Good morning … Given lack of any significant economic / macro FUNduhMENTAL data (and resisting the urge to become uber fatalistic about the MAG7 earnings which did begin on an underwhelming note — NAZ futures fall after Alphabet, TSLA earnings -CNBC), I’ll lead with a Bloomberg headline to chat about ‘round the water cooler this morning …

… The facts have changed, so I’ve changed my mind. The Fed should cut, preferably at next week’s policy-making meeting.

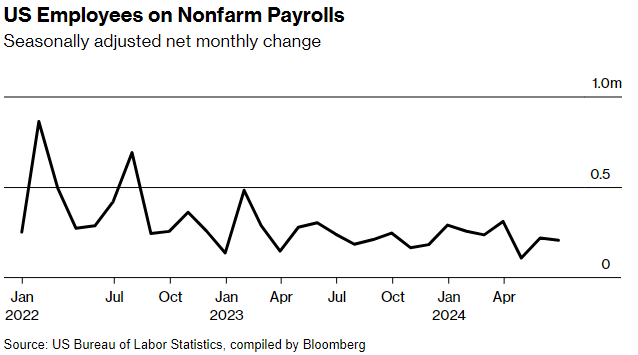

… Most troubling, the three-month average unemployment rate is up 0.43 percentage point from its low point in the prior 12 months — very close to the 0.5 threshold that, as identified by the Sahm Rule, has invariably signaled a US recession.

Meanwhile, inflation pressures have abated significantly after a series of upside surprises earlier this year. The Fed’s favorite consumer-price indicator — the core deflator for personal consumption expenditures — was up 2.6% in May from a year earlier, not far above the central bank’s 2% objective. The June reading, coming next week, is likely to reinforce this trend, judging from already reported data that feed into the core PCE calculation. On the wage front, average hourly earnings were up 3.9% in June from a year earlier, compared with a peak of nearly 6% in March 2022 …

… Historically, deteriorating labor markets generate a self-reinforcing feedback loop. When jobs are harder to find, households trim spending, the economy weakens and businesses reduce investment, which leads to layoffs and further spending cuts. This is why unemployment, having breached the 0.5-percentage-point threshold, has always increased a lot more — the smallest rise was nearly 2 percentage points, trough to peak.

Although it might already be too late to fend off a recession by cutting rates, dawdling now unnecessarily increases the risk.

AND NOW for a quick recap …

How about that there 2yr auction?? !! ??

#Got2s? Foreigners jumped into the boat (thanks, Team Rate CUTS!!) and took most. Ever …

at BobOnMarkets (twitter on INDIRECT, ie FOREIGNERS, bidding for 2s, a good visual)

WOW! The US Treasury 2-year note auction was a home run. indirect bidders took what looks like a record 76.6% of the $69 billion offered

with 4.00% squarely in bulls sights thanks in large part to perceived turn of FED cycle rapidly approaching one might only HOPE (not a strategy) then for a DIPORTUNITY (aka concession) into this afternoons upcoming $70bb 5yr auction…)

5yy DAILY

yields remain within a well defined RANGE as momentum adjusts…

ZH: US Existing Home Sales Puked (Again) In July... ZH: 'Worst Since COVID Lockdowns' - Regional Fed Surveys Plunged In July

… added up at days end TO …

ZH: Small Caps Surge On Short-Squeeze, Sloppy-Surveys; ETH Outperforms BTC As ETFs Launch

… Treasuries were mixed today with the short-end outperforming...

...which dragged the yield curve (2s30s) almost to being dis-inverted....

… which then leaves us looking forward with great HOPES for the day ahead with even LESS macro funDUHmental inputs (mortgage apps, trade, S&P mfg/svc PMI and new home sales all detailed HERE) and SO … for early excitement we’ll lean on DUDLEYS change of heart and mind as Team Rate CUT looks to declare another victory of a day!!

Here is a snapshot OF USTs as of 630a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Equities in the red amid post-earning losses in LVMH, Tesla and Alphabet, Bunds bid after dire German/EZ PMIs … USTs are flat, Bunds initially propped up on dire German/EZ PMI releases but are now off best levels … USTs are moving in-line with EGBs thus far with macro newsflow, but docket does pick up later on with the region's own PMIs and a 5yr auction both scheduled. Currently, at a 110-31 peak with yesterday’s best just above at 111-00.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

BARCAP: Existing home sales continue descent in June

Existing home sales declined 5.4% m/m in June to 3.89mn. Both single-family and multifamily sales registered declines, leading to an increase in the monthly supply of homes. Elevated mortgage rates remained a driving source of weakness for home sales.

… In keeping with our near-term range-trading thesis, it was encouraging to see the post-auction follow-through that brought on-the-run 2-year yields to 4.476% – comfortably below 4.50% and up against the 9-day moving-average. We see more room for the 2-year sector to rally with the opening gap of 4.417% to 4.424% still a distance away. The local low yield level in the 2-year benchmark is 4.404%, reached on July 16th and providing solid resistance in the case of a rally. Strong sponsorship for front-end supply can only carry the sector so far without either further weakness on the data front or dovish monetary policy guidance. The latter will have to wait until next Wednesday’s FOMC statement and Powell’s press conference.

