Good morning … Thankfully, things have not gone from bad to worse in global markets overnight and early on, given weekend developments in the middle east.

That in mind, holiday-shortened weeks always seem longer (or is it just me)?

With markets closed on Thursday and little to no 1st tier data Friday, SIFMA is all but endorsing a 4d weekend with the week ahead, highlight being Wednesdays FOMC meeting, updated DOTS <GO> and press conference.

Today, hours after the ‘Empire State Mfg’ data point, Bessent & Co will ask Global Walls assistance in funding, offering 20yr USTs — a spot on the curve causing concern last month — and Global Wall will be watching.

… momentum (stochastics, bottom panel) are leaning more bearishly — a concession might be warranted BUT …

20yy WEEKLY: levels much the same but …

… here I’d note WEEKLY momentum looks qite the opposite and more bullish if ANYTHING at all so as always, see whatever you wanna see and keep your friends close and your stops closer …

Size and risk / reward / stops in mind, I’ll skip right ahead but first … here is a snapshot OF USTs as of 651a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: Broadly positive sentiment, Crude in the red despite continuing Iran-Israel strikes, ES +0.4% … Bonds fade overnight gains as inflation dictates recent action … USTs are currently softer. A pullback that comes after a brief spike to a 110-26 peak just after trade resumed, as desks digested the weekend’s geopolitical escalation between Iran and Israel. Thereafter, the benchmark waned and has been gradually under pressure since, despite crude moving into the red this morning. Thus far, USTs are holding around Friday’s 110-14 base but did briefly move a few ticks below this to a 110-10+ low. Focus ahead on a 20yr supply later, which may also be factoring into some of the pressure so far.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

Stumbling across this one (thanks to friends in low places), better late than never, IMO, is a weekly rates writeup from THE bank of the land…and a MONTHLY chart of 30s caught MY attention as they pose possibility of <gulp> bonds up TO 6.24% **IF** buyers do not defend 5.18% (double top) … read on …

13 June 2025 BAML: Global Rates Weekly SLR-umber party

The View: Remarkable range Several events in the next week—such as shifts in underlying macro data, central bank moves, fiscal developments, or geopolitics—have the potential to test recent ranges.

Rates: US data & sentiment shift = close pay Z6 & 10s30s US: US data & sentiment shifts = close pay July FOMC & Z6 + 10s30s steepener. Risk of higher Fed ’25 dot = pay Dec FOMC OIS; SLR changes coming but won’t matter much.

…Bottom line: we adjust trade recommendations due to recent mixed US data & shifting back-end rate sentiment (close pay July FOMC OIS, pay Z6, & 10s30s steepener). Fed dot plot shift next week should support our pay Dec ’25 FOMC OIS view.

… Technicals: US 30Y yield – summer spike risks US 30Y yield is retesting the cycle highs at +/- 5.18%. Long term history shows yield spikes tend to occur when forming seven double top patterns since 1997

Yields have risen in Q2 in line with a series of technical patterns and signals. US 30Y yield recently spiked to 5.15% which is near the Oct-2023 high of 5.18%.

Spikes help to signal key turning points especially when they occur at extreme levels with stretched positioning and sentiment. The spike in 30y yield this year tested a key level, which is notable, but presence of other conditions was less so.

Trend following indicators and patterns favor yield uptrends. Sentiment is hesitant to buy. A spike in yield where 30Y makes a higher high such as +/- 5.30% and ends the same period (day, week, month) below 5% may signal buying interest or top.

Our base case is that the latest developments in the Middle East are not a prelude to a further severe escalation. That said, the immediate market reaction looks complacent to us – we expect a further rise in geopolitical risk premiums over the coming days.

In the near-term escalating tensions pose a downside risk to our bullish view on the EUR and European spreads, but we remain positive medium-term. We stay long EURUSD and long Spain vs France but have taken profit on EURCAD and added a GBP downside hedge against further escalation.

The FOMC is likely to keep rates on hold this week, with the next live meeting likely not until October, as uncertainty around the inflation trajectory keeps the committee cautious.

… US rates: In US rates, the 10y and 30y auctions had the market on edge last week, given the widely talked-about ‘buyers’ strike’ for longend Treasuries. However, ahead of the auctions, we introduced our new Curve Option Skew Indicator (COSI), which measures the curve bias in positioning, and noted that investors currently have the highest underweight in long-end Treasuries versus the short end – i.e. the biggest steepening bias in the last 10 years (see Steepeners – big, but not as beautiful, 9 June 2025). We concluded that a rally led by long-end Treasuries could be a pain trade in this setup. Indeed, both 10y and 30y auctions registered strong end-user demand, helping the curve bull flatten through the week. We continue to like 2s10s conditional bull flatteners – a trade that does well under our base case of modest growth slowdown and better-than-feared fiscal picture, but does not lose if a ‘Liz Truss moment’ materialises (see Tail risks 2025: BNP Paribas grey-swan analysis, 11 February 2025).

