weekly observations (12.09.24): URATE UP, yields down; UST "Liquidity has deteriorated moderately over the past two months"; 2025 surprise -- a Japan BID for bonds?

Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

10yy WEEKLY: 4.00% noted as it REMAINS both psychologically and technically significant over the past several years …

… bullish momentum, lower rates ahead despite or because of supply and data

… I’ll leave it to YOU to decide if price follows data and narratives OR if narratives follow data following price and so, once decided which comes first, then you’ll know which to pay attention to, first…as the dust settled on the week just passed, clearly the URATE a bullish occurrence as far as ushering Santa PAUSE out the door …

ZH: Big-Tech, Bitcoin, & Bonds Bid On 'Bad' Data; Rate-Cut Odds Surge On Week

… so bad is good, right, k, got it …

Lets deal with a couple / few things items from the week just passed (in other words, a couple snarky ZH links which contain visuals and info graphics helping tell the tale of markets — INCLUDING rates — which you may / may not have already stumbled upon) … A few curated NFP related links for your dining and dancing pleasure …

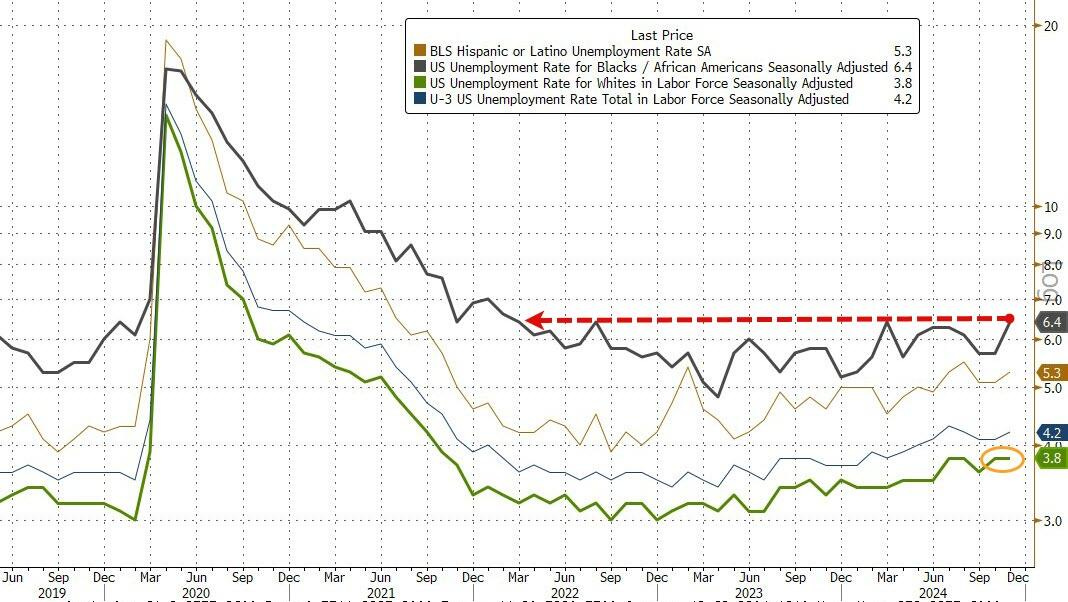

ZH: November Jobs Surge Above Estimates As Wage Growth Comes In Hot, Unemployment Rises

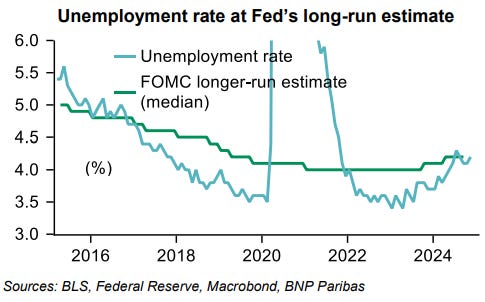

… Those looking for a clear indication whether the Fed will keep cutting or halt its easing cycle in two weeks, will have to wait because the rest of the jobs report was mixed: on one hand, unemployment rose from 4.1% to 4.2%, and above the 4.1% estimate (with Black unemployment at 6.4% rising in November, while the jobless rates for adult men (3.9 percent), adult women (3.9 percent), teenagers (13.2 percent), Whites (3.8 percent), Asians (3.8 percent), and Hispanics (5.3 percent) showed little or no change over the month)...

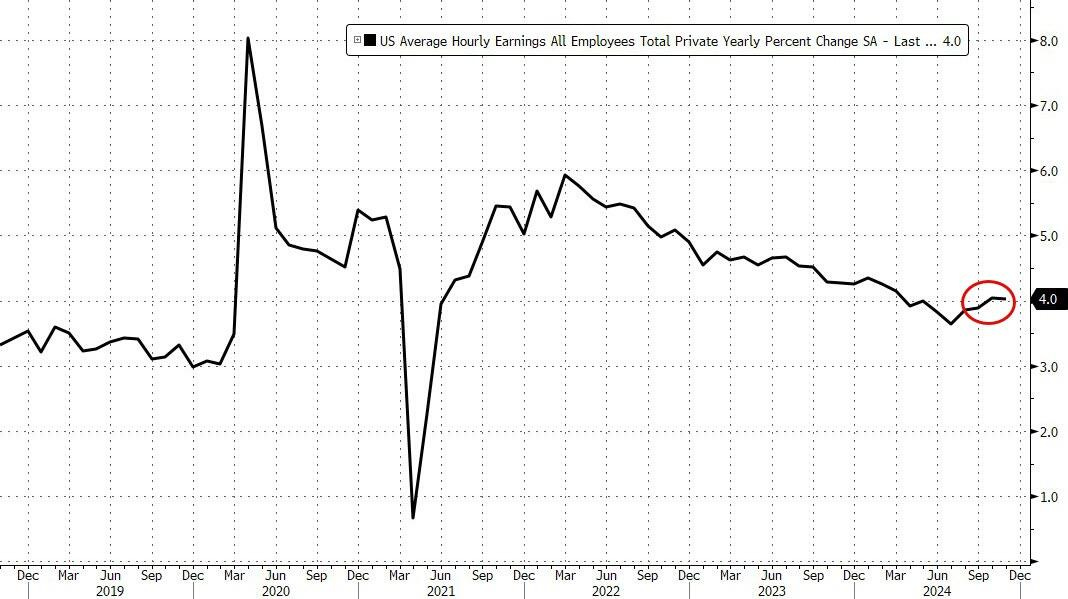

...but hourly earnings also rose, rising 0.4% MoM in November, above the 0.3% estimate, with annual wage growth flat at 4.0%, also above the 3.9% estimate, both indicating that wage growth pressures remain.