While 2s outperformed, the 10-year sector managed to drift lower in rates, slipping back below 4.25% as the market continues to respond to the evolving political landscape and the dearth of top-tier data…

… Those tech earnings started on an underwhelming note last night. Alphabet did post a modest revenue and earnings beat, boosted by cloud computing and advertising growth, but its shares slid -2.2% in post-market trading after the management call alluded to upcoming expense pressures. Meanwhile, Tesla fell by -7.7% after-hours as it missed earnings expectations for a fourth consecutive quarter and delayed its Robotaxi event until October. Both Alphabet and Tesla had earlier fallen by about 1% in the final 30 minutes of regular trading (they were +0.07% and -2.04% on the day respectively), contributing to a weak equity close …

With growing conviction about future rate cuts, that helped push yields on 2yr Treasuries down -2.6bps to 4.49%, whilst those on 10yr Treasuries were down -0.2bps to 4.25%. Front-end outperformance was aided by a very strong 2yr auction which saw $69bn of bonds issued 2.3bps below the pre-sale yield as primary dealer take up fell to its lowest since the start of the data in 2003 …

Since late January, 5y5y inflation has traded in the tightest 6-month range on record, with swaps fluctuating between 2.53% and 2.67% (recall these reference CPI). This is striking given the inflation overshoot of recent years and questions around whether trend inflation is likely to be higher going forward.

One interpretation of the tight range is that Fed policy over recent years has actually bolstered their credibility on inflation, with two sides to this coin…

An alternative explanation for the tight 5y5y inflation range is that this measure, which the Fed relies on as a key signal of longer-run inflation expectations, doesn’t actually trade with views on 5-to-10-year-ahead inflation; while those views determine the expected terminal payoff to 5y5y inflation swaps, ten years is a long time to hold the position and market liquidity and other factors prevent related arbitrage opportunities from being exploited…

Both explanations have merit but we lean towards the latter…

… So Trump and tech might have a complicated relationship if he gets elected but the graph seems to suggest the market currently believes Trump would be good news for tech overall.

Assorted business sentiment opinion polls are published, in an otherwise quiet data calendar. This, unfortunately, means that the surveys will get more attention than they deserve because talking heads have little else to talk about. Political polarization and biases in news cycles have depressed sentiment, which has tended to underperform economic reality.

US politicians continue to politick. US President Biden addresses the nation tonight—it is very unlikely that he will say anything markets care about. Vice President Harris appears to have a majority of delegates backing her presidential bid, with discussions today about a virtual vote to nominate her as candidate. Markets only care about this process if Harris signals a significant policy shift (unlikely) or if odds around the presidential election alter.

US new home sales data is volatile, has been weak, and is sensitive to the relentless repression of the Federal Reserve’s policy. US June wholesale and retail inventory data is generally overlooked (almost no economist forecasts this). However, there are stories of firms building up inventories with fears of more aggressive trade taxes (tariffs are paid by US consumers, not foreign exporters)…

Summary Higher-For-Longer Mortgage Rates Drain Demand Existing home sales fell 5.4% in June, the fourth consecutive slip reflecting the numerous affordability challenges currently afflicting homebuyers. As of June, the pace of resales nearly retreated to the prior cycle low reached last October. A resurgence in mortgage rates has kept the housing market in a lull this year. The 30-year fixed mortgage rate surpassed 7.0% toward the end of April and stayed there through most of May, stifling buyer demand. Although resale inventories have improved considerably, the combination of rising prices and higher financing costs are likely to keep a lid on housing market activity in the months ahead. Pending home sales, which tend to lead existing home sales by a month or two, slumped to its lowest level in May on record going back to 2004.

We remain cautiously optimistic about the path of housing demand, however. Although still elevated, the average mortgage rate recently hit an 18-week low during the third week of July. Our expectations for monetary policy easing this fall, if realized, would likely correspond to additional mortgage rate improvements and help to bring buyers back from the sidelines.

We do not anticipate any major surprises in the July 31 Treasury refunding announcement. We expect coupon auction sizes to remain unchanged for the second consecutive quarter.

The federal budget deficit is tracking somewhat wider relative to our expectations at the last refunding on May 1. We forecast a budget deficit of $1.85 trillion in fiscal year (FY) 2024 and $1.95 trillion FY 2025. That said, the overarching story has not changed materially. The federal budget deficit is running on trend at roughly 6.5% of GDP, about two percentage points larger than its pre-pandemic level.

A slowdown in the Federal Reserve's quantitative tightening program has helped keep growth in Treasury's financing need in check. Starting in June, the Federal Reserve reduced the cap on monthly balance sheet runoff for Treasury securities from $60 billion per month to $25 billion. The Federal Reserve reinvests the proceeds of maturities in excess of $25 billion, eliminating the need for Treasury to raise that money from private investors.

We project net T-bill issuance of $286 billion in Q3 and $32 billion in Q4. If realized, this would bring net T-bill issuance up to $430 billion for 2024.

