… and economically speaking, perhaps even MORE reason for celebration and in addition TO moves lower in crude and yields … The economy showing cracks …

CalculatedRISK: ISM® Manufacturing index Decreased to 48.7% in May

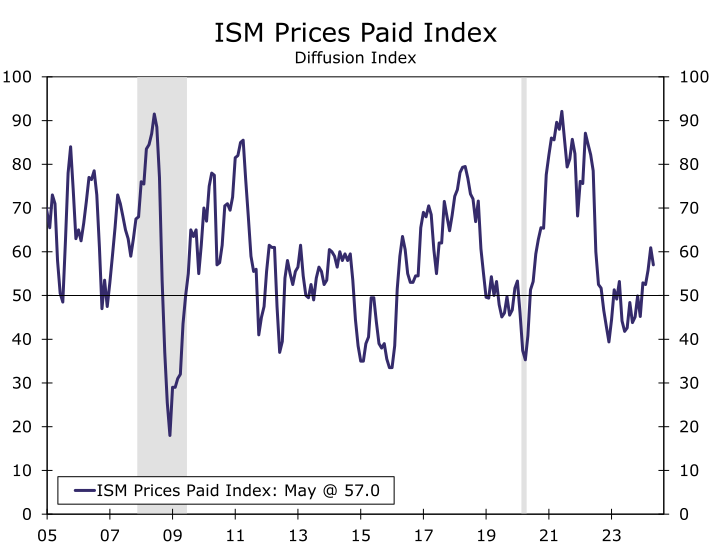

ZH: ISM Manufacturing Survey Signals Further Stagflation: Growth Slows, Prices Rise

ZH: Market Breaks As Multiple NYSE Trading Halts See Entire Berkshire Market Cap Wiped Out

… but hey, bonds went BID cuz stocks broke AND the worse things appear economically, the better they are for Team Rate CUT (and the charts — weekly HERE, monthly HERE — will continue to have that bullish look) … by days end when all was said and done and FRB Atlanta GDP outlook accounted for …

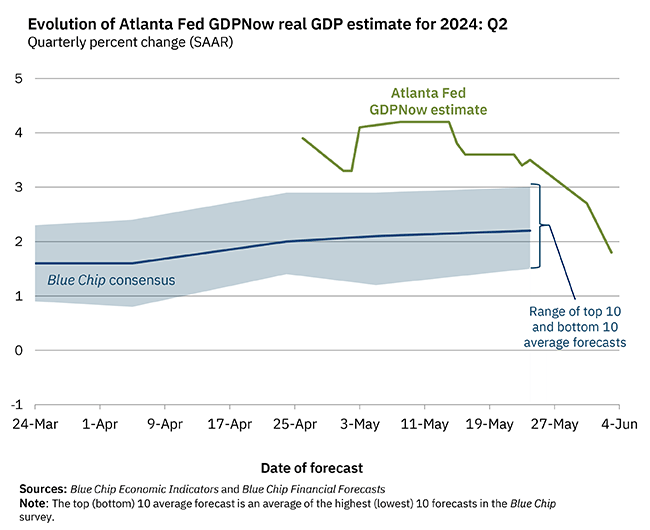

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2024 is 1.8 percent on June 3, down from 2.7 percent on May 31. After recent releases from the US Census Bureau and the Institute for Supply Management, the nowcasts for annualized second-quarter real personal consumption expenditures growth and real private fixed investment growth declined from 2.6 percent and 3.1 percent, respectively, to 1.8 percent and 1.5 percent.

The next GDPNow update is Thursday, June 6.

… Which ultimately combined and produced this sorta clickbait …

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are creeping higher, led by the belly, after a modest retracement overnight in Tokyo on BoJ contemplation of reduced Rinban purchases (~110% volumes). Flows have been characterized as sociable, with receiving in the belly and some cash demand from real$ in intermediates, the 2s5s10s fly -0.3bps richer here at 7am. APAC risk-asset performance was mixed with China firmer (SHCOMP +0.4%), India demonstrably weaker (SENSEX -5.7%) and Japan mildly lower (-0.2%). The down-trade in industrial commods continues with Crude (-2%) and Copper (-2.1%), while precious metals are also on the back-foot this morning (XAU -0.9%, XAG -3.3%). S&P e-minis are showing some weakness too at -0.6% at time of writing.

