while WE slept: USTs firm (weak China PMI); 1st 4 trading days=contrarian signal; '25 the, "Year Of The Yield Curve" -Winghart; stocks usually goes up (but usually≠always)

Good morning … First up a few words ‘bout last night …

… Overnight in Asia, 2025 hasn’t got off to a particularly good start in trading so far. Weak data hasn’t helped matters with China’s Caixin manufacturing PMI coming in softer than expected in December, at 50.5 (vs. 51.7 expected). Against that backdrop, the CSI 300 (11.56%), the Shanghai Comp (-1.21%) and the Hang Seng (-1.51%) have all seen clear declines this morning, whilst South Korea’s KOSPI (-0.22%) has also lost ground. Japanese markets remain closed until next week.

Those declines overnight come on the back of a clear risk-off move since Christmas. Indeed, the S&P 500 has lost ground for 4 consecutive sessions for the first time since September, falling -2.62% over that time. That’s been driven by losses among tech stocks, with the Magnificent 7 down by a larger -5.30%, which took some of the shine off a very strong overall performance last year. That said, futures are pointing towards a recovery this morning, with those on the S&P 500 (+0.41%) and the NASDAQ 100 (+0.58%) both advancing. Meanwhile in Europe, futures on the Euro STOXX 50 are up +0.53% this morning …

… These comments are from DB just about 145a — more from them below.

Welp … stocks UP. Bonds UP. What could possibly go wrong?? A clean slate ahead and a quick note on previous post (‘meet the new year, same as the old’) and I’d note the ink wasn’t even dry and ‘MAY be a rental…’ couldn’t have been any more wrong.

Yields drifted HIGHER into the day, month and years end and I’ll spare you a short/medium term visual of rates and poorly timed trades (ie ‘rentals’) and head TO a recap or two for some context …

2s began 2024 approx 4.26%, the Fed raised rates 100bps and then 2s ended at 4.24%

Let that sink in and lets see a show of hands — be honest — who’d have gotten that call right … I know those on Global Wall are in the narrative business and they are equally as much in the moving of goal posts business … Anywho’s, lets move right along and mention …

10s started ‘24 at ~3.87% and ended just north of 4.57 30s started out the year at 4.02% and ended just inside 4.79

Agg RETURNS and a couple snapshots …

… and for posterity sake …

ZH: Stocks Suffer Worst Year-End Run Since '66 As Stagflationary Fears Loom

… Bonds had a very mixed year with the short-end actually seeing yields lower (by 2bps) on the year while the long-end surged (30Y +71bps)...

The long-end yields have risen for four straight years with 2022 standing out (+194bps), but 2024 stood out for its massive curve steepening (2s30s +74bps) - the biggest steepening year since 2013...

It has been a surreal year for Fed expectations with Dec 2025 pricing swinging from 3.2% to start the year to 4.50% in April to 2.8% in September to around 4.00% to end the year...

… AND for more reference and posterity sake, a couple MORE widely circulated publications summarizing the year that was …

FT: US stocks soar more than 20 per cent for second year in a row

… Investors have also had to dial back their expectations of rate cuts over the coming year. With inflation still above target, forecasts released by the Fed suggesting interest rates will fall in 2025 by less than previously hoped inflicted the S&P 500’s worst session in four months in early December. That damped investor exuberance after Trump’s election win in November, and helped push the index down 2.5 per cent in December.

Megacap tech stocks including the so-called “Magnificent Seven” — Apple, Microsoft, Meta, Amazon, Alphabet, Nvidia and Tesla — were again the dominant force in the US market.

Bulls contend that big tech’s earnings growth and AI’s potential to spur productivity justify valuations…

… Bouts of volatility briefly interrupted the S&P 500’s otherwise steady ascent. In addition to December’s fall, stocks sold off sharply in early August, with falls extending beyond the tech sector.

Nevertheless, at the start of December asset managers’ net long exposure to the S&P 500 had risen to the highest level in more than 20 years, according to Bank of America’s monthly survey of global fund managers, indicating “super-bullish sentiment”. Meanwhile, retail investor enthusiasm for stock market gains over the next year had never been higher, according to Deutsche Bank…

WSJ: Stocks Cap Best Two Years in a Quarter-Century

…Uncertainty abounds on the political front. Stocks rallied when Republicans swept the November elections, raising hopes that business will benefit from tax cuts and looser regulation. But President-elect Donald Trump has also proposed sweeping tariffs as well as mass deportations, policies that could add to inflation if enacted.

