while WE slept: USTs are firmer; "The Worst Investing Mistake" (Yield Hunting); "T-bill and chill" (BNP, sorry, not sorry a good read); "potential medium-term yield top pattern" (JPM on bonds)

Good morning, except in markets where equity futures are down, oil is up but hey, all is NOT lost, as USTs are a touch lower on the day … this means one thing — It’s almost time to break out a new box of crayola and redraw some TLINES …

10yy DAILY: in the short-run, watching 4.46 support and 4.40 resistance as stocks sell off and the ((s))triangulation compresses … beyond this, I’ll watch 4.50% (psychologically important, round number) support followed by ~4.60 (multi month high) while on the flipside, i’ll be watching 4.30 …

… momentum isn’t really compelling in either direction …

… Good morning, unless, of course, you bot 20s because, well … that ‘bearish momentum’ read noted (HERE) turned out to be fairly accurate despite a fair-to-midland auction …

16 JUN 2025 Axios: Trump team proposes Iran talks this week on nuclear deal, ceasefire The White House is discussing with Iran the possibility of a meeting this week between U.S. envoy Steve Witkoff and Iranian Foreign Minister Abbas Araghchi, according to four sources briefed on the issue…

… AND getting back to the day ahead, we’ll ponder ReSale TALES and a couple other data points, too. Meanwhile, the BoJ overnight did weigh in …

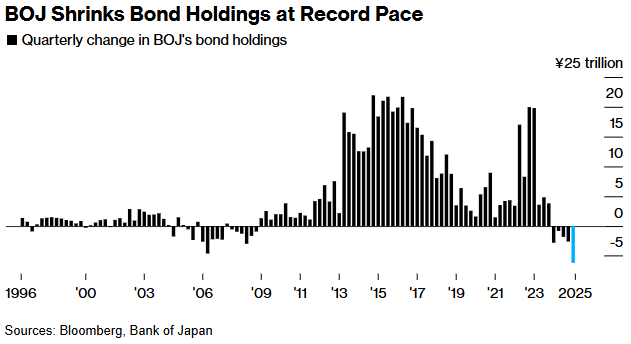

June 17, 2025 at 3:52 AM UTC Bloomberg: Japan Bond Futures Dip After BOJ Plans Slower Bond Buying Cuts

… The bank retained a line in its statement indicating its readiness to step into the market in the event of a sharp increase in bond yields, though since last year, the bar for such action appears to much higher than during the days of its yield curve control program.

Over the years, other central banks including the Federal Reserve have also fine tuned the pace of quantitative tightening. The BOJ remains a long way behind its global peers in addressing the size of its stockpile of assets.

Tue, June 17, 2025 at 3:59 AM EDT Bloomberg: BOJ to Slow Bond Market Withdrawal After Standing Pat on Rates

… and with that little in mind, we look TO the day ahead and while today is likely to be as funTERtaining as yesterday, tomorrow, as always, holds the promise of being even more so, given the FOMC meeting, DOTS and presser … after which, trading across much of Global Wall likely to come to a halt. Ahead of that … here is a snapshot OF USTs as of 647a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure … today I’ve brought forward some comments from Yield Hunting which I found particularly important — I’m guessing very basic for all the pros out there but is as good a reason as any to point, click and subscribe to the site, IMO …

NEWSQUAWK US Market Open: Crude bid and stocks hit after Trump comments & continued strikes, DXY flat into Retail Sales … Two-way action for JGBs; USTs just about firmer while EGBs & Gilts reside in the red … USTs are firmer, but only modestly so. In a relatively thin 110-15+ to 110-23 band. Overnight, the 20yr auction was better than the prior, but roughly in-line with the six auction average. More recently, USTs saw some modest movements alongside JGBs. Overall, the benchmark is awaiting US data and clarity on a number of moving parts.

This graphic shows a buy and sell too soon as the worst investing mistake. However, what it doesn't show is the time you held it and what you did with the capital once you sold it.

What if the security you put it in after selling went up much faster than this one? In that instance, how is it the worst investing mistake?

In general, holding stocks long-term is a good strategy. However, one thing I've learned over the years is to hold a basket or index of stocks rather than an individual stock.