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Risk sentiment pressured and benefiting havens ex-precious metals; US JOLTS due … Bonds are firmer in continuation of the prior day’s gains, though now off best levels following source reports relating to the BoJ’s bond buys … USTs are firmer and continue to extend on the the post-ISM upside, with additional bullishness stemming from a well received JGB sale overnight and the general risk tone. Since, Bloomberg reported that the BoJ is said to mull bond buys as early as the June meeting, sparking some modest pressure across the fixed income complex; as such, USTs are off best levels but still in the green.

Deterioration in new orders moved the ISM manufacturing PMI to 48.7, near the upper-end of the range it has generally occupied since late 2022. Downbeat new orders were mixed with the first expansionary employment print since September, and less robust input price pressures. We are inclined to view much of this as noise.

BARCAP: April construction spending declines further on weak nonresidential spending

Construction spending fell 0.1% m/m in April, driven by a decline in nonresidential spending. Today's data acted as a drag on our GDP tracker, as it pulled our structures spending tracker down with the weaker-than-expected nonresidential construction spending data…

… Today's weaker-than-expected construction spending data acted as a 0.1pp drag on our Q2 GDP tracking, putting it at 2.0% q/q saar. This was led by sluggish nonresidential spending, which caused our tracking for structures investment to decline.

Volatile data to start the year have raised important questions about the US outlook: Is the economy accelerating? Is disinflation progress stalling? Despite these uncertainties, we continue to see the economy achieving a soft landing with progress toward 2% inflation delayed rather than derailed, allowing the Fed to move cautiously towards rate cuts.

Aside from tweaks to the components, our growth forecast is largely unchanged. We expect real GDP growth to be near 2.0% in 2024 and ~2.25% in 2025 and 2026 (Q4/Q4). In the near-term, the easing of financial conditions over the past half year should be a tailwind for private domestic demand. Consumer spending continues to be the primary driver of growth despite some signs of emerging pockets of weakness. Conversely, the government's growth contribution is starting to wane.

The labor market has rebalanced and wage growth should approach rates consistent with 2% price inflation this year. Our baseline is that job gains slow but remain elevated, in part helped by immigration (see "How large was the inflation mitigation from immigration?"). However, with robust employment data reliant on a low layoff rate, any upward movement in the latter represents a downside risk to the labor market.

After a bumpy start to 2024, the monthly run rate of inflation should slow meaningfully as we progress throughout the year. Due to base effects, the year-over-year rate for inflation should show more limited progress, with core PCE ending the year at 2.75%, near current readings. Disinflation should be led by shelter, where recent data have added to confidence that rent prices are decelerating, even if only gradually.

With inflation surprising to the upside and the solid economy removing urgency, we continue to see the Fed cutting rates once this year in December. An earlier cut is possible, but it likely requires a sharper slowing in inflation as well as some softening in the consumer and labor market. Beyond the first reduction, we see the Fed first delivering a mid-cycle adjustment of 75bps, followed by reductions in 2026 that bring the fed funds rate to its neutral level (3.75-4% in nominal terms).

The election is a close call with tight margins in the few battleground states. Under either outcome we expect budget deficits to remain elevated (see "Fiscal outlook: A chicken in every pot is costly"), though policies could differ substantially in other areas (e.g., trade - see "Trade war II: Supply-side risks versus revenue rewards"). Our forecast does not project an election outcome but does assume that most if not all of the TCJA tax cuts are extended and that significant and broad-based tariffs are avoided. Violation of either of these assumptions would lead to adjustments in our views.

With new forecasts for the Fed path and UST yields, our refreshed USD fixed income optimal portfolios based on our strategists' targets now have a strong preference for Agency MBS and other spread products.