ZH: "The Market Is Pricing A December Cut": Wall Street Reacts To Today's Solid Jobs Report

… AND a few more curated words / links for your review …

Will remain very data dependent. Will point to unemployment rate as a reason to remain vigilant, but will also have to address the strength of ADP and Establishment versus the Household. I think that holds them in check and they won’t commit to cutting more at next meeting.

The small rise in wages, couple with other hints of inflation, which is likely to tick higher as some companies are buying up merchandise ahead of “expected” Trump tariffs.

That will definitely be something Powell is forced to highlight.

Should be a “neutral” to mildly hawkish 25 bps, as the underlying data, away from the unemployment rate, based on back to back bad months in the Household survey, is likely to be deemed the outlier.

This could be the “final” squeeze of this recent short squeeze and I expect yields to tick higher, possibly later today, but definitely early next week.

I think relatively indifferent for stocks, but given how excited people have gotten about the market, they will need more data or news to drive prices higher, and I think we are in a “lull” out of D.C. where the next set of comments from President Elect Trump will likely to be ramp up the chaos level to reset negotiation starting positions even further apart from those whom he plans on negotiating with!

Bonddad: November jobs report: the expected monthly rebound masks deeper declining trends

CalculatedRISK: November Employment Report: 227 thousand Jobs, 4.2% Unemployment Rate

WolfST: Labor Market Doing Fine. The Fed Can be “Careful” with Rate Cuts. Maybe Time for Some Wait-and-See?

Payrolls & wages jump, prior 2 months revised higher, solid bounce-back from Hurricanes and Boeing strike. 3-month average payrolls +173,000!

… with NFP in mind (more recaps / victory laps by Global WALL below), also worth noting some other data and snark (or reality … call it whatever you will) …

ZH: Trump Victory Sparks Biggest Jump In Consumer Sentiment Since Clinton In 1992

… Ok I’ll move on AND right TO the reason many / most are here … some WEEKLY NARRATIVES — SOME of THE VIEWS you might be able to use where THIS WEEKEND, a few things which stood out to ME from the inbox along with ALL things NFP recap and victory lap related …

… The Price is Right: BofA Bull & Bear Indicator says no global exuberance; but froth forming in crypto (bitcoin >$2tn market value…11th largest economy in world), S&P500 (5.3x price to book ratio now exceeds March 2000 high – Chart 6)…Q1 overshoot risk high (US$ breaking parity vs Euro, SPX melt toward 6666); Fed likely easing Dec 18th unless Nov US payrolls >275k (Chart 3), AHE >0.3%.

The November report signals more labor market slack despite strong job and income gains. We think the FOMC is likely to pay close attention to the unemployment rate, which increased again, and could downplay the job gains as payback effects. We maintain our call for a 25bp Fed rate cut in December.

… AND same firm w/a weekly econ recap noting the friction of economics & politics …

BARCAP: Global Economics Weekly: Policy rates and political rumble

Robust US jobs growth, combined with higher unemployment, supported market optimism: allowing for further Fed cuts, but not signaling a collapse in growth. Meanwhile, developments in France and Korea kept politics in focus. Next week, we expect the ECB to cut 25bp and have an eye on US CPI…

…US Outlook It's getting more complicated With the jobs report showing more slack despite solid income and job gains, we reiterate our call for another 25bp Fed cut in December. However, we think that disagreements about the neutral rate will make an FOMC consensus more challenging in upcoming meetings.

Much as we expected, November's employment report showed a strong post-strike and post-hurricane rebound in job gains, with upward revisions to prior months. Estimates of average hourly earnings and payroll income were also robust, sustaining solid fundamentals for household spending. The unemployment rate posted a surprise increase from 4.1% to 4.2%.

Pre-blackout communications reiterated the FOMC's conviction that policy remains restrictive and that inflation remains on course for a sustained return to 2%. Although inflation, output growth and the employment rate in 2024 are all likely to exceed median September projections, we think signs of renewed labor market slack will give the FOMC enough confidence to cut in December.

Next week, the FOMC will see November CPI estimates, which we expect to show a modest deceleration in the core component, from 0.28% m/m (3.3% y/y) to 0.25% m/m (3.2% y/y), consistent with some slowing in core PCE prices. Preliminary reports point to solid post-Thanksgiving sales, hinting at a strong November retail sales estimate just before the meeting.

… best in show took profits in long Jan FedFunds and are now are in SOFR Z5/Z6 flattener …

In the week ahead, the final factor in determining whether the FOMC has the needed cover to cut rates later this month will be revealed by the November inflation data. Wednesday’s core-CPI print will do the bulk of the heavy lifting for the market's expectations in this regard. Nonetheless, the combination of CPI, PPI, and Import Prices will be known before the end of the week – as well as reasonably accurate core-PCE predictions. The resulting information will define the tone of the Fed’s decision, which we continue to see as erring on the side of lowering rates on December 18th. It’s worth considering how big of an upside surprise the Fed could absorb and still cut rates. Given that the current coreCPI consensus is +0.3%, it is reasonable to anticipate that a low +0.4% move that is accompanied by a more moderate move in core-services ex-shelter (i.e. supercore) would fall within the range of acceptability. However, a high +0.4% or a +0.5% would be sufficient cause for a pause from the FOMC…

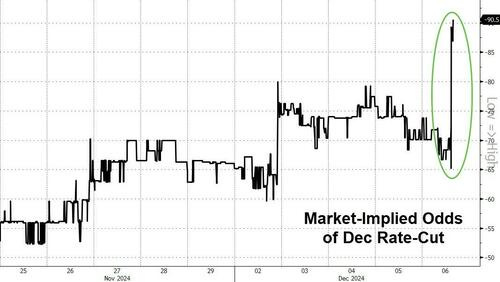

…The Treasury market found solace in the jobs report as 2-year yields moved below 4.08% on improving odds of a 25 bp cut – which currently stand at 88%. Inflation will have the final say on these expectations – at least in terms of the fundamentals. In the event of firmer core-CPI that doesn’t conform with a pause, one should anticipate the Fed to once again utilize the communication channel of the financial media. We’re encouraged by the steepening move that followed payrolls and brought the 2s/10s curve to the 20-day moving-average of 6.6 bp. Our expectations are for the momentum behind the current steepening trend to extend the price action above 10 bp, even if it will take the fundamentals of benign inflation to drive a more significant steepening breakout that challenges the Bollinger Band top of 15.8 bp …

