while WE slept: USTs (and Global Wall) aggressively UNCH; 10s at (1st) resistance; "Seasonal patterns in ... 10y UST yield"; 'mystery bond buyer' identified (Bessent)

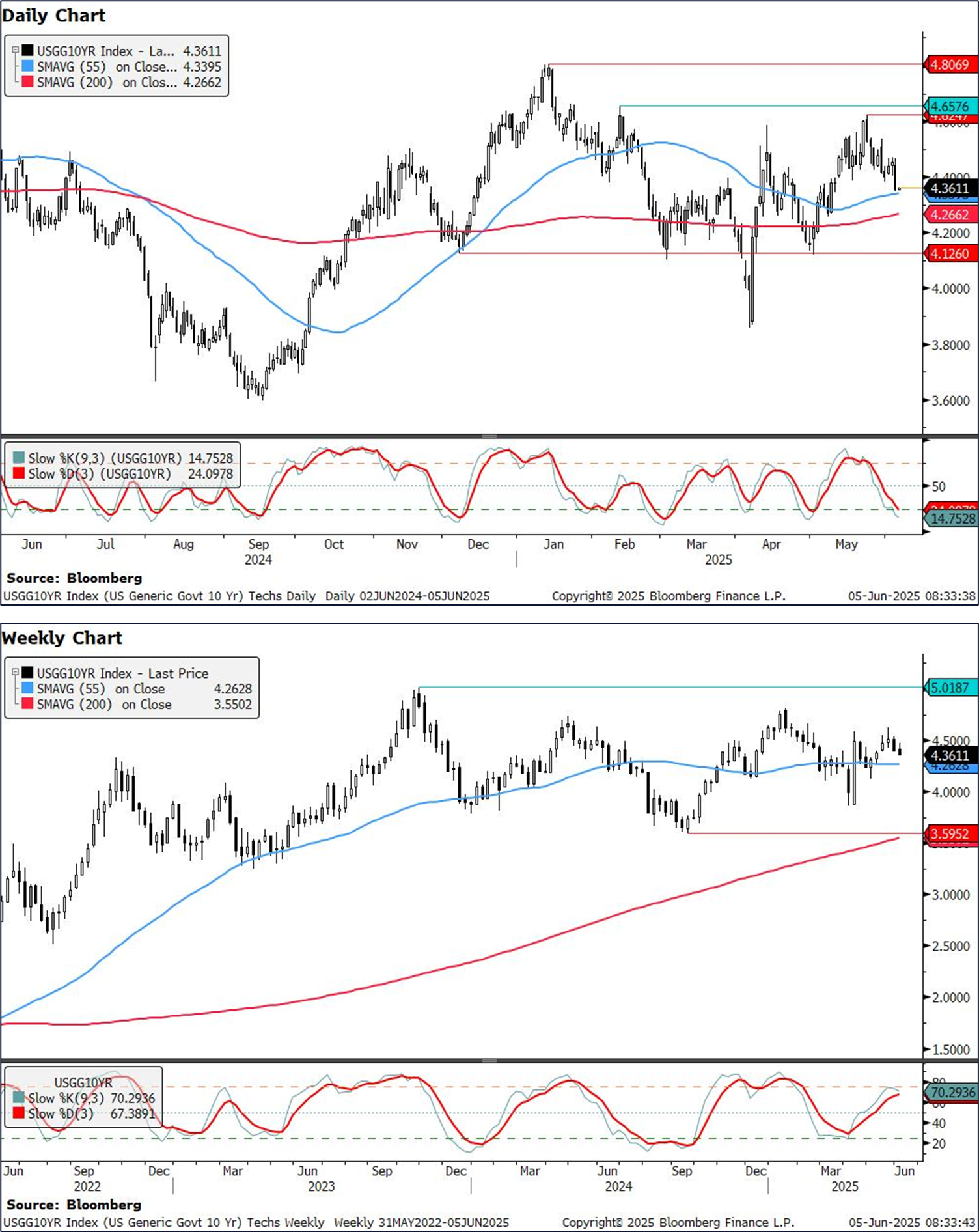

Markets have seen a move lower in US treasury yields following weak ISM services and ADP numbers on Wednesday. This means that 2y yields have broken below 3.89% (55dMA) while 10y yields are testing support at 4.34% (55d MA). Nevertheless, we do not think that this changes the broader picture yet.

Key levels to watch:

2y yields: Support at 3.75%, followed by 3.62%. Resistance at 4.07-4.08%

10y yields: Support at 4.34%, followed by 4.26%. Resistance at 4.62-4.65%.

30y yields: Support at 4.79%, Resistance at 5.18%

…US 10y yields 10y yields have closed just above support at 4.34% (55d MA) on Wednesday. We are also neutral on yields here after having called for a small move lower last week following the engulfing candlestick. Daily slow stochastics entering oversold territory adds to this picture. As a a result, we prefer to look to the weekly close for a further technical signal.

A weekly close below 4.34% opens the door to a move to 4.26% (55w MA, 200d MA). If we hold above, then it would emphasize that we still remain in the 4.34%-4.65% range (Feb high).

Note that weekly momentum is looking to cross lower again after touching overbought territory. While we keep this in mind, we do not think this is a strong signal yet, and prefer to look for further signals to add to the building blocks.

… With this in mind, a quick run through data set which brought us here to this moment … Yesterday kicked of with ADP …

ZH: "Too Late!" - Trump Blasts Powell After Weakest ADP Jobs Report In Over 2 Years

… the flow of news got even more funTERtaining …

ZH: Baffle 'Em With Bullshit: Services Surveys Signal Soaring & Plunging Economy

… even MORE good / fun news fannin’ the rate CUTS flames …

ZH: Oil Prices Tumble On Report That Saudis Want To 'Super-Size' OPEC Production Hikes

