Good morning … THAT was fun … CPI, a SLOPPY long bond auction (on heels of 2 other great auctions) and a press conference all topped off with a FREE SLURPEE!

Woo HOO … this is the stuff for a funTERtaining summer Thursday!!

How ever are we to match level of enthusiasm today, Friday, July the 12th??

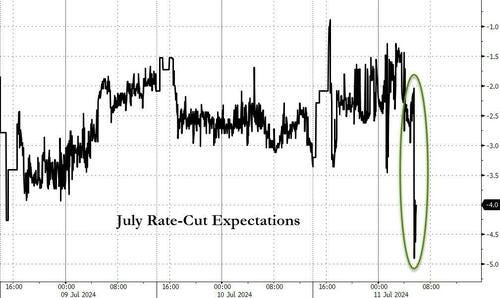

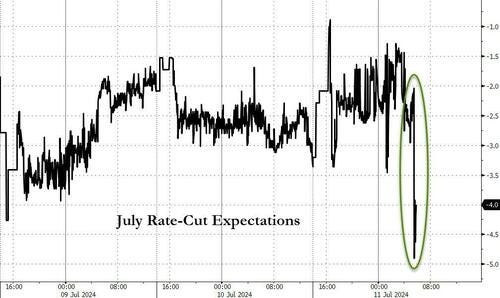

NOT by starting off your day with a look at some randomly selected UST yield just because … With CPI moderating, a more clearly defined pathway TO September CUT is being forged … here’s a look at the front end — 2yy … in context AND in wake of the data …

2yy: 4.50% an important level dating back to Sep 2023…

… momentum becoming stretched / overBOUGHT on both daily and WEEKLY charts and this on heels of double digit basis point move LOWER in moments just AFTER the data print and by days end, apparently the drop in yields was biggest in 5.5mos (RTRS HERE)

… whatever it is YOUR view, well, kinda makes the CRESCAT folks saying 2% 2s somewhat less lunatic fringy?

Good news is that yesterdays less than good 30yr auction didn’t seem to dent HOPE for September CUTS …

ZH: Gruesome, Tailing 30Y Auction Sees Plunge In Bid-to-Cover, Foreign Demand

… After two superb coupon auctions, where both the 3Y and 10Y sales earlier this week showing remarkable buyside demand, we were wondering if today's 30Y auction would be just as strong. And then we read bloomberg's always wrong preview which said that the auction was "likely to stop through"...

... at which point we knew it would be a tailing mess.

And sure enough, pricing at a high yield of 4.405%, not only was the yield higher than last month by 0.2bps - when all previous auctions saw a drop in yields - but the auction also tailed the When Issued 4.383% by 2.2bps, the biggest tail since last November's record 5.3bps tail. So much for that "likely stop through."

… good time to slip in a GRUESOME liquidity event … on heels of benign CPI which has 3rd rate CUT 2024 hopes creeping back in to the markets … said another way …

… hey, look, kids … I didn’t force you to read this and many of you have arrived and left after a short time — sorry — not sorry.

Finally, a look and link back TO yesterday …

ZH: Consumer Prices 'Deflated' Most Since COVID Lockdowns In June; Core Prices Continue To Rise (written / offered just AFTER data point…)

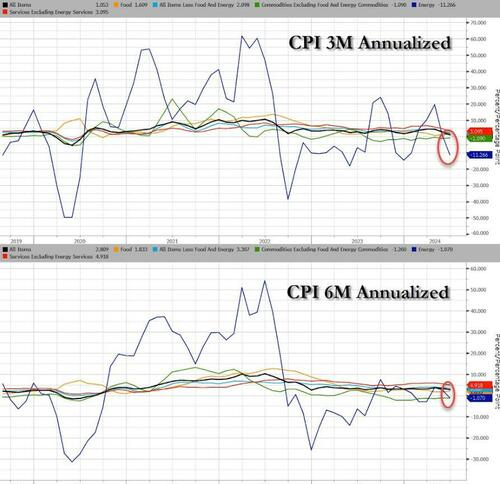

Expectations for more 'evidence' of a return to disinflationary trends were high heading into today's CPI and they were more than satisfied by a 0.1% MoM decline in headline consumer prices in June (below the +0.1% MoM exp) - the biggest MoM drop since May 2020. That pulled the headline YoY CPI down to +3.0%...