Key takeaways

Our new yield and spread forecasts in our year-ahead outlook have led to shifts in optimal allocation weights and our discretionary allocation recommendations

We like assets that have the triple 'C's of cheap optionality, convexity, and carry to weather uncertainties beyond year end – agency MBS fits the bill

This is reflected in the AGG+ optimal portfolio – it is OW in Agency MBS and other spread products on the back of our call for lower yields, tighter spreads

Expect UST returns also to be strong – ~10%+total returns in the next 12M – but relative risk-reward and carry still mean spread products are more attractive

Some of our strategists' most favored instruments like CLO equity are not part of our allocation exercise, but also have very compelling risk-reward

… An environment of stable growth, inflation trending down, and rate cuts is good for risk assets, one of the reasons we go overweight in global equities in our strategy mid-year outlook, with Europe and Japan as top picks. But this is also an unusually supportive backdrop for fixed income, especially in light of the uncertainties beyond year-end, and good convexity and carry will likely become increasingly important investment themes. We recommend an OW in Agency MBS, and prefer assets like EM sovereign credit, leveraged loans, and securitized credit, especially CLO equity tranches.

This is not to say we think government bonds would do poorly. On the back of our economists' Fed path forecast, we expect 10-year Treasury yields to end 2024 at 4.1% and reach 3.75% by 2Q25, while 2-year falls to 4.4% by year-end and 3.6% by middle of next year. This translates to about ~10%+ total returns over the next 12M, significantly higher than average levels seen over the last 2 decades (Exhibit 2), and why our US rates team has recommended going long duration.

We participate in the NY Fed's Survey of Primary Dealers, which collects expectations about monetary policy and economic indicators in advance of each FOMC meeting. In this note we provide a snapshot of our responses to the survey.

… GDP continues to grow at a "solid pace". We published our mid-year outlook on May 19 where we forecast GDP growth at 2.1% 4Q/4Q this year and next. The economy expanded by 1.3% Q/Q annualized in the first quarter and we are tracking 2Q GDP growth at a solid 2.5% annualized pace (as of May 31) vs Atlanta Fed's GDPNow at 2.7% and NY Fed Nowcast at 1.8%…

… Core PCE inflation has eased significantly over the past year (Exhibit 2), but progress flattened out in 1Q24, and we think progress resumed with the recently released April data. The lack of convincing progress has emboldened the Fed to stay on hold for longer, and we expect the first 25bp cut in September, followed by cuts at every meeting through mid-2025. Our conviction inflation will head toward target remains high. We expect faster deceleration ahead, with monthly readings moving below 0.20%—a 2 ½% annual rate which we believe to be a comfortable pace for the Fed to begin cutting as inflation continues to fall.

The US provides the main data releases. JOLTS data on job vacancies is expected to continue to decline. The initial surge in vacancies in 2021 was strongly influenced by labor market churn. As that subsided, vacancy rates fell. Nominal wage growth continues to slow, which argues against a tight labor market.

US April factory orders data is of moderate interest—the US still has some influence as a manufacturer. The consensus range for this data is quite wide, so comparisons to “market expectations” should be tempered—“the market” does not really know what to expect.

US President Biden is expected to announce immigration restrictions. Current UK Prime Minister Sunak pledged a cap on future immigration. Opposition to immigration is likely to persist; with increasing structural economic change, scapegoat economics is a growing trend and migrants are a focus. Governments may limit immigration to contain social tensions, but less migration slows trend growth rates and increases fiscal pressures…

Wells Fargo ISM: Not Much Relief on Prices Despite Soft Activity

Summary The ISM Manufacturing index slid for the second-straight month amid a sharp pullback in new orders. There was a pickup in hiring but only some relief from prices paid, leaving the overall sector constrained.