Since equity futures are HIGHER along with bond yields — there’s almost NO identifiable impact of conflict in the middle east, save to say EARL and so …

Monday, Jun 16, 2025, 2:44 CitiFX Oil: Levels to watch

Oil prices have soared significantly on the back of the Israel-Iran conflict and the risk of potential disruption to global oil supply. In techs, Intraday price action broke through several resistance levels in both WTI and Brent. We think techs point to oil holding at these levels, with a risk of higher prices following the developments.

…WTI (CL1): Similar picture in WTI, with prices having broken the resistance at 68.65-70.93 (200d MA, 55w MA) and 72.28 (April high), We also hit the double bottom indicated target of 75.06. We note weekly slow stochastics is ticking higher as well.

Similarly, we think that WTI could hold above the 200d MA at 68.63 in the short term, with techs tilted for a move higher. We see resistance at 80-80.77 (psychological level, August 2024 high, 2025 high).

With the price of oil in mind as equities are recovering a bit, some further context offered out of German shop …

… As geopolitical shocks are becoming more frequent it seems its now at least a yearly occurrence that we refer to our equity strategists work on the impact of such shocks and how long it takes for the market to recover from them. Our strategists Parag and Binky reminded us of the work on Friday night and highlighted that the typical pattern is for the S&P 500 to pull back about -6% in 3 weeks after the shock but then rally all the way back in another 3. They believe this incident will likely be milder than this unless we get notable escalation as they highlight that equity positioning is already underweight (-0.33sd, 28th percentile), and a -6% selloff would need it to fall all the way to the bottom of its usual range. See their report here for more and the table of geopolitical shocks over the last 80 years and how it impacts equities. I may use it in my CoTD later …

… Ahead of that, the FOMC will attract the most attention this week outside of events in the Middle East. See our economists' preview here. As is widely expected, they expect the Fed to be on hold and maintain their existing biases in the statement, the Summary of Economic Projections (SEP) and Chair Powell's press conference. Having said that, the SEP will likely show weaker growth, higher inflation, and could show a softer labour market. With these adjustments, their baseline is that the median dot only shows one rate cut this year, though they admit it is a close call between that and the existing two. Beyond 2025 they expect only modest adjustments to the SEP, with the 2026 median fed funds rate moving 25bps higher, in part supported by a small increase in the long-run dot.

Powell's press conference is likely to emphasise uncertainty and a wait and see approach. The recent spike in oil will just add to all of this even if recent inflation data has been better than expected. Future price increases from tariffs loom in the background even if their initial impact has taken a bit longer to show up than expected. So it's a meeting where we could learn very little, partly as the Fed really don’t know which way the world is evolving and feeling that they have flexibility at current policy settings …

16 June 2025 DB: Mapping Markets: Will geopolitics actually have a market impact this time?

Geopolitics doesn’t normally matter much for long-run market performance. This is a pretty consistent pattern, including over the last two years with the Middle East. For instance, there was a brief risk-off move in April 2024 after Iran’s attack on Israel, but markets quickly recovered. Then in October 2024, further Iranian strikes led to an oil price spike, but when Israel’s response was more limited than many anticipated, prices fell back again.

This week’s events have clearly been much bigger than 2024. But apart from commodities and Middle Eastern equities, the wider market impact has been limited. In fact, the MSCI World index closed just over -1% beneath its record on Thursday, whilst US HY spreads widened just +2bps on Friday.

