Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

Holy CRAP.

All that follows seems just a bit less important given news of the latest and literal ‘shot heard ‘round the world’ …

CNBC: Photos show Trump with blood on his face after shots fired at rally

While DJT is apparently fine, the shooter has been sent to meet his maker and another rally attendee has unfortunately succumbed to his injuries …

ZH: "I Was Shot": Trump Responds After Assassination Attempt; Shooter Dead; Secret Service Reportedly Ignored Warnings

… Now with this story only going to continue and likely to ‘hot up’ more in the days and weeks ahead and as I’m NOT qualified to comment other than to say how horrific an innocent bystander / rally attendee has been killed — thoughts and prayers to the families of ALL impacted …

I’ll carry on and back to somewhat more mundane macro economics and rates narratives of the moment …

10yy: it would appear to ME that a thick WEEKLY triangulating range being broken BUT at the very same time, it would seem to ME that momentum (stochastics, bottom panel) is becoming overBOUGHT …

… and we KNOW that either TIME at a price OR some ‘concession’ will be required to resolve this ‘overBOUGHT’ condition … diving a bit deeper into the DAILY, much the same …

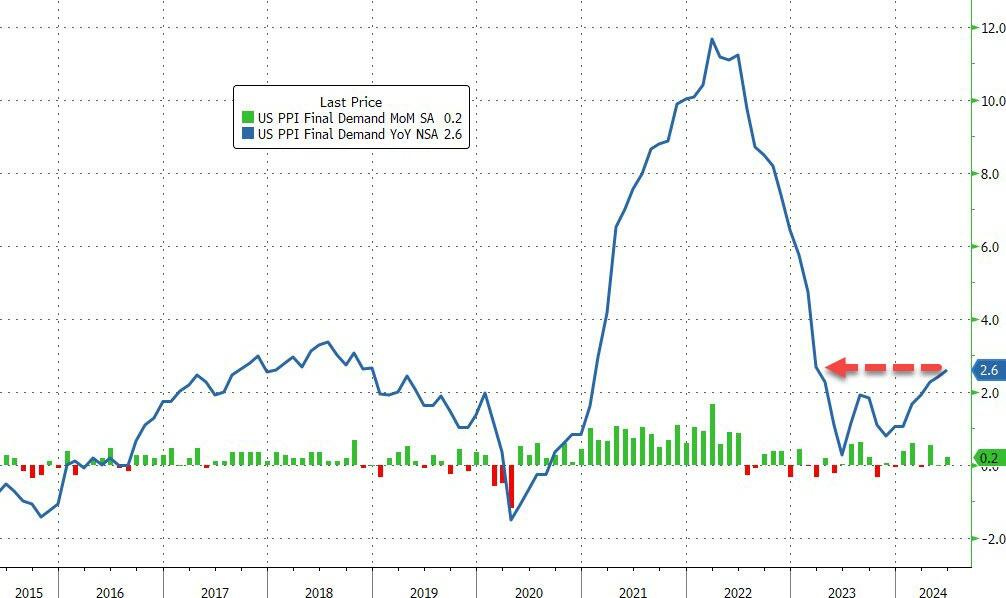

… AND from 10s TO a couple / few things items from yesterday … and is it ME or is it quite fitting to have a benign CPI followed by a … well … less ‘benign’ PPI

ZH: US Producer Prices Surge At Fastest Pace In 15 Months As Services Costs Soar

… After May's MoM deflationary impulse (thanks to a plunge in energy costs), June was expected to see a modest 0.1% rise (and we have seen energy prices starting to rise again). Sure enough, headline PPI printed HOT at +0.2% MoM (and May was revised higher), pushing the YoY print up to 2.6% (well above the 2.3% expected)...

Source: Bloomberg

That is the highest PPI since March 2023.

… and never to fear, UoMISSAGAIN is here …

ZH: "Stubbornly Subdued" - UMich Sentiment Slumps As Home-Buying Conditions Hit Record-Low

… UMich Director Joanne Hsu warned: "Although sentiment is more than 30% above the trough from June 2022, it remains stubbornly subdued."

"Nearly half of consumers still object to the impact of high prices, even as they expect inflation to continue moderating in the years ahead.