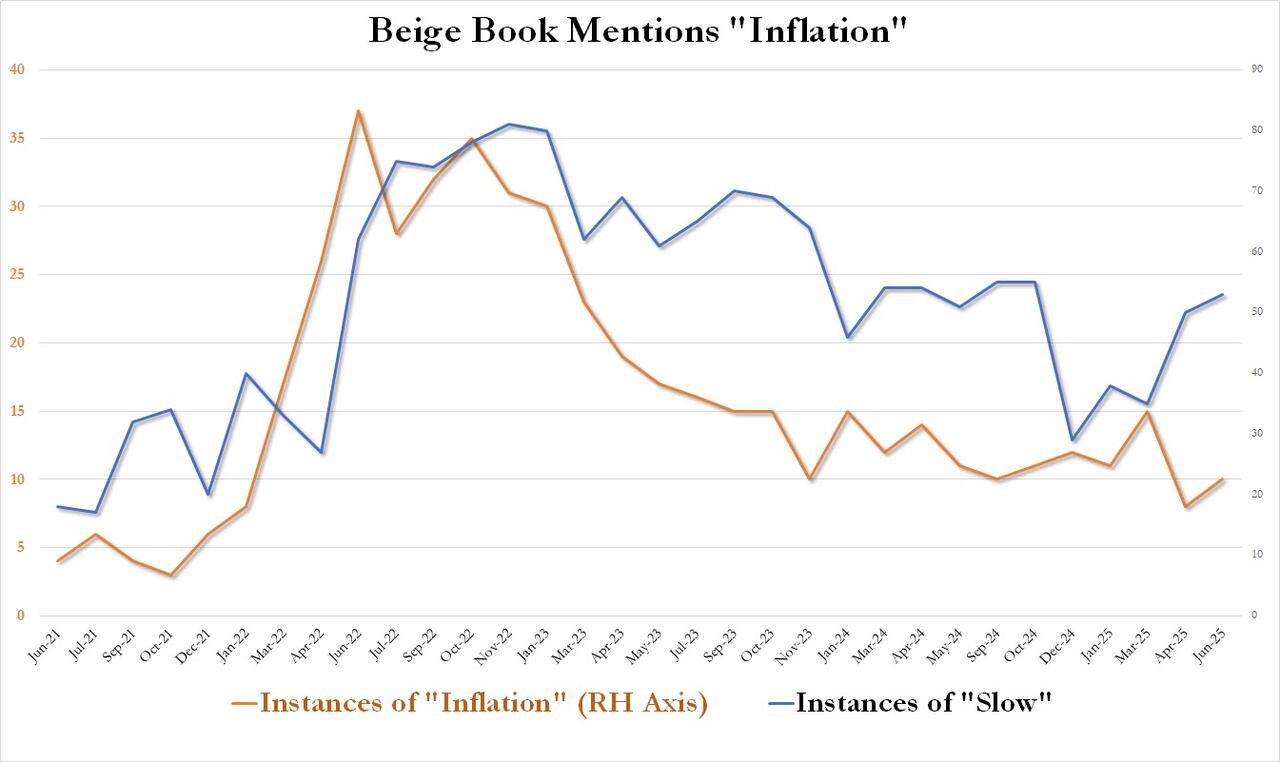

… Finally, in the afternoon, the BEIGE BOOK …

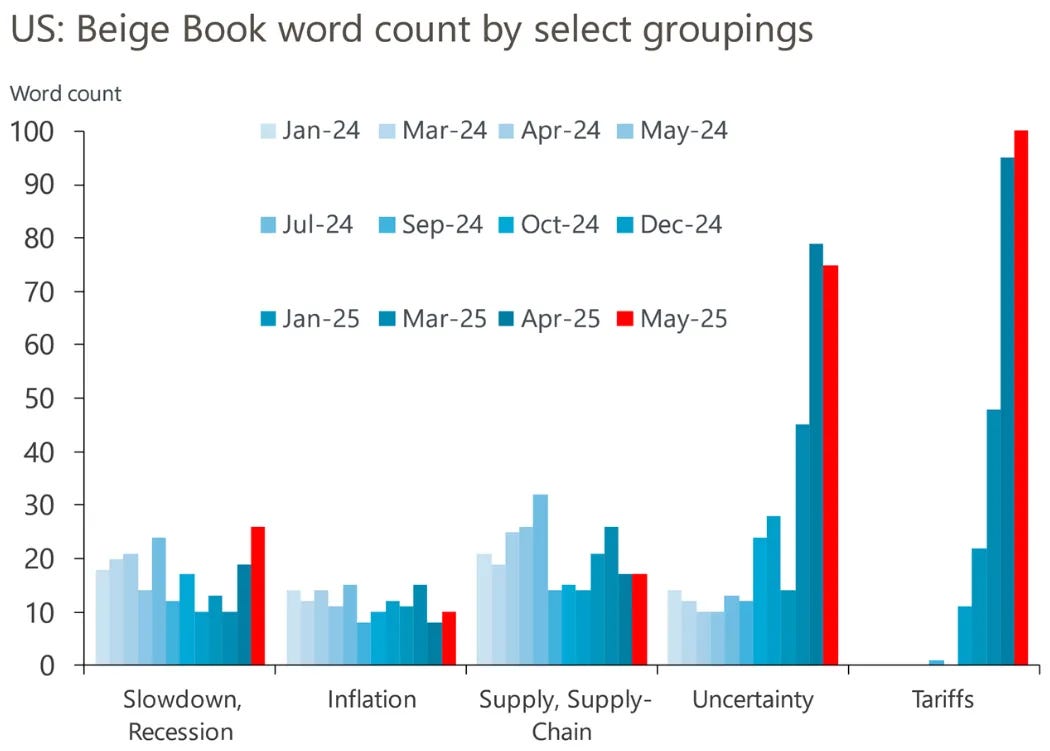

ZH: Beige Book Finds US Economy Diverging By Party Lines, No Trace Of Runaway Inflation

… And finally, confirming that contrary to conventional wisdom the economic picture has been largely unchanged since April, the latest February Beige Book saw just 1 mention of recessions, the lowest this year, and down sharply from 6 three months prior. Where there was some concern is that mentions of "slow" rose from from 50 in April (which was down to 53, the biggest highlight for another month is that contrary to prevailing media narratives, mentions of inflation actually rose ever so modestly from a three-year low of 8 to 10, the second lowest going back to the start of 2022.

All of which suggests that the US economy - while hardly on fire as it was during the hyperinflationary period of Biden's admin - continues to chug along and is hardly collapsing as so many Trump foes would like to see; and it certainly is not seeing prices explode higher.