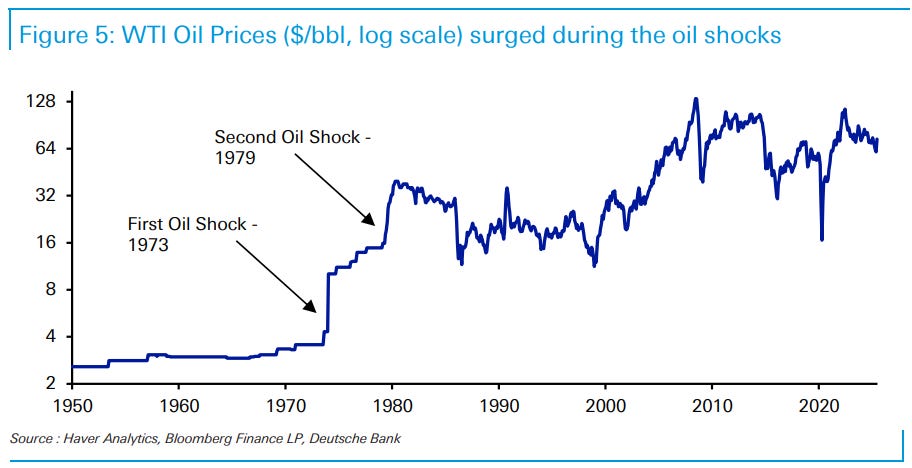

So what would cause geopolitics to have a wider market impact? Historically, it’s only been when it’s affected macro variables like growth and inflation. So for markets, the geopolitical events that mattered were the stagflation shocks, like the 1970s oil crises, the Gulf War in 1990, and Russia’s invasion of Ukraine in 2022.

Today, we haven’t seen a shock on that scale so far. Brent crude oil prices are still beneath their 2024 average of around $80/bbl. So this isn’t causing wider inflationary problems yet. Clearly, a larger price spike would evoke the 2022 scenario where central banks hiked rates to clamp down on inflation. But so far at least, we’re yet to see that. If anything, the extent of the market’s resilience to repeated shocks in 2025 has been a significant story in itself.

A(nother couple ) note from inbox yesterday morning …

June 15, 2025 MS: History Lessons in Timing the UST Yield Curve Steepener | US Rates Strategy

Most of the Treasury yield curve steepening leading up to cuts in the fed funds target rate occurs in the 3 months leading up to the first cut in the cycle. Our economists think the Fed delivers the first cut in the coming easing cycle in 8 months. Should you wait until December? We don't think so.

Key takeaways

Think the next rate cut will be small or delayed? Favor steepeners involving 30s. Worried about earlier or larger rate cuts? Favor steepeners involving 2s.

… Because we find ourselves caught between these two concerns, we like curve steepeners that marry both ideas, while trying to reduce negative carry and expected roll.

Of the UST 2s10s and 10s30s curve steepening that occurs in the 8 months leading into the first rate cut, about 80% of it occurs in the final 3 months.

The 10s30s curve steepened more than 2s10s when the Fed started with a 25bp rate cut, while 2s10s steepened more when the Fed started with a 50bp rate cut.

In the first 6-12 months of previous easing cycles, the 2s10s curve steepened much more for a given amount of rate cuts than the 10s30s curve did.

We continue to suggest US Treasury 3s30s curve steepeners and term SOFR 1y1y vs. 5y5y steepeners as a yield curve breakout could occur at any moment.

June 15, 2025 MS: Sunday Start | What's Next in Global Macro: A Détente, Not a Deal: The State of US-China Trade

While media headlines may have suggested last week's trade agreement between the US and China was a breakthrough, we think investors need to see it more as a détente than a comprehensive deal. The agreement represents a tactical pause in escalating tensions rather than a resolution of fundamental disagreements.

… For investors, we see value in positioning for slower growth and continued uncertainty in US-China relations. The currency and Treasury markets hold some opportunities here. Higher tariffs are leading to a weaker relative growth outlook for the US, which should pressure both the dollar and Treasury yields lower. Yet tariffs also create greater-than-normal uncertainty about the future path of inflation, suggesting that investors should position not simply for lower yields, but a steeper yield curve as longer-maturity yields must reflect this uncertainty. Adding to that dynamic are other tax policy proposals which could push up the risk premium that investors demand for US dollar-denominated fixed income assets. For example, remittance taxes and incremental foreign corporate taxes, if enacted, increase the costs of non-US actors in the US dollar ecosystem, which, over time, should be consistent with monetary policy easing and lower yields.

… Same shop on stocks AND another note on the global consumer …

June 16, 2025 MS: Weekly Warm-up: Leading Indicators Point to Earnings Resiliency

Key gauges we follow are pointing to a better EPS backdrop than many expect. Under the surface, we favor Capital Goods and Software, which are showing relatively strong EPS revisions in level and rate of change terms. These groups are also beneficiaries of a weaker USD and structural tailwinds.