With the upcoming election, consumers perceived substantial uncertainty in the trajectory of the economy, though there is little evidence that the first presidential debate altered their economic views."

On the positive side, year-ahead inflation expectations fell for the second consecutive month, reaching 2.9%. In comparison, these expectations ranged between 2.3 to 3.0% in the two years prior to the pandemic. Long-run inflation expectations came in at 2.9%, down from 3.0% last month and remaining remarkably stable over the last three years.

However, these expectations remain somewhat elevated relative to the 2.2-2.6% range seen in the two years pre-pandemic…

… Ok I’ll move on AND right TO the reason many / most are here … some WEEKLY NARRATIVES … some of THE VIEWS you might be able to use.

THIS WEEKEND, a couple / few things which stood out to ME this …

With June's CPI inflation surprising to the downside amid gradual cooling of the labor market, we now expect the FOMC to cut rates twice this year, in September and December, and three times in 2025. We thus expect the fed funds target range to be 4.75-5.00% at end-2024 and 4.00-4.25% by end-2025.

BMO Weekly: Rhetoric on Deck (some highlights as they look to get long, buying dip, 5yy…)

… Our constructive outlook on Treasuries remains well intact, and we anticipate that this summer will see 10-year yields dip into 3-handle territory as dip-buying becomes thematic …

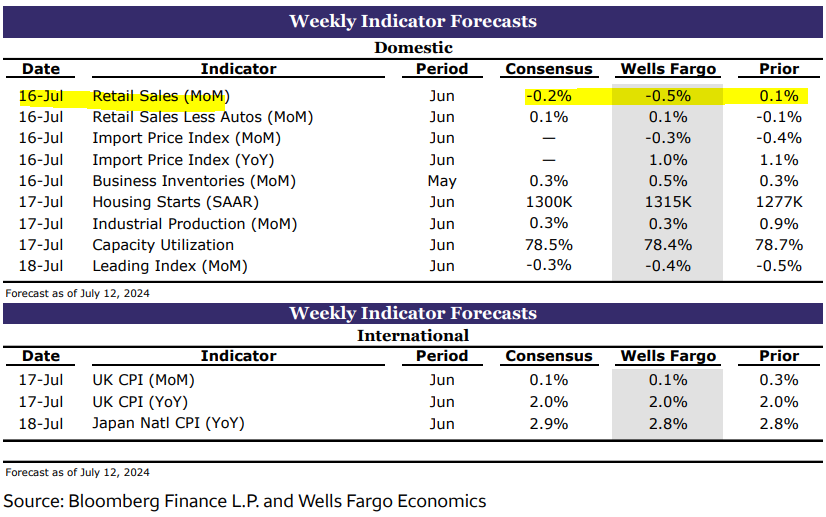

… For a new trade this week, we'll look to buy a dip in 5s in the event of a stronger-than-expected Retail Sales print on Tuesday. The control group beats 58% of the time in data for the month June, which is tied for the second most seasonally strong month of the year behind July (which beats 67% of the time). Our constructive outlook on Treasuries as an asset class has certainly taken solace in the fact that the bulk of the top-tier economic data over the last couple of weeks has shown mounting evidence of the lagged influence of tighter monetary policy. After all, the underlying bond bullish motivations that led 10-year yields back below 4.20% in the wake of CPI will not be changed by a firmer read on spending.

DB: Keeping the expansion alive with 75(bps) before '25 (AND … as data dust settles on week that just was … 3 rate CUTS being defended by Global Wall AND … with such precision, the guide on into 2025 … Global Wall is so good, smart and golly I wish I had as good a crystal ball …)

Recent data have showed a continued softening in the labor market and substantial cooling in inflation pressures, importantly in the shelter category. In response to these data, we have adjusted our forecast for the Fed. We now expect the first rate cut to come at the September meeting, followed by two more reductions in November and December. This would complete the 75bp mid-cycle adjustment the Fed has pursued during past cutting cycles outside of recessions (see the mid-1990s and 2019) and which has been part of our baseline view for some time (see “(Mid-cycle) Adjusting the Fed’s narrative for rate cuts”).

