Good morning … Markets appear to have digested week-ending payrolls news and depending upon how deeply you’d like to ‘analyze’ it, you are likely to find whatever it is you may be looking for. Some reflections and narratives here …

The BondBeat: weekly observations (12.09.24): URATE UP, yields down; UST "Liquidity has deteriorated moderately over the past two months"; 2025 surprise -- a Japan BID for bonds?

Top-line strength (so, Santa PAUSE) or underlying trend weakness and a pop in the URATE (further cuts ahead).

I’ll note that while we now KNOW the data, there IS some data in the week ahead (CPI) that may not have a seat at the FOMC table BUT it may very well have a vote.

Strength might rattle the doves and vice versa. I’ll leave that all to the pros.

In other ‘news’, geopolitical concerns (Syria now) and Chinese de / disinflation (and so, easing) may very well continue to keep an underlying BID for the bond market…

Bloomberg: China’s Shift Boosts Stocks Amid Political Risks: Markets Wrap Bloomberg: China eases monetary policy stance, vows more fiscal support Reuters: Fed cut gets baked in, China shifts monetary stance

…This becomes incrementally important for those helping finance the years final installment of duration supply in the week ahead (3s, 10s and bonds). Everyone likes a discount but currently, prices are inflating and we’ll have to wait and see IF this impacts the bidding process and price action, in turn, getting in the way of high / rising equities. That will be a topic for another day … I’ll quit while I’m behind and take a peak at 2yy (which is NOT up for auction in the week ahead) …

2yy WEEKLY: TLINE approx 4.10% …

… with momentum (stochastics) rolling over / crossing bullishly reflecting data and macro backdrop and so, too, rate CUTS pricing …

… with that somewhat longer-term context in mind and, in the case I don’t get chance to hit send tomorrow at regularly scheduled spammation time (morning meetings), a quick look at 3yy ahead of supply …

3yy DAILY: rangebound …

… momentum more bearish on a DAILY basis but (down)trend remains …

AND … here is a snapshot OF USTs as of 706a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: China’s Politburo sparks risk-on sentiment, but gains in equities have faded … Bonds were initially weighed on from the Politburo read-out, but now off worst levels; USTs a touch lower whilst European paper is slightly higher … Mar'25 UST contract is a touch lower after pulling back from highs after positive commentary from the Chinese Politburo which noted that fiscal policy is to be more proactive next year, whilst monetary policy is to be moderately loose; first shift in monetary policy since 2011. The main focus this week will be on US CPI on Wednesday. Mar'25 UST is currently tucked within Friday's 110.28+ to 111.20+ range.

Finviz (for everything else I might have overlooked …)

Opening Bell Daily: Stocks ignore inflation … The last inflation report of 2024 won't derail the stock market's historic year … November CPI comes due with asset prices hitting records and exuberance soaring.

Moving from some of the news to some of THE VIEWS you might be able to use … here’s SOME of what Global Wall St is sayin’ and which I’ve stumbled on since having a look and making a mention Saturday (HERE) …

First up, another crack at #2025 dart-throwing contest …

It might be a cliché, but the macro and policy backdrop appears unusually uncer tain as we head into the New Year. Tail risk looms large from many perspectives, at a time when risk assets have discounted a lot of good news and bullish senti ment is frothy. Meanwhile, the path to significantly easer Fed policy has all but disappeared.

There are two key macro and policy themes that will determine how 2025 plays out. We are on the optimistic side for both themes, but admittedly, there is plenty of room for things to go wrong.

(1) Productivity Tailwind: Echoes of the 1990s …

(2) Trump 2.0 Will Be Watered Down …

… Treasury Outlook: Limited Scope For Rate Cuts? A recent report4 discussed the reasons behind Alpine Macro’s view that the equilibrium short-term interest rate has increased to around 3.75%. These include robust productivity growth and the end of consumer deleveraging.

Fed policymakers will likely take a gradual “data dependent” approach to additional easing next year. However, an elevated R-star will limit the Fed’s room to maneuver, especially given the resilient economy, recent inflation stickiness and the potential for some fiscal stimulus.

As for Treasurys, adding a 50 basis point term premium to our R-star estimate gives a 4.25% fair value estimate for the 10-year yield. This implies that long-term Treasurys are near to fair value as we go to press…

…Investment Conclusions We believe that R-star has shifted sharply higher since the pandemic, but the Treasury market has largely discounted that story. Our fairly benign, supply-driven macro base-case view is positive for risk assets, but it is not consistent with a major shift in yields in either direction. Of course, a shocking geopolitical event could push Treasury yields sharply lower in a flight-to-quality. But outside of that, we think the Treasury market is fairly priced. The10-year yield is close to our estimate of fair value at 4.25%.