… What Are the Risks? The main risk to our more constructive view remains interest rates. While last Wednesday's below consensus CPI report was helpful in terms of keeping yields contained, we find it interesting that rates did not compress on Friday amid the rise in geopolitical tensions and the risk-off price action in equities. As a result, the 10-year yield remains within close distance of our key 4.50% level, above which, rate sensitivity should increase for stocks. Our long-standing Consumer Discretionary Goods underweight is based on tariff-related headwinds, weaker pricing power and a late cycle backdrop, which typically means underperformance of this cohort—this cycle has been no exception. That said, staying underweight the group also provides a natural hedge should oil prices rise further amid recent events in the middle east, as consumer-related equities should be most sensitive to potentially higher fuel costs. Lastly, we would not be surprised if lagging macro data looks softer over the coming months as tariff impacts are felt and some payback in demand post the tariff pull-forward plays out. However, as discussed in detail last week, we think this type of moderate slowdown in growth without a labor cycle is already priced (the average S&P 500 stock already experienced a 30% drawdown this year). In fact, such data could actually prove to be bullish for stocks if it pulls forward more material expectations for Fed rate cuts and does not involve an accelerative rise in the unemployment rate.

June 16, 2025 MS: Global Economic Briefing: The Weekly Worldview: As the Consumer Goes

The step down in real consumer spending drives our US growth slowdown later this year.

Market economists have to remember that for an investor, the term for getting the analytics exactly right but getting the timing wrong is called being wrong. Since we cannot get the analytics exactly right all the time we have to be doubly humble about what we know about the timing. We have said tariffs and immigration restriction will lead to a meaningful slowdown in US and global growth. Last week’s CPI data for the US underscores that there has been no sign yet of the anticipated boost to inflation, but we still think it is coming and will likely peak in the third quarter. And the experience of 2018-19 tells us that slower growth will be another quarter later. For the rest of the world, we expect slower growth and lower inflation over the next year.

No evidence of the slowdown exists so far in the US data. Private final domestic demand, predominantly real consumer spending, has remained largely solid in the first quarter, and we expect the second quarter demand data to continue with moderate growth. When tariffs finally do show through to consumer price, some pullback will start to happen. But because the tariffs are hitting big swaths of capital goods and intermediate inputs to manufacturing, we expect a pullback from businesses, and as output slows, hiring needs will slow, and thus spending will slow. Higher inflation and slower hiring makes real incomes slow even more. These forces should push consumption growth lower in the third quarter. Slowing spending growth spills to the already decelerating labor market, and by the fourth quarter, payrolls growth stalls, as does consumer spending growth. And of course, in an economy, everyone’s spending is someone else’s income, so as businesses spend less and consumers spend less, incomes will slow more, leading to additional rounds of slowing.

We feel reasonably confident that overall growth will slow, but because the consumer is the driver of the US and global economy, are there risks for the consumer that could be skewed to the downside? A simple statistical model that decomposes trends in income, net wealth and spending suggests that the current saving rate is around desired target levels. One downside risk is that uncertainty about the economy, especially as the labor market softens up, could drive a rise in precautionary savings, especially by the upper income cohorts. Those upper income households disproportionately drive spending. Any greater slowdown in the spending of these cohorts would lead to an even larger slowdown in consumption growth. As for upside risk, the details of the fiscal package remain to be seen, but the SALT adjustments could support this group. More generally, a sustained resolution of the uncertainty around trade and immigration could also improve the outlook…

Swiss weighing in on conflict in the middle east …

The ongoing exchange of missile strikes between Iran and Israel this weekend has not had a major impact on financial markets. The severity of Israel’s initial strike against Iran was unexpected and caused a reaction. Further market moves would be justified only if there were expectations of even more disruption to energy supplies or shipping lanes.

The economic consequences of Middle Eastern conflict focuses on energy prices. The important issue is probably US inflation perceptions, as higher oil prices will hit just as trade taxes start to impact consumer prices. Higher US inflation perceptions and lower spending power might weaken US President Trump’s trade negotiating position, if international counterparts assume this undermines the US ability to continue raising taxes on their own consumers…

…The US Empire State business sentiment poll is unlikely to say much about economic realities. China’s May retail sales data were boosted by the early timing of a spending festival (service sector sales were more stable).

Housing. Things underneath are a changin’ and covered wagon folks would know, since they underwrite their fair share …

June 16, 2025 Wells Fargo: Housing Struggles Continue Amid Shift in Underlying Dynamics Housing Wrap Up

Summary Flipping the Script: Monetary Policy Getting Housing Back in Line The past several years have been anything but normal for the housing market. Ever since the pandemic, the residential sector has experienced a roller-coaster ride in mortgage rates, rapid home price appreciation, extremely low resale supply and a wave of new single-family and multifamily development. Through the first half of 2025, the script is starting to flip. Home sales generally remain weak, in large part due to persistently high mortgage rates. Yet, the underlying dynamics are shifting. Home price appreciation is softening, inventory is on the rise and construction is now pulling back.