… in this next note, a large French bank weighs in on NFP solidifying a Dec CUT (no more Santa PAUSE for you …!) …

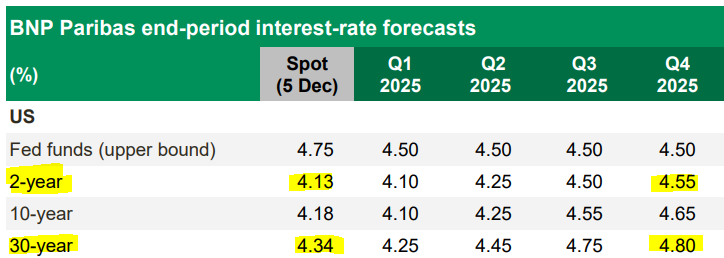

BNP: US November jobs report: Reinforcing December rate-cut call

KEY MESSAGES

The 227k gain in November nonfarm payrolls embeds expected rebounds from storm and strike impacts in the prior month, suggesting that the trend pace is nearer 150k excluding those special factors.

There were positive signs in cyclical sectors ex-manufacturing and stronger wage inflation.

Nevertheless, we think the rise in the unemployment rate to 4.2% increases the likelihood of our base case that the Fed goes ahead with a rate cut at the December FOMC meeting.

… setting NFP aside, French looking towards 2025 …

BNP: Global Outlook 2025: Navigating unpredictability

We adopt a scenario-based approach to navigating the 2025 economic and market outlook, with policy unpredictability implying plenty of two-sided risks.

In our central case, US growth settles into a soft landing in early 2025 before idling into 2026 as the impacts of import tariffs and immigration policies outweigh more pro-growth initiatives.

Uncertainty and the return of inflationary pressures in H2 2025 look set to keep the US Federal Reserve on hold throughout 2025.

China is likely to make the fiscal and monetary moves required to meet the authorities’ minimum acceptable 4.5% GDP growth rate in the face of US tariffs.

We cut our 2025 GDP growth outlook for the eurozone and see near-term risks skewed to the downside as geopolitics and local political uncertainty weigh. However, US policies could prompt a bolder European policy response and thus a brighter medium-term outlook.

Higher US import tariffs are likely to be particularly negative for growth in open EM economies.

We expect the market to shift to price in higher US inflation and fewer rate cuts than it currently does.

Our forecasts put the end-2025 2y yield differential between the US and Germany at about 45bp wider than forwards currently imply.

Given our expectation of widening front-end interest rate spreads, we expect EURUSD to fall to parity in 2025.

We also see further upside for the USD against the CNY, MXN, CAD, SEK and CEE3 currencies.

Bearish pressures are likely to develop on crude oil prices in H2 2025, as tariffs sap demand growth.

A stronger USD and an on-hold Fed will keep a lid on gold prices into H2 2025, in our view, after hitting new highs in early 2025.

… a diversion away from payrolls for just a moment and one worth noting ahead of this coming weeks supply of USTs …

Today’s chart introduces our new Treasury Illiquidity Index…A higher index value corresponds to reduced market liquidity…

As shown in the chart, market illiquidity has increased somewhat over the past two months, with a sustained rise around the presidential election in early November. Potential factors behind the deterioration in market liquidity could include uncertainties around the implementation of tariffs, fiscal policy, and the Fed easing cycle, as well as the market repricing over the past few weeks. Although the index remains lower than levels registered during the second half of 2022 to the end of 2023, the recent rise raises questions around whether we could see a further reduction in liquidity going into next year.

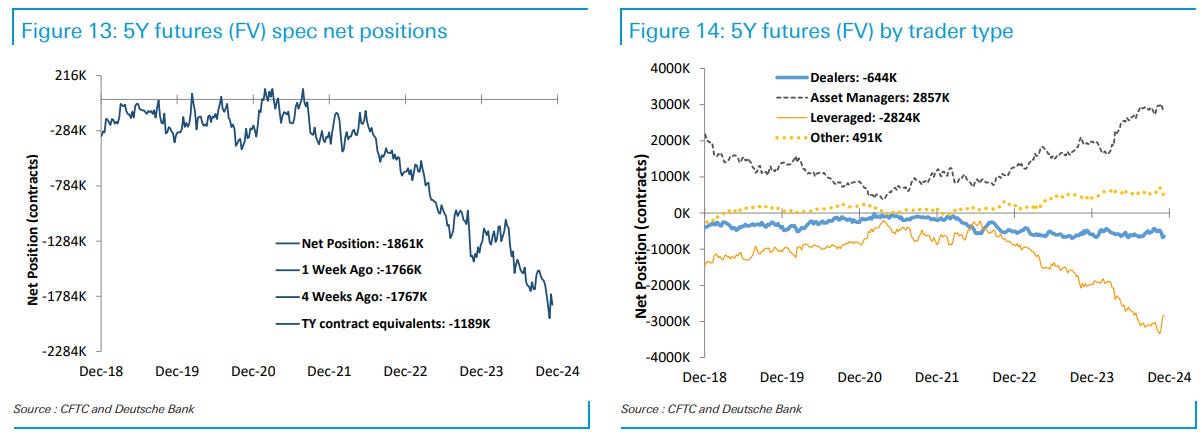

… same shop talking about speculative positions as it seems to be an increase in 5yr shorts (perhaps driving some of the price action …?) …

…Seeing the slowing trend in the labor market, and given its Keynesian worldview, that it probably has enough room to cut rates again by a quarter point on December 18, but markets will have to wait and see whether the process of rate cuts will continue in January. Our forecast right now: the Fed will see that inflation is still a threat and slow the pace of rate cuts, starting with a pause in January.