… MORE on the BEIGE below but for now … here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT USTs are twist-flattening after some dynamic px-action overnight. Initially, UST strength failed to carry into the Asia reopening with UST futures under pressure (on several small futures block sales) into the 30y JGB auction. After a bullish reversal/digestion of the weaker auction however, duration has been led higher by EGBs following stronger auctions in Spain/France and a weaker Eurozone PPI print. S&P futures are flat here at 6:45am, 10s flat as well, with Crude +0.5%, Copper +2.5%, Silver +3.6% and DXY -0.1%.

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: DXY lacklustre & US equity futures firmer but off best ahead of the ECB, US data and Trump-Merz … Bonds broadly trading near session highs, Bunds benefit after strong auctions from Spain/France … USTs are higher by a handful of ticks and within a 110-12 to 111-07 parameters. Specifics light in the European morning and no catalyst behind it but US equity futures, and European peers, saw a jump just after the European cash equity open. This weighed on USTs slightly to a 111-00+ base. From a US standpoint, Fed speak, Jobless Claims and Challenger Layoffs are all due.

Reuters Morning Bid: ECB to cut, Fed hopes up

Today's key chart

U.S. economic activity has declined and higher tariff rates have put upward pressure on costs and prices in the weeks since Federal Reserve policymakers last met to set interest rates, the Fed's latest "Beige Book" said on Wednesday. "On balance, the outlook remains slightly pessimistic and uncertain", concluded the report. "There were widespread reports of contacts expecting costs and prices to rise at a faster rate going forward."..

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ … Without much in way of comment, what I see below mostly a bond market reflex bid and data recaps …

UK on what services say and the short-comings of the GDPNow …

4 June 2025 Barclays: May service ISM: Some "stag" and some "flation"

The ISM services PMI weakened 1.7pts in May, occupying sub-50 territory for the first time in nearly a year. The estimates show some "stag" and some "flation," with activity and new orders both plunging and the prices paid index reaching heights not seen since the post-pandemic supply chain crunch.

5 June 2025 Barclays GDPNow: Crosswinds expose methodological shortcomings

The latest readings for the Atlanta Fed's GDPNow tracker point to Q2 GDP growth exceeding 4% q/q saar. We strongly caution analysts to be skeptical about this measure amid a second consecutive quarter of wild tariff-related distortions to the international trade data.

Treasuries rallied sharply on Wednesday as a weaker-than-expected round of economic data fueled economic jitters …

… As for the price action, 10-year notes headed into today’s ADP update at 4.45% but ultimately slipped below 4.35% in the wake of the weaker private hiring and ISM Services figures. The 10+ bp rally breached a number of key technical hurdles and led to a departure from the 4.40-4.60% trading zone that had defined the price action since May 12th. Daily momentum remains bullish but stochastics are quickly approaching overbought territory. The 50-day movingaverage of 4.345% is now initial resistance and if that level is breached, a rally would go largely unimpeded by the technicals until the 200-day moving-average of 4.264%. Should we see a bearish retracement, 4.40% should offer some support in the path toward the departure point for today’s rally at 4.45%. Through there is a clear path until the all-important 4.50% …

… There’s been chatter about a WSJ article that was published on Wednesday that was titled, “Economists Raise Questions About Quality of U.S. Inflation Data.” The write-up said, “Economists say the staffing shortage raises questions about the quality of recent and coming inflation reports.” For context, today the BLS reported, “BLS is reducing sample in areas across the country… These actions have minimal impact on the overall all-items CPI-U index, but they may increase the volatility of subnational or item-specific indexes.” With the CPI series to be constructed with less data than usual in the coming months, there are concerns about the accuracy and volatility of the inflation data at a moment when tariffs are expected to drive up prices, although it’s unclear whether a greater reliance on imputed data will skew inflation higher or lower.

… continuing ‘round the globe, a few words from Germany …

… In terms of the market reaction, both the ADP and the ISM services prints led investors to price in more rate cuts this year, with clear moves in response to the two prints. In fact by the close, futures were pricing in 58bps of rate cuts by the Fed’s December meeting, up +8.0bps on the day, and the highest number in over three weeks. And there’s growing confidence that we’ll see the first rate cut by September, with futures now almost fully pricing (97%) one by that meeting. Given the additional rate cuts being priced, that triggered a major surge for US Treasuries yesterday. So at the front end, the 2yr yield was down -8.5bps on the day to 3.87%. And for the 30yr yield, the -10.3bps move was actually the biggest daily decline since February, pushing the yield down to 4.88%. Only a small amount of that rally has unwound this morning, with the 10yr yield up +0.6bps, and the 30yr yield up +0.5bps.

The large slide in Treasury yields had the added benefit of reassuring investors about the fiscal situation, which had been in growing focus as the 30yr yield hovered around the 5% mark. So even with the weak economic data, risk assets held up reasonably well with the S&P 500 (+0.01%) narrowly posting a 3-month high in a session that saw the lowest daily trading range for the index since mid-February. The S&P 500 now stands just -2.82% beneath its all-time high in February, although futures this morning aren’t suggesting much momentum, with those on the S&P 500 down -0.05%…

Netherlands on survey says …

4 June 2025 ING: US surveys slide further on trade uncertainty

Very weak ISM service sector data and a soft jobs number from the ADP indicate that the corporate sector remains concerned about the economic environment despite the recent de-escalation in some of the trade tensions. Until there is clarity on the trading envirtonment it appears that the business sector will remain wary of putting money to work

…Today’s US economic data has provided more reason for caution on the US economic outlook. The key report was the surprisingly soft ISM services index, which has dropped below the 50 break-even level into contraction territory for the first time since June last year. The 49.9 outcome for May is down from April's 51.6 and below the consensus forecast of 52.0. It also means that we have both the services survey and the manufacturing survey pointing to tougher times ahead for the economy. The chart below shows the relationship between the ISM manufacturing and service sector output series. Both are now reporting a clear softening that points to the risk of much cooler GDP growth in the second half of 2025.