The worrying long-term trend in federal debt is unlikely to change next year. Nonetheless, we do not expect the U.S. market to suffer a “Liz Truss” moment in which Treasurys are sacked by bond vigilantes (please see the above-mentioned report for details).

This means that we do not have a bias to be long or short duration heading into 2025. Also, we are not recommending Treasury curve plays at the moment. Until something happens that causes us to adjust our base-case view, our duration strategy will be to play a trading range…

… and here, the known unknowns are what some are calling the only certainty, or something something something …

…Rates: Only certainty is uncertainty US: Recent rate declines consistent with our modestly constructive duration stance. In spreads, we suggest fading de-reg optimism and focus on upcoming bill cuts.

…Bottom line: recent rate moves were consistent with our modestly constructive duration stance. The market appears better balanced to us now, but we still retain the bias. We encourage clients to fade the de-regulatory optimism in spreads & SOFR/FF widening with ON RRP cut. Instead, clients should focus on large upcoming bill cuts.

…Technicals: US 5s30s steeper, again, in 2025 One of our technical trades heading into 2025 is a US 5s30s steepener with targets of 60bp and 85bp provided it remains above 0. The triple bottom of 2022-2023 set the stage for a multi-year steepening cycle that is not yet complete. In 2024 our target of 60bps was reached. Then a head and shoulders top formed and a three-wave decline followed (ABC) to the bottom of the channel at +/- 25bp. Uptrend channel support has remained. In our view, wave III up is not yet complete. This wave tends to exhibit larger and longer trend periods. Momentum as shown by RSI remains supported and in favor of an uptrend. MACD has corrected but remains above 0 or still in favor of an uptrend. While the view remains, there may even be upside risk to the declining trend line that began in 2011 near 100bp. The risk to this trade is a loss if the stop is reached.

Ban on exports of critical minerals to the US, suggesting increasing use of nontariff measures in retaliatory move; and MoF announced preference procurement policies for domestically made products. The annual CEWC will be in focus, though any new package will likely be unveiled in March.

.. AND on the data overnight (perhaps we will import disinflation and Fed can / will continue cutting rates?) …

November CPI inflation came in below expectations, while the PPI has now stayed in deflation for 26 months. We think risks to our below-consensus 2025 CPI forecast of 0.8% are tilted to the downside, given the absence of DM-like demand-side stimulus, a looming trade war and structural headwinds.

•November: 0.2% y/y for CPI, and -2.5% y/y for PPI

•Bloomberg consensus forecast (Barclays): 0.4% (0.4%) y/y for CPI, and -2.8% (-2.8%) y/yfor PPI

•October: 0.3% y/y for CPI, and -2.9% y/y for PPI

… France calling last rate CUT, but maybe NOT the grinch who stole a Santa Pause — um, sorry — but, well …

We expect a 25bp rate cut at the December FOMC meeting, but we see this as the last reduction for some time with the Fed staying on hold through 2025.

As the new administration’s policies begin to hit, we expect the market to price in higher US inflation and fewer rate cuts than currently.

Accordingly, we continue to see scope for a stronger USD driven by widening US-RoW interest rate differentials.

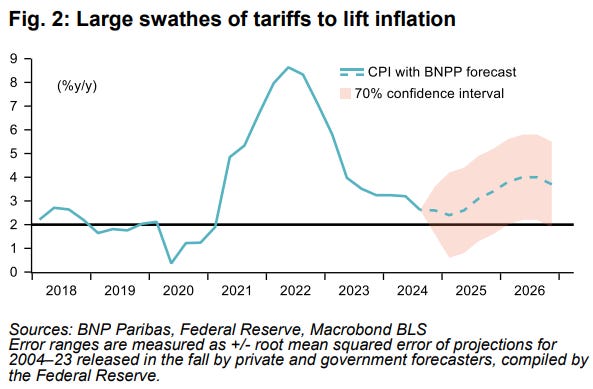

… The sheer degree of anticipated tariffs suggests that the direct lift to consumer prices could be around 80bp on its own. However, we see tariffs affecting inflation not only through rising prices for imported goods, but also via second-round effects on the general price level. Our modeling finds that rises in import prices transmit broadly to other goods, services and wages, and are amplified through short-term momentum. As such, we are above consensus on US inflation next year (Figure 2) and one of our top trades remains being paid US 5y breakevens. Current pricing does not appropriately incorporate upside risks, in our view.

