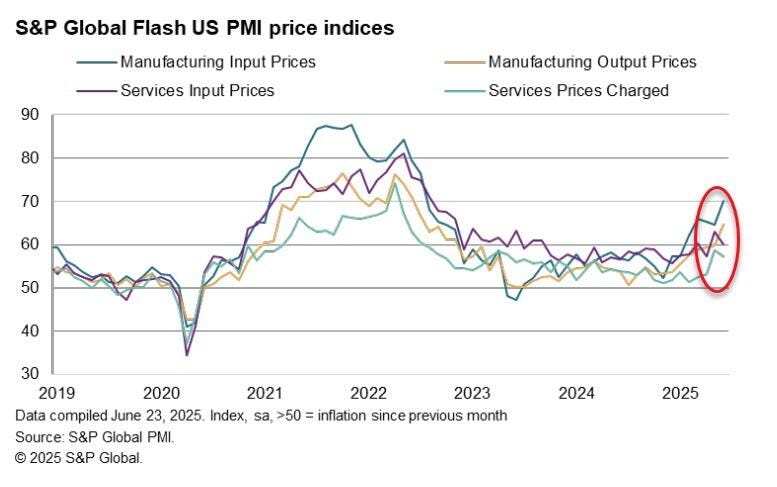

ZH: US Existing Home Sales Print Weakest May Since 2009 ZH: US PMIs Beat Expectations In Early June Data, But...

… However, prices also rose sharply in the service sector, likewise often attributed to tariffs but also reflecting higher financing, wage and fuel costs. Service sector input costs and selling prices nonetheless rose at slower rates than in May, in part reflecting more intense competition.

… and Waller NOT to be outdone — this is important, too, as it was prior TO any / all ceasefire …

ZH: Bowman Joins Race For Powell's Job, Supports July Rate Cut

… these comments added to / set the table for a more bullish move in rates (just ahead of front-end auction and so, making it somewhat MORE EXPENSIVE for Bessent’s Dept of Tsy to fund 2s) …

Nevertheless, it likely doesn’t matter as it would appear we’re seeing necessary weakening of economic data proceed (save for mfg PMI prices which again, may be totally consistent / thematic) and perhaps there’s a touch of doubt being brought in relating to stagflation) … This likely continues to add up and keep Fed on sidelines for now until there’s more concrete evidence, beyond shadow of a doubt (and at which point will already be too late …)

That is just how it goes and speaking of going, I’ll move along but first … here is a snapshot OF USTs as of 705a:

… HERE is what this shop says be behind the price action overnight…

… WHILE YOU SLEPT

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: Sentiment bolstered after Israel-Iran ceasefire comes into effect; Israel claims Iran violated agreement … Bonds hold a bearish bias given latest Iran-Israel ceasefire; USTs are lower by a handful of ticks whilst Bunds are hit on updates via the German Finance Ministry … USTs are lower by a handful ticks in what has been a choppy European morning so far. Overnight, benchmarks lost their haven allure given Trump's Iran-Israel ceasefire agreement. Though this was short-lived, as Israel claimed Iran had broken the agreement by launching two missiles into the area - This sparked a modest bid in the USTs, taking it to 111-14. Pressure has since resumed more recently in tandem with Bunds, after the latest updates from the German Finance Agency (details below); USTs are currently trading just of lows at around 111-09+. For the US specifically, traders will eye US Consumer Confidence, 2yr supply and a slew of Fed speakers (incl. Fed Chair Powell).

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

A note from across the pond on positioning, where this tidbit caught my eye …

24 June 2025 Barclays: Long & Short of It Geopolitics flare, but retail remains sanguine

Re-risking by institutions has been muted, but retail sentiment is improving (flows, Equity Euphoria Index & call buy/sell to open ratio); Middle East conflict poses acute risks; markets could react sharply to Iran-Israel escalation, which could then spark Vol Control/CTA de-risking.

…Retail investors favored bonds over equities last month

Best in show offering a few words on the day that just was …

…Treasuries rallied on Monday in a move that was linked to the retreat in oil prices and boosted near-term rate cut pricing. WTI plunged back below $70/bbl as a less-severe-than-feared retaliation from Iran eased concerns of interference with energy flows and a disruption of global oil supply. On the monetary policy front, the marketimplied odds of a rate cut on July 30th climbed as high as 1-in-4 as another Fed official expressed an openness to cutting rates at next month’s FOMC meeting. Despite being viewed as one of the most hawkish members of the Committee in recent quarters, Fed VC Bowman said, “It is time to consider adjusting the policy rate,” … “Should inflation pressures remain contained, I would support lowering the policy rate as soon as our next meeting in order to bring it closer to its neutral setting and to sustain a healthy labor market.” While two of the seven board members have voiced conditional support for a July cut since last week’s FOMC meeting, we suspect that Waller and Bowman hold dissenting opinions on the Committee…

Given MY feeble attempt at updating look at Earl (above), a few charts from the pros …

Jun 24, 2025, 2:39 CitiFX: Revisiting levels: Oil, DXY, JPY With the geopolitical tensions easing, we revisit levels to watch for Brent, WTI, DXY and JPY.

…WTI (CL1): Similar to Brent, we posted a bearish outside day on Monday. We are now testing ~65.27 (September 2024 low, March 2025 low).

Thus far, we have come relatively near resistance at the 80 handle, and then broken back below the 200d MA at 68.63. IF we close below 70.56 on a weekly basis, we would complete a bearish outside week.

We think bias remains for a move lower at this stage here. We see support at 65.27 first, followed by 63.27 (55d MA). Below that there are no strong support levels till the April and May low of 55.12. On the other hand, resistance is likely at 68.63 (200d MA), followed by 72.28 (April high).

A German bank fan favorite stratEgerist offered up a few thoughts on the day that was …

Despite all the fears over the weekend, over the last 12 hours we've seen a pretty remarkable de-escalation of tensions in the Middle East. The best scorecard of this has been the price of oil which now trades just below $70/bbl, having opened at just over $80/bbl early yesterday morning in Asia. Brent crude (-7.18%) posted its biggest daily decline since 2022 and is subsequently trading another -2.56% lower this morning at $69.65/bbl, close to the levels before Israel’s strikes against Iran on June 13. Easing geopolitical concerns helped the S&P 500 rebound +0.96%, with futures another +0.55% higher overnight. Easing inflation fears supported bonds, with Treasuries also benefitting from more dovish Fedspeak, more on which later…

…Prior to those Middle East developments, the main new story of the day had been on the Fed, as rate cut speculation got further support after comments from Michelle Bowman, the Fed’s Vice Chair for Supervision. She commented how inflation had come in at or beneath expectations recently, and said “ we should recognize that inflation appears to be on a sustained path toward 2 percent and that there will likely be only minimal impacts on overall core PCE inflation from changes to trade policy.” As such, she said that she’d support a rate cut as soon as the next meeting in late July, if “inflation pressures remain contained”. Those remarks meant futures dialled up the likelihood of a July rate cut, rising from 17% before the weekend to 23% by the close, while pricing of rate cut by September rose to 96%, its highest since mid-May. So that really heightens the importance of the next CPI report, as a 5th downside surprise in a row would really keep up the momentum for a rate cut. There has been talk about potential candidates for the Fed Chair role becoming more vocal around dovish thoughts if they believe in them given the President's very public view on what the Fed should do so this may be something to bear in mind in the weeks and months ahead. Powell's term ends in May 2026 but a replacement could be named very soon. Staying with all things Fed and rates related, today, we’ll see Fed Chair Powell appearing before the House Financial Services Committee, so it’ll be interesting to hear his thoughts too but this time the gap between this and last week's FOMC isn't large so new information may not be forthcoming.