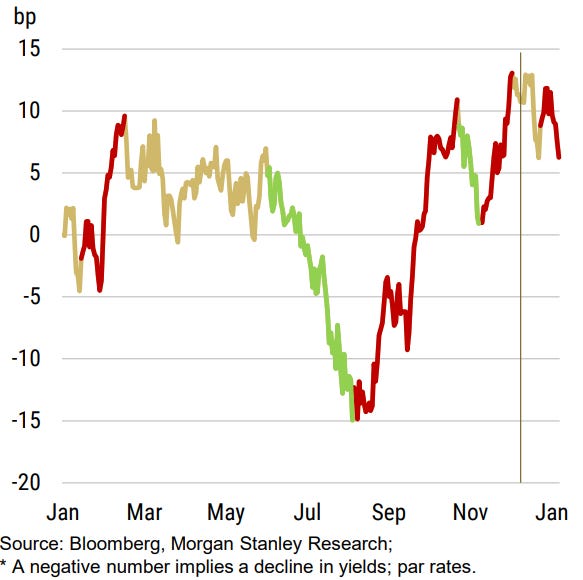

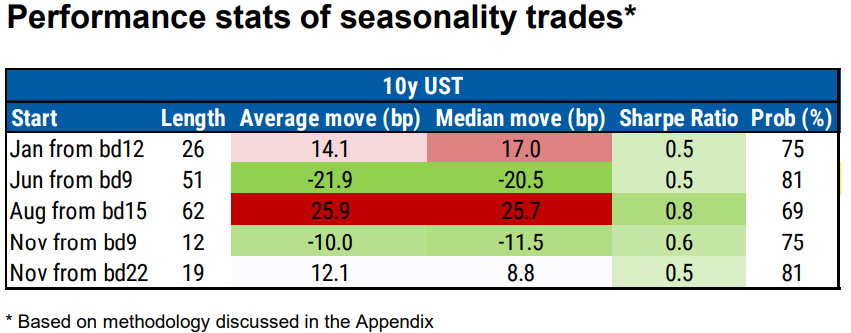

We look at the seasonal patterns in EUR, UK, and US rates markets. We are about to enter a seasonal period for rates, with a rally expected in the next few weeks followed by a sell-off in August.

…Seasonal patterns in duration: 10y UST yield Average performance for the 2009-24 period*

The chart above shows the average cumulative change in bond yields in bp (1st Jan = 0) for the 2009-24 period

The table above shows the main statistics for strong seasonality patterns: sell offs starting in January, August (strongest) and November, and rallies starting in June and November…

USTs rally after soft economic data; ISM services data raise stagflation concerns; BoC keeps rates on hold; KRW and local equities gain after South Korea election; SOFR swap spreads extend widening; DXY at 98.81 (-0.4%); US 10y at 4.355% (-9.9bp)

USTs rally sharply (10y: -10bp) after a sizeable miss in ADP employment at 37k (C: 114k) with the move accelerating after ISM Services unexpectedly falls into contraction, heightening growth fears.

ISM Services data signals stagflation concerns, weakening to 49.9 (C: 52.0; P: 51.6); growth slows with new orders entering contraction territory for the first time since June 2024, while the Prices Index rises to its highest level since November 2022 …

Switzerland has no problems so they’ve gotta talk ‘bout ours …

… US President Trump is likely to become even more irate after criticizing the Federal Reserve for not cutting rates. Fed Chair Powell’s insistence on data dependency certainly increases the risk of policy error (policy operates with a lag, and real time data is increasingly unreliable). While data dependency is normally a bad option, there may be little choice now. Per yesterday's Beige Book, the US economy is plagued by growth and inflation uncertainty.

US first quarter productivity data is not market moving. Actual productivity matters enormously to long-term trend growth. Technology should boost productivity, but also increases fear of the future. That encourages scapegoat economics—scared populations blame others for their insecurities. Groups whose status recently improved (e.g., LGBTQ+ groups) and foreigners are traditional scapegoats. The resulting prejudice politics undermines long-term growth. How we use technology is what really matters, which requires the right person, the right job, and the right time. Random immigration bans, attacks on LGBTQ+ people, and economic nationalism undermine trend growth…

… Covered wagons rolling in …

June 4, 2025 Wells Fargo: Some Early Signs of Service-Sector Stress in May ISM

Summary The Services ISM flashed contraction in May. The overall report was a bleak read on service-sector activity, but the details mostly reflect the dynamics of a pull-forward in demand ahead of tariffs. The plunge in demand does not bode well for coming activity, but it's too soon to know if cost pressure will be sustained and its influence on hiring.

The 10-year US Treasury bond yield fell to 4.36% today on a batch of weaker-than-expected economic indicators. Bond investors weren't fazed by Elon Musk's attack on President Trump's "big beautiful bill" on Tuesday afternoon. Musk thinks it’s ugly: "This massive, outrageous, pork-filled Congressional spending bill is a disgusting abomination." Nor were they fazed by the fact that the Congressional Budget Office said today that the bill (as passed by the House) could add $2.4 trillion to the federal budget deficit over the next 10 years. The Committee for a Responsible Federal Budget reiterated that the bill will more likely increase federal government debt by $3 trillion, or roughly $5 trillion if made permanent. The Trump administration counters that better-than-expected economic growth will bring in more revenues.

The bond market apparently isn't on the verge of a debt crisis, as widely feared just a few days ago. Instead, investors bought US Treasuries today in response to weaker-than-expected reports from ADP on private payrolls and ISM on nonmanufacturing business activity. Nevertheless, they didn't shake our confidence in the resilience of the economy, as we discussed again yesterday. Consider the following:

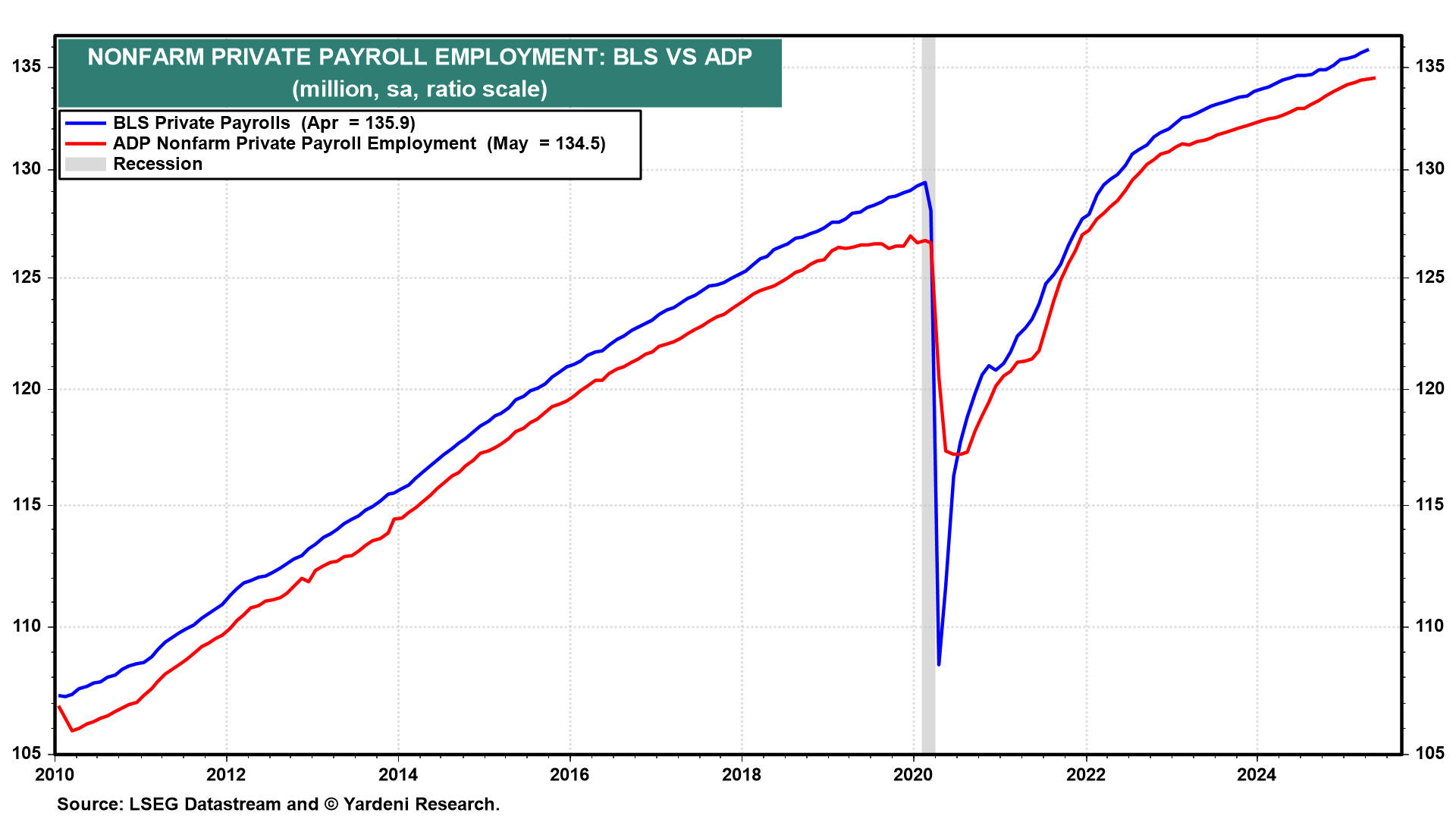

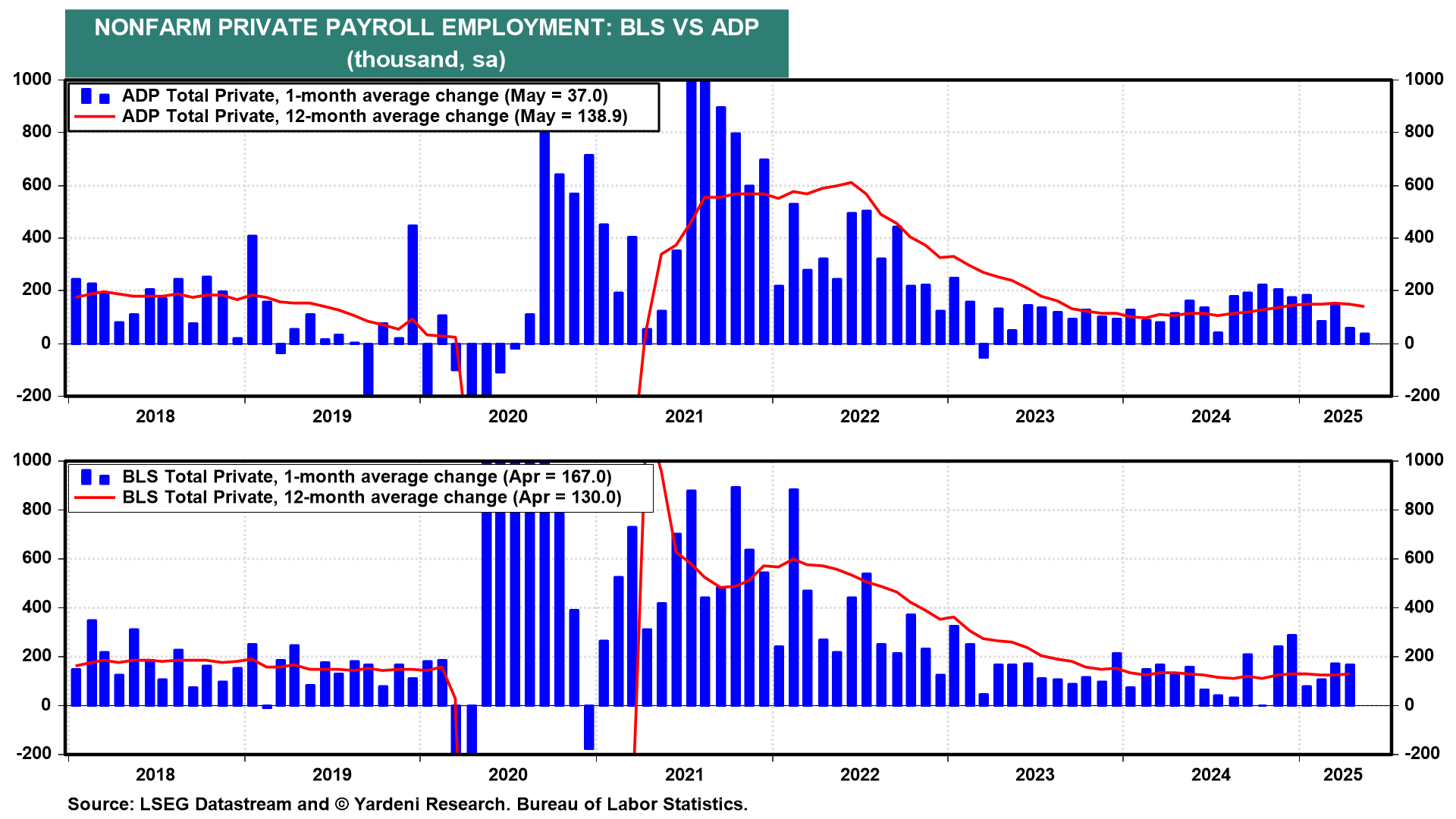

(1) ADP payroll report. While ADP’s private payrolls series does track the Bureau of Labor Statistics’ (BLS) private payrolls, it doesn't track monthly changes in the latter very well (chart).