… and a large German shop weighs in with a couple MONTHLY visual recaps … first one of Friday’s NFP and another of … CURVEBALLS and the year ahead …

DB: US Economic Chartbook - November employment: Stability supports slower pace of easing

The November payroll report pointed to a solid rebound from October’s weather and strike-related weakness. Headline (+227k vs. 36k) and private (+194k vs. -2k) payroll gains were largely in line with our expectations. In addition, payroll gains for the prior two months were revised up by a cumulative 56k. As we highlight in our chartbook, the recent trend in monthly job gains has rebounded of late and is now close to the 12-month average – an important signal of stability for Fed officials. The upshot of the one-tenth uptick in hours worked (to 34.3hrs) along with another 0.4% gain in average hourly earnings was that the year-over-year growth rate of our payroll proxy for nominal income (compensation component) was steady at 5.1% and tracking up 6.1% annualized relative to Q3 – sturdy readings that continue to support robust consumer spending…

…As we noted in our recent outlook update (see "US Economic Perspectives: Trump II: Growth too fast, inflation too furious for Fed cuts"), we view the past several months on balance pointing to diminished downside risks to the labor market. That said, the labor market is not out of the woods, so to speak. The dynamic of employment gains relying on the continuation of a historically low layoff rate as the hiring rate stays subdued continues to prevail. This remains a somewhat fragile equilibrium, where if layoffs were to rise without hires picking up, payroll gains could slow more rapidly. This is one reason why we continue to expect the Fed to cut rates by another 25bps at its upcoming December 17 FOMC meeting. However, next week’s inflation data could still challenge that assumption if it were to meaningfully surprise to the upside.

…Most of the trend measures of headline and private payroll gains increased with the November data

DB: Thematic Research - Monthly Chartbook: Curveballs for 2025

With 2025 approaching, it’s worth remembering that very few years proceed as expected. That’s been particularly true this decade. So, although our "Trump 2.025” outlook provides the central DB house view, this pack looks at potential realistic positive and negative curveballs that could change the direction of travel.

Examples of the unexpected this decade include:

In 2020 the pandemic meant the year-ahead outlooks were redundant by the end of Q1.

In 2021 a surge in inflation surprised virtually everyone.

… An inflation rebound: With tariffs on the agenda for 2025, just as monetary policy is being loosened, is inflation set to come back?

In 2022 markets were caught off guard by the most aggressive rate-hiking cycle since the 1980s.

In 2023, the consensus wrongly expected a US recession.

In 2024, no-one expected an S&P 500 return that could hit 30% YTD in the days ahead.

So as we look forward to 2025, it’s safe to say that the most surprising thing would actually be a lack of surprises. And in light of this, we got thinking about some potential curveballs (both positive and negative) that could change the global outlook again next year.

… everyone trying to game the whatever next …

MS: Sunday Start | What's Next in Global Macro: America Next: Policy Sequencing and Severity Matter

… We call our base case for the US policy path over the next two years ‘Fast Announcement, Slow Implementation.’ In short, we expect the Trump administration to achieve meaningful changes in these four policy channels, but believe practical and political constraints will shape their implementation. Let’s consider tariffs. The announcement of tariff escalation aimed at China could come soon after the inauguration, but with staged implementation. Why not a broader array of tariffs enacted more quickly? We’re assuming new tariffs would largely rely on existing executive authorities, with a slim Republican majority in Congress either unwilling or unable to quickly grant new and broad mandates. True, it’s been reported that Republican Congressional leadership are considering broad import tariffs as a way to mitigate the cost of further potential tax cuts. But that approach faces several roadblocks. Tariff implementation may not be permissible under the rules of budget reconciliation, which Republicans would likely have to use given their slim majorities in both houses of Congress. And while there appears to be a Republican consensus around higher tariffs on China, it’s less clear that there’s broad support for a wider array of tariffs. But clear executive authority does exist to ramp up tariffs on imports from China and some products from Europe, whereas it may take time to develop new authority through the regulatory process to levy tariffs on other countries. High tariff targets in those areas could be announced quickly but phased in over time to allow companies to adjust, in line with comments made over the past year by Trump advisors who are now nominees for key roles in the administration…

…So the bottom line is this: the sequencing and severity of these policy choices will matter a lot, but clarity on both is a work in progress. That may contribute to volatility in markets, and we’ll certainly be flexible in our approach as we learn more in the coming weeks.