With oil prices falling and markets pricing in more rate cuts, this proved good news for US Treasuries, with the 2yr yield down -4.5bps to 3.86% and the 10yr down -2.9bps to 4.35% and another -1.5bps lower overnight. That’s their lowest levels since May 7, before US and China announced a pause in the retaliatory tariffs. Rising rate cut expectations and easing geopolitical risks also drove a big turn around for the dollar, which had climbed by as much as three-quarters of a percent by European lunchtime, but ended the day -0.29% lower…

… as well as a chart yesterday I thought worth mentioning (and it seems as though it’s fully comprehended already by markets) …

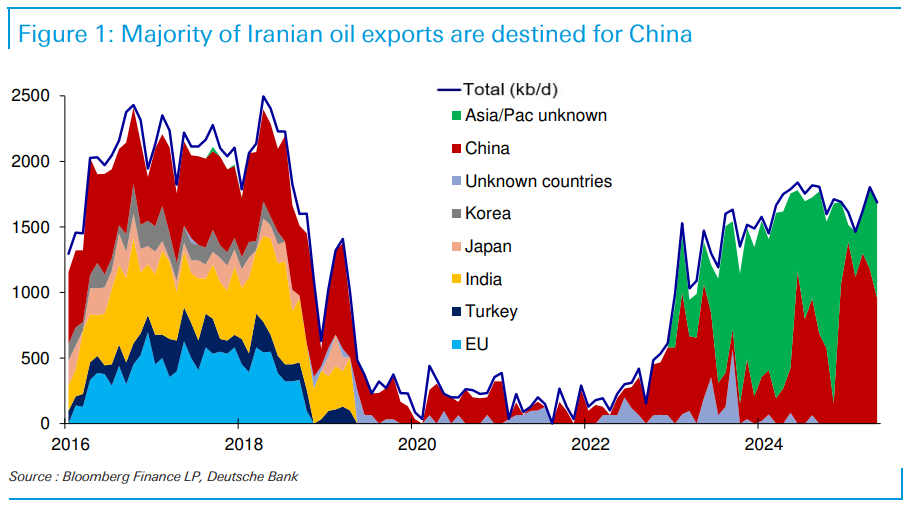

The first chart highlights that the majority of Iran’s oil exports are directed to China, with the remainder primarily going to other Asia-Pacific nations. Most of these shipments pass through the Strait of Hormuz—a critical chokepoint for global energy markets. Despite being just 21 nautical miles wide at its broadest point, the strait handles a significant share of Middle Eastern oil exports. It features two narrow 2-mile-wide shipping lanes, separated by a 2-mile buffer zone.

Given these constraints, the continued accessibility of the Strait of Hormuz is pivotal to the global economic outlook—especially following U.S. involvement in the regional conflict over the weekend. As the chart suggests, China is likely to play a key role in influencing Iran’s strategic choices….

The second chart examines European oil consumption as a share of GDP…

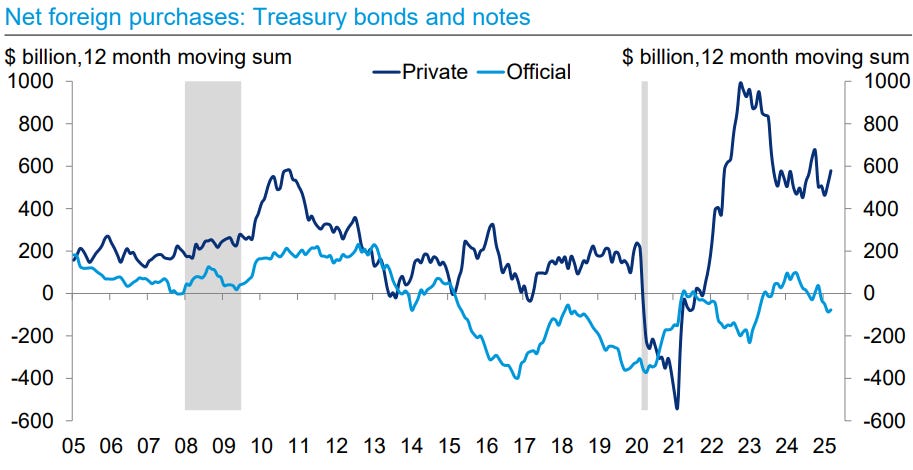

… Same firm offering a look at who’s buyin’ USTs — this one used to be a personal favorite of mine … here’s a chart may help calm fears / nerves about wholesale abandonment of rates complex …

23 June 2025 DB: Who is buying Treasuries, mortgages, credit and munis? (June 2025)

…Foreign purchases of Treasury securities driven predominantly by the private sector

…Foreign demand shifting toward short-term debt and equities

… AND a few words from the large German institution on … the Fed …

23 June 2025 DB: United in uncertainty or divided on when rates should fall?

With Chair Powell set to deliver his semi-annual Congressional testimony this week, we expect a continued emphasis on elevated uncertainty which is keeping the Fed sidelined for the time being. While the outlook is no doubt uncertain, our bigger takeaway from the June SEP was that the Committee is better described as historically divided into two camps rather than historically uncertain.

We present a suite of summary statistics of the June SEP and compare them to historical dot plots to demonstrate our point. These show that the outlook is uncertain, but not unusually so. What is unusual is the degree of division across officials. These divisions indicate that we should anticipate greater disagreement – and potentially even dissent (see comments from Governor Waller and Bowman about a July cut) – across the Committee in the coming months.

…Taken together, our read of the June SEP is that the outlook is uncertain, but not unusually so. What is unusual is the degree of division across officials. Those divisions are evident from a dot plot distribution that is highly bimodal. These divisions indicate that we should anticipate greater disagreement – and potentially even dissent (see comments from Governor Waller and Bowman about a July cut) – across the Committee in the coming months.

Importantly, despite or because of ALL the news, RangeZilla still intact …

24 June 2025 ING Rates Spark: Middle East news isn't impacting trading ranges

Markets appear untroubled by recent developments in the Middle East, with oil prices indicating that the crisis, at least in terms of market relevance, is largely over. Economic data from the eurozone gives little reason for rates to change course, while German spending plans are taking shape and highlight the fiscal impact of geopolitical change …

Geopolitical headlines aren't translating into high volatility The escalation in Iran this weekend didn't trigger sharp market moves, and Monday's attempts at de-escalation helped calm the markets further. Oil even ended the day lower than last week, with Brent falling back to US$70/bbl after a pre-announced retaliation by Iran that appeared to be more geared towards its domestic audience. Bunds reversed their earlier outperformance versus swaps, although a 10-year yield 2bp below swaps still reflects some demand for safety. Further retaliation from the Iranian regime could still challenge overall risk sentiment, but breaking from current trading ranges has proven difficult already. Over the past week, the 10y swap rate has stuck to a 2.52-2.6% range despite all headlines.

The overall economic picture in the eurozone remains one of weak but positive growth, and the data so far gives no reason for rates to deviate from this outlook. The PMIs on Monday failed to surprise and a eurozone composite index of 50.2 brings little excitement. Recent developments in the Middle East add to the uncertain economic backdrop, which we expect will continue to weigh on business confidence. But until the data turns into a material deterioration, we see no reason for markets to deviate from the expected European Central Bank landing zone of 1.75%…

…Tuesday’s events and market views After Monday’s PMIs, we’ll get the German Ifo survey numbers. Consensus sees the expectations component nudging slightly higher in June. From the US, we have the Conference Board consumer confidence indices, which are also expected to see some improvement. Meanwhile, the NATO summit could bring interesting headlines on defence spending ambitions….

Here are a few cross-asset comments from the shop with the 7 rate cuts call …

June 23, 2025 MS: Cross-Asset Playbook: Long Hot Summer Daze

Macro – A Sticky Situation

Tariff off-ramps remove most negative tail risks to macro, but the growth outlook remains muggy and inflation sticky. For the US, uncertain effects of uncertain policies keep the Fed on hold. In Europe, weak exports offset robust domestic demand. For China, détente cools trade tensions but domestic growth challenges remain.