This is the third consecutive 'miss' for CPI - prompting calls for July rate-cuts - with 3m and 6m annualized inflation declining...

First things first, rate cut expectations are soaring after the deflationary CPI print...

July rate cut expectation remain subdued though for now...

… and finally, Global Wall REACTS thru ZH (more just below) …

ZH: Wall Street Reacts To Today's Dovish CPI Shock: "It's Time To Cut"

… and not to be outshined by CPI …

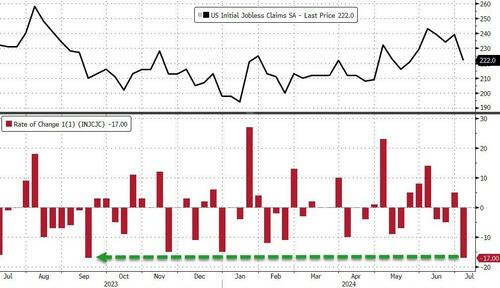

ZH: Initial Jobless Claims 'Plunged' Last Week By Most In 10 Months

… So initial claims saw the biggest week-over-week drop since Sept 2023?

Makes perfect sense...

… and so as all of this making PERFECT sense, by days END here’s how the cookie crumbled …

ZH: Nasdaq Pukes To Worst Day Versus Small Caps In 22 Years, Gold Soars Near Record High After Soft CPI

Misses across the board today in CPI left US macro surprise data languishing in 'not so soft landing' territory...

...all of which prompted a surge in rate-cut hopes, with 2024 expectations at their highest since April (61bps) as 2025 is now pricing in four full rate-cuts...

… AND we’ll quit while we’re behind and offer a look at USTs as of 644a:

… and from prices TO some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: RTY continues to outperform, Dollar is flat & Bonds slightly pare recent gains; US PPI due … Bonds are pressured giving back some of the post-CPI strength … USTs are very slightly softer, in a paring of US CPI-induced strength and following a subdued 30yr auction on Thursday. Docket today includes US PPI and UoM Prelim. Currently trading around 110'30.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ about CPI and a few other things …

BARCAP: June CPI: Weak across the stack (good news, just don’t worry ‘bout your COSTCO membership going up cuz … you know … prices are comin’ down…)

June core CPI inflation surprised to the downside, rising by only 0.065% m/m (3.3% y/y), 10bp slower than in May. Disinflation in core services, led by shelter and transportation services, was accompanied by another month of deflation in core goods. The data suggest core PCE inflation could round up to 0.2% m/m in June.

… All told, we remain of the view that core CPI prints similar to June's seem unsustainable, and we expect some payback next month. We think these magnitudes of declines in lodging and airline fares are unlikely to repeat next month. Regarding rent and OER CPI, we think the relief in June partly reflects payback from some regions, including NY, where inflation was outsized in May. In addition, OER for the Jun/Dec cohort appears very low compared with recent moves in other cohorts, while the Jan/Jul cohort, which matters for next month, has been running higher than the rest (Figure 6). As a result, we are inclined to pencil in a slightly firmer rent/OER CPI in July, although we retain our baseline that rent CPI will slow to 0.25% m/m and OER to 0.30% m/m by year-end.

BARCAP: Disinflation underway, but beware of bumps

Core CPI surprised to the downside, printing at 0.06% m/m (3.3% y/y) in June, amid weak shelter and transportation services inflation, and another month of goods deflation. Some of this slowing looks unsustainable, and we expect some payback in July. Our year-end core CPI forecast is marked down by 0.2pp to 3.0% y/y.

… All told, we remain of the view that core CPI prints similar to June's seem unsustainable, and expect some payback next month…

…We have revised our core CPI forecast lower for this year by 0.2pp, to 3.0% y/y in December 2024, but leave our December 2025 forecast unchanged at 2.6% y/y. The downward revision for this year's forecast largely reflects the weaker-than-expected June print, but also incorporates a very modest downward revision to our core CPI m/m path for this year, after taking on board the slowing in June OER and rents CPI (Figure 4).