For one, it can reduce the emotions as the volatility is typically much less. The emotional aspect of owning individual stocks is one that is grossly overlooked.

Second, most stocks suck. Only 40% of stocks ever beat cash. Most stocks (~90%) don't even come close to beating the index and only a handful account for most of the value gained in the last three decades - out of over a hundred thousand of them globally.

Lastly, regret is a key aspect of investing. Minimizing it is very important in order to be a good long-term investor. If taking the profit and moving on will result in less regret than holding and potentially losing that profit, then do it…

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

France with a ‘trade idea’, or a take on pop culture, you decide AND a note on FISCAL RISCALS …

We think the Treasury can, and actually might, follow a strategy of ‘T-bill and chill’ for the foreseeable future – keep coupons stable and finance incremental funding needs with bills (or bills & front-end coupons). Cutting long-end coupons modestly is a viable option too.

Investors need to think beyond the 15-20% range for bill share, and think about a 20-25% range. We see plenty of demand for T-bills including (1) money market funds, (2) growing stablecoins, (3) increase in foreign demand, and (4) the less talked about demand from the Fed in 2026. We think the rollover risks from a higher share of T-bills are manageable.

In a T-bill and chill strategy, we expect T-bills to trade well and maintain a +/-5bp range versus OIS in the long run – a significant cost saving for the Treasury over issuing longer dated coupons. The knock-on effect of stable long-end supply could help stabilize to lower long-end yields, and could have a chilling effect on the bond vigilantes.

…MMFs now hold about 40% of their assets in USTs, with 80% of those UST holdings invested in T-bills. We estimate one-third of the total T-bill free float is owned by taxable 2a7 MMFs (see Figure 2).

…, recycled interest income should continue to favor MMF inflows while bank deposit rates sit well below 1%. Their growth should still outpace the increase in Tbill supply that we expect if Treasury were to leave coupon auction sizes unchanged over the next three years, keeping T-bill rates marginally rich and stable versus swaps (see Figure 3).

…Stablecoins want T-bills The TBAC estimates stablecoins will reach USD2trn in market cap by 2028 and suggests that stablecoins hold roughly half their holdings in T-bills, which could lead to a USD900bn increase in T-bill holdings over the next 2-3 years.

KEY MESSAGES Our assessment of sovereign debt ratios of big economies suggests less room for counter-cyclical policies in the face of a severe shock than in 2020 and therefore more risks to growth, particularly in more indebted EM countries.

We model alternative scenarios for the debt/GDP ratios of the US, Brazil, France, Italy, Japan, the UK, Colombia and South Africa – large economies with a combination of high debt ratios and high budget expenditure risks.

Our exercises suggest that debt paths could worsen substantially under plausible alternative (and slightly more negative) scenarios, highlighting how fiscal risks might remain in the forefront of investors minds.

…Alternative debt/GDP paths: US and Italy US: The country stands out in our subset for having significant increases in its debt/GDP ratio even under positive alternative scenarios with higher growth or lower deficits. Even under a smaller primary deficit than assumed in the baseline, US debt rises by around 24pp of GDP over the next 10 years to around 146%, highlighting the challenge of reining in its debt growth.

With debt above 100% of GDP, we find that the US is most sensitive in the interest rates scenario: a 100bp permanent increase in long-term rates would lead to an increase of around 7pp of GDP relative to the baseline by 2035, to about 153%. Shaving off 50bp from primary deficits would amount to a 5pp decrease relative to baseline, significantly slowing down the rate of increase in the ratio. Still, our sensitivity analysis suggests that it might not be enough to completely counterbalance an environment of higher interest rates or lower growth over the coming years, which we think is a risk, should it materialize. In Global Outlook Q3 2025: Trade war and peace, dated 20 May, we explore the impact of automatic fiscal stabilizers on the deficit, which would lead to much higher increases than the one considered here (plus or minus 50bp).

We expect the tax and spending bill currently making its way through Congress – which mostly extends prior tax cuts and adds some new provisions, but also engages in some outlay cuts – will leave the federal deficit in the vicinity of 6% of GDP over the coming years. That number would be larger without substantial new revenue from tariffs, and the risk is those receipts prove smaller or impermanent. We also believe the risks are skewed towards higher deficits should negative shocks materialize or the uncertainty over trade policy translate in longer-lasting growth impacts.