… While price pressure isn't cooling fast enough, the most troubling development came in the way of softening demand. The new orders component fell 3.7 points, and, at 45.4, it not only sits at the lowest reading in a year, but it looks unusually weak outside the recent run (chart). The Chemical Products' industry was the only of the top-six largest sectors to report an increase in orders last month, and even there the included comment from a purchasing manager noted concern: “Seems like a minor slowdown is happening. With less spending in the economy, less pressure on us for our products.” Underlying activity continues to be mixed across manufacturing sectors, but the overall industry remains constrained by tighter financial conditions and restocked inventory levels.

The hiring picture brightened somewhat last month as the largest gain came from the employment subcomponent, which rose to 51.1, or the highest index reading since the summer of 2022. The employment index has not been the best leading labor market indicator in recent years, as it has lagged overall measures of hiring…

Small Rise in Residential Not Enough to Offset Drop in Nonresidential Summary Construction Remains Under Pressure from Higher Borrowing Costs High interest rates continue make their mark on construction activity. Total construction spending declined 0.1% in April, the second straight monthly drop. The pullback largely was the result of a retreat in nonresidential outlays, notably within the commercial and healthcare categories. Meanwhile, gains in single-family and home improvement project spending were enough to offset another drop in multifamily spending, resulting in a small improvement in overall residential outlays. Although several segments have managed to side-step the effects of restrictive monetary policy, the downshift in nonresidential and multifamily spending indicates that increased financing costs and reduced credit access remain as a significant headwind for the construction industry …

Wells Fargo: Mid-Year 2024 Global Election Reflections

Summary Politics have been in focus over the first half of 2024 as many systemically important emerging market countries have hosted elections. While opportunity for widespread policy change was present earlier this year, in our view, the main takeaway from most elections has been the high likelihood of continuity of already existing policy. Across Asia, elections in Indonesia, Taiwan and India are not likely to result in significant policy adjustment. In Latin America, Morena outperformance has generated initial local markets volatility; however, we believe that, at a high level, policy continuity will prevail and material policy change is not likely to materialize even if Morena secures a congressional supermajority. South Africa, however, is the one country that does not fit the policy continuity theme. The direction of local policy will change; however, we take comfort in our view that a market-friendly coalition is likely to prevail and policy change in Africa's most industrialized nation could result in a more business-friendly landscape.

Fed expectations have been on a roller coaster ride over the past 12 months, going from six cuts to two cuts to six cuts and now 1.5 cuts, see chart below.

Source: Bloomberg, Apollo Chief Economist

Bloomberg: Is The Economy Starting To Look More Recessionary?