The change can be owed to the long and variable lags of monetary policy. One way restrictive monetary policy works is by increasing financing costs to suppress demand and limit price growth. Housing has traditionally been a channel through which interest rate policy transmits to the economy. In this recent cycle, the residential sector was a target. Housing demand surged well ahead of available supply after the pandemic, creating a surge in housing prices and a significant source of inflation in general. Mortgage rates spiked in early 2022 as the Federal Reserve lifted the fed funds target rate in order to tamp down such price pressures. Inflation has receded since, yet mortgage rates are still highly elevated. As of this writing, the average 30-year mortgage rate stands just under 7%, essentially unchanged from year-ago levels and well above the 3% average rate that prevailed in 2021.

Although difficult for buyers, elevated mortgage rates do appear to be tilting the residential sector toward a more balanced state. Persistently weak home buying demand is now leading to increased supply, which is exerting downward pressure on home price appreciation. Overall, the pace of existing home sales has bounced around over the past several years, but the trend has essentially moved sideways since 2023. In April, existing home sales were running at a 4.0 million unit pace, roughly 25% below their pre-pandemic pace.

… and finally, from Dr. Bond Vigilante, a call and an economic week ahead …

Israel is in the middle of the Middle East. Iran's Mullahs have been threatening Israel's existence since they overthrew the Shah of Iran in February 1979. There has been a covert war between the two since then. It turned more overt last year and escalated on Friday when Israel launched a preemptive strike targeting nuclear facilities (Natanz, Khondab, Fordow), military installations, and residences of senior officials in Iran. The strikes killed key Iranian military figures, including IRGC commander Hossein Salami and Armed Forces Chief of Staff Mohammad Bagheri, along with nuclear scientists and civilians (reports vary from 78 to 90 deaths). Iran reported damage to oil fields and gas production facilities.