… and same shop with rates-focused start to the week EQUITY NOTE …

MS: US Equity Strategy: Weekly Warm-up: Focus Is on Rates, Consumer and December Seasonality

Corporate, consumer and investor sentiment (i.e., animal spirits) have picked up since the election, but the rise has been more measured than 2016 thus far. Meanwhile, rates have remained in a sweet spot for valuations as we head into a period of seasonal performance strength in the 2H of December.

Are Animal Spirits Picking Up? So far over the last month, sentiment data has improved overall. Conference Board Consumer Confidence, University of Michigan Consumer Sentiment, NAHB Home Builder Sentiment and the AAII Bullish Sentiment series ticked higher post the election, while the ISM Composite PMI fell modestly. These series currently sit in the 34th percentile on a median basis (since 2000); 1 month/3 months after the '16 election, they sat in the 72nd/74th percentiles, respectively. We think incremental clarity on tariffs, in particular, will be helpful in terms of catalyzing further upside in these gauges. The more measured rise in animal spirits thus far and the stickiness of interest rates suggest it makes sense to remain up the quality curve within cyclicals and constructively focused on sectors with clearer de-regulation tailwinds. Financials is our preferred OW sector.

Good Is Still Good...The 1-month correlation of S&P 500 return versus change in bond yield remains in positive territory (i.e., "good" macro data is "good" for equity returns overall). Further, there is a clear bifurcation in terms of this correlation between cyclical and defensive sectors. Cyclical sectors are showing a positive correlation to rates, while defensive cohorts are showing a negative correlation. In our view, this is a sign that higher quality cyclicals, in particular, want to see stronger macro data even if it comes amid higher yields (at least for the time being).

December Seasonality...The S&P 500's median return over the month of December is +1.5% with a high hit rate of positive performance (73% over 45 years). December seasonality tends to be stronger for the Russell 2000, potentially benefiting small caps near term, but it’s not a significant enough driver to catalyze a durable rotation, in our view. We remain neutral on the small vs. large cap pair…

… On the flipside, given this correlation structure, a material drop in yields from here that's driven by weakness on the macro data front would also not be a welcomed outcome for cyclicals broadly. Thus, 4.00%-4.50% on the 10-year is likely the sweet spot for equity multiples. Yields below that range can certainly be tolerated by equities assuming the driver is Fed rate cuts in the absence of a material slowdown in growth. Yields above that range can also be tolerated if the pace of the rise in rates is measured and the driver is stronger nominal growth (versus a more hawkish Fed or a term premium surge).

… and on heels of DJTs wide ranging interview yesterday, a few words from across the pond …

US President-elect Trump gave a wide ranging interview, touching on several points that matter to investors. Trump seemed to acknowledge the independence of the Federal Reserve (the chair cannot be dismissed on presidential whim). This will reassure markets. Investors may, however, be concerned by the determination to deport migrants established in the US economy.

Trump acknowledged that taxing US consumers of foreign goods via tariffs may be inflationary. There are four ways prices may rise. The tax itself is paid by US importers, and is likely to be passed to consumers. US firms face less competition, allowing them to raise prices. Wages may rise in response to higher prices, pushing up costs. Retailers may engage in profit-led inflation under the narrative of the tariffs. Washing machines are a good example—US tariffs have been repealed, but US washing machine prices are still up 20% from 2017 levels (when prices elsewhere are generally lower)…

... finally, an economic look at the week ahead (with a visual of FF changes expected …)