Best in the biz offers a remark about a mostly unremarkable trading session …

…Monday’s price action was remarkably contained by recent standards. The two notable developments were 1) headlines that Iran is seeking to de-escalate with Israel and 2) a solid takedown of the 20-year reopening. While the price action netted to a bear steepener on the day, the momentum was established during the overnight session and simply carried through as a theme. US equities recovered much of Friday’s weakness and financial markets appear to be content with a wait-and-see approach to the conflict in the Middle East. Even oil prices managed to leak lower on the day, although it is unclear how Israel will respond to the overture by Iran. With geopolitical tensions back in focus and the relatively limited data calendar, we suspect that the overnight session will be particularly sensitive to headlines related to the Israel/Iran conflict…

…The solid takedown of the 20-year auction didn’t prevent longer-dated yields from ticking higher and the curve steepening. We’ve been lamenting the fact that every auction brings with it an increasingly tired refrain of anticipating a buyers’ strike. There was no evidence of such a dynamic today, although we’re skeptical that the series of strong auctions seen since Liberation Day will, in totality, be sufficient to completely eliminate the specter of a pullback in overseas sponsorship for US Treasuries. Perhaps it won’t be until July’s auction cycle has run its course that the market will be comfortable moving on from the notion that the trade war will materially erode participation in Treasury auctions. After all, apparently auctions bring out buyers….

A fan favored German bank stratEgerist weighs in with some factoids on the BoJ news overnight …

… Overnight the Bank of Japan (BOJ) has left short-term interest rates at 0.5% as widely expected in a unanimous vote after a two-day policy meeting. More importantly, it announced that it intends to slow the rate at which it reduces its bond purchases next year. Beginning in April 2026, it will decrease its bond purchases by approximately 200 billion yen per quarter, down from the current rate of 400 billion yen per quarter. This action is likely aimed at minimizing market disruptions while still providing adequate support for the Japanese economy amidst economic uncertainty arising from US trade policies. Furthermore, the BOJ indicated that it will perform an interim assessment of the plan to reduce bond purchasing in June 2026. Looking ahead, attention is now directed towards BOJ Governor Kazuo Ueda post meeting comments. 5-year and 10-year Japanese Government Bonds (JGB) have increased by +4.3bps and +5.5bps respectively split before and after the meeting…

Amsterdam callin … calm cool and collected … AND a note about BUY AMERICA … back. again …

16 June 2025 ING: From Sell America to Buy America Back? What's next

Despite all the "Sell America" talk, the dominating impulse in more recent weeks has been "Buy America Back". Equity markets are up, credit spreads down and Treasury yields have calmed. We'll take it, even on a weaker dollar. But there are issues ahead. Specifically a double whammy of 4% inflation and more intense issuance pressure. Careful out there...

We've morphed to a Buy America Back phase

Some months ago, and well before 'Liberation day', we coined the phrase “Sell America Inc.” Post Liberation Day, it became a global thing, at least for a week or so. But since then, we’ve had a period we can only describe as “Buy America Back”. The calming in the generic all-in high yield to back below 7% is a decent metaphor for this. On the day of the tariff pause that yield had topped 8.5%.

The morph from "Sell America" to "Buy America Back"

The 5yr All-In High Yield (USD)

Source: Source: Macrobond, ING estimates

Similar can be seen on stock markets. The S&P 500 is not just an impressive 20% above the lows hit in the days after Liberation Day, but, frankly, an even more striking 7% above its pre-Liberation Day level…

…US Treasuries have calmed too as a consequence

Perhaps we can glean some information from the bond market, often seen as the deep thinker of financial markets. There too there has been some material calming. The 10yr Treasury yield topped out at 4.6% on the day the tariffs were paused. And while it has wobbled, it’s ultimately found its way back down to the 4.4% area. Recent subdued inflation data and rises in jobless claims have helped, in turn reflected in decent demand at the most recent 10yr and 30yr auctions. On top of that, the market discount for the Fed funds rate is both supportive (100bp of cuts discounted), and comforting. Comforting as the forwards discount a bottoming at or around neutral, and then a tendency for rates to edge back up again. We’d take that discount all day long, as if proven correct, there is absolutely nothing to worry about.