… anyone hearing the lion roar …

ING: Softish US jobs report favours a December rate cut

US non-farm payrolls rose broadly in line with expectations after recent strike and hurricane distrortions, but unemployment picked up by more than expected. With valid questions over the quality of the jobs the US is currently creating, we continue to expect the Fed to cut the policy rate 25bp on 18 December

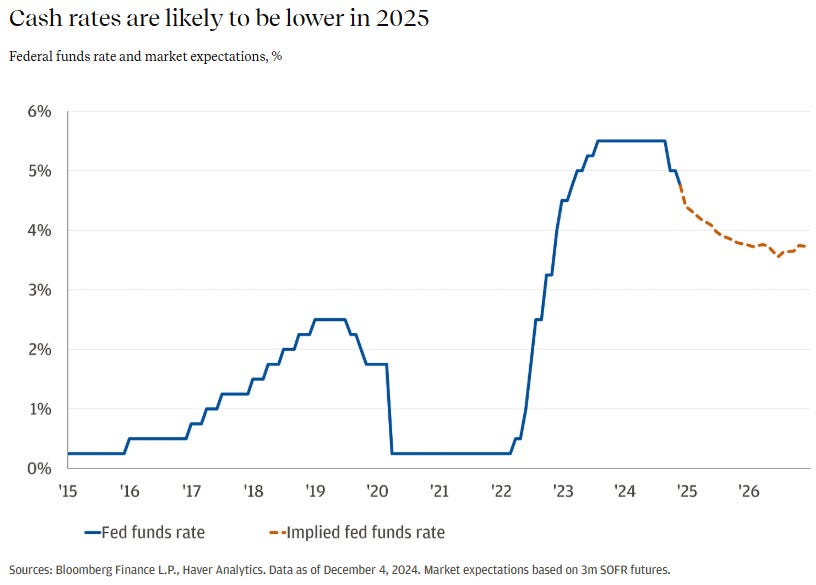

… Cash yields are likely going to continue to fall. We said coming into 2024 that cash rates would move lower. That’s happened—and we believe the trend will continue in 2025. The federal funds rate, which sets the rate banks can lend money to each other overnight (and is the biggest input for cash rates), stands at 4.75%, down 75 bps this year so far. The market is pricing another 85 bps of cuts next year.

Many think of cash as a safe haven or even a source of income when interest rates are high. But, as rates continue to move lower, we believe cash is likely to underperform other asset classes. Historically, in 10 of the last 12 cutting cycles, bonds have outperformed cash.

Cash is a necessary part of any lifestyle, but it’s not designed to beat inflation or produce long-term returns. What is? Equities. U.S. equities have historically returned 16% on average during soft-landing (our base case) cutting cycles.

Lower cash rates can present an opportunity for investors to consider moving out of excess cash and into assets that may have the potential for higher returns…

… recaps gettin’ old yet? hope not …

MS: Employment Situation: November rebound and upward revisions

A solid rebound in payrolls and upward revision are consistent with strong output & consumption growth in 4Q. The rise in the unemployment rate despite lower LFPR hinted at softening, but it reflected somewhat slower hiring rather than new layoffs. We continue to expect 25bp cut at the Dec FOMC.

…We continue to expect 25bp in Fed fund rate cuts in December. The Fed remains data dependent, but the data that would be most likely to change the Fed's path are the inflation prints, which we expect tame enough to allow further rate cuts.

… so, lemme get this straight, if the labor market ‘regaining footing’ does that justify increased rate cut odds … asking for a friend …

MS: Friday Finish - US Economics Weekly: The labor market regains its footing

The labor market has cooled but remains stable. Employment rebounded and growth in labor market income continues to outpace inflation. November CPI inflation should see another weather-related boost to goods prices, but we think the Fed remains on track for a 25bp cut in December.

Key takeaways

At 181k per month in October and November, employment gains are running ahead of 2Q and 3Q averages.

Growth in labor market income remains solid. The payroll proxy rose 5.2% 2m/3m saar through November.

We expect November headline / core CPI to move up by 0.27% / 0.28% m/m.

… same firm asking what’s on YOUR Global Macro BINGO card … Japan BUYING USTs to help keep this bid alive and well? got supply coming this week for them to dig in …

MS: Global Macro Market Bingo | Global Macro Strategist

Not many investors had lower UST yields into year-end on their 2024 bingo card. Not many investors have a US dollar bear market on their card for 2025. A full-fledged bond bull market may need a bit longer to begin, but we think the time is right to start positioning for the 2025 USD bear market.

… Interest Rate Strategy United States We discuss a likely 2025 surprise for Treasury market investors outside of Japan: investors in Japan will start buying Treasuries. In all of our year-ahead outlook scenarios, the policy rate differential between the Fed and BoJ compresses in 2025. This reduces the currency hedging costs to buying a USD-denominated bond for life insurance companies in Japan – making those purchases more likely. In addition, our projections for the curve between the Fed's policy rate and the 10y Treasury yield suggest a much-improved carry profile for Japan's mega banks.

We think investors should position for a higher market-implied probability of a 25bp rate cut at the January 29 FOMC meeting via receiving fixed on the January FOMC meeting OIS rate at 4.300% or buying the FFF5 fed funds futures contract at 95.64. Our economists expect the Fed to deliver a 25bp rate cut at the January meeting, but the market is not yet pricing in a full rate cut. We provide other rationale that supports a higher market-implied probability of a rate cut at the January meeting.

We recap the December-March Treasury futures rolls, which had their first delivery on Monday, December 2. Most contracts ended up trading flat through the peak liquidity period of the roll with the exception of the US contract, which richened about 2 ticks. In addition, all contracts richened into first notice, but it may have been difficult for most investors to capture this move as liquidity is often low.

We suggest investors exit paid the belly positions on the 2s3s30s 50:50 SOFR swap fly. Following the election, we stated that we were neutral on duration and curve in the US, but that stronger data into year end could move yields higher. We recommended this fly as a way to get indirect bearish rates exposure. Given the bond market rally, we no longer suggest this position.

… MORE on the URATE from the great white north, you hosers …

November's U.S. labour market data was largely as expected - a gentle slowing more consistent with normalization than cyclical weakness.

Absent a big upside surprise in October CPI next week that could raise the odds that the Fed chooses to pause rate cuts, we think the data's still soften enough to argue for additional rate cuts, and expect a 25-bps cut from in the December.