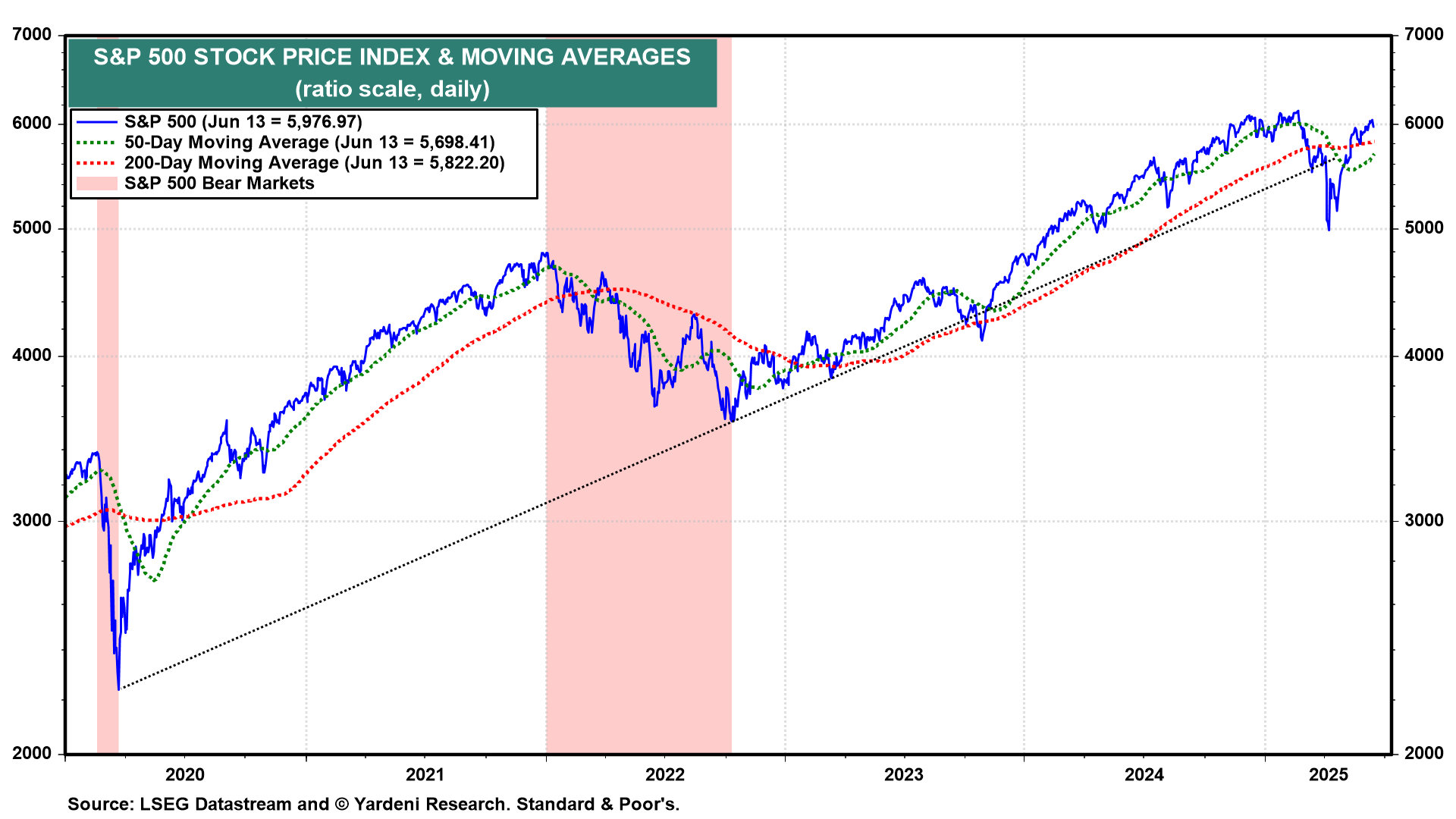

The S&P 500 is now in the middle of the Middle East. The S&P 500 fell on Friday on the unsettling news out of the region but by only 1.13% to 5,976.97, which remains not far below the February 19 record high (chart). We anticipated this development in last Thursday's QuickTakes and recommended using any selloff in the stock market as a buying opportunity.

We also reiterated our view that the 10-year US Treasury bond yield should remain around 4.50% through year-end. Following last week's lower-than-expected CPI and PPI inflation reports on Wednesday and Thursday, bond yields fell a bit on expectations that the Fed might respond to the good news by lowering the federal funds rate sooner rather than later (chart). Yields rose a bit on Friday on news of Israel's attack on Iran, which caused the price of oil to soar. The Fed now has to worry about the inflationary consequences of President Donald Trump's latest round of threatened tariffs as well as the price of oil.

The latest war in the Middle East means that investors are facing a host of known unkowns. How long will the war last? Not long if Israel continues to knock out Iran's military assets. Crippling strikes against Iran's nuclear facilities haven't occurred yet. But Iranians living near these sites have been warned by the Israelis to run for the hills to avoid radiation released when the sites are bombed…

Jun 15, 2025 Yardeni ECONOMIC WEEK AHEAD: June 16–20

The moment Fed watchers have waited for is finally here—albeit with less drama than many believed a few weeks back. As we've long said, the two-day June Federal Open Market Committee meeting (Tue-Wed) should come and go with the federal funds rate still in the 4.25%-4.50% range that it's been in since December. Even as headline inflation measures appear to moderate, the robust labor market, evidenced by May's 4.2% unemployment rate, leaves Fed Chair Jerome Powell with little urgency to ease.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

Recession or slowdown? Whats the diff …

June 15, 2025 Apollo: Slowdown Coming. But Not a Recession.

US economic growth is currently facing headwinds from higher oil prices, increased tariffs, the resumption of student loan payments, and higher long-term interest rates associated with the fiscal situation.

When we quantify these four drags on growth, we conclude that they are insufficient to push the economy into a recession.

In other words, these shocks are milder than those of Covid-19 and the Lehman crisis, see chart below.

However, we are closely monitoring these four risks to assess whether they become significant enough to put GDP growth into negative territory later this year—for example, if oil prices, tariffs, or long rates increase further.

