Reuters: Trump-victory trades to swell after shooting, investors say

… Before the shooting, markets had reacted to the prospect of a Trump presidency by pushing the dollar higher and positioning for a steeper U.S. Treasury yield curve, and those moves extended a little in Asia trade on Monday morning …

… Under Trump, markets expect hawkish trade policy and looser regulation over issues from climate change to cryptocurrency. Bitcoin is up roughly 7% since the shooting.

Investors also expect an extension of corporate and personal tax cuts, fuelling concerns about rising budget deficits.

That could drive bond selling, said Michael Purves, CEO of Tallbacken Capital Advisors in New York and potentially add to inflation as interest rates fall.

"If (Trump) wins and does this stuff he said he is going to do, you are going to see a much bigger selloff in the back-end of the bond market,” he said. “I think the bond market is the big (election) trade this year, rather than equities.”

Trump also said in an interview in February he would not re-appoint Federal Reserve Chair Jerome Powell, whose second four-year term as chair will expire in 2026 …

AND with that in mind, a few words recorded BEFORE the weekend developments from BMO … “Doneflation” … this is the title of this past weekly podcast by none other than BMOs rate strategy group…

Every four years, athletes from around the world meet to compete in the Summer Olympic Games and this time there will be 329 events in 32 sports. We've been searching the list and while we've found Trampoline, Skateboarding, Table Tennis, BMX Freestyle, Badminton, and Artistic Swimming, we came up short on our dream of a Wonky Interest Rate Podcast event. But let's face it - we would never have qualified anyway. Maybe we will have better luck in 2028 -- after all, that year it will be in Los Angeles.

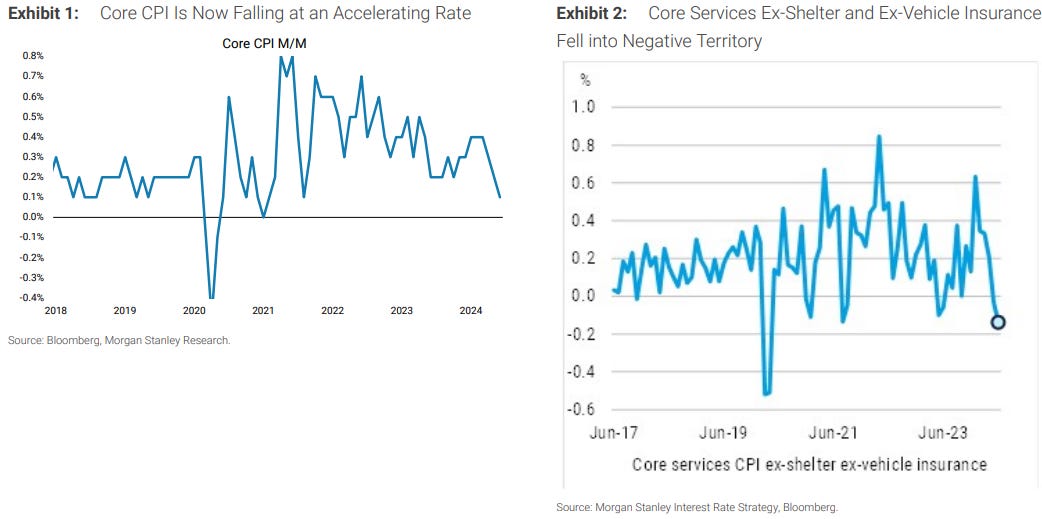

Episode 282: "Doneflation" is now available. This week, in addition to our ongoing shameless appeals for votes in the Institutional Investor survey, the team discusses the unexpectedly soft core-CPI (and supercore) data as well as galvanized expectations for a September rate cut despite the proximity to the Presidential election.

… It is readily avail for any / all if you know where to look … simply search for "Macro Horizons" on your favorite podcast app.

iTunes/Apple Podcasts

Stitcher

Google Podcasts App (which I believe has now been sunsetted) …

As good a way I can think to help pass some of these summer doldrums as we await next quarterly writeup from Dr. Lacy Hunt of HIMCO … BMOs podcast ALSO terrific for for any / all who might have missed the weekly writeup (HERE — link has been corrected, sorry for that) where it was noted their willingness to get long (5yy) on a dip.