Markets – Lukewarm Demand for USD Assets?

Going into a period of lower summer liquidity, we don’t think the main risks lie in breaks in valuations or fundamentals, both of which look benign. Rather, there’s a tension in USD assets – are they safe havens against a backdrop of heightened geopolitical risks? Or risk assets in an environment of increasing policy uncertainty? This should drive fluctuations in flows, correlations and returns.

…Cross-Asset Themes | What Happens When the Curve Steepens? Historically, bull- or bear-steepening mostly make little difference to risk asset performance, but bear-steepening was driven by growth, not term premium.

Our US rates strategists are projecting the 2s10s curve to bull steepen, with most of the move coming from 2Y in 1H26

Strategy – Stay Cool-Headed, Stay the Course

We maintain our EW global equities and OW core fixed income allocation, with a bias towards the US. Markets have historically looked through bouts of geopolitical risks, so focus on the low growth, lower policy rates backdrop instead. Prefer high-quality. Sell USD.

We expect continued downgrading of growth expectations by investors as the prospect of longlasting tariffs sinks in.

If investor growth expectations fall further, so too should the prices of riskier asset classes – raising risks for downside surprises in economic growth data.

Other risks remain related to US-China trade, so we still see favorable risk/reward in 3s30s curve steepeners

Risk(s)

Lifting of Trump tariffs or continued sticky inflation could keep rates elevated.

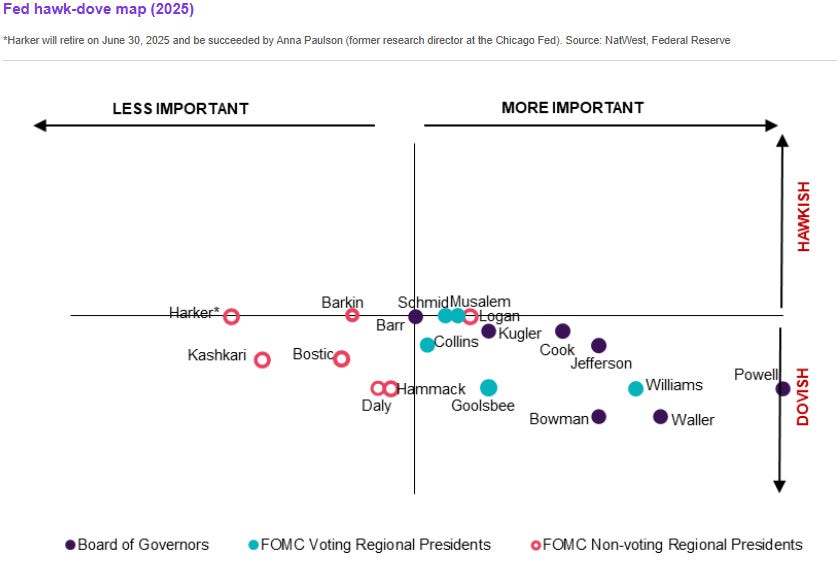

… AND ahead of JPOW testimony later on this morning (ahead of this afternoons 2yr auction), a few words and a Fed hawk-O-dove-O meter …

… On Tuesday at 10am ET, Fed Chair Powell will present the Fed’s semiannual monetary policy testimony to the House Financial Services Committee. (Note: The prepared remarks could be released earlier—perhaps around 8:30am ET—prior to the start of the testimony.) Given the chair’s press conference was less than a week ago, it is not clear that the chair will provide too many new wrinkles about the expected path of near-term policy. However, Chair Powell will likely face questions from lawmakers on any potential insights on the outlook following the recent US strike on Iran's nuclear sites. (Note: Chair Powell will also testify on Wednesday, June 25 before the Senate Banking Committee.) Also, following last week's FOMC meeting, a few Fed officials seem to have (loosely) registered what sounds like some disagreement with the timing of policy by raising the possibility of potentially swifter action than the Fed chair hinted at on Wednesday. In particular, comments from Governors Waller and Bowman were seen by market participants as a dovish challenge to Fed Chair Powell's FOMC presser (odds of a July 25bp rate cut moved up from 8% following last Wednesday's meeting to 20% currently)…

Iran and Israel seem to be saying “if they stop, I’ll stop,” although there were some missile exchanges overnight. That is enough for markets, with oil prices back to the levels of a couple of weeks ago (wiping out the potential economic impact). As with situations like North Korea, investors are not inclined to give weight to extreme tail risks, so things like the location of enriched uranium will be overlooked.

There were some moderately dovish comments from members of the US Federal Reserve, which should support financial markets. The suggestion was that rates could be cut over the summer, and could come down while inflation rose. The US economic sequence is higher inflation, lower real incomes, slower spending, slower hiring, slower growth. If data dependency is replaced with forward looking policy, the slower growth conclusion could allow rate cuts with rising inflation.

US Federal Reserve Chair Powell testifies to Congress. The testimony has value. The question and answer session often fails to add anything other than social media soundbites. Sixteen other central bankers are speaking today (ECB Chief Economist Lane speaks twice, but Chief Economists are always worth listening to more than once)…

Looking for a better way to gauge the economy? Look no further …

June 23, 2025 Wells Fargo: A Better Measure What to Exclude for a Cleaner Read on the Economy

Summary

Headline GDP numbers this year are apt to be buffeted by trade wars, inventory trade-offs and geopolitical conflicts. It is precisely for times like these that alternate measures exist. We unpack them and what they say about underlying growth in the U.S. economy.

Final sales to private domestic purchasers (private domestic final purchases, PDFP) = Gross Domestic Product less Inventories, Net Exports and Government Spending

…In reviewing economic developments at the start of the June post-monetary policy meeting press conference, Fed Chair Powell referenced this measure—which the Fed refers to as PDFP (private domestic final purchases)—as growing at a solid rate in Q1 despite net exports complicating the GDP measurement.

Figure 3

Source: U.S. Department of Commerce and Wells Fargo Economics

In Q1 this measure rose at a 2.5% annualized clip, which is just below its average run rate from last year and well above the pace of GDP growth which clocked in at -0.2% for the quarter (Figures 4 & 5). This tells us that underlying demand among consumers and businesses was actually fairly steady in the first quarter. As we look out over the course of this year, this measure should reveal a clearer read of current demand conditions.

So How Are We Doing? Incoming data through May suggest underlying domestic demand held up through the second quarter. But while we look for overall GDP growth to rise north of a 3% annualized clip in Q2, it’s a collapse in imports and boost from net exports that would be behind that knock-out print. Real final sales to private domestic purchasers will come in weaker. Retail sales suggest a moderating pace of consumer spending, while manufacturing and orders data point to a stalling in capex. Overall household and business sentiment also remain depressed clouding the outlook.

We ultimately look for PDFP to contract in the second half of the year as tariff pressure bites and diminishes households' ability to purchase and businesses' desire to invest. Watch this measure in the quarters ahead for a cleaner read on how the domestic economy is doing.

Same shop asking a different and maybe better / best question … where the answer, ahead of time, is UNLIKELY but maybe, IF …

June 24, 2025 Wells Fargo: Can the U.S. Grow Its Way Out of the National Debt Problem?

Summary

The outlook for the federal budget deficit and national debt is daunting. At present, the U.S. federal budget deficit is nearly double the long-run average and unusually large for an economy that is not in a recession or engaged in a major war.

Reducing the budget deficit via tax increases and/or spending cuts has proved politically difficult. Political developments in Washington, D.C. have time and again shown that meaningful deficit reduction is a challenging undertaking.

Could we grow our way out of the debt problem? Perhaps the least painful solution to the long-run debt situation would be faster economic growth. Both public and private sector forecasters generally believe real GDP growth will average roughly 2% over the long run, but what if they are wrong? What would the long-run fiscal outlook look like if the U.S. economy grows faster or slower than 2%?