After the initial 75bps of cuts, we then see the Fed pausing their cutting cycle until September 2025, when they resume guiding the policy rate back to its neutral level of 3.5-4.0%. Specifically, we anticipate 25bp rate cuts in September and December of 2025 with a final cut in March 2026, which would put the fed funds rate near our unchanged estimate of nominal neutral (~3.75%).

Risks are skewed towards a more cautious approach by the Fed where they start on a quarterly basis. Such an approach could be realized if concerns about downside risks to the economy and labor market dissipate, or if inflation pressures prove more resilient over the coming months.

MS: Where Art Thou, Inflationistas? | Global Macro Strategist

The stickiness of US inflation has lost its tack. Proponents of higher equilibrium inflation have gone silent as recent data proved consistent with 2% or lower core PCE inflation. Downside risks to inflation from residual seasonality and a weaker labor market lurk. Stay in US curve steepeners.

… Interest Rate Strategy United States In the US, the latest June CPI print is good news for the Fed as officials have sought additional confidence around the progress of inflation in the last few months. That has involved a combination of (1) looking for cooler realized inflation readings, especially after upside surprises in 1Q24, and (2) expecting sustainability if inflation actually cools. The June print shows progress on both fronts.

With respect to our current recommendations, we continue to expect a strong bias toward steepeners to persist, though we see pathways to this steepening via bull-, twist-, and bear-steepening. We continue to suggest 2s20s steepeners andanticipate pathways to all bull-, twist-, and bear-steepening scenarios. We also maintain receive July FOMC OIS contract, and long 2y breakevens (see United States | June CPI : A surprise slowdown ).

… Steepeners are doing well in the post-debate world. We turned to (2s20s) steepeners following the presidential debate two weeks ago, changing our long-held resistance to steepeners, with the idea that rising probabilities for a Trump presidency would be linked with rising term premiums in the back end (Exhibit 15) and intersect with an already cooling economy, thus steepening the curve.

MS: Friday Finish – US Economics: Addressing Worries Over US Strength

Slowing consumption and labor market indicators have stoked fears that the US economy is headed for a recession. We continue to look for a soft landing, with important support from lower interest rates. We walk through the numbers that are driving investor concerns and the data to follow from here…

… We do not expect that much weakness and continue to see the Fed first cutting 25bp at its September meeting and following up with 25bp cuts every meeting through mid-2025. Softening in recent data has made a strong case for the July statement to solidify expectations for a 25bp cut in September. And we think it would take a big shock to convince the Fed to cut later this month.

… United States Flawless landing? Policy is in a good place, with inflation cooling off as the labour market remains relatively strong. June core CPI rose by 0.1% mom, well below consensus expectations, for a 0.2% mom rise. The decline in initial jobless claims and the Atlanta Fed now showing 2% GDP growth for 2Q are also encouraging. In this context, the Fed is well positioned to achieve a flawless landing, but the timing and magnitude of cuts are still in question. The market is fully pricing in two cuts, one more than the SEP median dot for this year and three by January. With the economy “much more in balance”, Powell in his testimony to Congress set the stage for rate cuts but did not signal timing. Although yields declined sharply following the soft CPI print, curve steepeners remain the favourite trade as investors are still broadly agnostic as to the directionality of yields in the near term. We expect yields to gradually decline heading into the November elections but to rise afterwards.

➔ While the data is supportive of rate cuts sooner than we had anticipated, the market might be getting ahead of itself in pricing a September rate cut and a total of three cuts by January. Despite positive inflation data, the Fed will likely move cautiously on cuts. Hence a later start and a regular cadence of say one cut per quarter thereafter might make sense.

TD: Global Rates Weekly - A Song of Ice and Fire (missed and seems they got long exactly THE best day past couple weeks to do so … good on them!!)

…Buying the Dip: Entering Long 10y Treasuries This note was originally published on July 01, 2024.

10y Treasuries erased much of their 28bp June gain in the past week's bear steepening move — a move likely aided by rising expectations of a Republican sweep in November, which could push deficits higher. While rates could remain choppy as investors wait for key data, we see several reasons to enter 10y Treasury longs here:

Technical levels: We see a psychological resistance around 4.5% as expectations for Fed rate cuts have not changed significantly. In addition, 4.54% represents the top of the recent bullish channel, which should help backstop the selloff (Fig 1). We would look to add to the trade if markets are unable to break the range.