“What happens to all this excitement when we start to get all the details?” said Anna Rathbun, chief investment officer at CBIZ Investment Advisory Services. “We don’t know what the tariffs are going to look like. We don’t know what deregulation is going to look like.”

At the very least, many investors expect, markets could be in for a bumpy ride in 2025.

… and with all the longer-term contextualization, a visual and a tweet seems fitting …

at EddyElfenbein

The century is one-quarter over. The S&P 500 Total Return index is up 542%, which is about 7.7% per year (not including inflation).

Since the March 2009 low, the S&P 500 Total Return is up over 1,000%.

As late as 2011, the market was underwater for the century.

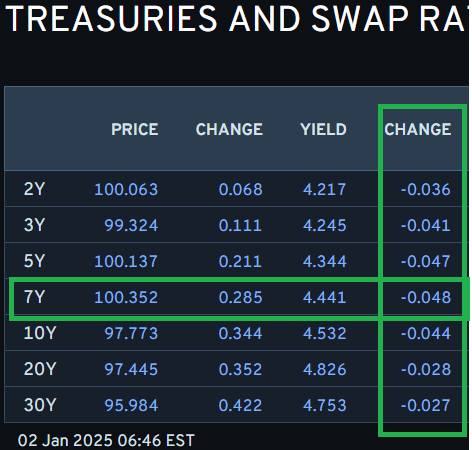

NEWSQUAWK: US Market Open: US equity futures gain & USD flat; sub-par China Manufacturing PMIs hit sentiment in the region … USTs firmer after China Manufacturing PMI and ahead of their own metrics … USTs are in the green as the region awaits its own data prints which include weekly jobless claims before the Final Manufacturing PMI for December and then the US Treasury will announce sizes for next week's 3yr, 10yr reopening, and 30yr reopening sales; no changes to the auction sizes are anticipated. Currently at the top-end of a 108-18+ to 109-03 band, though it remains shy of 109-06 from the end of 2024. Benchmarks are perhaps deriving impetus from the soft China data (more below) and the relatively tepid European tone.

Manufacturing PMI eased but still in expansion. Services and construction PMIs accelerated. Small manufacturers facing increased pressures. Price-related indicators weakened, and contracting employment indices reflect soft labour market. Overall, recovery in Q4 GDP should stay mild.

… So with 2024 out of the way, obviously all minds are now thinking about what’s going to happen in 2025. But don’t expect to get many clues today from the first trading day of the year. In fact, for the last 4 years, the first trading day has been a contrarian indicator, with the S&P 500 ending the year in the opposite direction it moved on the first day. For example, we began 2024 with three consecutive daily declines, before the index ended the year up more than +20%. By contrast, 2022 saw an all-time high on day one, before we then witnessed the S&P’s worst annual performance since 2008.

As we look forward to the year ahead, it’s also worth remembering that none of the last 5 years have exactly gone to plan or consensus in the macro sphere. 2020 was the best example of that, with the pandemic making the 2020 outlooks redundant by the end of Q1. And since then, the surprises have kept on coming. After all, the surge of inflation in 2021 surprised virtually everyone if you look back at consensus forecasts. Then in 2022, markets were caught completely off guard by the most aggressive rate-hiking cycle since the 1980s. By 2023, the consensus was then expecting a US recession that didn’t happen. And in 2024, the upside growth surprises continued, and the S&P 500 has just seen its strongest two-year performance since the late-1990s …

… In the meantime, central banks are set to stay in the spotlight in 2025. Over the course of 2024, most of the major central banks finally began to ease policy, with both the Fed and the ECB cutting rates by 100bps. Moreover, they’ve signalled that further rate cuts are ahead, with the Fed’s dot plot pointing to another 50bps of cuts this calendar year. But for both the Fed and the ECB, headline and core inflation rates are still lingering slightly above the 2% target, and we know that there are potential price pressures in the pipeline, not least from any new tariffs. So it’s going to be interesting to see if we do get the additional rate cuts that markets are pricing in, or whether this will be another year (as with the last three) where market expectations prove to be too dovish …

2024 was another strong year for asset returns, as economic growth surprised on the upside and central banks finally began to cut rates. That meant the S&P 500 posted a total return of +25%, marking the first time since the late-1990s where it’s achieved back-to-back annual returns above 20%. The index was powered by further gains for the Magnificent 7, which were up +67%, and other risk assets did very well too. Indeed, credit spreads tightened further whilst Bitcoin more than doubled. Moreover, the US exceptionalism narrative helped push the US Dollar to its strongest annual close since 2001.