We model three different economic scenarios for the next 10 years to derive a plausible range of outcomes for the budget deficit and national debt.

In all three scenarios, we assume the House version of the One Big Beautiful Bill Act (OBBBA) becomes law, temporary OBBBA provisions are made permanent, and tariff rates decline after the Trump presidency but remain higher than they were pre-2025.

Baseline scenario (2.1% real GDP growth and an average interest rate on the national debt of 3.7%): The federal budget deficit widens from its current value of 6.4% of GDP to roughly 8% by 2034. The debt-to-GDP ratio rises from 98% to 126%, surpassing the all-time high of 106% reached during World War II.

"Pessimistic" scenario (1.6% real GDP growth and an average interest rate on the national debt of 4.0%): The budget deficit as a share of GDP hits 10% by 2034, and the debt-to-GDP ratio surges to 140%.

"Optimistic" scenario (2.6% real GDP growth and an average interest rate on the national debt of 3.4%): The federal budget deficit remains roughly unchanged at 6.5%. The debt-to-GDP ratio continues to climb, hitting 114% in 2034, but the pace of the rise is much more gradual than in the other scenarios.

The key takeaway, in our view, is that it will take a very meaningful acceleration in real GDP over a long period of time to "solve" the unsustainable trajectory of the nation's public finances absent structural changes in revenues or outlays. To stabilize the debt-to-GDP ratio around 100%, it would likely require real GDP growth of more than 3% annually for the foreseeable future, all else equal.

Perhaps generative AI and other new technologies will lead to an economic boom that yields GDP growth rates this high. But, we would remind readers of additional downside risks to the fiscal outlook that we did not incorporate. For example, there may be unexpected developments, such as wars or natural disasters, that prompt Congress to step in with more spending than is incorporated into our projections.

Ultimately, even if real GDP growth is somewhat faster than the consensus forecast in the years ahead, we think it will still take a reduction in the primary budget deficit via higher taxes, lower spending or some combination of the two to reduce the federal budget deficit back to a more sustainable 3% of GDP.

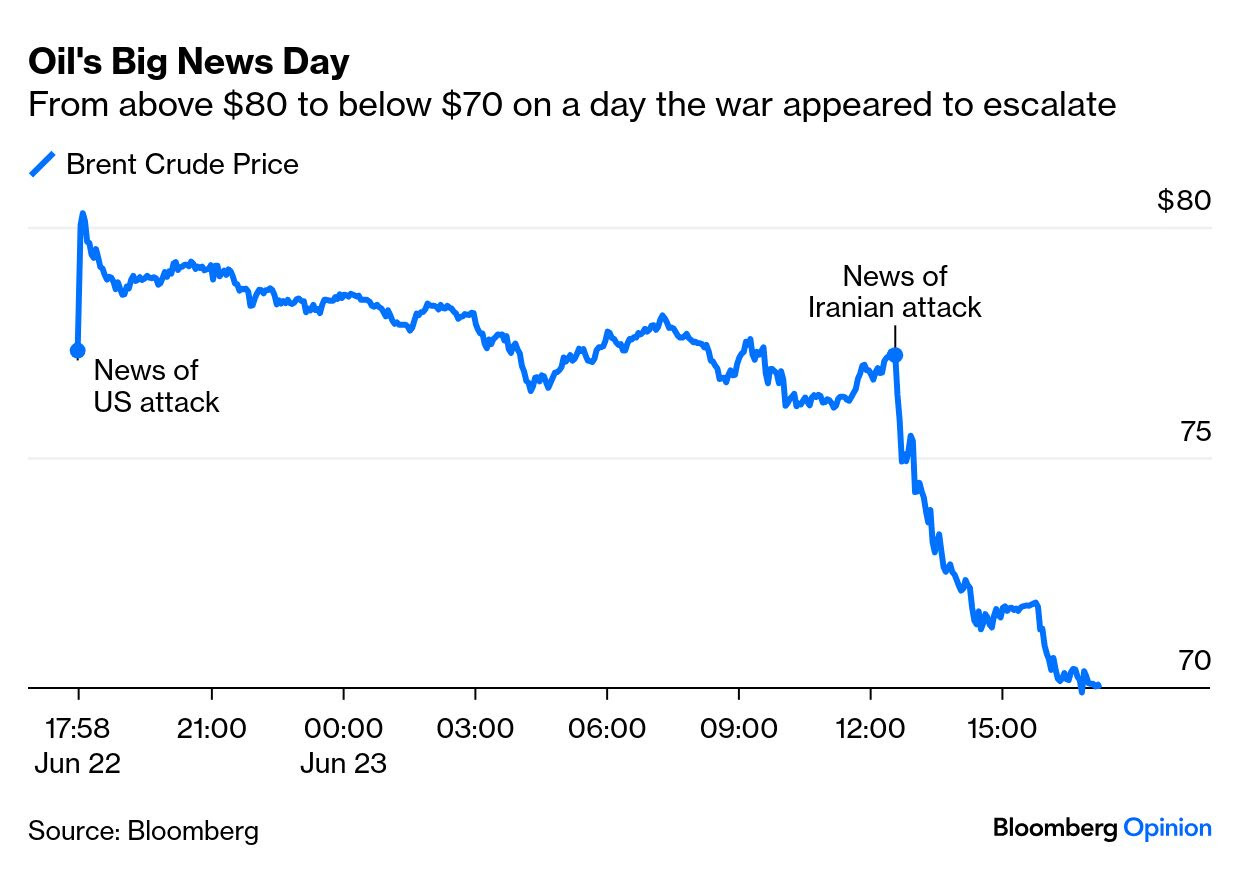

This morning, Iran launched a missile attack on the US military's Al Udeid Air Base in Qatar in retaliation for US airstrikes on Iranian nuclear facilities the previous day. The attack involved short- and medium-range ballistic missiles, with Qatar reporting that its air defenses intercepted most of them, and no casualties were reported. Earlier in the day, President Donald Trump thanked Iran for giving the United States advance notice of the coming missile strike! The notice, he wrote on social media, "made it possible for no lives to be lost, and nobody to be injured."

Stock prices rallied on the news because it greatly reduced the likelihood that Iran would retaliate by blocking the Strait of Hormuz. Polymarket.com showed that the odds of this outcome plunged from 60% on Sunday to 16% today (chart). The odds of a US recession in 2025 edged down to 27% today from 66% on May 1. Instead of a blockade, we had reckoned that Iran would sue for peace. This evening, Trump declared on social media that the "12 day war" between Israel and Iran was set to end in a ceasefire. (There was no immediate word from either country on the ceasefire, and the terms of the announced deal were unclear.)

The price of a barrel of Brent crude oil plunged 11.1% to $68.49 this evening, reflecting widespread relief that Iran staged a phony retaliation event in Qatar rather a real one in the Strait of Hormuz. The ceasefire is also bearish for oil.The US might lift sanctions imposed on Iranian oil exports if Iran behaves better.

Meanwhile, the 10-year US Treasury bond yield remained around 4.35% today as a second Fed official turned more dovish. Now there are two Fed governors who support cutting the federal funds rate at the July meeting of the Federal Open Market Committee (FOMC). Governor Christopher Waller told CNBC on Friday that he thinks the Fed should do so. Today, Federal Reserve Governor Michelle Bowman seconded Waller's motion. Both of them have become less concerned about the inflationary impact of Trump's tariffs and more willing to bolster the labor market by easing credit conditions. "I think it is likely that the impact of tariffs on inflation may take longer, be more delayed, and have a smaller effect than initially expected, especially because many firms frontloaded their stocks of inventories," Bowman said.