… and covered wagon folks weighin on NFP …

Wells Fargo: November Employment: Softer Than Meets the Eye

Summary The November employment report signaled that supply and demand in the labor market has come back into balance. Nonfarm payrolls grew a robust 227K in November, rebounding from an October reading that was depressed due to strikes and hurricanes. Over the past six months, nonfarm payroll growth has averaged a solid-if-unspectacular 143K per month. The separate household survey was underwhelming. The unemployment rate rose by one-tenth of a percentage point, the labor force participation rate fell onetenth, and the underlying details of the survey were indicative of a labor market that continues to lose momentum gradually. Perhaps the only "hot" component of the report was the 0.4% increase in average hourly earnings that pushed the year-ago change for wages back up to 4.0%.

On balance, today's employment data further reinforces our view that the FOMC will reduce the federal funds rate by 25 bps at its upcoming meeting on December 17–18. We do not think the labor market is positioned to be a source of inflationary pressure headed into 2025. Next week we will receive important inflation data for November from the CPI and PPI, and perhaps unexpectedly hot readings could still derail the FOMC's rate cut plans. But barring a major surprise, the FOMC is on course to cut rates once more before the year is out.

… Finally, Dr. Bond Vigilante talkin … stocks valuations …

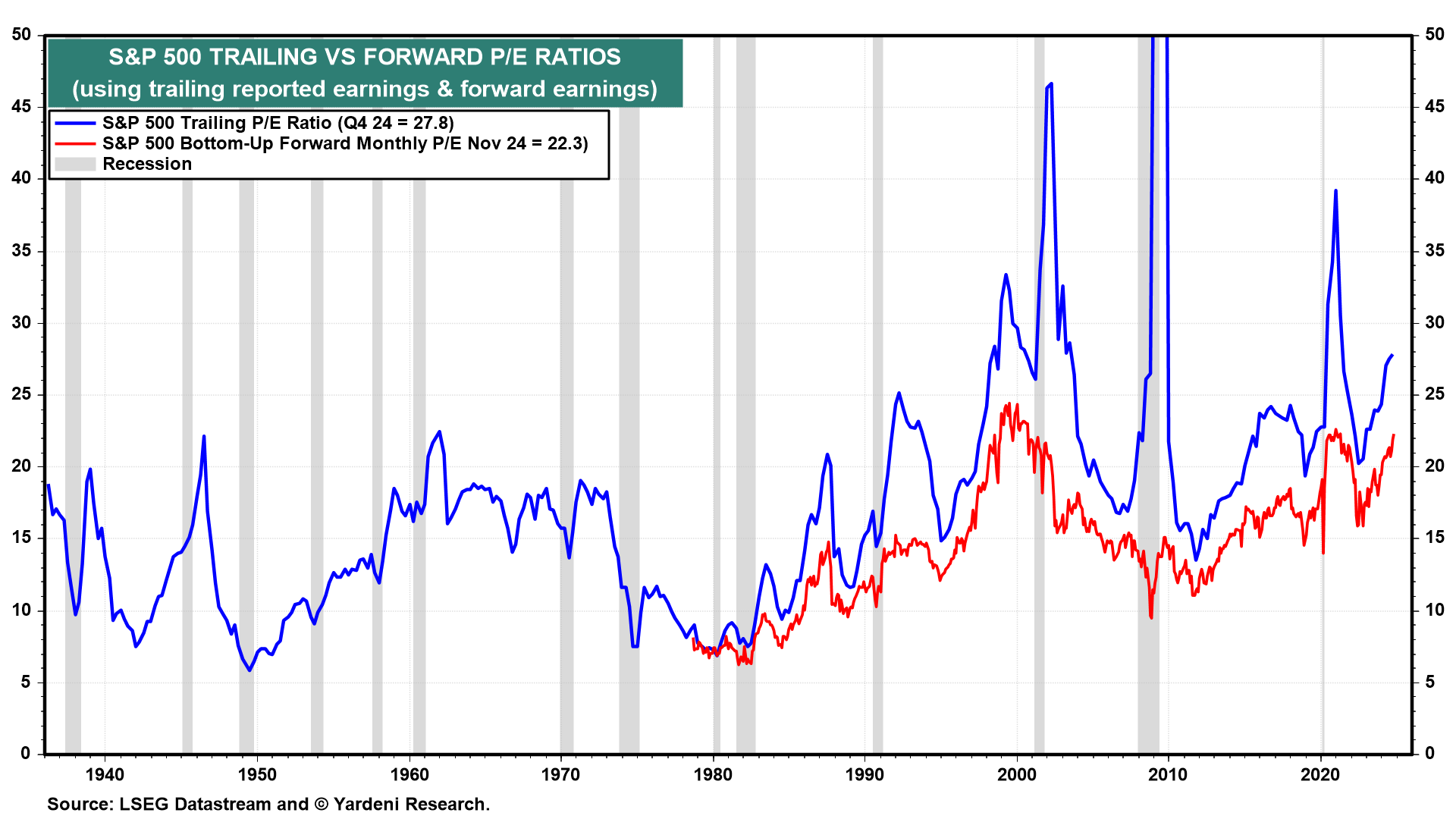

Yardeni: DEEP DIVE: Does the Stock Market Have a Valuation Problem?