This looks like a soft landing plus a subsequent take-off

The Fed funds rate market discount plus the forward profile

Source: Source: Macrobond, ING estimates

Put simply, the markets are absolutely not discounting a recession of any consequence. Equity markets are well up, credit spreads are well down and the rates profile shows no signs of macro malaise. Sounds too good to be true? Feels that way…

16 June 2025 ING Rates Spark: On edge, but risk perception calms

Risk has calmed and Treasury yields are edging higher again, as we head close to a big Wednesday (FOMC, TIC data and 20yr auction). In the eurozone, the 10y EUR swap rate remains confined to its 2.4% to 2.6% range as the Israel/Iran conflict only adds to a long list of uncertainties while at the front-end energy price risks keep the ECB on edge

Risk calms and Treasury yields rise as we head close to a big Wednesday Volatility and credit spreads are on a declining path again. Developments out of the Israel / Iran spat are seen as either contained or manageable, with none of the worst fears for a wider impact materialising, as least not as of yet. US Treasuries broadly discounted as such from the very outset, preferring to home in on the potential inflationary ramifications rather than engaging on a safety play. This can cut both ways, and can manifest into a 'quality' flight. But so far the market has not been minded to morph this into a flight to bonds. Rather its been marked as a higher inflation risk and thus negative for Treasuries. The return of risk-on fits the same mold.

Ahead, the 20yr auction on Wednesday will be watched, as it tailed badly last time. At the same time, last week's 10yr and 30yr auctions went super well. Flows in the past week show some shedding of duration as a theme, and that can be gleaned from latest price action that is proving to be more heavy than seen in previous weeks. It seems when there is nothing front and centre to worry about that yields tend to creep higher, at least until we get some poor data to help pull yields back down again. The data in the coming days is mostly second tier, but still impactful enough to assess investor sentiment on direction.

Wednesday also sees the FOMC outcome, and we'll have the latest TIC flows data which will add some color to the appetite, or more likely the lack of it, as we progressed through a difficult period for Treasuries up until the tariff pause announced on 9 April. We expect to see some evidence of selling, but we doubt it will be as dramatic as some have predicted…

…Tuesday’s events and market view During the European session Germany’s ZEW for June will be the main indicator to watch with the consensus still seeing a further improvement, though some of the response will have come in ahead of the Middle East escalation. ECB’s Villeroy and Centeno are scheduled to speak.

US data will take centre stage with the release of the retail sales data for May. We already know that auto sales volumes were down heavily in May, which will drag down the headline retail growth rate, while a soft ISM report suggests manufacturing is receiving little benefit from the current trade tensions. The consensus is looking for a 0.6% month-on-month contraction in the headline figure, but still a 0.2% rise ex autos. Other data to watch are the import prices as well as industrial production.

In primary markets the EU has mandated banks for a tap of the EU Oct39 bond, which should be Tuesday’s business. Germany will auction taps of its 4y and 8y green bonds (€1.5bn) while the UK auctions 5y gilts (£4.5bn). The US auctions 5y TIPS (US$23bn).

Jamie Dimon’s bank offered a sneak peak of 5y TIPS auction but it was a tech update on long bonds which caught MY attention given the, “potential medium-term yield top pattern” …

…Technical Analysis The 30-year bond backs up for a second day after Friday’s bearish reversal day from key pattern and moving average resistance near 4.80%. We’ve highlighted the pattern neckline for what looks like a May-Jun yield top pattern in that area as a critical level for the near-term outlook (Figure 6). It is also important to note that the pattern has developed around the 5.15% May cheap, which effectively retested the 5.18% Oct 2023 cycle yield high. Furthermore, it unfolded within the most oversold conditions since the fourth quarter of 2024 and triggered a momentum divergence buy signal on the weekly time frame, a setup that points to a bullish bias into mid-summer. We are expecting the current backup to find buying interest near 5.00%. We suggested entering a 50% long trade near that level in last week’s mid-year update. A break richer than 4.80% would open the door for a rally to resistance levels surrounding 4.60%, in our view. Conversely, a re-acceleration of the bear market through 5.15-5.18% would turn our attention to the 5.32% Apr-May equal swings objective and Sep 2024 channel trend line as the next support layer.