… Interest Rate Watch: Balanced Risks Drive the FOMC Closer to a September Rate Cut

Since January, the FOMC's post-meeting statement has signaled that neither further hikes were likely nor were rate cuts near. In Congressional testimony this week, however, Chair Powell's comments suggested that the FOMC is getting closer to exiting its holding pattern and preparing to descend.

… Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW

AllStarCharts: Bonds Are Ready to Rip (haven’t these guys HATED bonds? when facts change they change, what would you … never mind…)

The rally should pick up momentum once buyers drive price above the two-year downtrend line.

We’re targeting 113’06 and 117’00 as long as price holds above 109’17.

Remember, today’s CPI and tomorrow’s PPI prints will push a healthy dose of volatility into the markets – be prepared…

EPB Macro: Labor Market Breakdown (Chart Of The Week … good read as we all await the one, the only, Dr. Lacy Hunt of HIMCO …)

… The household employment level is contracting as of June, falling sharply from a 1.8% growth rate 12 months ago.

Aggregate weekly hours growth remains stable.

The 12 month average of non-seasonally adjusted jobless claims is trending higher, but at a very mild pace. The insured unemployment rate has moved higher from the cycle low-point but, similar to jobless claims, is relatively muted.

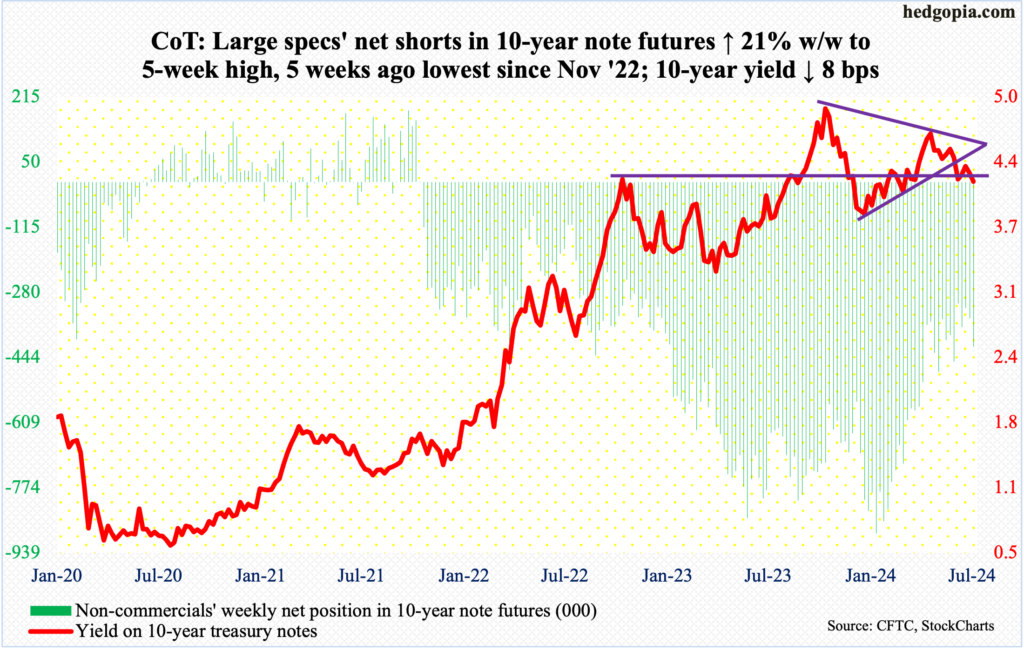

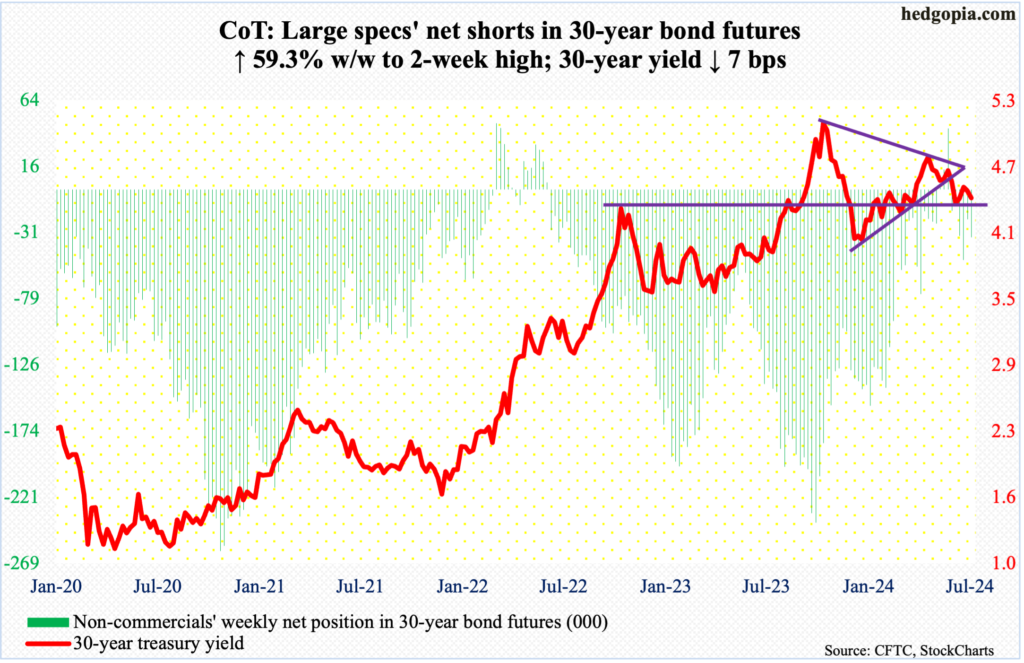

Hedgopia CoT: Peek Into Future Through Futures, How Hedge Funds Are Positioned (net shorts in both 10s and bonds UP WoW … positions matter and at moment, neither are extremes but interesting against backdrop of FALLING YIELDS — source for some of the bid?)

Since 2022, inflation concerns > growth concerns Thus, rising bond yields were behind every significant equity selloff. At least for a little bit, growth concerns will be > inflation concerns, which means there is a window for bonds to diversify again.

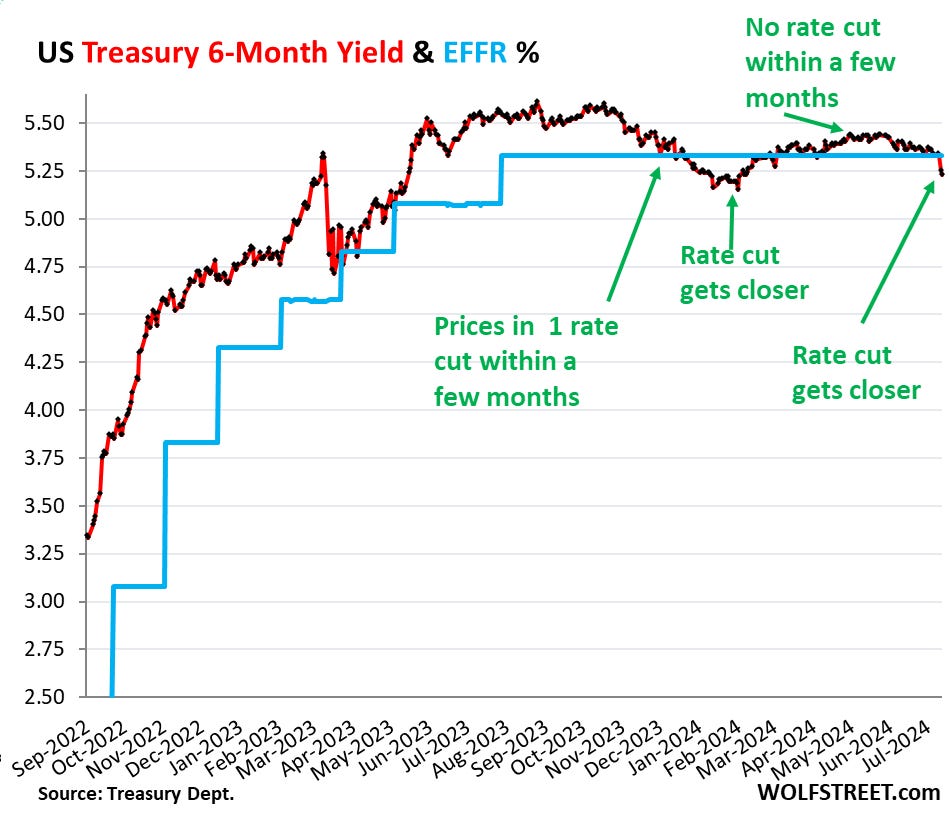

WolfST: What the Short-Term Treasury Market Says about Rate Cuts, and How Repeatedly Wrong it Was so Far

Inflation has the upper hand. The market (Goldman Sachs and me included) vastly underestimated the Fed. Someday the market might get it right.