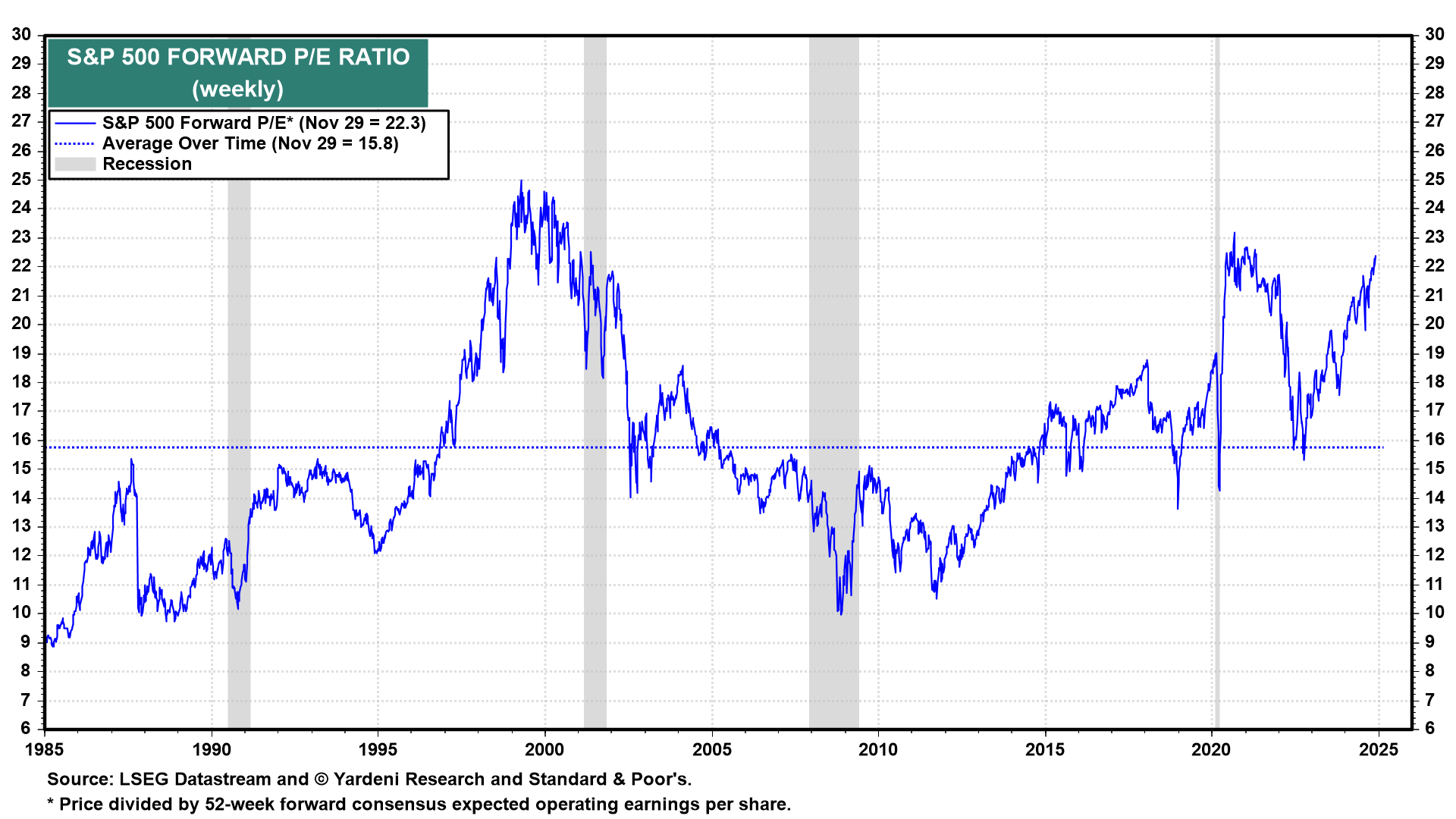

… Nevertheless, recession fears caused investors to slash the forward P/E for the S&P 500 from 21.7 at the start of 2022 to 15.3 on October 12, 2022 (Fig. 2 below). That was a 29.5% drop that was only partially offset by the 5.8% increase in forward earnings. The result was a P/E-led bear market.

Figure 2

Bear markets tend to bottom with forward P/Es well below the historical average of 15.8 (Fig. 3 below). But the latest one bottomed at a relatively high forward P/E because investors started to anticipate that recession fears might start to abate, as the economy proved remarkably resilient in the face of the significant tightening of monetary policy from March 2022 through August 2023.

Figure 3

So from 15.3 on October 12, 2022, the forward P/E rebounded impressively to 22.3 during the final week of November this year. That 45.8% increase in the S&P 500’s valuation multiple was bolstered by a 15.5% increase in the forward EPS. The result has been a solid bull market, so far, that has kept pace with the previous eight bull markets (Fig. 4 below).

… Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW … Batting in the lead off spot is the question nobody’s asked …

GDP growth in the third quarter came in at 2.8%, and the Atlanta Fed estimates GDP growth in the fourth quarter will be 3.3%, well above the CBO’s 2% estimate of long-run growth in the US, see the first chart below. In other words, momentum in the economy is strong, and the incoming administration may add additional tailwinds to the outlook.

Combined with the recent uptrend in inflation, the probability is rising that the Fed may have to raise interest rates in 2025, see the second chart.

In other words, a repeat of what we saw in the mid-1990s, where the Fed, after a few cuts, started raising interest rates again. Our weekly chart book with high-frequency indicators for the US economy is available here.

Source: BEA, Haver Analytics, Apollo Chief Economist

Bloomberg: Bill Gross Is On the Alert as Momentum Mania Sweeps Wall Street

(Bloomberg) -- Bitcoin rallying to the moon, meme stocks surging for no good reason, bearish bets cratering all at once…

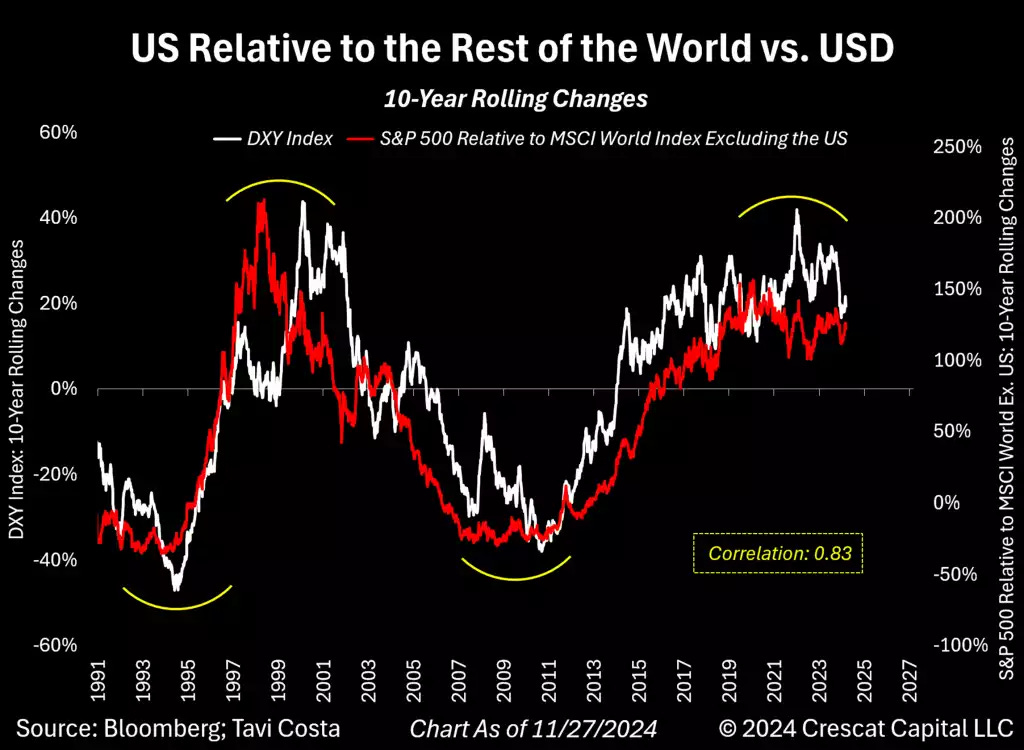

… everyone loves to hate on Tavi but some funTERtaining visuals nonetheless, esp as we collectively contemplate the future of the USD and it’s status …