Yet despite the generally upbeat performance, there were plenty of bumps along the way. Rate cuts took longer than many expected, meaning that sovereign bonds struggled to gain traction. In fact, the 10yr Treasury yield rose for a 4th consecutive year, which is the first time that’s happened since the 1980s. Political developments also caused several wobbles, particularly around April as tensions in the Middle East escalated. Over in France, the country’s assets underperformed amidst the political uncertainty. And there was huge (albeit brief) market turmoil in the summer, as weak US data and a BoJ rate hike led to the unwinding of the yen carry trade. So with quite a few concerns still in the background, gold prices posted their strongest annual gain since 2010.

… Year in Review – The high-level macro overview … Whilst global bonds recovered strongly over Q3, October was then their worst monthly performance since September 2022, back when the Fed were still hiking by 75bps per meeting. That was partly driven by strong economic data, as the US jobs report showed nonfarm payrolls were up +254k in September, with upward revisions. On top of that, the core CPI print for September also hit a 6-month high. And fiscal policy was back in focus as well, as prediction markets placed a growing probability that the Republicans would win the Presidency and both chambers of Congress, which was seen as raising the likelihood of fiscal stimulus compared to divided government. Meanwhile in the UK, the government announced additional borrowing in its budget, which contributed to a notable widening in the spread of gilt yields over bunds, with the 10yr spread moving above its 2022 peak when Liz Truss was PM.

…Which assets saw the biggest gains of 2024? Equities: Global equity markets advanced across almost every region in 2024. The S&P 500 was up +25.0%, the STOXX 600 rose +9.6%, and Japan’s Nikkei advanced +21.3%. Emerging markets were relatively weaker, but the MSCI EM index still posted a +8.0% gain.

… back TO JPM (Cembalest) for another 2025 outlook …

The Alchemists. Deregulation, deportations, tariffs, tax cuts, cost cutting, crypto, oil & gas, medical freedom and Agency purges: What could possibly go wrong? Other sections include the AI Golden Goose, the invisible nuclear renaissance, DOGE Quixote, the two China traps, Dr. Seuss goes to Europe, a crypto update and the 2025 Top Ten list

… this next note / title is NOT the most uplifting one …

2025 is the best of times, and the worst of times; an epoch of belief, an epoch of incredulity. In an increasingly polarized world, people will cling to one side or the other—without recognizing that both sides can have a point. It is an economist’s role to impartially assess the economic consequences of politics, in clear and direct language. The likely result is that I will upset everyone this year.

2025 starts with developed economy consumers in a solid position—balance sheets are OK and real incomes are rising. Developed economy consumers dominate the global economy, and this suggests benign growth. The risk is political uncertainty.

US President-elect Trump’s stated aim of aggressively taxing US consumers via tariffs is an example. Markets are not pricing in the inflation and growth consequences of policy pledges becoming reality, and assume dilution. The shift in immigration policy from Trump’s advisor Musk can be cited as a parallel—economic reality tempering political rhetoric.

Investors’ assumption that economic reality will limit political extremes is evident elsewhere— China and Germany, for example. As polarization reduces the middle ground, it is inevitable that markets have to pick a side rather than a compromise. But if markets pick the wrong side, the economic fallout will be more dramatic.

… Finally, the good Dr Bond Vigilante talking about single stock (7, actually) performance and post election activity and offering a look back at 2024…

YARDENI: Some Air Coming Out Of Post-Election Balloon

The post-election rally has been losing steam since early December (chart). The S&P 500 peaked at a record high on December 6. From a sentiment perspective, there have been too many bulls. From a technical perspective, breadth has been narrowing again as a few LargeCap momentum stocks continue to outperform. From a fundamental perspective, while earnings growth should remain bullish, the Fed may be done easing monetary policy for a while at the same time as the outlook for fiscal policy under Trump 2.0 is uncertain. From a valuation perspective, forward P/Es are stretched.

This suggests that the Magnificent-7 might continue to outperform during the first few months of the year. But we expect that broadening will resume during the spring (along with the bull market) as Trump 2.0 policies become clearer and should be bullish on balance.

A closer look at the stock market from the different perspectives suggests a cautious stance for now..