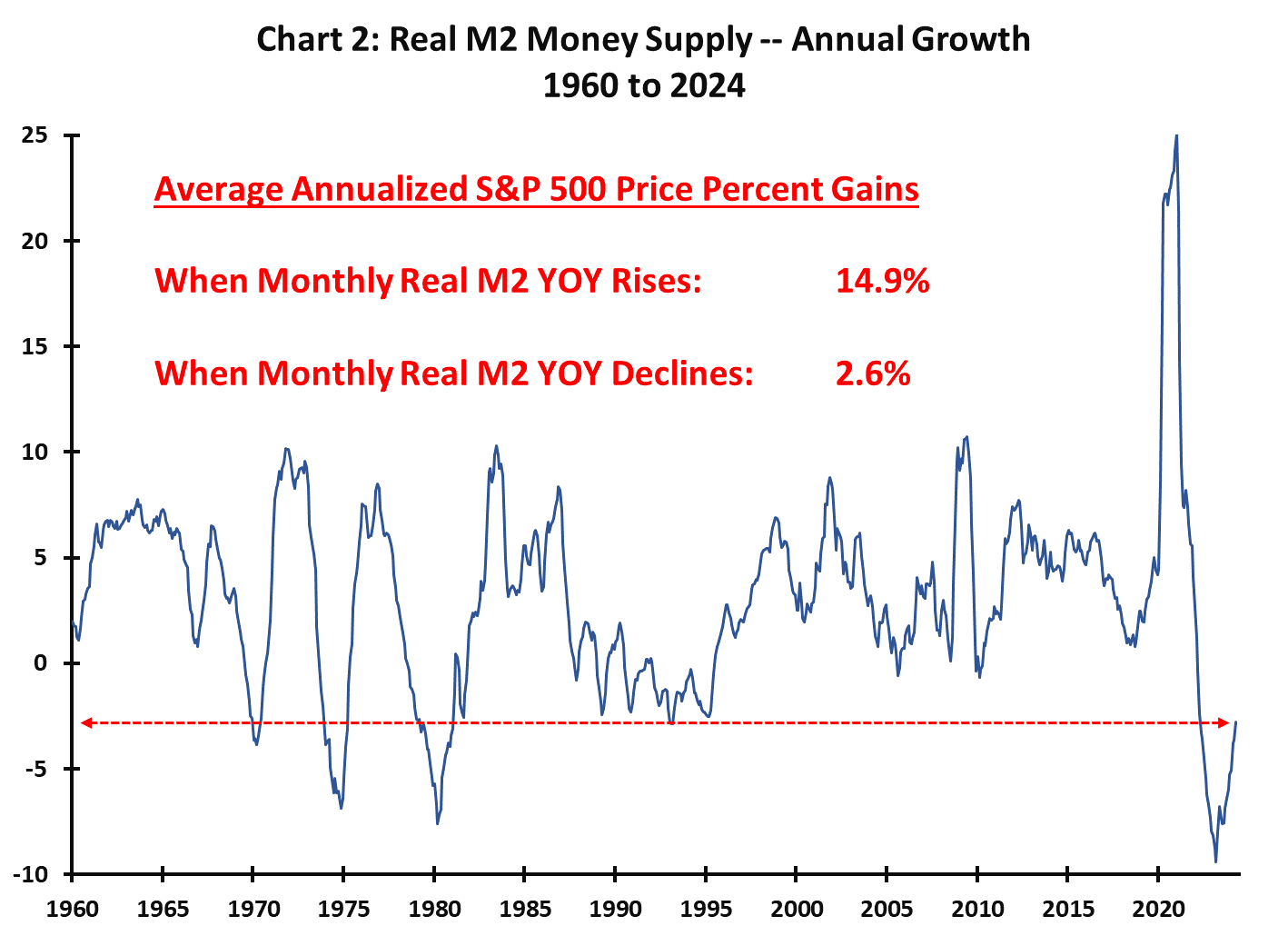

A soft-landing may allow the Bull to use all Three Horns -- rising confidence, improved monetary growth and lower bond yields…