Given the strength of other employment indicators, we doubt that private payrolls rose just 37,000 in May (chart). We still expect a May gain exceeding 100,000 in the BLS series, which will be reported on Friday. We also expect a significant upward revision in April's BLS gain, as we explained yesterday.

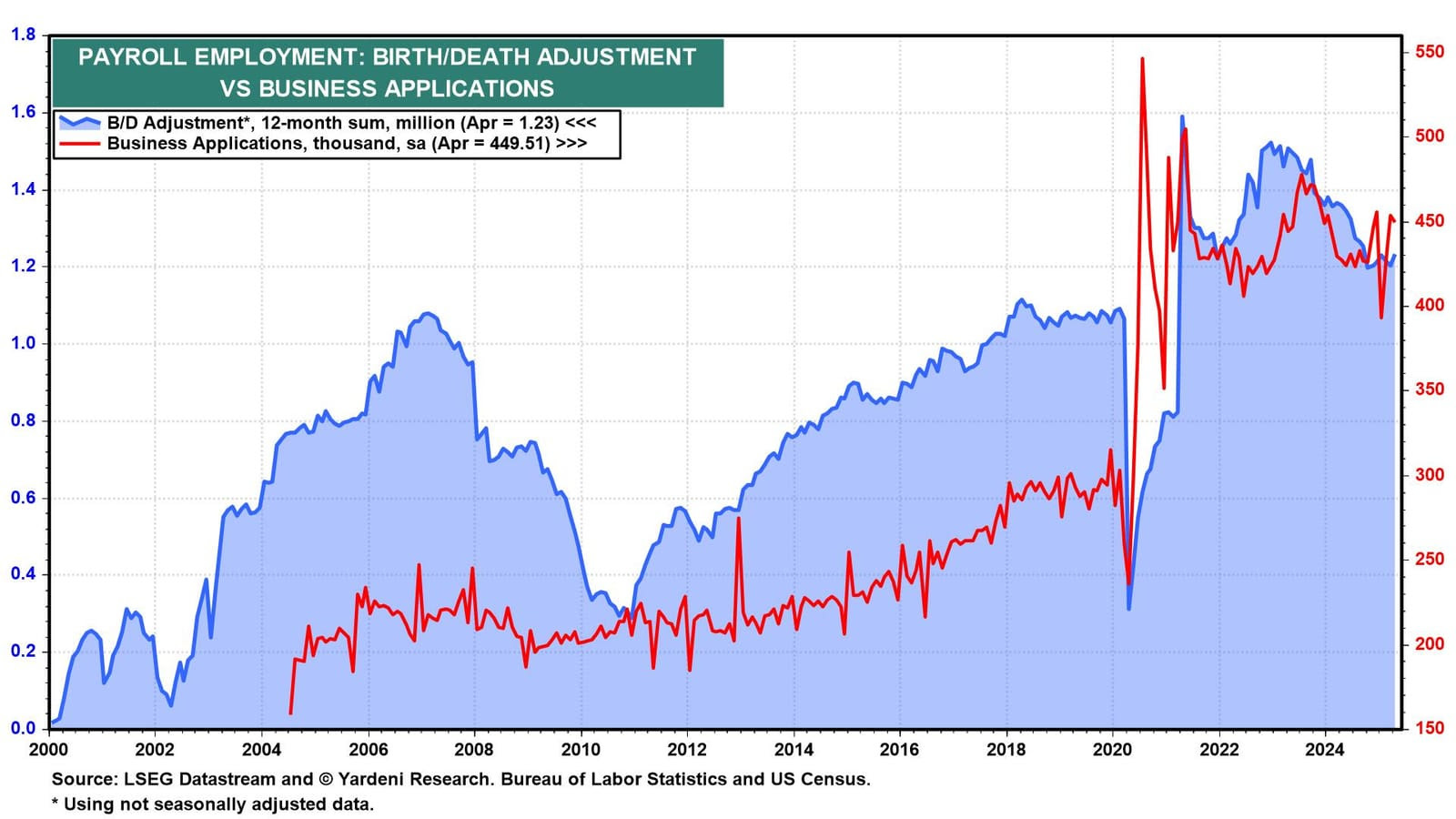

We note that monthly business applications remained very strong at 449,510 during April (chart). That's impressive considering the drop in the stock market as well as the weakness in consumer and business confidence surveys during April on terrifying tariff fears.

(2) ISM purchasing managers reports. The drop in the ISM's national NM-PMI, to 49.9 (indicating a contraction of the non-manufacturing, or services, sector, since it dipped below 50.0) also challenges the economy's resilience (chart). The new orders subindex fell to 46.4. The employment subindex was relatively weak at 50.7. That's unsettling since the services economy has accounted for most of the strength in the labor market all year. Also weak last month was the ISM's national M-PMI, for manufacturing industries, at 49.9.

Then again, the S&P Global measures of both the M-PMI and NM-PMI strengthened in May to solid readings of 53.7 and 52.0 (chart). Go figure!

Yesterday, we observed that the weak ISM national M-PMI has been a misleading indicator of the solid growth rate of goods in the real GDP calculation over the past three years. The NM-PMI has been a better indicator of the growth rate of services in real GDP (chart). However, the weak reading for May's NM-PMI doesn't jibe with the AtlantaFed's current GDPNow estimate showing a robust 3.2% (saar) increase in real personal consumption expenditures on services.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

A view from one of Global Walls more popular OpEd’ers … seems more positive than many (so maybe not fully buying IN to Team Rate CUT narrative …

June 5, 2025 at 4:00 AM UTC Bloomberg: The Dark Side of Data Needs Some Tariff Light The US economy is showing signs of strain. But there are some caveats.