Core-CPI printed at just 0.065% in June vs. 0.163% in May and the +0.2% consensus. The yearly pace of Core-CPI slipped to 3.3% vs. 3.4% prior and 3.4% anticipated. Headline CPI also disappointed at -0.1% MoM vs. 0.1% forecasted and 0.0% in May. The YoY headline pace slipped to 3.0% vs. 3.3% prior and 3.1% anticipated. Within the details, we see Rent at 0.261% and OER at 0.276%. Core services ex-shelter came in at 0.073% from -0.047% in May while core-CPI services ex-Rent/OER was -0.052% versus -0.042% prior. The net of the data reinforces the dovish messaging from Powell and offers confirmation that the Fed's tighter policy stance is weighing on consumer price inflation. Initial Jobless Claims during the week of July 6 registered 13k below the 235k consensus -- with the 222k print representing a 17k decline from last week's 239k and a 6-week low. Continuing Claims were also better-than-expected at 1852k versus the 1860k consensus and 1856k prior …

BNP: US June CPI: Clearing the path to a September rate cut (missing some of the former DB > Bloomberg names but am sure quality of the recap and victory lap just the same)

KEY MESSAGES

US headline and core CPI surprised to the downside for the second straight month in June, with the details overall supportive of a softening inflationary trend.

While the print benefited from a few categories delivering chunky declines, weakness was broadly based.

We now see the Fed beginning its cutting cycle in September (versus December previously).

… Core PCE tracking a soft 0.2% m/m with key data ahead: We pencil in a 0.16% m/m rise in core PCE inflation for June after today’s CPI report, which would be a step up from May’s 0.08% print but well below its 0.34% monthly average pace through the first four months of the year. Importantly, this would leave the 3m/3m saar rate at 2.7% compared to 3.7% in March, which should bolster the Fed’s confidence that inflation is heading back down to its 2% target. We note potential for PCE to print relatively more strongly than the CPI as many of the key categories of weakness in the June CPI report (such as airfares) derive from the PPI in the PCE. About a third of the PCE index comes from PPI (Friday 8:30 EDT) and import prices (Tuesday 8:30 EDT), hence we will update our forecast as these data are released.

BNP US rates: Enter 3m5y receiver spread and 5s30s steepener for a breakout (and finally, the year of the steepener, right?)

A cooling labour market and faster-than-expected disinflationary progress convince us that outright yields and the curve are breaking out of their recent ranges.

Our forecast for the Fed’s first rate cut is now September’s FOMC meeting and historical analysis suggests the curve begins to sustainably bull steepen when the first cut occurs within the next three months.

We favour using 5y swaps and 5s30s UST due to less punitive negative carry, reliance on the depth of the cycle rather than the near-term timing/volume of cuts, and the potential for negative news on the deficit adversely impacting the long-end of the curve.

Trade idea: Buy 3m5y A/A-30 receiver spread…

Trade idea: 5s30s UST steepener. Entry: 28.25bp…

…We favour 5s30s over alternatives such as 2s10s because the carry is less punitive (-2.3bp vs -5.5bp for 1m) and relies on an economic slowdown driving the depth of the cutting cycle rather than front-loaded cuts. Further, to the extent that expectations for the deficit remain poor or deteriorate, we would expect the long-end of the curve to be most negatively impacted. To wit, the 11 July 30y bond auction tailed 2.2bp, which may be a reminder of the ongoing deficit-induced record UST supply.

DB: June CPI recap: May's good news becomes great with rent downshift

… The major story within the June CPI data was weakness on the services side, rents in particular. Both primary rents (+0.26% vs. +0.39% in May) and OER (+0.28% vs +0.43%) took a significant step down and are now back in line with pre-pandemic prints. Given how these data are constructed, they tend to be somewhat sticky and we expect similar prints going forward, though the Fed will likely want to see at least one more month of tame rents before sounding the all clear…

…With rents returning to pre-pandemic rates, the balance of the June inflation data are likely to qualify as a "really good" reading, to use Chair Powell's taxonomy. As a reminder, the median 2024 Q4/Q4 core PCE forecast of 2.8% in the June SEP would be consistent with an average pace of about 20bps a month over the rest of the year. Barring a particularly large upside surprise in tomorrow's PPI, this data, when paired with the softening in recent growth and labor market data, is likely to give the Fed enough confidence to begin cutting rates earlier than our December baseline expectation. We will update our Fed expectations after the PPI data give a fuller read on the Fed's preferred inflation measure.