Again, offered and noted it was cobbled together BEFORE this past weekends horrible events in PA and it is with THAT in mind, I’ll continue with a look at 5yy …

5yy DAILY: momentum is overSOLD and either rates go UP OR we’ve got to spend TIME AT A PRICE … Now, with TRUMP implications (see above), we might still see that year of the steepener but it just may be a more bearish one than previously thought? Whatever the case, it would appear a less opportune time here / now to be BUYING 5s IMO

… and as the world pivots back TO Global Wall and what SHOULD be a very quiet, summer doldrums week ahead with JPOW up at 1230p … a quick look at some developments from China o/n

ZH: China's GDP Growth Unexpectedly Tumbles As New Home Prices Plunge Most In 9 Years

… AND here is a snapshot OF USTs as of 616a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Initial strength in the USD sparked by the Trump assassination attempt fades, RTY outperforms & BTC > 62K … Bonds were initially subdued in reaction to the assassination attempt on former President Trump, pressure which has since pared … USTs were pressured overnight after the attempted assassination of former President Trump and the strengthening of his betting odds for the November election; USTs went as low as 110-24+, but were then lifted alongside a bid in EGBs in the European morning.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

BNP: Sunday Tea with BNPP: Unambiguously good progress

KEY MESSAGES

With US inflation cooling more rapidly than expected, we have brought forward our Fed call for the first cut of the cycle to September.

We think that risks are asymmetrically skewed toward lower yields ahead of the data this week.

All eyes will be on the start of earnings season, where we will be watching the airlines closely.

… After bringing forward our Fed rate call to September, we also added a 5s30s UST steepener. We favor 5s30s over alternatives such as 2s10s because the carry is less punitive and relies on an economic slowdown driving the depth of the cutting cycle rather than frontloaded cuts. Further, to the extent that expectations for the deficit remain poor or deteriorate, we would expect the long-end of the curve to be most negatively impacted. Notably, the 11 July 30y bond auction tailed 2.2bp, which may be a reminder of the ongoing deficitinduced record UST supply…

… Real Clear Politics has the probability of a Trump victory increasing from around 55% on Friday to around 65% as we type. On a state basis, the shooting took place in Pennsylvania, one of the three most important battleground states and one Biden almost certainly needs to win to be President given where current polling is. Before the weekend Trump was around 3.5% ahead in the state in the latest poll of polls. When Biden performed poorly in the debate 2 and a half weeks ago, Treasuries sold off 20bps in a couple of sessions as markets looked to price in a more fiscally loose Trump clean sweep. Since then there has been positive inflation data which has reversed that sell-off. With Japan closed overnight there is no US bond trading but Treasury futures are falling and are giving up much of the gains seen after Thursday's weak CPI print so expect yields to open a handful of basis points higher. S&P 500 (+0.19%) and NASDAQ 100 (+0.26%) futures are edging higher along with the dollar index (+0.12%).

Outside of the Presidential race, the most consequential event of the week could come today as Fed Chair Powell is interviewed at the Economic Club of Washington DC at 5pm London time. Will his tone take a notably dovish shift given the soft CPI print last week. Our economists new Fed forecasts would suggest he might as they now expect three cuts in the remainder of 2024 (Sep, Nov, Dec) as a mid-cycle adjustment before three more from September 2025. See "Keeping the expansion alive with 75(bps) before '25" for more. Eight other FOMC voters will also be on the radar this week (see them detailed in the diary at the end) so we'll have a good idea of whether the Fed are moving direction by the end of the week. Interestingly, our economists point out that back in December 2023 and March 2024 the Fed median forecasts from the SEP expected 75bps of cuts this year with unemployment at 4.0-4.1% and core PCE inflation 2.4-2.6% by year-end. Recent data suggest that reasonable year-end forecasts are now 4.0-4.2% for unemployment and 2.5-2.6% for core PCE…

MS: Sunday Start | What's Next in Global Macro: Breaking the Rules

It’s a general rule that you should avoid saying “This time is different.” So far, though, I have broken that rule in this cycle, because so much of what we are seeing is fundamentally different from past cycles. Other “rules” are being tested this cycle, and in my mind, I hear Mark Twain saying, “It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so.”