… And a Monday kickstarted with a couple from The Terminal dot com …

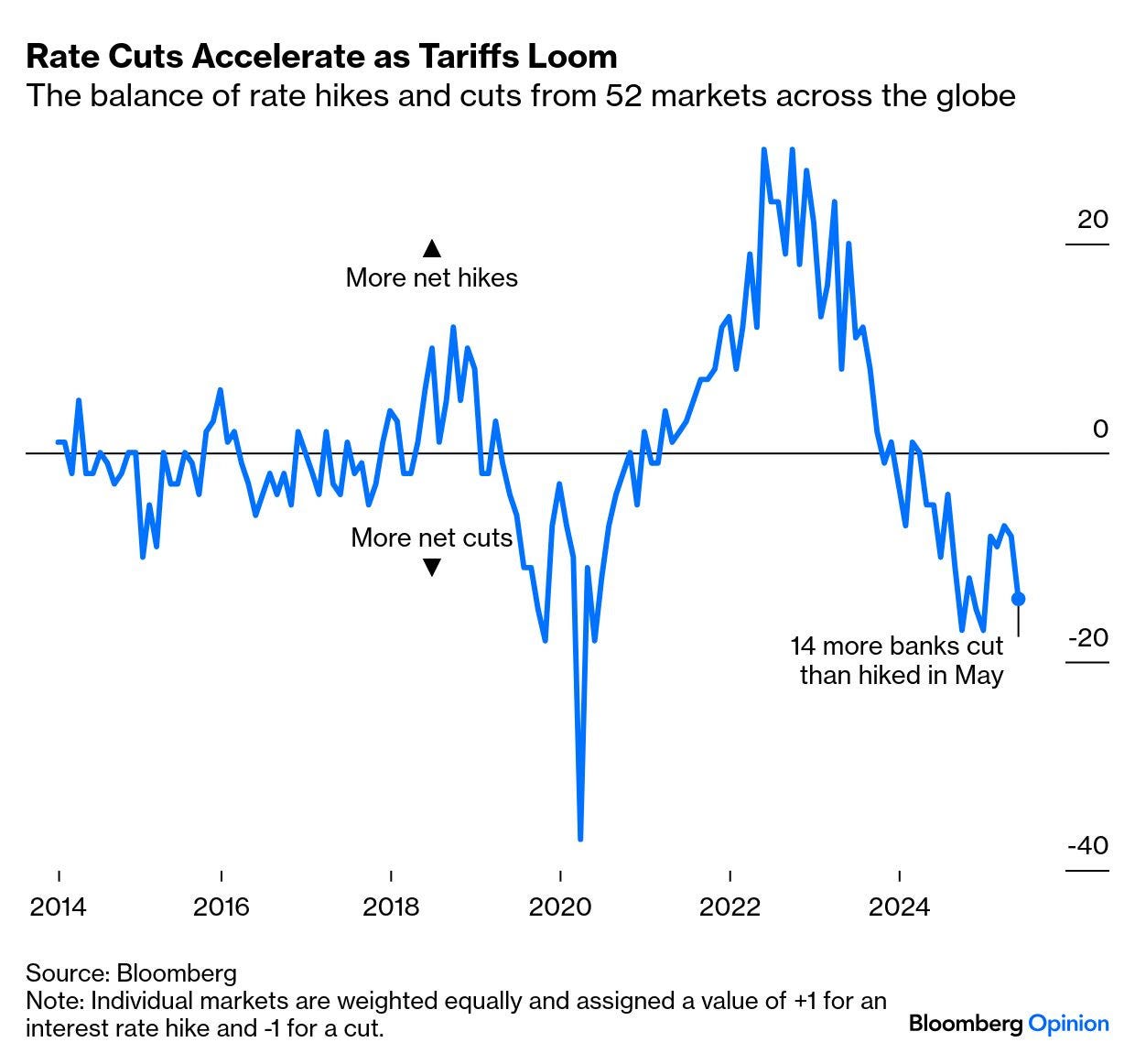

June 16, 2025 at 5:00 AM UTC Bloomberg: The US is exceptional — when it comes to rates The Fed is expected to maintain its pause as the gap widens with other central banks.

…Trump’s tariffs and their effect on inflation expectations have derailed easing cycles for a while. It’s not only the Fed that finds a “wait and see” approach more logical. But now, with optimism rising that the US trade policy bite won’t be so bad, cuts are the norm once more. This is the latest edition of our diffusion index, in which rate cuts or hikes by each of 52 central banks counts equally:

June 15, 2025 at 7:00 PM UTC Bloomberg: Bond Investors Look to Fed for Guidance on Timing of Rate Cuts

Treasuries investors whipsawed by President Donald Trump’s trade and fiscal policies will this week glimpse the impact on the Federal Reserve’s interest-rate policy.

While Fed Chair Jerome Powell and his colleagues are set to keep their benchmark steady at the June 17-18 meeting, traders will scrutinize economic and interest-rate projections for insight into how policymakers may respond to the uncertainty.

Markets ended Friday pricing in a roughly 80% chance the Fed next lowers rates in September, with less than two quarter-point cuts fully priced in by year-end. A rally in Treasuries last week was tempered Friday as escalating geopolitical tensions led to a surge in oil prices…

Sun, June 15, 2025 at 3:00 PM EDT Bloomberg: Fed on Hold Leaves Wall Street Asking What It Will Take to Cut Interest Rates

A fourth straight meeting without a cut could provoke another tirade from President Donald Trump. But policymakers have been clear: Before they can make a move they need the White House to resolve the big question marks around tariffs, immigration and taxes. Israel’s attacks on Iranian nuclear sites have also introduced another element of uncertainty for the global economy.