DB Mapping Markets: Weighing up the good news and bad news (in this note they — DB — are both the good AND bad guys, card carrying Team Rate CUT and otherwise … have a click and read, choose a side and enjoy the weekend …?)

Over recent weeks, there’s been a growing divergence in market narratives, and it’s possible to put both a positive and a negative spin on how markets and the economy are doing right now.

On the bright side, risk assets are performing strongly, with the S&P 500 up to successive record highs. Broader volatility is subdued, credit spreads are fairly tight, and financial conditions remain pretty accommodative. Alongside that, inflation is getting closer back to central banks’ targets, bringing the prospect of rate cuts into play. And overall, there’s a growing sense that we’re finally moving past the various economic shocks of recent years.

But there are also more negative interpretations on where things stand right now. Unfortunately, a lot of traditional leading indicators for the US economy are pointing to downside risks ahead. That comes as global data surprises have also become more negative in recent weeks. Inflation is still lingering above target in the US and the Euro Area, even if it has come down from its peak. And the market rally we’ve seen is unusually narrow by historical standards, having been dominated by gains among megacap tech stocks.

… In light of these competing narratives, we put some of the evidence forward for both cases…

Incorporating inputs from CPI, we now forecast core PCE inflation increased 0.205%M in June vs. 0.08%M in May. This would raise the y/y from 2.57% to 2.61%. Headline PCE is forecasted at 0.105%M vs. -0.01%M the month prior. Core services ex housing translation points to 0.22%M in June vs. 0.10% prior. We will update our forecast tomorrow after PPI, incorporating inputs to forecast healthcare, financial services, and airfares.

A core PCE print aligned with our expectations would be the second weakest this year, and the second consecutive reading adding to the convincing evidence the Fed needs to start cutting in soon. We expect more deceleration ahead, especially in 2H24, and we maintain our call for a first cut in September this year, followed by cuts at every meeting through mid-2025…

MS: Cross-Asset Dispatches: The Future of the 60/40 Portfolio (esp funtertaining read on heels of the Team Rate CUT excitement after CPI)

The equity/bond diversification strategy will live on. But the correlation and volatility levels of the last three decades are shifting, partly driven by the secular narratives of AI and the emergence of a multipolar world. The 60/40 mix needs a rethink.

… Against a backdrop of high rates volatility, low government bond returns and higher-than-average stock-bond correlation over the last two years, one frequently asked question has been: is the 60/40 equity/bond strategy – where 60% of a portfolio is allocated to stocks and 40% to fixed income – dead? We think that its demise is grossly exaggerated – or at least the demise of the concept of the strategy is. But exactly how one thinks about the right mix of equity/bond strategy will need to change.

… What Are The Factors That Will Drive The 60/40 Strategy's Future?

FACTOR 1: CORRELATION – HOW LOW CAN IT GO? The short but maybe disappointing answer is – we think that correlation will normalize in the short run, but where it goes beyond that is harder to quantify…

…FACTOR 2: VOLATILITY – WHAT'S NORMAL ANYWAY? Another short but maybe disappointing answer – we think that volatility will normalize in the short run, but probably not to where investors would want it to be at…

…FACTOR 3: EXPECTED RETURNS – PAIN OR GAIN? What argues strongly in the 60/40 strategy's favor is bonds' good expected returns: For the last 15 years or so, the worry about fixed income becoming less effective as a diversifier stemmed from low yields – Bund yields at 0.25% can only fall so far to offset equity losses, for example. This is not the case now. Exhibit 19 and Exhibit 20 show for USTs and EGBs our estimates of long-run returns, a function of today's yields and some adjustment for roll-down. With bond yields close to 20-year highs, expected returns over the next decade also stand at attractive extremes. On a related note, higher prevailing yields and long-run expected returns for bonds can justify the asset as a source of return rather than 'just' a diversifier, especially attractive to an ageing demographic who want high and stable cash flow to fund a longer retirement.