… So the 6-month yield is now pricing in one rate cut within its 6-month window, more heavily weighted toward the first two-thirds or so of that window, after having already wrongly done so at the beginning of this year.

… The market was wrong about the Fed’s rates, and all 2-year notes that were bought at auction and that matured in 2024 or will mature in 2024 were a lousy deal. Buyers would have been better off with a series of short-term T-bills that stick closely to Fed’s actual policy rate — rather than follow market projections.

Someday, the market is going to get the rate-cut bets right. But it will only take a few more lousy inflation readings for the rate cuts to get moved further into the future. On Friday, the PPI showed up with red-hot services inflation, now delineating a clear U-Turn in December. Producers that pay those higher prices for services will try to pass them on, and so they may ultimately filter into consumer prices and higher inflation readings over the next few months. Or if producers cannot pass on the higher costs of services, their margins will get squeezed.

WolfST: Services PPI Inflation Dishes Up Another Nasty Surprise, 6th Month in a Row. Bottom of U-Turn was in December

Services are huge, 62% of total PPI. We see parallels to early 2021, when this mess started. But core goods are well-behaved.

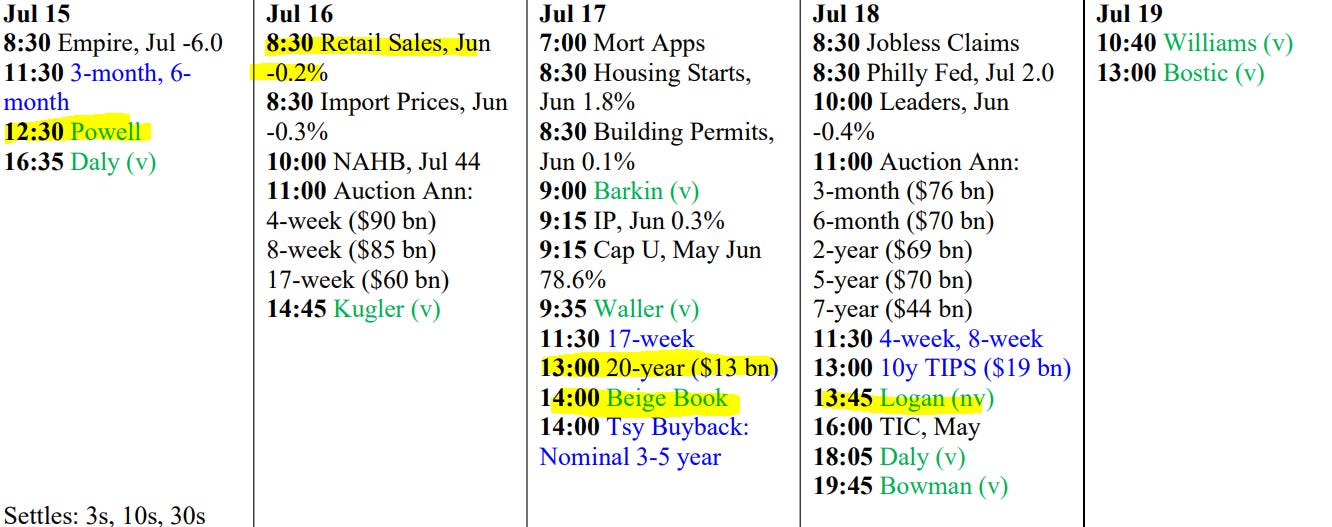

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

{kind=link}

{kind=link}

All so surreal Sta safe lots of the normal stuff I wanna read and think about all seem so insignificant right now

Request Denied for Trump and RFK jr

https://youtu.be/WZQyyN1VPTI