Rules for recession indicators have had a particularly tough time. We recently marked the two-year anniversary of the inversion of the 2y10y yield curve. While I have no doubt that at some point the US will go into recession, the rule that an inversion is the harbinger of recession has been violated. Similarly, when money supply growth (M2) turned strongly negative at the end of 2022, it was a clear sign of a slump for those who put stock in that measure of “money” or “liquidity.” Eighteen months later, money supply growth is positive again, and the economy remains solid. The ISM index has a long track record and over many cycles it has correlated well with activity, but it has been negative for 19 of the last 20 months without a recession. These false positives, to use a statistical turn of phrase, only reinforce how different this cycle is to those of the past…

…Our base case is that much like the other recession signals, the rise in the unemployment rate is another false positive. In the 1990s, arguably the other soft landing for the US economy, similar red flags were raised. The yield curve flattened almost completely; money growth ground to a halt, and the ISM was sub-50. Of course, a recession eventually followed, and I am sure we will have one in the future, but in the 1990s, it didn’t come for half a decade. History doesn’t repeat itself, but it does often rhyme. I don’t know that we have a half decade of expansion to go, but for now, we need to see other indicators to change our minds.

MS: Weekly Warm-up: What Does Falling Inflation Mean for Stocks?

Economic growth and inflation data have softened, setting the stage for rate cuts. In today's note, we dissect what this backdrop entails for equities. We maintain our preference for large caps, but believe there's a nuanced, relative call to make within small caps—long growth over value.

MS: The Weekly Worldview: What's Another Word for "Transitory"?

Last week's inflation data reaffirmed our long-held view that inflation is trending down. Measured housing inflation started to soften again, and services ex-housing surprised to the downside. These reinforce our call for a September cut and three cuts this year.

UBS: Violence and consequences (? shh, don’t anyone tell Paul but … he’s absolutely dead wrong as one can see RealClear poll GRAPH HERE who’s popped up to now 65% ?? Paulie … ‘not necessarily true’? )

The shooting at former US President Trump’s election rally during the weekend has provoked only a limited market reaction. Markets are concerned about policy probabilities, and while individuals may condemn acts of violence against political candidates, they will not necessarily change their policy projections. There is a popular perception that acts of violence against a candidate increase their support, but this is not necessarily true. Analysis is complicated by US polarization, and shorter news cycles from social media. This adds to uncertainty without necessarily changing policy probabilities…

… And from Global Wall Street inbox TO the WWW,

Bloomberg: Markets Will Digest Shock of Trump Attack (Authers’ OpED)

He’s the clear front-runner in their base-case scenario, but victory is not inevitable.

… Many talk of a “Trump trade” in which the bond market revolts at an agenda that seems almost designed to drive up the deficit and stoke inflation, from permanent tax cuts to sweeping tariffs. That would imply an end to rate cuts, and therefore, in all probability, the bull market in stocks. However, the dollar would be buoyed by safe haven flows as the world grew even more uncertain. David Roche of Quantum Strategy suggests that Trump 2.0, which he is now prepared to predict, would be good for the US dollar, but bad for most other financial assets.