At the same time, the generally healthy, if slowly cooling, US economy has few expecting a rate move any time soon. Investors are betting the central bank won’t lower borrowing costs until September at the earliest, according to pricing in futures contracts.

“The safest path to take in that situation, when there is no urgency to cut rates right now, is to just sit on your hands,” said Seema Shah, chief global strategist at Principal Asset Management.

Policymakers gather June 17-18. They’ll release a statement at 2:00 PM Washington time, and Powell is scheduled to take questions from reporters 30 minutes later.

Difficult Choices The president’s tariffs are widely expected to raise prices and slow growth, risks that officials flagged in their last post-meeting statement. That could eventually force the Fed to make a difficult choice as the economy pulls them in opposite directions.

“I don’t think at this point there’s anything to be alarmed about,” said David Hoag, fixed income portfolio manager at Capital Group. “But the longer we have uncertainty — for the consumer, for companies in terms of planning — the more concerned I’ll get about the fundamentals of the economy deteriorating.”

So far, however, the economy isn’t flashing warning signs that would prompt the Fed to intervene.

The unemployment rate has held steady for three months even as job growth has slowed, in part because a sharp decline in immigration is also lowering the supply of workers. The longer the jobless rate remains stable, the longer the Fed can hold rates as a defense against potentially higher inflation.

Yet price data has also provided little to worry about. Underlying inflation rose by less than expected in May for the fourth straight month. Treasuries rose last week on the news, bolstered by wagers on more than one rate cut this year. The yield on two-year notes, most sensitive to the Fed’s policy, declined by more than seven basis points on the week to 3.96%.

Still, officials are likely to wait for additional months of data to understand how much of the tariffs are being passed on to consumers. Israel’s airstrikes on Iran will raise additional questions. Fed officials traditionally look through energy price moves, but an oil price shock could affect inflation expectations…

Sun, June 15, 2025 at 3:44 PM EDT Bloomberg: Global Rate Limbo Reigns After 150 Days of Trump

…US economic data in the holiday-shortened week include the latest readout of consumer demand. Economists project a decline in May retail sales, primarily due to fewer motor vehicle purchases. Excluding autos and gasoline, however, Tuesday’s report is likely to show sales firmed after a soft start to the second quarter.

Concerns have been building that flagging consumer sentiment will translate into a sustained pullback in household demand.

Also on tap are reports on May housing starts and industrial production. The Fed’s production report on Tuesday is seen showing a second month of declining manufacturing output, as factories contend with uncertainty stemming from trade policy.

Economists forecast figures on Wednesday will show little change in new residential construction, consistent with a sluggish housing market that’s battling various headwinds, including high borrowing costs…

Sam Ro details lots, as always and aside from macro chart review, his words on ups and downs — in biz as well as life — resonate with this guy, here, who’s still just about 39m post Bloomberg terminal access :) …

Jun 15, 2025 TKer by Sam Ro: Sometimes, the best business decision is to change businesses

… A quick personal note… The evolution of many companies isn’t too dissimilar from the ups and downs many of us face in our lives.

As I recently shared with Joe Fahmy on his podcast, my entry to writing about markets was anything but planned and orderly. And over the span of my career, I experienced at least six major pay cuts, including one big one that occurred after I got laid off.

Few of us are lucky enough to live a life where everything goes up and to the right in a smooth, straight line.

But most of us are on a non-linear path, whether by choice or because of forces outside our control.

The good news is that just because things don’t go as planned doesn’t mean we’re doomed to spiral. Read enough biographies (and business case studies), and you’ll eventually see that the most impressive people (and companies) were the ones who had to overcome many challenges by making big, unplanned changes.

Just a thought.

…Card spending data is holding up. From JPMorgan: “As of 06 Jun 2025, our Chase Consumer Card spending data (unadjusted) was 2.7% above the same day last year. Based on the Chase Consumer Card data through 06 Jun 2025, our estimate of the US Census May control measure of retail sales m/m is 0.45%.”

(Source: JPMorgan)

From BofA: “Total BAC card spending per HH was up 0.8% y/y in May…

Credit markets are currently pricing in a 6-level credit downgrade for the United States, which would give it a rating of BBB, just a smidge above investment grade

https://t.co/iWGdomCBwx

This seems overly pessimistic....

Credit markets are currently pricing in a 6-level credit downgrade for the United States, which would give it a rating of BBB, just a smidge above investment grade