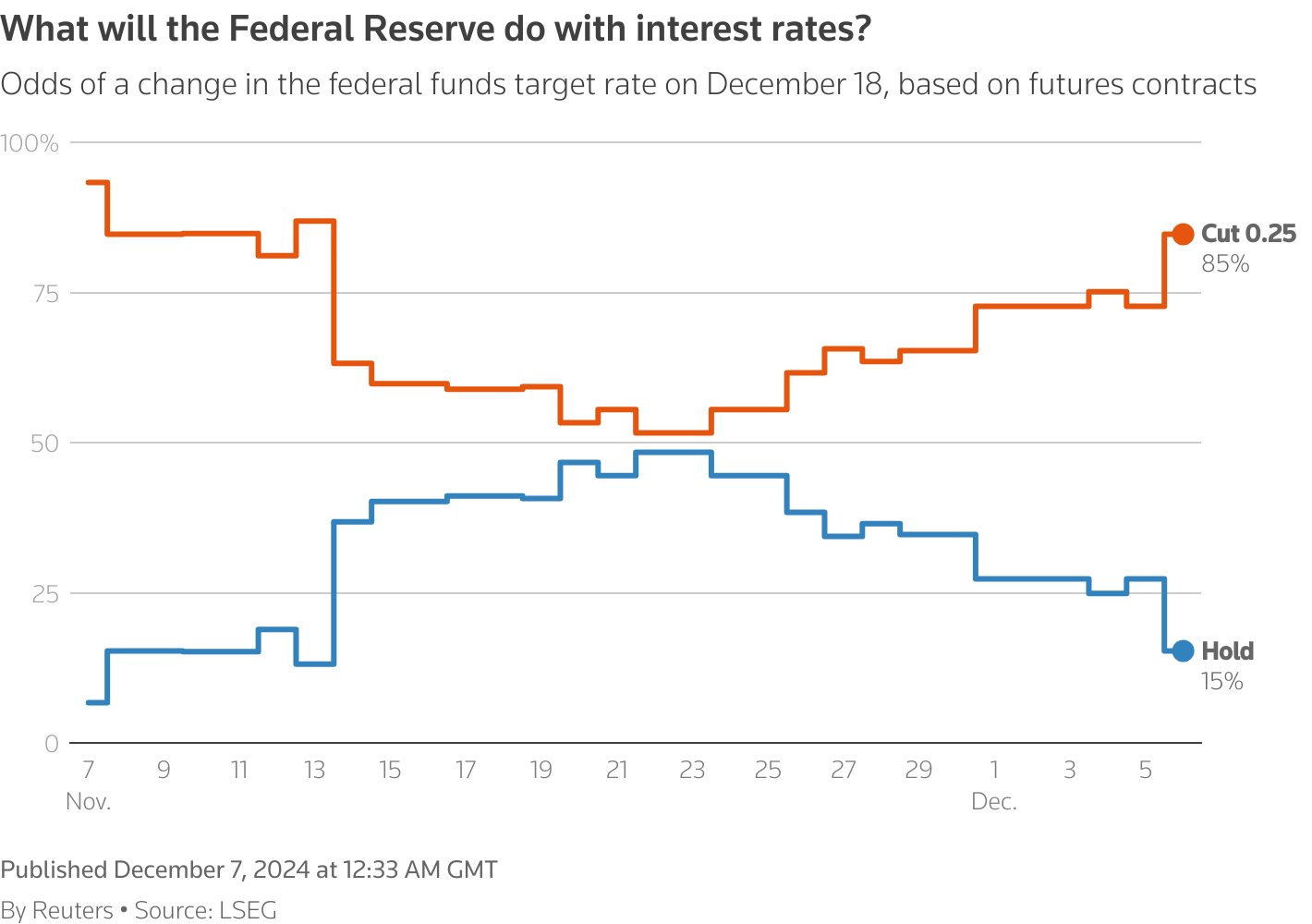

The economic week ahead is chockful of inflation updates. We're expecting stickier inflation readings that should ruffle the feathers of the Fed's doves. The FOMC is in a blackout period ahead of its December 17-18 meeting, meaning FOMC members won't be able to comment publicly. If the CPI news changes their minds about cutting the federal funds rate (FFR), they'll have to plant a front cover story in The Wall Street Journal. Current CME FedWatch odds show an 85% chance of a 25bps cut, and FFR futures show at least one more cut early next year (chart).

Further FFR reductions are likely to overheat the economy and the stock market, in our opinion. The 75bps of cuts since September 18 may have done that already. Optimism over Trump 2.0 should do enough to keep the Roaring 2020s roaring without additional rate cuts, and we expect that to be reflected in November's NFIB small business survey (Tue).

… And from Global Wall Street inbox TO the WWW … First up an OpED from The Terminal which recaps Friday’s NFP (just what you were hoping for … another opinion) … ‘last hurrah’ ?

Bloomberg: Syria surprise — markets need to rethink Putin’s ‘genius’

… Unemployment Down, Inflation to Go Another non-surprise on the road to the Federal Open Market Committee’s last meeting of the year: November’s nonfarm payrolls came in almost exactly as expected. The previous month’snear-zero print as labor strikes and two hurricanes hit the US southeast had set the stage for a huge rebound.Despite an upward revision of about 36,000 jobs, October remains the weakest month since the pandemic. For November, nonfarm payrolls rose 227,000, slightly above the 220,000 estimated bytheconsensus of economists surveyed by Bloomberg.