… Observe in this chart, for example, the 10-year rolling performance of the US dollar, as measured by the DXY index, demonstrates a strong correlation (0.85) with the ratio of the S&P 500 to the MSCI World Index over the past three decades. Both lines now appear to be reversing direction, which may indicate a potential shift in the dollar’s trend.

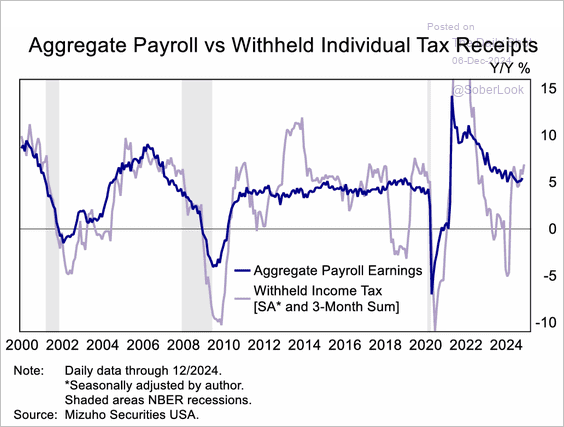

wage GROWTH = rate cuts?? must be so in the new math …

The United States: Stronger tax withholdings could indicate more robust wage growth.

… taking a longer view …

Longview Economics: What’s the Message of the Bond Market? Why is it Different from the Equity Market?

… Indeed, since US yields popped higher on Trump’s election, 10 year yields have softened, and moved further below their 200 day moving average yesterday (FIG 2); Chinese 10 year bond yields, meanwhile, have moved decisively below 2% in recent trading sessions (which is unprecedented, except for one day in April 2002), and are increasingly behaving in a manner similar to Japanese bonds in the 1990s (FIG 1). Added to which, German 10 year yields have been trending lower since October last year. Currently, they are sitting at the bottom end of that 12 month range (as are 30 year German government yields). Coupled with that, pessimism is widespread about the Eurozone economy. How is it going to cope with a Trump Presidency? How will it grow given its two main economies are currently in political turmoil? And, given Germany is now widely regarded as the ‘sick man of Europe’, which part of Europe will drive growth in the region?

FIG 2: US 10 year bond yields shown with moving averages

… here, a post leads with BBG visual of Dec FF cut chances and as always, Spectra does not disappoint …

A bit of a funny week as Waller laid out his conditions for a Fed cut, some other Fed members hinted a cut might not be necessary, the labor market data came in pretty solid, and… The cut got just about fully priced in anyway. With so much policy uncertainty in 2025, one might think that the path of least regret would be to wait, but the market doesn’t think that!

It is basically unheard of for the Fed to pass on a cut that is fully priced in, but I would say the disconnect between the guidance and the pricing is about as big as it ever gets. I am not saying they are guiding to no cut, but their guidance has not been suggesting of an 88.8% chance of a cut! But the market decides when the Fed will cut, generally, not the other way around. Oh, and here’s the Atlanta Fed’s excellent real-time measure of US GDP …