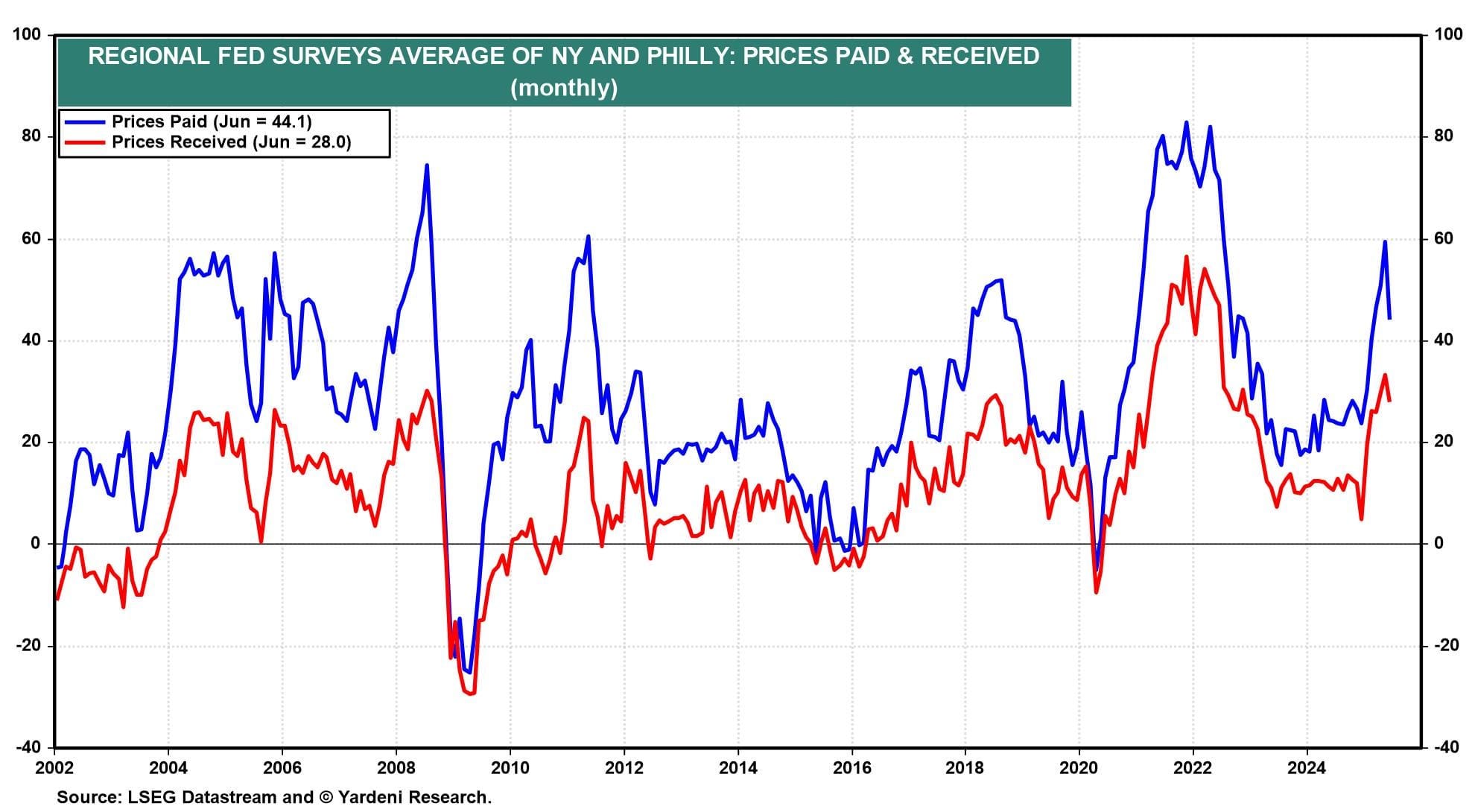

The average of June's prices-received and prices-paid indexes for the New York and Philly Fed districts rose sharply earlier this year, but might have peaked in May, as both indexes dipped in June.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

A midyear update worth a click, time permitting …

June 24, 2025 Apolo: New White Paper—Mid-Year Outlook: At the Crossroads of Stagflation

Higher oil prices, higher tariffs, and restrictions on immigration are putting downward pressure on GDP growth and upward pressure on inflation. Lower GDP growth and higher inflation is the definition of stagflation.

The upward pressure on inflation is limiting how much the Fed can cut interest rates later this year. As a result, all-in yields will stay higher for longer, which will continue to support fixed income assets, including private credit.

We have published our consolidated views in my newest white paper, Mid-Year Outlook: At the Crossroads of Stagflation—What’s Next? You can download it here…

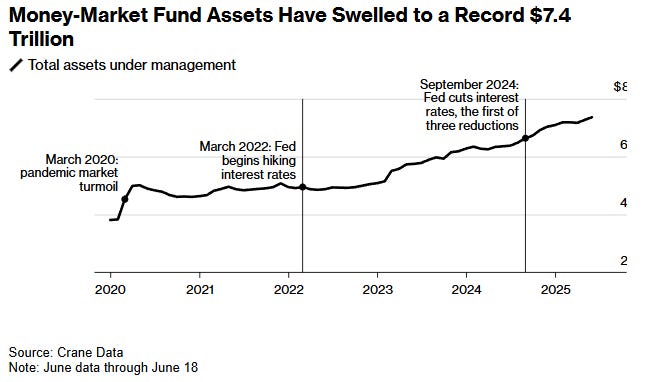

From the terminal dot com on choosing to do nothing (ie mmkt) having paid off and so, the idea continues a pace …

June 23, 2025 at 12:30 PM UTC Bloomberg: Investors Rush to Pour Cash Into $7.4 Trillion US Money-Market Fund Industry

The rush of cash into the US money-market funds is showing few signs of slowing as it secured a record $7.4 trillion in assets.

Investors have poured more than $320 billion into the funds so far this year, according to Crane Data LLC, making it one of the biggest benefactors of the Federal Reserve’s current monetary policy. That’s something of a surprise for those on Wall Street who’d gone into 2025 assuming officials would lower interest rates and sap the attractive returns offered by the industry.

“$7 trillion can easily be $7.5 trillion in 2025,” said Deborah Cunningham, chief investment officer for global liquidity markets at Federated Hermes. “Five-percent-plus rates were nirvana, four-percent-plus is still very good — and if we dip down into the high threes, that’s quite acceptable as well.”

The average simple seven-day yield is now 3.95% for government funds and 4.03% for prime, an 8 basis point spread, according to Bank of America Corp. It’s a compelling backdrop as some 600 participants gather at the annual Crane’s Money Fund Symposium, which kicks off Monday in Boston.

Money funds have seen their coffers swell in recent years, notably in early 2020 for their haven appeal and again as the Fed’s rate-hiking cycle boosted yields. Even as the Fed pivoted to cutting rates last year, assets continued to rise, with these funds typically slower to pass along the effects of lower rates when compared to banks.