YARDENI: 2024 Was A Roaringly Good Year For Stocks

This is the time of year when we all wish one another a healthy, happy, and prosperous new year. The past two years were certainly prosperous ones for equities investors, as the S&P 500 rose 23.3% following a 24.2% gain in 2023. Those gains more than offset the 19.4% loss during 2022. On average, the S&P 500 is up 9.4% per year over the past three years, consistent with its long-run average growth rate of 7.2% (chart). Of course, accounting for dividends, returns are even higher than that performance suggests.

Three consecutive years of double-digit gains don't happen too often. Nevertheless, that’s what we are expecting: We see the S&P 500 increasing 19.0% this year to 7000. However, we think it could be a bumpier ascent than in recent years, especially during the next couple of months. Fed officials are likely to be less dovish in the coming weeks. In addition, uncertainty about fiscal, trade, and immigration policies might continue to put upward pressure on bond yields…

… And from the Global Wall Street inbox TO the WWW … a few curated links … In this first hit, one of the best in the business — agree with his view or NOT — bringing ivory tower thought process to the masses, notes / thoughts on Term Premium …

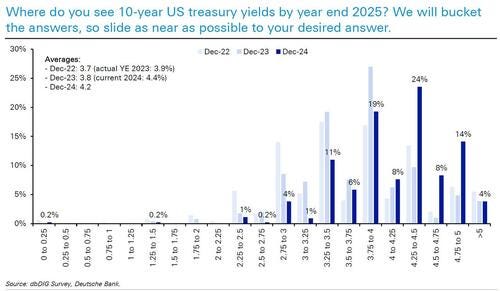

Apollo: Term Premium Up 75 Basis Points in Three Months

The term premium for 10-year Treasuries has increased 75 basis points (bps) over the past three months, see chart below.

In other words, 10-year rates have increased an additional 75 bps more than what can be justified by changing Fed expectations, which is likely a reflection of emerging fears in markets about US fiscal sustainability.

Combined with the significant decline in the Fed’s Reverse Repo Facility (RRP) usage and the dramatic increase in T-bill issuance in 2024 (which needs to be rolled over into longer duration), the risks are rising that rates markets will be more volatile in 2025.

The first chart below shows that Fed hikes have not had the desired effects on firms. You would normally expect that when interest rates go up, corporates see an increase in debt-servicing costs.

But because of locked-in low interest rates combined with strong corporate earnings, net interest payments as a share of operating surplus have been going down.

The bottom line is that Fed hikes have not only had a limited negative impact on consumers because of locked-in low mortgage rates (see the second chart) but they have also had a very small impact on corporates because of locked-in low interest rates and rising earnings.

In short, the transmission mechanism of monetary policy has been much weaker than the economics textbook would have predicted. This is because consumers and firms locked in low interest rates during the pandemic.

As a result, the economy never slowed down when the Fed raised interest rates, see the third chart. And now the Fed is cutting, boosting asset prices and growth in consumer spending and capex spending further.

To be sure, households and firms with weak earnings, weak revenue, and weak cash flows have been hit by Fed hikes. But the aggregate outcome seen in the charts below shows that, from a macro perspective, the negative effects of Fed hikes on corporates and consumers have been small.

… this next one is from before the holidays and I’m posting in case you missed wise words from THE inventor of the bond market vol index — Harley Bassman, aka …

… The Macro View I have been relentlessly trash-talking those I refer to as “Team Transitory”. These would be the financial bloviators who have insisted that inflation is transitory; and indeed, inflation tagging 9.1% in 2022 was “transitory”.

But the implication was that inflation would return to its 2012 to Covid average of 1.6%; and I would propose this is unlikely. Thus, my macro-interest rate view is “higher for longer” with the Yield Curve rotating around the T10yr …

… My investments for 2025 circle around the notion that “Fair Value” for the UST 10yr rate is 4.35%. That is 147bps (the 35-year average) over a longterm Fed Funds rate of 2.88%. T2yrs will head to 3.35% and T30s to 4.75% …