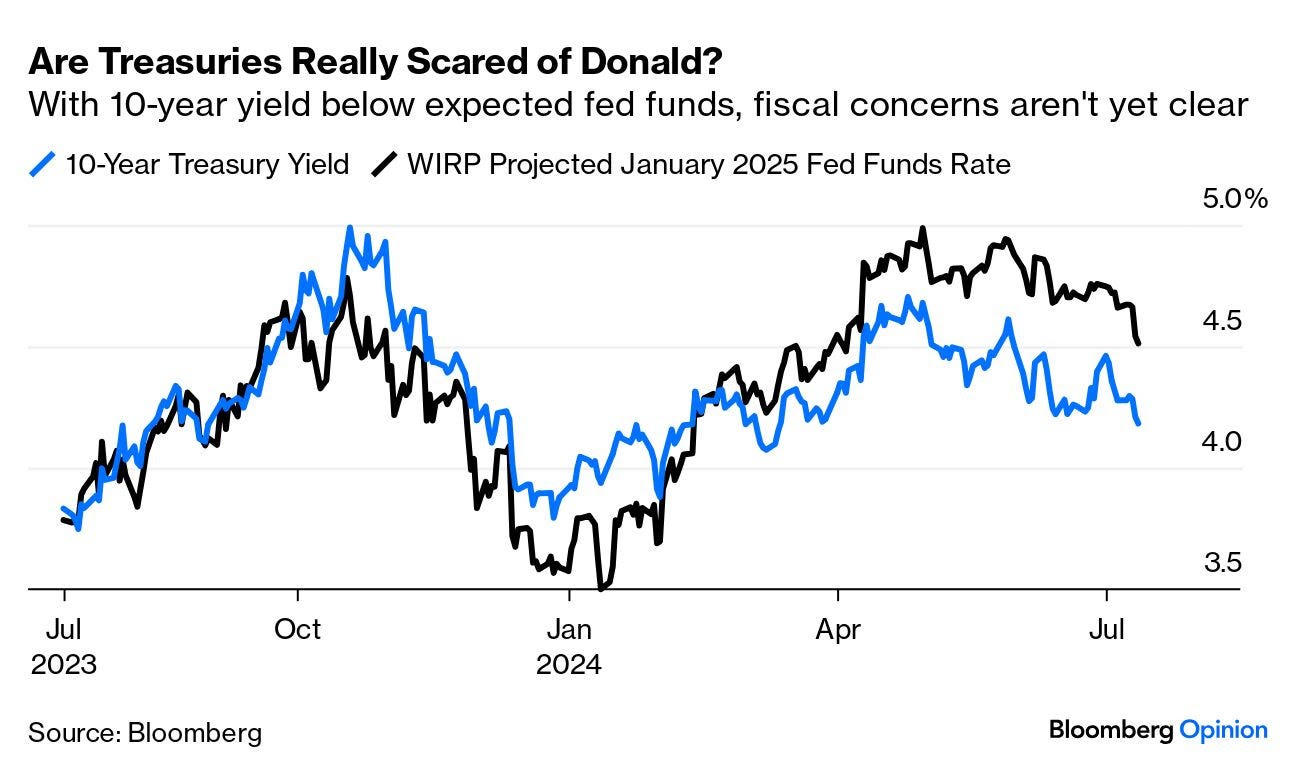

If there is any concern about this to date, it’s well hidden. Bond yields are moving in line with the expected course of the fed funds rate, and in recent months have reduced more than Fed expectations would suggest, despite Trump’s growing chances. There was a bond riot after Trump’s first victory in 2016, which came as a great surprise. At 1.85% on election day, the 10-year yield reached 2.6% before the year was out. Markets aren’t yet taking evasive action against a repeat:

Either traders don’t think it’s worth pricing in a Trump victory yet, or they don’t think he would be that bad for the bond market. The latter is more likely.

Sam Ro from TKer: One of the stock market's most consistent trends

The Babylon Bee:

Party That Called Trump 'Hitler' For 8 Years Shocked As Someone Tries To Assassinate Him

Will we ever get any Accountability out of the Biden Regime ????

http://trk.amgreatness.org/c/7/eyJhaSI6OTkyNjA2OTcsImUiOiJ2YW5oZXluaW5nZW5AeWFob28uY29tIiwicmkiOiIxMzc1NTM2OTQwIiwicnEiOiIwMi1iMjQxOTctMGEwZGQ5MjMzZjI5NGQ4MjgyZDQ3MDFjN2JhOGJjMzEiLCJwaCI6bnVsbCwibSI6ZmFsc2UsInVpIjoiIiwidW4iOiIiLCJ1IjoiaHR0cHM6Ly9hbWdyZWF0bmVzcy5jb20vMjAyNC8wNy8xNC9lcmlrLXByaW5jZS1uZWFyLXRydW1wLWFzc2Fzc2luYXRpb24tY2F1c2VkLWJ5LW1hbGljZS1vci1tYXNzaXZlLWluY29tcGV0ZW5jZS1ieS11LXMtc2VjcmV0LXNlcnZpY2UvP3V0bV9tZWRpdW09ZW1haWwmdXRtX3NvdXJjZT1hY3RfZW5nJnNleWlkPTk0MTEifQ/B4cuTpJWwkThqqEMcysUGQ