… did someone say Buffet? why, yes, yes they did …

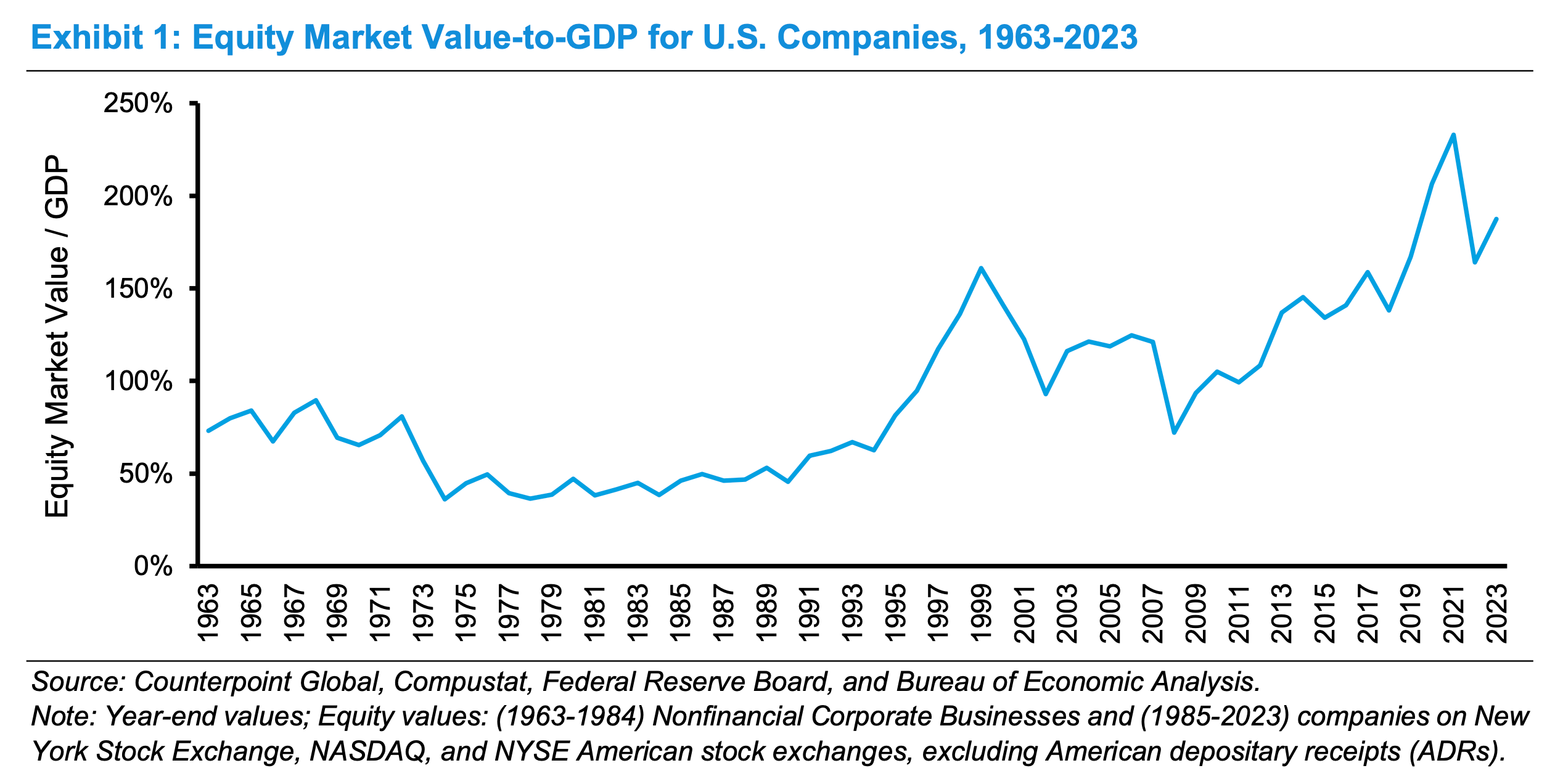

TKer by Sam Ro: Two problems with the so-called 'Buffett Indicator'

… In a 2001 interview with Fortune, the legendary investor pointed to what he then called “probably the best single measure of where valuations stand at any given moment”: the market capitalization of the U.S. stock market divided by U.S. gross national product (GNP).

When a valuation metric rises above some long-term average, the market is considered relatively expensive. When it’s below, it’s considered relatively cheap.

Buffett’s observation came near the peak of the dotcom bubble, which was about the time this Buffett Indicator was hitting new highs. A legend was born.

Today, the indicator is above levels seen during the dotcom bubble. In fact, it’s been up there for much of the past four years.

The Buffett Indicator is elevated. (Source: Morgan Stanley)

In a note published on Thursday, Morgan Stanley’s Michael Mauboussin identified two of them:

We use gross domestic product (GDP) in our analysis as it is the measure economists commonly reference today and is highly correlated with GNP. … There are a couple of reasons that the ratio of equity market capitalization to GDP may not be comparable over time. The first is that U.S. companies now get more of their sales from outside the U.S. than they did in past decades. GDP does not include those sales. That means the numerator, market capitalization, reflects a larger addressable market than what the denominator, GDP, captures. Second, GDP is arguably understated because it fails to measure accurately the quality of goods and services as well as the value of new goods and services. The rise of digitalization makes measurement today more challenging than in the past.

…The bottom line is that you should heed Buffett’s advice and be wary of putting too much weight into a single metric. Investing in the stock market just isn’t that simple.

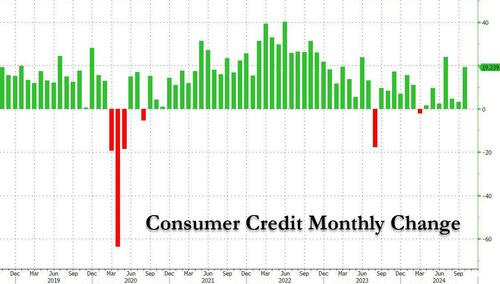

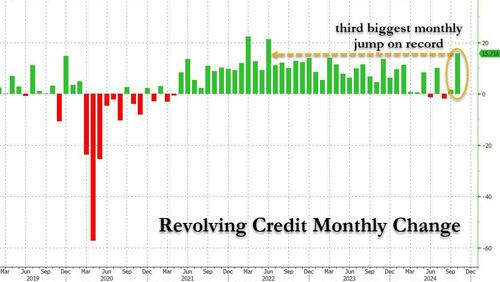

… finally, from ZH on Consumer Credit …

ZH: In "Last Hurrah", Credit Card Debt Explodes Higher Despite Record High APRs As Savings Rate Craters

In "Last Hurrah", Credit Card Debt Explodes Higher Despite Record High APRs As Savings Rate Craters

One month ago, when multiple discount retailers (here and here) were lamenting the sudden collapse in US consumer purchasing power, we highlighted the reason this unexpected hit to US consumption: as the US personal savings rate had collapsed, the growth in consumer credit was slowing, and in last month, the Fed reported that credit card debt growth posted its first decline since the covid crash.

But fast forwarding just one month later, when in a striking reversal, October consumer credit growth unexpectedly reversed the dramatic September slowdown, and soared more than $19 billion, to a new record high of $5.084 trillion.

… ... the highlight was that the much more consumer-outlook sensitive revolving credit (i.e. credit card debt) exploded, and in October surged the most since the covid crash and was - amazingly - the third biggest monthly increase on record!

But what was truly remarkable about the latest consumer credit data, is what the Federal Reserve's own website said was the average APR on credit cards across the US. Readers may recall that in September, just after the Fed's jumbo rate cut - the first rate cut in years - we made a prediction that while rates on deposits and savings accounts immediately dropped, interest rates on debt - such as credit card APRs - will barely budge (if not keep rising)…

…This collapse in savings explains why most US consumers are not only living paycheck to paycheck, but have maxed out both their Buy Now, Pay Later accounts and, as we now learn, their credit cards too as everyone braces for the moment when the US economy suddenly grinds to a halt and collapses under the weight of its own debt.

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

AND THAT is all for now. Enjoy whatever is left of YOUR weekend … be it football or some gal givin’ a concert up north … I’m done for now, may be more before markets open Sunday night OR perhaps then just Monday morning …

The Yardeni bull Market chart since 66 is quite something never seen a breakdown likes that 👌looks like I had luck behind me when I invested my 1st $4,000 in 1994. Awesome chartbook download I'll get right on that soon as I catch up on Syria!

If you're in NJ, this maybe coming to a town near you....

Let's turn "Jersey" MAGA Red !!!!

https://nypost.com/2024/12/07/us-news/republican-who-helped-trump-win-pennsylvania-sets-sights-on-nj/?utm_source=aol&utm_campaign=nypost&utm_medium=referral

The Yardeni bull Market chart since 66 is quite something never seen a breakdown likes that 👌looks like I had luck behind me when I invested my 1st $4,000 in 1994. Awesome chartbook download I'll get right on that soon as I catch up on Syria!