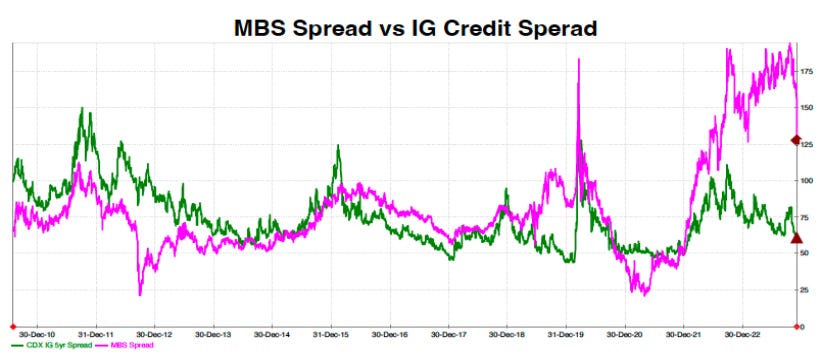

Buy newly-issued Mortgage-backed Securities (MBS) … Newly-issued -sorti line- MBS trade about 130bps above the UST 10yr, still well above its long-term average of +75bp. More important, this is about 80bp more than the -sabz line- spread of Investment Grade (IG) Corporate bonds.

… AND with (yet)a(nother) look ahead to 2025, I can honestly say I did NOT know it is to be …

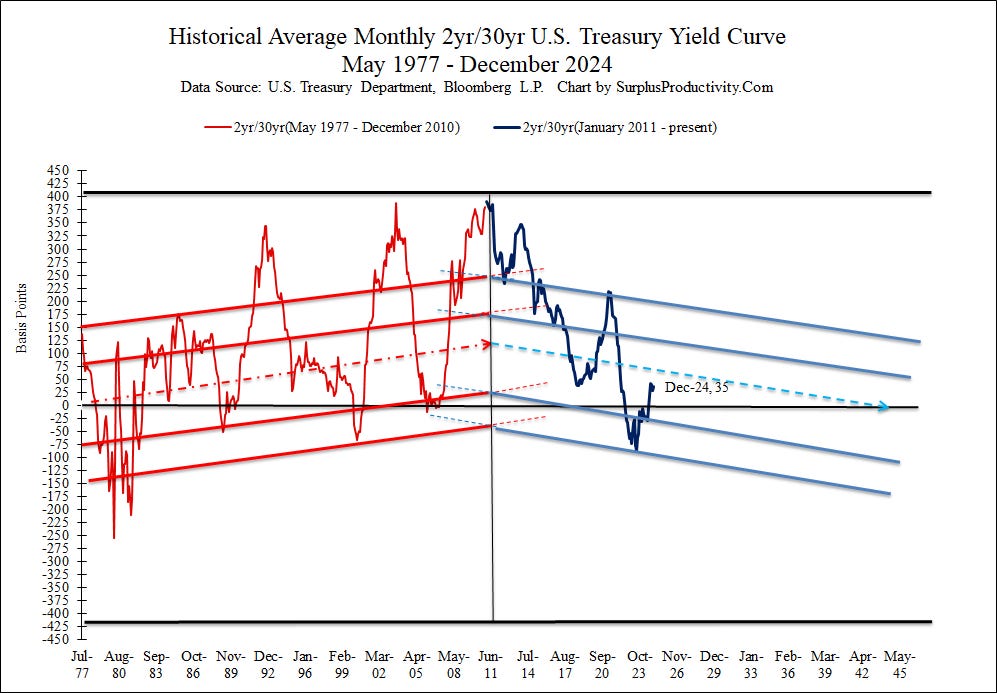

Behavior of the U.S. Treasury yield curves continue to confuse and confound

Flatter figuratively forever

Don’t conflate yield volatility for price inflation

The irony in the fact that the only thing that is clear in this new year is that monetary policy is a mess isn’t lost on the Treasury market. This situation, of course, has been building for years as the surplus productivity led widening of the output gap has, by and large, been allowed to encroach across the entire economic landscape pushing labor’s share of income to 76 year lows and price volatility to new heights. These two results strike at the heart of the Fed’s dual mandate of full employment and stable prices which means that momentary policy is increasingly failing the economy as a whole; reflected in the the behavior of the yield curves. Given its generally silent and stealth approach, surplus productivity is the crucial piece that many continue to miss in today’s economic puzzle leaving many bewildered as to just what the Fed is doing or not doing enough of. However, if the ability to predict is the best test of any theory, then surplus productivity’s forecast impact on everything, much less the trending dynamics of the 2yr/30yr yield curve over these past 6 years proves that it is much more than a force to be dealt with; it is THE force to be reconciled with in the economy in 2025 and much beyond.

Saw this coming? Some not only did but also see what is still coming.