…We believe that the 60/40 equity/bond strategy will need a fundamental rethink, not because bonds are not longer good diversifiers – they remain so – but because correlation and volatility have shifted from pre-pandemic and post-GFC levels…

…There is another solution. Instead of a 60/40 equity/government bond strategy, investors can look to a multi-asset portfolio – dialing up and down duration risk, adding credit exposure, increasing allocation to EM, etc. We will present our thoughts on these portfolio allocation topics over the next few months in a series of notes.

RBC: Another downside surprise in U.S. June inflation

… Bottom line: A second U.S. CPI downside in a row in June has added to market odds for a first rate cut from the Federal Reserve this September. That’s also building on a weaker round of employment data last week that showed persistent unwinding in tight labour market conditions. From the Fed’s perspective, these are all data prints that they would like to see at this stage to confirm that interest rates are working to cool inflation pressures sustainably and to realize their dual mandate. Powell has always communicated the Fed’s decision making as a risk-management process, but also reiterated in his congressional testimony this week that there are downside risks to the economy and labour market from rates being restrictive for too long. After today's CPI report, we think an interest rate cut at the Fed’s next meeting in July is still unlikely but the odds are tilting towards a September cut.

RBC: At Last: U.S. economy shows signs of softening (yer really a sick bunch if this is ‘at last’ and in some way … a relief but then … who DOESN’T like lower prices … just dont worry about COSTCO increasing cost of yer memberiships…lets just enjoy the moment of how at last, econ showing signs of weakening… ?)

Highlights:

U.S. gross domestic product growth and labour market conditions are finally softening alongside two straight downside inflation surprises. We now expect the U.S. Federal Reserve to cut rates in September—earlier than our prior December assumption—with a gradual easing cycle to follow.

The Canadian economy is stuck in excess supply with per-capita GDP continuing to decline and unemployment persistently trending higher. Inflation is set to moderate further following slower growth in mortgage and rent costs. We expect three more cuts from the Bank of Canada this year with the overnight rate at 4% by December.

The economic rebound in the euro area and the U.K. is continuing in Q2 after a softer 2023. But, still elevated services inflation is arguing for a gradual easing cycle from the European Central Bank and Bank of England. We retain our call that the ECB will follow with a second cut in September and the BoE will make a first cut in August.

In terms of broader implications for the U.S. economy from the November presidential election, we think if Trump is re-elected, his second presidency would look a lot like the first one. There will be another round of potential trade disruptions representing a threat to an already weakening manufacturing sector.

Wells Fargo: June CPI: September Rate Cut Incoming

Summary This morning's CPI report was arguably the most encouraging one the FOMC has received since it began its inflation fight nearly two and a half years ago. Consumer prices declined by 0.1%, led lower by a drop in energy prices and a modest increase in food prices. Excluding food and energy, the core CPI increased by just 0.1% (0.06% unrounded), which was the smallest increase since January 2021, a time when high inflation was far from most minds. The slowdown in core CPI inflation was broad-based, with core goods prices once again declining and core services inflation advancing only 0.1% compared to the previous six-month average gain of 0.4%. A leg down in shelter inflation was a key contributor, but drops in more discretionary spending categories like airfares (-5%), lodging away from home (-2%) and recreation services (-0.1%) also played a role in the softer reading.

On balance, the economic data are the most supportive of a rate cut that they have been all year. Over the past three months, the core CPI has increased at a 2.1% annualized pace. This marks the smallest three-month change in core prices since March 2021. Furthermore, it is not just the inflation data that have shown signs of cooling in recent months. A deceleration in employment and a rise in the unemployment rate are just a couple of the numerous indicators that are pointing to less heat in the U.S. labor market. Chair Powell nodded to these trends in public comments this week, saying that "elevated inflation is not the only risk we face." A rate cut as soon as the July 31 FOMC meeting is unlikely, but we remain of the view that the FOMC will cut the federal funds rate by 25 bps at its September meeting and reduce the fed funds rate by another 25 bps in December.