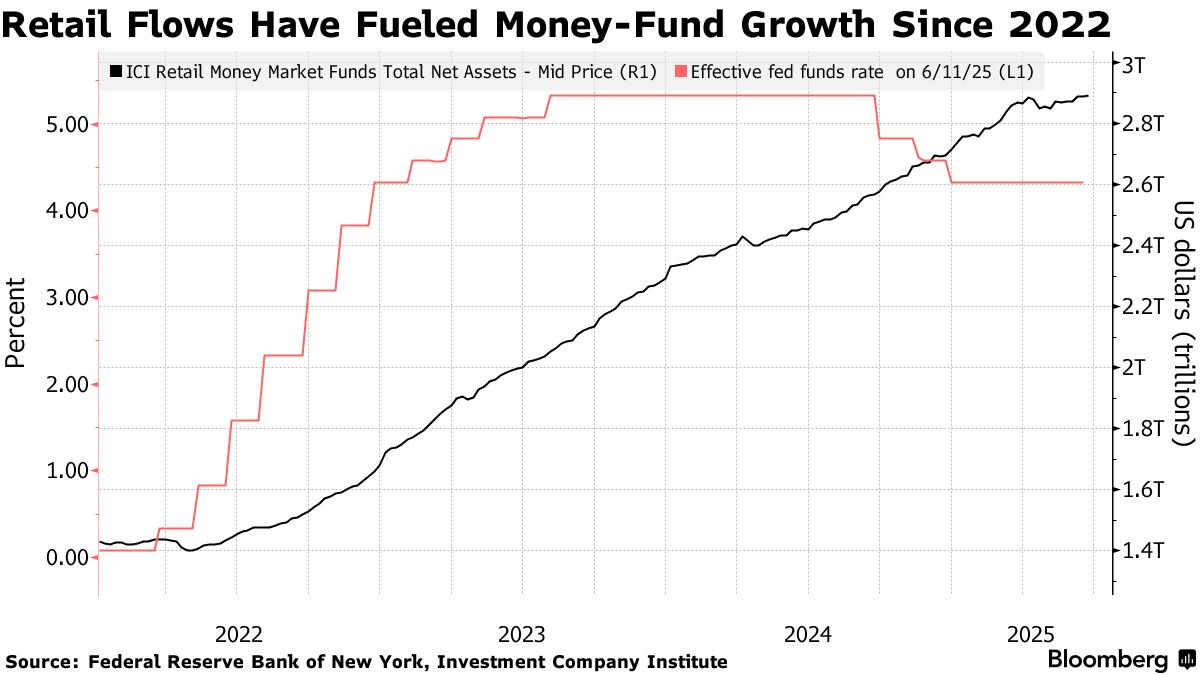

Households have been a key driver of the inflows. Since the Fed started raising rates in March 2022, total assets under management in US money funds have swelled by roughly $2.5 trillion, and retail investors have accounted for about 60% of that, Investment Company Institute data show. Data from ICI exclude firms’ own internal money funds, unlike Crane Data, which tracks the money market industry.

Inflows have continued even as the industry sees some investors embrace alternatives, such as ultra-short funds in the fixed income or equities, Cunningham said. Overall, though, it’s a far cry from the exodus of cash from money-market funds that some on Wall Street had forecast.

“It’s not surprising asset levels have held on and grown,” said Michael Bird, senior fund manager at Allspring Global Investments. “Even if the Fed picks up its easing campaign this year, rates will still be relatively high.”

The Fed last week laid out forecasts for two quarter-point rate cuts this year, aligning with market pricing. Although the risk that conflict in the Middle East drives up oil prices and causes a resurgence in inflation remains an uncertatinty, traders see a quarter-point reduction as likely in September and all but guaranteed by October.

Given that interest-rate backdrop, money-market funds are trying to extend the weighted-average maturity — known as WAM — of their holdings as long as possible to capture elevated yields.

Fund managers have also adjusted holdings to compensate for the effects of debt-ceiling drama. While Wall Street strategists largely expect the government to raise the debt limit as part of the reconciliation process by late of July or early August, some funds have put more cash toward repurchase agreements — loans collateralized by Treasuries or agency debt — as an alternative.

Still, “the expectation is when the debt ceiling gets resolved, there will be a significant increase in bill issuance, which helps yields,” Bird said. “Uncertainty is helping our product.”

… and a view from The Terminal …

June 24, 2025 at 4:00 AM UTC Bloomberg: Is it over when Trump says it’s over? We’ll see Oil prices couldn’t wait to fall again, but it’s unclear what Iran has really agreed to.

…Strait to the Point

What on earth is going on? In one of the strangest days of trading oil in history, Brent crude breached $80 per barrel at the first chance to react to the US attack on Iranian nuclear facilities, and then fell. When Iran retaliated by firing missiles at a US military base in Qatar — which might have been expected to send prices upward again — the fall turned into a rout, and Brent dropped below $70. That was a total decline of 13% in response to what appeared to be terrible news.

The reason is that the Iranian response has been judged as no more than symbolic. More contentiously, there’s a belief that the issue is over — supported by President Donald Trump’s announcementthat Israel and Iran have agreed to a ceasefire to end what he suggested will henceforward be known as the “Twelve-Day War.” Follow here for more developments.

Already, Trump’s reaction to a direct attack on a US base had showed that he saw it exactly as the oil market did. Stating that no Americans had been harmed, he said:

Most importantly, they’ve gotten it all out of their “system,” and there will, hopefully, be no further HATE. I want to thank Iran for giving us early notice, which made it possible for no lives to be lost, and nobody to be injured. Perhaps Iran can now proceed to Peace and Harmony in the Region, and I will enthusiastically encourage Israel to do the same.

If the Iranian attack was meant to help the regime save face at home, this response almost completely invalidated it. Drawing such praise from a US president scarcely saves Tehran’s honor, and it’s hard to believe that it’s “all out of their system.”

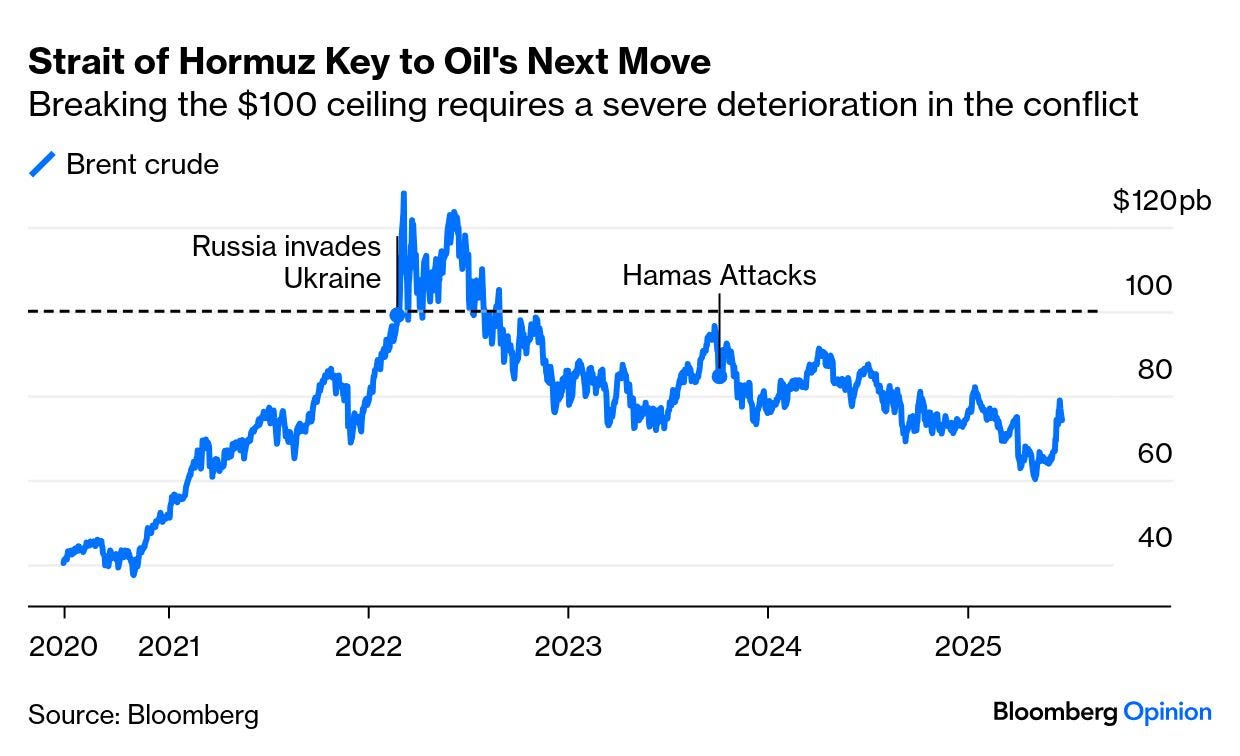

Are the reactions premature? And how can a chapter of hostilities including what is effectively the long-feared “big one” have been received so differently from the last serious geopolitical shock, when Russia invaded Ukraine in 2022? That episode took Brent to $120:

Robin Brooks of the Brookings Institution explains why exploding the most powerful bomb to be used in conflict since Nagasaki has had comparatively little impact:

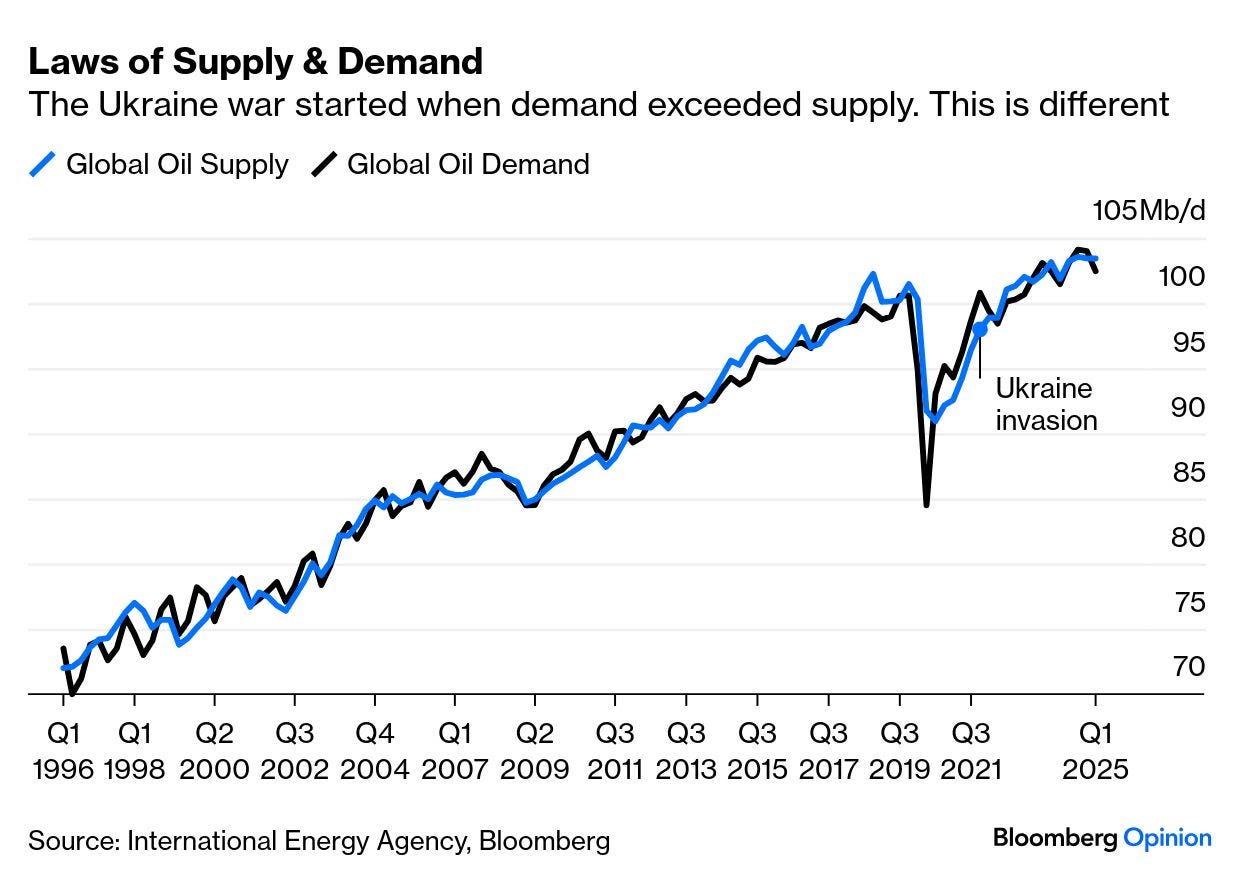

The risk of Russian oil supply being taken off the global market was high, at least in markets’ eyes during those early weeks following the invasion. The sad truth is that the same does not hold true for the Middle East. Markets are inured to endless violence, which means that the hurdle for severe market fallout is higher.

A missile strike against a military target — rather than hitting energy infrastructure in a way that damaged the supply of oil — can in this context be seen as good news. There’s also the fact that the dynamics of supply and demand were pushing the oil price upward three years ago, whereas now supply exceeds demand. This is how global oil demand compares to output in the last three decades, according to the International Energy Agency:

So far in this conflict, oil has only briefly topped $80 per barrel, then retreated. The market consensus was that Iran’s next move would be telling. The missiles fired at Qatar, though not a definitive olive branch, was more or less the best-case scenario.

With more than a fifth of the world’s oil production transiting the Iran-controlled Strait of Hormuz, the regime retains high leverage on where oil prices head next. A closure would have far-reaching consequences. It’s not yet clear, despite the market reaction, that Iran’s muted initial response means that this option is off the table.

However, there are strong inducements not to close the Strait. Ted Gardner of Westwood’s Enhanced Midstream Income ETF argues that a blockade would most hurt Iran’s allies, particularly Iraq and China. Further, the regime still has much to lose even after the US attacked its nuclear program:

The fact that Trump and Israel haven’t targeted Iran’s economic infrastructure — only military and nuclear — means Iran hasn’t lost much beyond nuclear capability. If their economic infrastructure were hit, we’d be far more likely to see retaliation through a Strait closure.

Against this, there is still the argument that disruption to the Strait of Hormuz could in a worst-case scenario drive prices above $130 per barrel. Capital Economics’ David Oxley, who made this forecast, argues that the countries that would be most affected happen to hold nearly 95% of OPEC+’s 5.5 million barrels per day of spare capacity:

As well as disrupting the flow of energy to the global market, a closure of the Strait would also severely limit the extent to which OPEC+ could employ its spare capacity to offset upward pressure on oil prices.

A further question is whether higher prices would be sustained. The longer they’d last, the greater the risk of pass-through to consumer prices and, subsequently, central banks’ rate decisions. Seth Carpenter, Morgan Stanley’s chief global economist, notes that oil never returned to its $82 peak from mid-January. Since then, as Points of Return reported here, more central banks have cut than hiked. “History suggests that a 10% permanent increase in oil prices moves core inflation by only a couple of basis points,” says Carpenter, “an amount that easily gets lost in the noise.” Moreover, the US is the world’s largest oil producer.

…Fighting the Fed “Don’t fight the Fed” is an ancient market dictum, but it doesn’t apply to politicians. There’s a long history of senior government leaders clashing with the central bank, whose role is naturally in tension with theirs. Democratically elected politicians are generally happy to be able to serve some punch to the population, while the Fed’s job is to take away the bowl.

It does seem to be going a little further now. Last week saw the Federal Open Market Committee leave rates unchanged, eliciting virtually no market reaction. The S&P 500 remains very close to its all-time high despite the uncertainty; inflation is falling, unemployment is low. But this week started with Kevin Hassett, head of the president’s Council of Economic Advisors, telling CNBC: “I think there’s no reason at all for the Fed not to cut rates right now. And I would guess that if they see one more month of data, they’re going to really have to concede that they’ve got the rate way too high.”

That followed a tweet from Howard Lutnick, the commerce secretary, saying: “These high interest rates make no sense. Enough is enough!!!” The vice president, and of course the president himself, have also been inveighing on social media.

It’s highly questionable whether Jerome Powell can be fired before the end of his term, which is coming up within 12 months in any case, and pressure like this perversely makes it harder for him to oversee a cut. The long-term credibility of the Fed could be damaged by any sign of caving to political pressure. But now that he’s into his “lame-duck” phase, interest in Fedspeak from other officials intensifies.