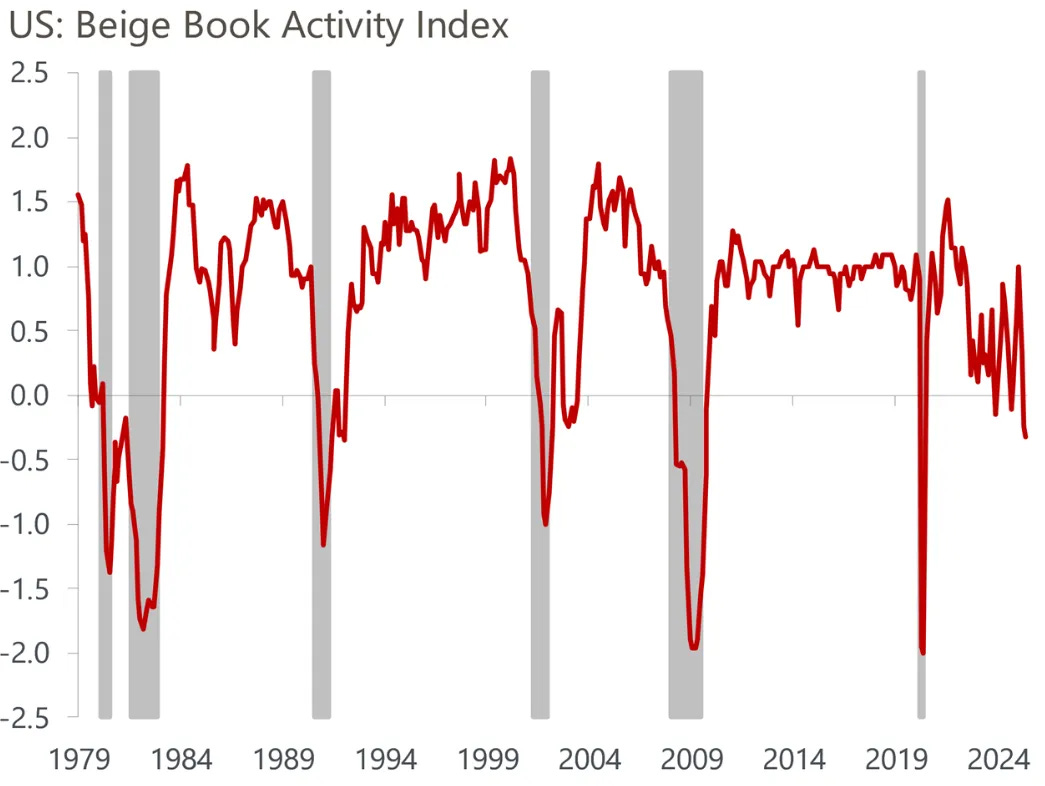

… In the afternoon, the Federal Reserve published its Beige Book, which comes out ahead of each Federal Open Market Committee and smooshes together anecdotal reports from the central bank’s regional branches. It’s impressionistic, but it’s easy with current technology to count words and produce something quantitative. This is Oxford Economics’ index of the strength of economic activity, and it suggests Fed officers are more negative than they have ever been outside of official recessions:

No prizes for guessing what the Fed’s contacts talked about most. Mentions of tariffs continue to rise, even though this survey covered the period after the administration had backed down on the main threats it made on “Liberation Day:”

US equities registered another small rise, but had their worst day relative to bonds since April, as yields fell significantly. The dollar had a bad one, too. All of that makes sense on a day of much so-so economic news.

Now the caveats start. These numbers were produced under massive tariff uncertainty. Traders can blithely assume that President DonaldTrump “always chickens out” and keep on taking risks, but people trying to run businesses have to be more careful. The lull in activity might easily end as soon as there is clarity that tariffs aren’t happening.

Then there’s the problem that the data may not be trustworthy. Government cuts mean fewer people to do statistical grunt work. Calculating inflation, in particular, is a labor-intensive endeavor. And so it was chilling to see the Bureau of Labor Statistics’ announcement that in April it suspended consumer price indexdata collection entirely in Lincoln, Nebraska, and Provo, Utah, followed this month by Buffalo, New York.

This is not an entirely new problem. Points of Return wrote 18 months ago of the sharp fall in response rates to labor surveys. “Garbage in, garbage out” tends to hold good: If the government lacks people to collect data, and people don’t cooperate, it’s easy to cast doubt on the numbers.

That’s one explanation for why such ostensibly poor figures have left the futures market still only pricing in one fed funds rate cut, which will not happen until September. Two months ago, futures priced in three cuts by then, at a time when the macro data looked stronger:

President Trump evidently thinks they should cut more. After the ADP data, but with more bad news still to come, he posted:

“ADP NUMBER OUT!!! ‘Too Late’ Powell must now LOWER THE RATE. He is unbelievable!!! Europe has lowered NINE TIMES!”

The European Central Bankhas in fact cut seven times to date, with an eighth more or less certain a matter hours after you receive this, and has a weaker economy and lower inflation. It’s not so ridiculous that it has eased more than the Fed. But Trump has a point that apparent weakness on the scale suggested by the data of the last few days would normally translate into imminent easier money.

The problem remains the tariffs. The Fed needs to be clear that Trump really has chickened out before it cuts rates.

… AND a word on JGBs overnight from the same outfit …

June 5, 2025 at 4:11 AM EDT Bloomberg: Japanese Bonds Rise as 30-Year Auction Brings Some Relief

… While immediate market reaction indicated relief — yields edged lower after the sale — the bid-to-cover ratio of 2.92 at Thursday’s offering points to a general lack of appetite for longer-maturity debt that is afflicting markets from Japan to Europe and the US.