Growth was powered by service sectors such as leisure and hospitality, health care, and education — complemented by a bounce in construction and manufacturing, sectors that were likely impacted by the hurricane and labor unrest in October. Smoothing out the last two months’ volatility, growth averaging 173,000 jobs in the past three months pales compared to the robust 200,000-plus figures typically seen earlier this year.Is this enough sign of a deterioration? Not entirely.

Unemployment inching up slightly to 4.2% points to a normalization, says Glenmede’s Jason Pride. A jobless rate around the low 4% range is roughly consistent with the natural rate of unemployment — that is, the baseline level of joblessness that persists in a well-functioning economy due to frictional and structural factors. “Sub-4% unemployment was not sustainable over the long-term,” Pride says. “But the low-to-mid 4% range could be thelevel that unemployment sits at for some time in a steady-state, late-stage expansion.”

The fine line between labor market deterioration and normalization is not lost on investors. The slower-than-expected growth in the Institute for Supply Management’s index of services activity for November is a sign that the largest part of the economy is losing steam. As the payrolls data rolled in, US Treasuries, sensitive to Fed policy decisions, rallied. That’s because a cut this month from the Fed, rather than a pause, is now deemed the most likely outcome. Subsequent consumer sentiment data from the University of Michigan, showing an uptick in inflation expectations, reined in the rate cut sentiment only a little:

The optimism of a December cut shows up in Bloomberg’s World Interest Rates Probabilities function, which derives implicit policy rate probabilities from futures and swap prices. The following chart shows the chance of a quarter-point cut at the next meeting increasing to 85% from about 70% a day earlier:

As the markets increased bets for the Dec. 18 cut, the JPMorgan Emerging Market Currency index got a marginal boost, as lower interest rates in the US will ultimately see investors seek higher returns elsewhere:

That said, with November’s inflation report to come this week, additional easing is still not seen as guaranteed. Federal Reserve Bank of Minneapolis President Neel Kashkari says the decision remains highly dependent on Wednesday’s CPI print. Should prices surprise to the upside, confirming the nascent sticky services inflation trends, there’s every chance of a selloff. Brandywine Global’s Jack McIntyre says that November’s labor print was as expected, explaining why there was no significant repricing of Fed expectations in 2025:

It allows them to ease this month, but next week’s CPI release could change that outcome. We think the Fed shifts to a more patient tone (think slow and steady) as there is no pressure for them to increase the scale of monetary easing going into 2025. The Fed’s terminal rate is going to be equally as important as the path of how they get to it.

Beyond this meeting, the greatest perceived risk is of economic overheating (which might be exacerbated by the incoming administration’s expansionist approach).The economy grew at2.8% in the third quarter. Should that reach 3.3% as the Atlanta Fed estimates, it will exceedthe Congressional Budget Office’s 2% projected long-run GDP growth. On this premise, Apollo’s Torsten Slok sees a potential for a Fed tightening. As in the mid-1990s, the Fed might lack a clear direction for a while.

… AND another crack at #2025 dart-throwing contest …

he stock market climbed to all-time highs, with the S&P 500 setting an intraday high of 6,099.97 and a closing high of 6,090.27 on Friday. The index gained 1% last week. It’s now up 27.7%year to date and up 70.3% from its October 12, 2022 closing low of 3,577.03…

… Below is a roundup of 14 of these 2025 targets for the S&P 500, including highlights from the strategists’ commentary….

… Two things about one-year price targets Most of the equity strategists TKer follows produce incredibly rigorous, high-quality research that reflects a deep understanding of what drives markets. Consequently, the most valuable things these pros have to offer have little to do with one-year targets. (And in my years of interacting with many of these folks, at least a few of them don’t care for the exercise of publishing one-year targets. They do it because it’s popular with clients.)

So first off, don’t dismiss their work just because a one-year target is off the mark.

Second, I’ll repeat what I always say when discussing short-term forecasts for the stock market:

⚠️ It’s incredibly difficult to predict with any accuracy where the stock market will be in a year. In addition to the countless number of variables to consider, there are also the totally unpredictable developments that occur along the way.

Strategists will often revise their targets as new information comes in. In fact, some of the numbers you see above represent revisions from prior forecasts.

For most of y’all, it’s probably ill-advised to overhaul your entire investment strategy based on a one-year stock market forecast.

Nevertheless, it can be fun to follow these targets. It helps you get a sense of the various Wall Street firms’ level of bullishness or bearishness.

I think RBC’s Lori Calvasina said it best in her outlook report: The price target “should be viewed as a compass as opposed to a GPS. It is a construct that helps to articulate whether we believe stocks will move higher and why.“