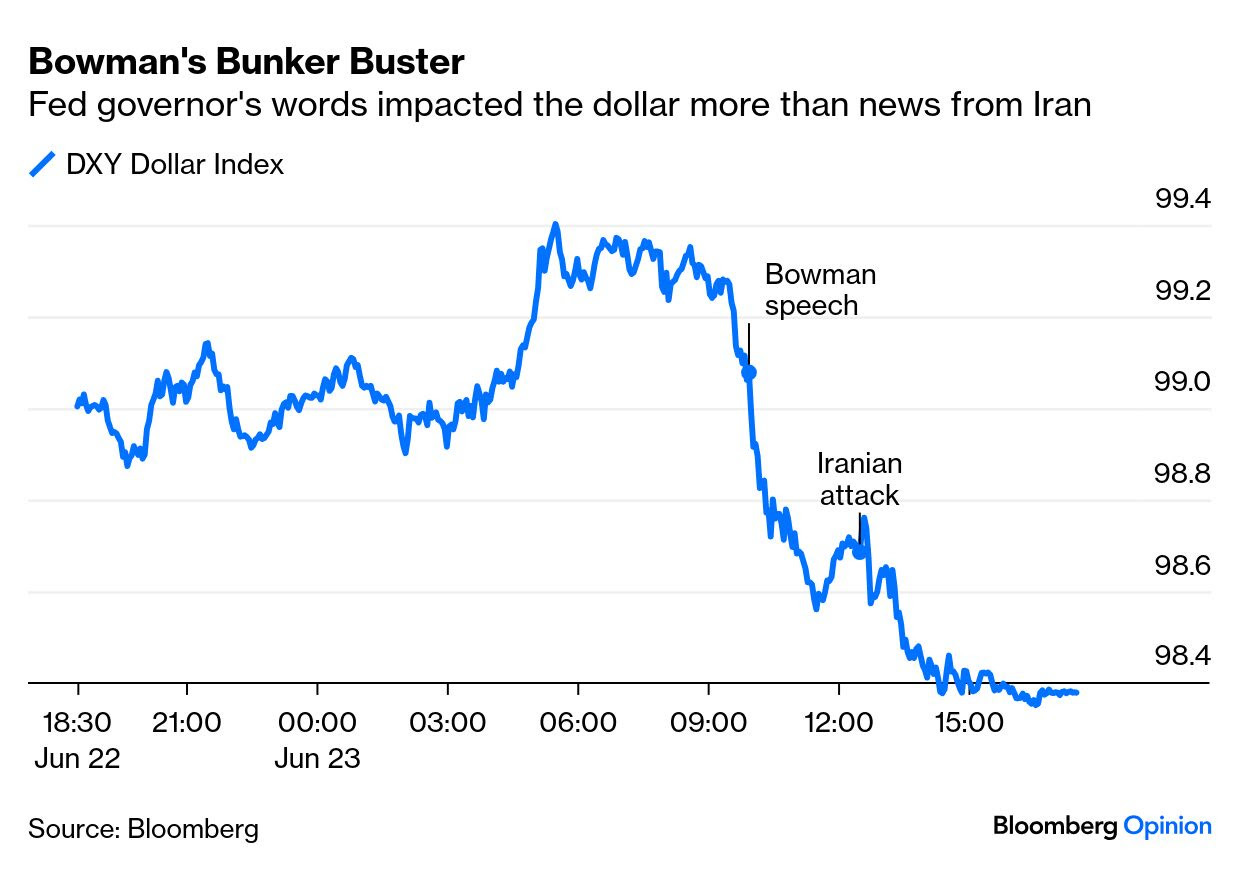

Any hint of cuts is still more than enough to bring down the dollar, even on a day of extreme geopolitical tension. Michelle Bowman, the newly appointed vice chair for supervision and widely seen as a candidate the administration might prefer for the top job, gave a speech mid-morning in which she said: “Should inflation pressures remain contained, I would support lowering the policy rate as soon as our next meeting.” The effect on the dollar was immediate:

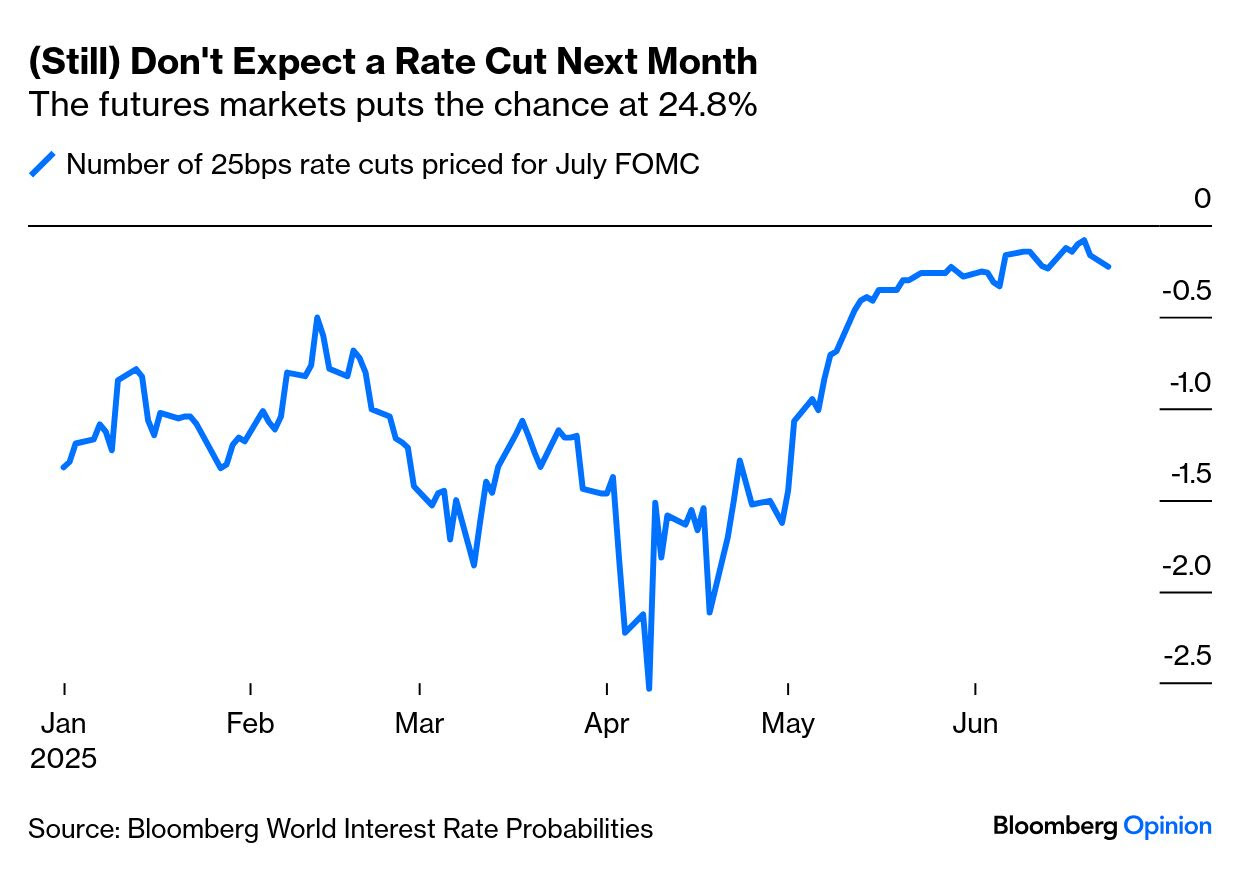

One sentence from a Fed governor was more impactful than the much-anticipated Iranian attack. Her comments followed Fed Governor Christopher Waller’s assertion on Friday that “we could do this as early as July.” Judging by the Bloomberg World Interest Rate Probabilities function, the chance of a rate cut next month is still very low, but changes at the margin matter:

Wrangling over the timing of monetary policy changes is far less exciting than war in the Middle East, or trade disputes with China. But a few words from a Fed governor can still move markets. Don’t you forget it…

Finally, all this war ON / off again gotcha down …

Follow me for more health and fitness tips and … THAT is all for now. Off to the day job…