Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

I KNOW I suggested there’d be some ‘radio silence’ for a few days and while that is still to be true, a complete ground stoppage, a coding issue impacting Global Wall and a president on verge of an exit from the race (?), well … I couldn’t help but slow down and check in on (bond)MARKETS … can take the guy outta the bond markets but cannot take the bond market outta the guy and so …

30yy — WEEKLY (daily bars, inset) …

… appears to me, yields remain within RangeZILLA here and so I’ll refrain from further commentary … middle of the summer, election cycle, couple / few more data points before September cut which is widely anticipated / priced …

SO … a couple few things I’m thinkin’ about … First, the PC I use IS having issues and while I did get that ‘blue screen’ of today’s death, it appears to be working BUT …

ZH: "Largest IT Outage In History" Sparks Disruptions Worldwide

NEXT … Team Rate CUT got some more cover with this past weeks claims data (survey week?)

ZH: Initial Jobless Claims Rebounds To Highest Since Aug 2023

Team BIDEN not having such a great go of things (i’ll spare you a visual of Biden saying if you got the vax, you won’t get COVID, but the irony isn’t lost on any of us) and rather …

ZH: Biden Nomination Odds Collapse On Reports Of Imminent Withdrawal, Harris Reportedly Vetting Running Mates

… I take off a couple days and the entire ‘thing’ goes to heck in a handbasket??!! C’mon now … and by days end, as the dust settled …

ZH: Bitcoin & The Buck Bounce As Biden, Big-Tech, Bonds, & Black Gold Breakdown

… Ok I’ll move on AND right TO the reason many / most are here … some WEEKLY NARRATIVES … some of THE VIEWS you might be able to use.

SO FAR THIS WEEKEND, a couple / few things which stood out to ME …

BARCAP: Global Economics Weekly: Theorising Trumponomics (better than good read …)

With rising odds of a Trump victory, markets are becoming increasingly interested in the macro implications of the policy mix he is proposing. Most point to a US economy with high nominal growth, elevated interest rates, and a strong dollar. Next week, eyes will be on PCE and Q2 GDP in the US and euro area PMIs.

BARCAP: Fed assemblies misprint trims GDP tracker 0.1pp

The Federal Reserve released a correction to the June industrial production release to amend an overstatement of reported vehicle assemblies. Due to this correction, we update our GDP to 2.5% q/q saar, 0.1pp below where it had stood with the data error.

We looked at RTY/SPX performance over the 13 rate cutting cycles between 1980 and 2020; the notion that the first rate cut signals a sustainable uptrend for small caps is not necessarily borne out. RTY tended to underperform SPX both before and after the start of rate cutting cycles over the last 40 years.

BMO Weekly: A Grind to GDP (stay long 5s bought on dip, tgt 4.00% and stop is NFP day close up nearer 4.225%)

In the week ahead, the US rates market will continue to define the prevailing trading range as the July 31st FOMC meeting quickly approaches. Monetary policymakers will be in their typical period of radio silence and therefore, Fed expectations are unlikely to change – which resonates given that the Committee is widely expected to leave rates unchanged, but prepare the market for a move in September. The Fed's stance will, of course, remain data-dependent, even if the bar for core inflation to derail normalization is now quite high. From the FOMC’s perspective, a 25 bp cut will simply be moving from restrictive to still restrictive, and we anticipate the official messaging will be consistent with this framing. The policy conversation isn’t, nor has it ever been during this cycle, about whether the US economy needs an accommodative policy bias. Instead, it’s revolved around the degree of restriction that's in place, and we expect that will be precisely what is communicated via the late-July FOMC Statement and Powell’s press conference…

… We’d be remiss to not acknowledge the evolving political landscape in the wake of the RNC, and ahead of what’s currently expected to be the pre-convention Democratic vote to confirm Biden as the nominee as soon as August 1st…We suspect the first order response to a Biden withdrawal would be incrementally bond friendly and most likely still a steepener. Simply a reversal impulse…

Estimated real US GDP growth of 2.2% q/q saar in Q2 2024 (report released on 25 July) would look like a sizable acceleration from 1.4% in Q1. However, the composition would reflect a similar underlying pace.

We estimate final sales to domestic purchasers (GDP ex trade and inventories) to rise 2.1% q/q saar, just slightly below 2.5% in Q1. A negative net trade contribution should roughly offset a pickup in inventories, as opposed to both dragging on growth in Q1.

The Fed would take comfort from a continuation of what Chair Powell called expansion “at a solid pace” in Q1, allowing policymakers to ensure they have a couple more months of “good” inflation data in hand so as to start the rate-cutting cycle in September.