… Horn # 1: Rising Confidence …

… Horn # 2: A Monetary Expansion

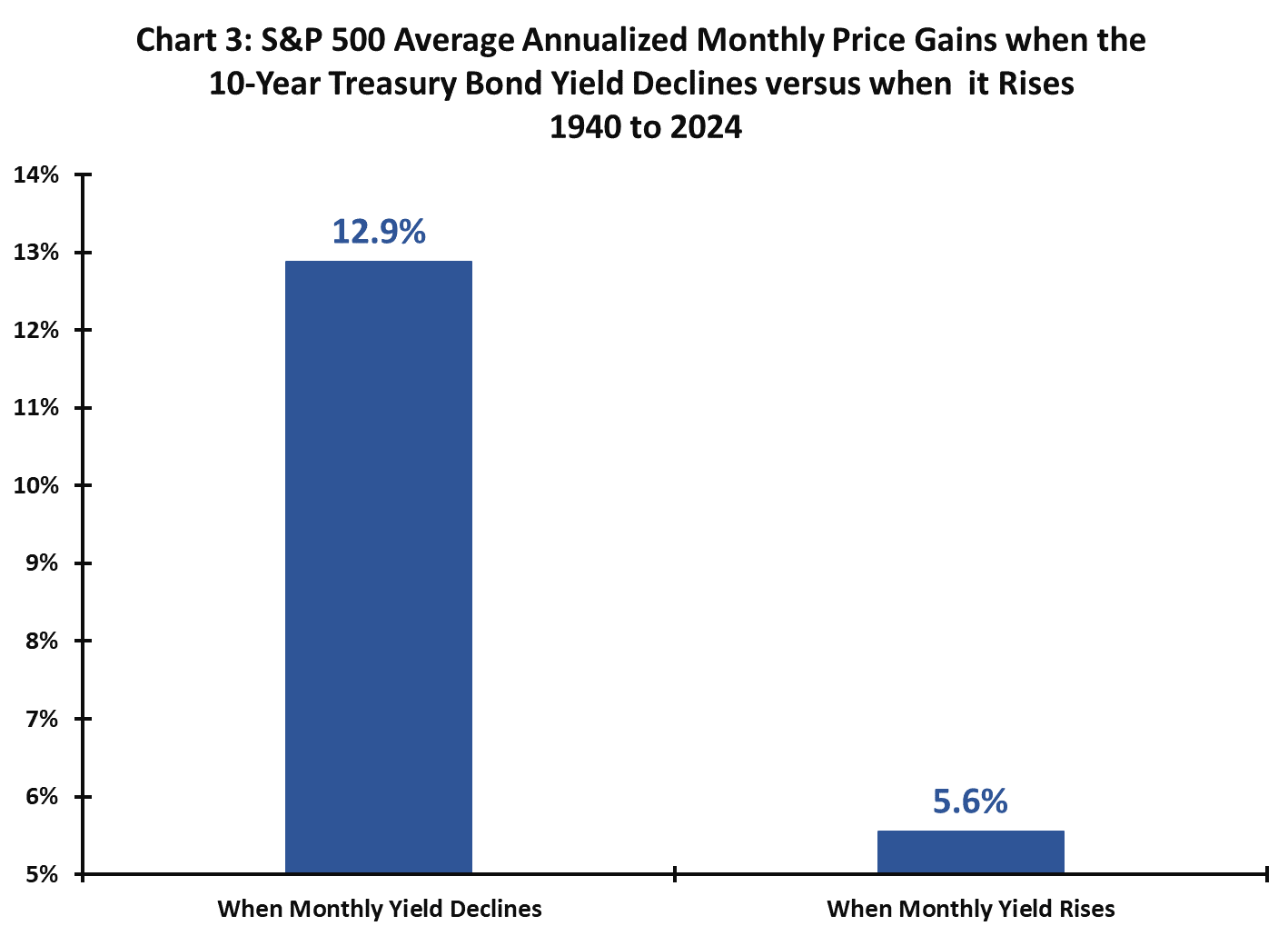

… Horn # 3: Lower Bond Yields

It’s not unrealistic to assume the Fed’s persistent and prolonged inflation fight -- despite the fact that CPI inflation peaked at 9.1% almost two years ago and subsequently declined to 3.5% -- has elevated and kept the 10-year Treasury yield artificially high. As inflation soared to its peak in June 2022, the 10-year yield rose also increased from about 0.5% to 3% and once inflation peaked so did the 10-year yield. After inflation crested, the 10-year yield hovered near 3% from April 2022 to August 2022. Only as the Fed, in unconventional fashion, made clear it was going to keep raising the Funds rate long after inflation had already peaked, did the 10-year Treasury yield reluctantly begin moving higher again. The point here is the bond market appeared comfortable with the 3% area for the 10-year yield once inflation peaked. Could the 10-year bond yield again return to this area when the Fed finally decides the inflation fight is over?

Should a soft-landing become consensus in the months ahead, a 3% to 3.5% 10-year Treasury yield looks plausible. And, as illustrated in chart 3, this bodes well for the stock market. Since 1940, for all months when the 10-year yield declined, the S&P 500 average annualized price gain was 12.9% compared to only 5.6% the rest of the time. Lower yields, with or without a recession, have proved very beneficial for stock investors. Let’s hope the Fed will soon declare victory over inflation and the Bull can wear its Lower Yield Horn!