… as good as that sounded, well, didn’t allow us to enjoy it long at all …

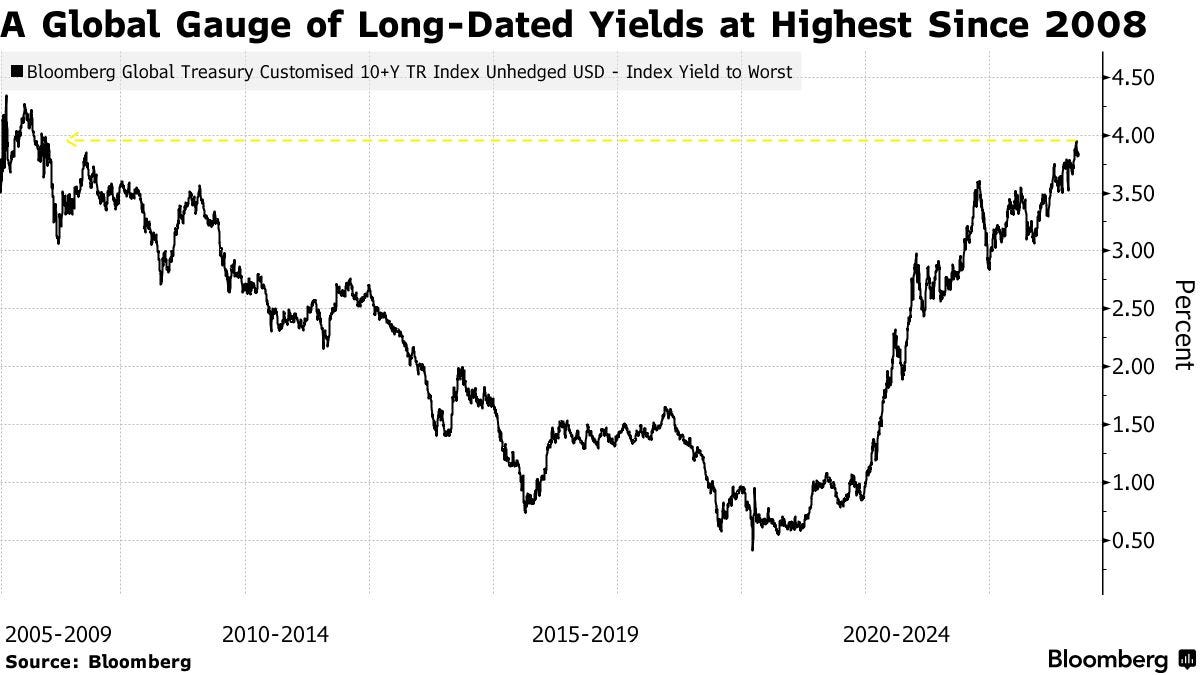

Updated on June 5, 2025 at 5:44 AM UTC Bloomberg: Global Bond Auctions Show Weaker Trend as Fiscal Pressures Grow

… With the US’s ‘Big Beautiful Bill’ expected to add trillions of dollars to the federal deficit over a decade, European defense spending on an upward trajectory thanks to the war in Ukraine and Japan pledging to relieve the impact of higher overseas tariffs, governments worldwide have ambitious plans that need funding. But that’s likely to come at a cost, especially if they want to borrow over an extended period — a Bloomberg global gauge of longer-dated sovereign yields has climbed to around the highest since 2008.

Investors largely took Thursday’s auction result in their stride, with Japan’s longer-dated bonds extending gains and Treasuries little changed, after Wednesday’s rally on softer-than-expected US jobs data. That kept alive hopes for Federal Reserve interest-rate cuts which could help shore up the bond market…

…“If long-term interest rates are going up because there is a genuine concern about fiscal sustainability, especially in the US, either bond vigilantes come back, or you have a Liz Truss moment resulting in a lot of panic,” said Luca Paolini, chief strategist at Pictet Asset Management.

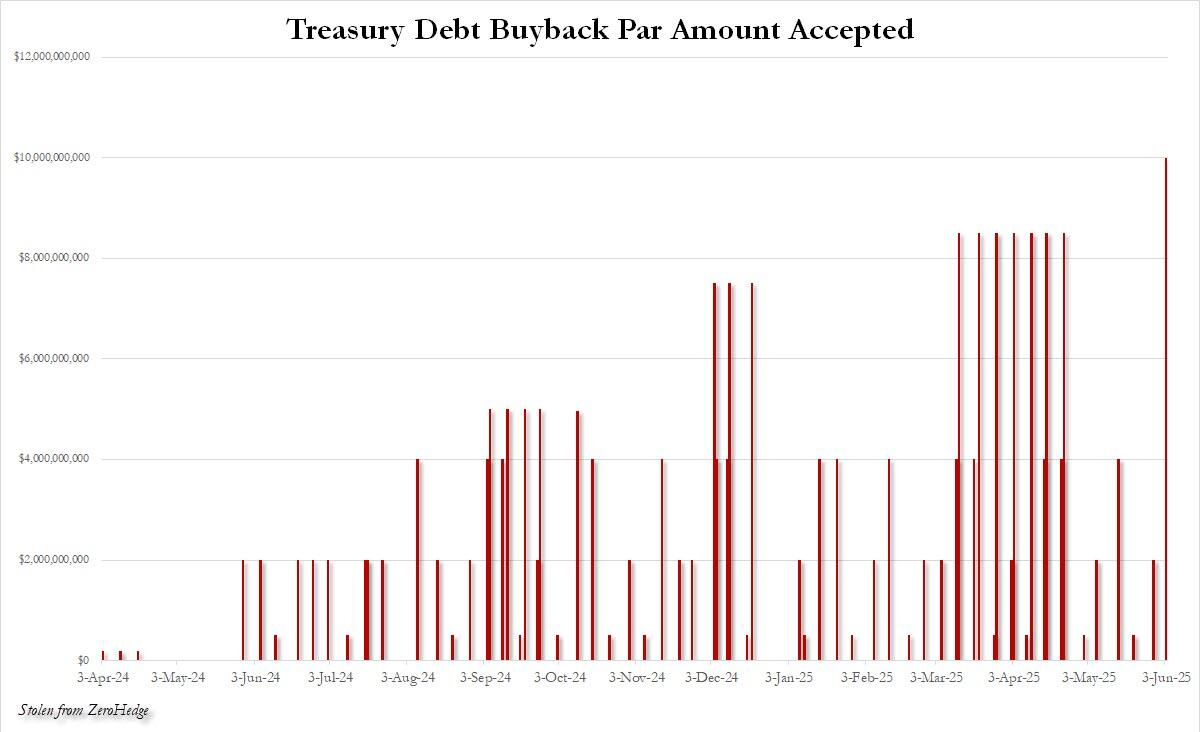

Finally, missed other day but thankfully was pointed out by a faithful and kind reader (thank you, Steve) AND helping complete the circle FROM ‘funding SECURED’ and a ‘mystery buyer’ to the USTs now BID …

ZH: It's Treasury Vs The Fed: With Fed Sidelined, Bessent Unleashes Record $10 Billion Bond Buyback

And while the maturity range of the cusips accepted for buyback was of low duration, in the interval between July 15, 2025 and May 31, 2027, we are about to see sizable increases in the total buyback size of longer duration treasuries.

{kind=link}