With last night’s positive close, the S&P 500 has now gone 351 trading days (back to 22nd February 2023) without a -2% down day. As today’s CoTD shows, this now places it in the top 10 of such streaks in 97 years of daily data. It is now the longest run since the 949 days (the longest ever) that ended in February 2007, at the foothills of the GFC…

DB: Investor Positioning and Flows - Rotations, Politics And Pullbacks

Look through the jump in jobless claims as the fallout from Hurricane Beryl and annual auto retooling. Conditions are still ripening for the first rate cut in September, and the market has moved further toward our expectation for 3 cuts this year. We provide a mock-up of the July FOMC statement.

United States: A String of Upside Surprises, but Growth is Slowing in the U.S. Retail sales, housing starts and industrial production all surprised to the upside this week. Yet, an uptick in initial jobless claims was a reminder that conditions in the labor market are cooling, which sets the U.S. economy on a path of slower growth in the second half of the year.

… Interest Rate Watch: Treasury Yields: Along for the Ride Through the first half of the year, the incoming data have whipsawed economists, and financial markets have come along for the ride. The see-sawing in Treasury yields over the first half of the year has been all the more notable as the policy rate has remained unchanged; the repricing has been primarily driven by expectations for future policy adjustments.

Wells Fargo: Hard Flex for Industrial Production, But Headwinds Remain

Manufacturing is still struggling under the weight of higher rates and caution around inventories may limit future gains, but industrial output just posted the biggest back-to-back gains since 2021, enough to hit a fresh cycle high and within striking distance of the all-time high reached in 2018.

Wells Fargo: Despite the Heat, the Animal Spirits are Cooling Off

Summary

Our Animal Spirits Index (ASI) fell in June to 0.53 from 0.88 in May but has remained positive in all six months of 2024.

Most components were subtractive in June, with the only strength tied to indicators reflecting the stock market.

Though a positive reading, it sits below the year-to-date average of 0.75 and is the lowest index value seen since November of last year, reflecting the recent deceleration seen in the U.S economy.

… More at some point but not likely until … perhaps Tuesday?

Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW

Apollo: Household Wealth Gains Are a Tailwind to Consumer Spending (FOOD. FOR. THOUGHT … all teams … rate cut and other guys)

Bloomberg: What Trump doesn't get about McKinley and tariffs (Authers OpED — why is it always have to be about his view of what folks don’t get … maybe, just maybe Team TRUMP gets things and OpED’ers don’t?)

They sound like an easy fix but will send prices up a mountain for ordinary Americans in more ways than one.

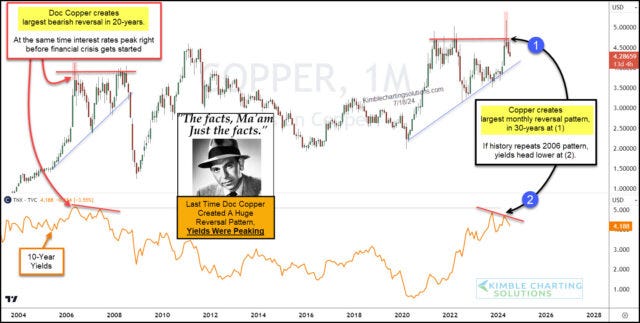

Kimble Charting: Copper Price Peak Signal Suggests Lower Interest Rates Ahead, Says Joe Friday

WolfST: The Foreign Investors Who Bought the Recklessly Ballooning US Debt: July Update (TICS report)

Who is still buying the US debt is an increasingly important question. Here are the foreign investors.

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

This is how you waste $ 230 Million......We deserve better leaders.....

http://trk.amgreatness.org/c/7/eyJhaSI6OTkyNjA2OTcsImUiOiJ2YW5oZXluaW5nZW5AeWFob28uY29tIiwicmkiOiIxMzc1NTM2OTQwIiwicnEiOiIwMi1iMjQyMDEtZjg2ZTRhZmNiMjM2NDlkMzgzNWE5MGI1OTVhNTY0MGEiLCJwaCI6bnVsbCwibSI6ZmFsc2UsInVpIjoiIiwidW4iOiIiLCJ1IjoiaHR0cHM6Ly9hbWdyZWF0bmVzcy5jb20vMjAyNC8wNy8xOS9iaWRlbnMtYWlkLXBpZXItaW4tZ2F6YS1zaHV0LWRvd24tc2VuYXRvci1kZWNyaWVzLW5hdGlvbmFsLWVtYmFycmFzc21lbnQvP3V0bV9tZWRpdW09ZW1haWwmdXRtX3NvdXJjZT1hY3RfZW5nJnNleWlkPTEwNDY1In0/-WIC9TS78pQimFOyVQyYfA

100% China tariffs are campaign bluster....while 10% Euro tariffs send icy chills down the old commie bones of the EU :)))