Oil prices fall as risk sentiment recovers; USTs bear-steepen after on-the-screws 20y auction; CAD gains amid trade developments; mixed China economic activity data; ECB's Nagel sees need for flexibility; US Senate Republicans release revised tax bill; DXY at 98.14 (-0.0%); US 10y at 4.446% (-5.4bp)

…USTs extend Friday's losses with the steepening pressure accelerating after the 20y UST auction, despite the result being on-the-screws; 30y yields rise 6bp d/d with the 2s30s curve steepening 4bp d/d…

…US Senate Republicans release a revised tax and health-care bill which clarifies that portfolio interest is excluded from the taxes imposed under Section 899…

June 16, 2025 MS: Consensus Views Not Always Sizeable Consensus Positions | Global Macro Strategist

Feedback from our mid-year outlook suggests our directional views are commonplace among strategists and investors alike. In response, investors have taken a cautious approach to implementing them – sowing the seeds for disappointment as USD declines and the UST curve steepens further.

Key takeaways

Our views on a lower USD and steeper yield curve are only aligned with consensus in their direction. We expect much larger moves than the consensus.

With investor positioning cautious, supportive fundamentals and technicals, and sentiment strengthening, we stay convicted: sell USD, buy curve steepeners.

… US May retail sales will not reflect trade tax effects; aside from a small number of products (like bananas) pre-tax inventory is being sold. Meanwhile the Bank of Japan, as expected, slowed the pace of quantitative policy tightening in response to higher government bond yields.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

Stocks vs bonds usually will catch MY eyes …

June 17, 2025 at 5:00 AM UTC Bloomberg: For Markets, the Israel-Iran War Is Already Over Risks to the oil price and global economy appear likely to stay contained.

…Cold-Blooded Calculation Versus Complacency International markets appear to have convinced themselves that the latest conflagration in the Middle East can be looked through as easily as all the region’s other flare-ups of the last decade. Are they right to do so?

Gold prices fell, Treasury yields rose, and equity volatility dropped Monday as Israel and Iran continue to pound each other with bombs and missiles. Most startlingly, stocks rebounded; relative to long bonds, they are their strongest since the day after President Donald Trump’s inaugural:

All the normal signs of a “risk-on environment” were in evidence. This despite the fact that an Israeli attack on Iranian nuclear facilities has long been regarded as “the Big One” that could transform the global risk environment for the worse. And yet the oil price fell Monday, and it’s far below its January peak:

… Authers, here, goes on to cite the DB report noted / cited in this note / space YEST

Love the QEs reminder chart …

16 JUN 2025 Hedgopia: With Fed Unlikely To Surprise Markets With Decidedly Dovish Message, Major US Equity Indices Probably Eyeing Lower Prints For Now

Unless the Fed surprises the markets with a markedly dovish message on Wednesday, the major US equity indices act like they want lower prints for now. Large-cap indices last week came so close but failed to top February highs.

The FOMC (Federal Open Market Committee) begins a two-day meeting on Tuesday. The policy-setting body is expected to hold the fed funds rate steady at a range of 425 basis points to 450 basis points.

Last year, the benchmark rates were lowered by 100 basis points – 50 basis points in September and 25 basis points each in October and December. The futures market does not expect a cut this year until September, followed by another in December – for a cumulative 50 basis points, ending 2025 between 375 basis points and 400 basis points (Chart 1)…

This week is stacked with key economic releases. Kicking things off is June’s first Leading Economic Indicator: The Empire Fed Index (out today), which is followed by the Philly Fed on Friday. We’ll also see the NAHB housing market update Tuesday, along with May’s Housing Starts and Building Permits.

Don’t expect big moves based on housing data until longer-term rates drop meaningfully.

All eyes are on the FOMC statement Wednesday. While money supply has picked up since last year’s rate cuts, a sign the Fed’s plumbing is working, it’s unclear if the cuts are impacting the real economy. Yes, the yield curve has steepened, but indicators like housing sentiment (see chart) are still scraping the bottom…