One development we will be looking for on July 31 is guidance from Treasury on the debt ceiling. The debt ceiling is currently suspended, and absent Congressional action it will be reinstated on January 2, 2025. During some previous debt ceiling suspension episodes, Treasury felt legally obligated to reduce its cash balance down to the level that prevailed when the debt ceiling was last suspended. However, this was not the case during the last debt ceiling suspension in 2021.

We expect Treasury to maintain business as usual when it comes to running its cash balance in the $700-$800 billion range through year-end. If Treasury uses a different operating framework, say a $500 billion cash balance target at year-end, this would imply significantly more T-bill paydowns in November/December and more T-bill issuance in January/February than we currently have forecast.

During recessions, Treasury issuance shifts to T-bills, partly because during recessions, short rates are low and T-bills are a cheap source of financing, see chart below. So why is T-bill issuance so high today when the fed funds rate is high and the yield curve is inverted?

And what will issuance look like if the economy is slowing down and we enter a recession later this year? If the Fed starts cutting in September and issuance shifts to coupons, it will likely lead to a steeper curve.

Apollo: Why Would Long and Variable Lags Be Asymmetric?

Let’s assume that the economy is finally slowing down.

If it took the Fed two years to slow the economy down, then once the Fed starts cutting rates, it will take two years for the economy to reaccelerate. As a result, cutting rates in September will not be enough to prevent a recession.

In other words, with the consensus expecting a soft landing, the key question in markets today is why the transmission mechanism of monetary policy should be asymmetric when the Fed is cutting rates versus raising rates.

If the long and variable lags are symmetric, it should take two years before the economy accelerates from when the Fed starts cutting in September 2024.

The consensus sees a 30% probability of a recession within the next 12 months, see chart below. The consensus likely thinks that the lagged effects of Fed hikes will eventually slow down the economy.

To be sure, we do not expect a recession, see also here. But this is what the Fed’s symmetric logic about long and variable lags would imply.

Bloomberg: The US Economy Is Slowing, Which Is Just Fine With the Fed

Data due on Thursday is expected to show the weakest back-to-back quarters of growth since 2022.

… Figures due out Thursday are expected to show the economy grew 2% in the second quarter. After the 1.4% growth of the previous quarter, that would be the slowest consecutive quarters of growth since 2022 …

… Also in June, economic activity in the services sector by one measure contracted at the fastest pace in four years. Data released July 12 showed consumer sentiment diving to the lowest level in eight months as high prices continued to weigh on Americans’ views of their finances and the economy.

… “It’s an unusual slowdown,” says Gregory Daco, chief economist at EY, the accounting and consulting firm. He says employers appear less inclined to reduce head count because worker shortages are still fresh in their minds. He thinks that could change quickly, though, especially if interest rates stay high. “Could this turn into something worse? That’s certainly a risk. We’re navigating uncharted waters when it comes to the post-pandemic labor market.”

Bloomberg: Don't dismiss the Magnificent Seven's correction — or ignore it (Authers’ OpED on PENSION FUNDS …)

The rotation into small-cap stocks doesn’t look like a complete change of direction. But Trump tariffs could mean a bigger risk ahead.

… Measuring these returns against the old 60/40 (60% stocks and 40% bonds) is a good starting point to understand how impressive they are. Per MPI’s analysis, a strict domestic 60/40 portfolio would have fetched 15.5%, while a global version yielded 12.5%. By those standards, the teachers of Georgia and Kentucky should be very happy. And they also enjoyed a strong performance in 2023:

As we’ve seen, the Magnificent Seven phenomenon can breed fear of missing out, and managers are very much aware that making allocations based on such near-term performance carries its risks. MPI’s Jeff Schwartz argues that market timing is among the scariest things pension fund managers could do. That’s particularly relevant given the recent rotation out of the biggest stocks:

I fear they’re being pulled to be market timers because we all want to judge them over these short periods. We’re living through a period where small caps are coming back, and foreign equity is coming back. Do we want to see these portfolios now showing huge allocations to small-cap and foreign? Is that what we’re looking for?

As always, investment managers must make decisions strategically. The small-cap premium will continue to exist in the long term. As Schwartz puts it, there would be genuine cause for concern to see a portfolio change dramatically just because everybody was saying small caps were back on the march.

All things being equal, MPI analysis projects an average pension fund return of 11.3%. Washington Public Employees’ Retirement System claims the crown as the top-performing fund over the 10-year period through fiscal 2023 and is projected to achieve a return this year of 10.2% with similar reported allocations to public and private equity. That 2024 performance doesn’t sound good until it’s viewed in the longer-term context, which is always the most important for pensions. Washington’s long-term performance should remind managers that piling into public equities isn’t an easy way out.

… AND before hitting SEND, a(nother)programming note. Travelling tomorrow and will NOT have access to things but will be monitoring markets and Global Wall St inbox best I can … will HOPE to be back to spammation of the intertube by Friday morning and so, good luck as you plan both your 5yr AND 7yr auction trades and TRADE your 5yr and 7yr auction plans!