… and not being able ever to leave well enough alone, a note ‘bout global equity markets from …

Sam Ro from TKer: The stock market usually goes up But keep in mind that 'usually' does not mean 'always'

…Stocks rallied in 2024 with the S&P 500 climbing 23.3% to close the year at 5,881.63.

If you feel uneasy about the >20% gain, you really shouldn’t. Gains of this scale are actually common.

As we discussed in October, you don’t earn long-term average returns by experiencing a lot of average years. You earn them by experiencing a lot of above-average years and some below-average years.

The stock market experiences a lot of above-average years and below-average years. (Source: Bilello Blog)

Importantly, long-term investors in the stock market experience far more positive years than negative years.

Any way you slice it, the historical data confirms that the stock market usually goes up.

“The S&P 500 remains in a bull market, and for all periods since 1928, the S&P 500 has been in a bull market on nearly 80% of all trading days,” Bespoke Investment Group analysts wrote in their annual outlook report.

“The S&P 500 has been in a bull market on nearly 80% of all trading days.” (Source: Bespoke Investment Group)

“Bull markets have historically been much more prevalent than bear markets, so if you bet against the market, the odds are stacked against you,” Bespoke analysts said.

The good news is what usually happens is the stock market goes up. It goes up on most days and in most years, and those gains have historically overwhelmed the many temporary losses during long-term investors’ holding periods.

… AND stocks for the long run …

WolfST: Global Stocks over the Long Term: the S&P 500, the Big Standout vs the Markets of Japan, China, Hong Kong, India, UK, France, Germany, Italy, Spain, and Canada

And how the decline of the yen & rupee impacted USD investors in Japanese and Indian stocks.

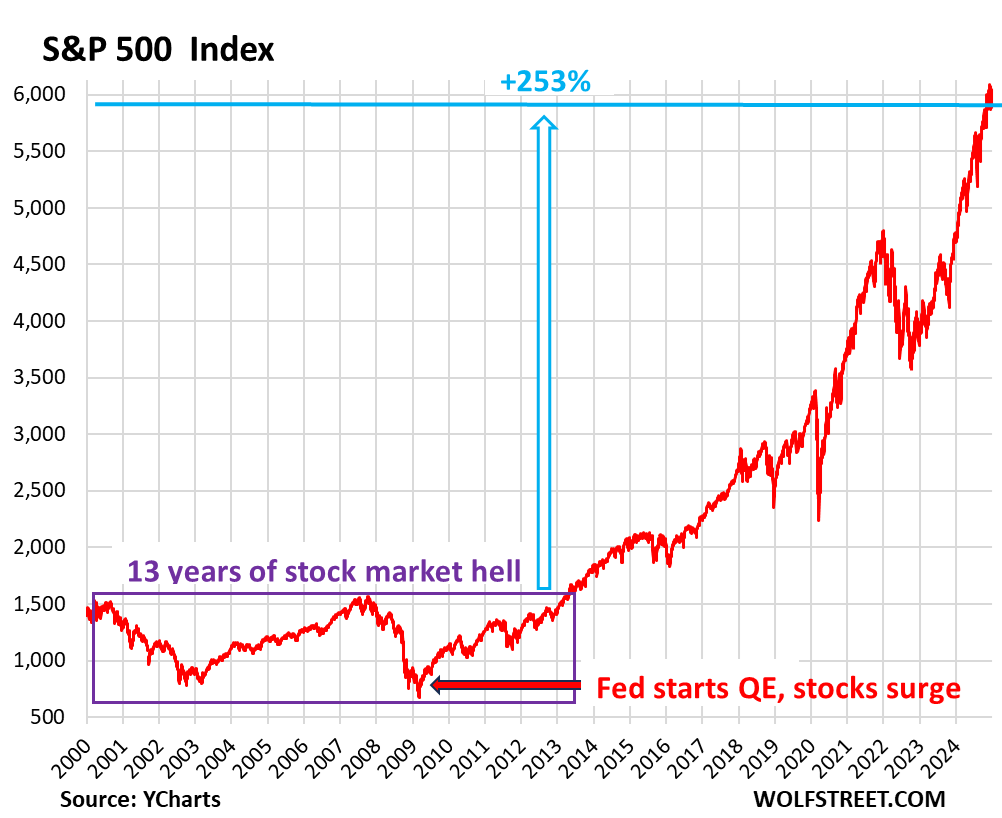

…But money-printing fixed all that. The S&P 500 has surged 253% since May 2013, which was when the S&P 500 finally surpassed its March 2000 high in a sustained manner (index data via YCharts).