Source: U.S. Department of Labor and Wells Fargo Economics

Yardeni: Disinflating CPI Broadens Market Rally As Investors Rotate To SMidCaps

… And from Global Wall Street inbox TO the WWW,

FRB ATLANTA: Atlanta Fed's Sticky-Price CPI Remained Elevated in June - July 11, 2024 (… this is fine…)

The Atlanta Fed's sticky-price consumer price index (CPI)—a weighted basket of items that change price relatively slowly—rose 2.6 percent (on an annualized basis) in June, following a 2.4 percent increase in May. On a year-over-year basis, the series is up 4.2 percent.

On a core basis (excluding food and energy), the sticky-price index rose 2.4 percent (annualized) in June, and its 12-month percent change was 4.2 percent.

The flexible cut of the CPI—a weighted basket of items that change price relatively frequently—fell 8.6 percent (annualized) in June and is down 0.4 percent on a year-over-year basis.

Bloomberg: Treasuries Wipe Out This Year’s Loss as Traders Bet on Rate Cuts

US Treasury index was down as much as 3.4% for 2024 in April

‘Powell sounding dovish is firing up investors,’ Mizuho says

… Bloomberg’s US Treasury Index has now gained 0.25% for 2024 after being down as much as 3.4% for the year in April when rate-cuts wagers were receding. Broadly cooler US inflation Thursday further cemented the recently growing conviction that policymakers will start easing monetary policy in coming months …

US two-year yields, which are comparatively sensitive to the outlook for Fed policy, slid as much as 13 basis points Thursday to the lowest level since March after the June inflation report. Markets are now fully pricing in a rate cut in September, compared with odds of only about 70% before the CPI data were published.

… Chart #4 compares the year over year change in the CPI ex-energy (which I have chosen mainly because it is a more stable index and thus provides an easier comparison to interest rates) and the level of 5-yr Treasury yields. Treasury yields tend to track inflation but with a lag that can approach one year or so. With the CPI ex-shelter now down to 1.8% (see the green asterisk in the lower right hand corner of the chart), we might reasonable expect Treasury yields to move substantially lower over the next year or so.

Headline CPI came in softer than consensus in June.

Headline CPI -0.06%MoM vs. 0.1% consensus and 0.01% the previous month, bringing the year-over-year change to 3.0%, the lowest level since March 2021.

Core CPI increased +0.06%MoM vs. 0.2% consensus, and 0.16% in May. The year-over-year rate declined to 3.3%, the lowest level since April 2021.

The 3-month rate of core CPI decreased to 2.1% annualized from 3.3%.

at hmeisler (Helene Meisler twitting inbetween tennis matches :) and while i’m maybe NOT such a fan of a big, fat LINE chart … is what it is and she’s got 225k followers on the twittersphere, not me and so … she must be doin it right…)

Market justifying our “bullish bonds” positioning as 2yr yields break sharply lower today, keeping the pattern of lower-highs and lower-lows intact for rates. From our daily note this morning …

WolfST: Beneath the Skin of CPI Inflation: Historic Plunge in Durable Goods Prices, Plunge in Gasoline, and Outliers in Services

Core Services CPI produced 2nd outlier. In the past, after two outliers in this very volatile data, the next move was a U-turn.

… and while that was a lot and frankly, not sure whatever may be left to say over the weekend if ‘they’ (Global WALL or, say HIMCO) have something of note, I will try and pass along / comment, too.

In the meanwhile,

… and best of luck as you plan your PPI trades and TRADE your PPI plans … THAT is all for now. Off to the day job…

I finally caught up! I'll always believe DB got a Stealth Bailout during 2019's 'Not QE' Repo crisis, someone Blew Up on that occasion. Actually I think the term is Zeroed Out, as in Brandon's mind :)

{kind=link}

/cdn.vox-cdn.com/uploads/chorus_asset/file/6438793/this-is-fine.jpg){kind=link}

I finally caught up! I'll always believe DB got a Stealth Bailout during 2019's 'Not QE' Repo crisis, someone Blew Up on that occasion. Actually I think the term is Zeroed Out, as in Brandon's mind :)