ZH: Stocks Flat As Mystery Buyer Emerges For Bonds After "Budget-Busting Bill" Passes, Bitcoin Tags $112,000

… STABILITY … I’m quite certain Team Rate Cut not yet heading back to the drawing board … an excerpt from a large German shop (more below) …

…One factor helping US assets to stabilise was some stronger US economic data, which continued to point away from a recession. For instance, the flash composite PMI for May was up to 52.1, up from 50.6 in April, and above the 50-mark that separates expansion from contraction. Moreover, the weekly initial jobless claims also remained in their recent range, coming in at 227k over the week ending May 17 (vs. 230k expected). So again, that showed no sign of a deterioration in the labour market, with the numbers still within their pre-Liberation Day range… -DB Early Morning Reid (23 May 2025)

… STABILITY in both stocks AND bonds was / IS even more impressive given S&P Global biz PMIs …

ZH: "Business Confidence Has Improved" - US PMIs Surged In May As New Orders Jump

… reminds me that, as Stephen Wright who used to say, ‘Can’t have everything. Where would you put it?’

Narratives continue to shape shift (more from Piper analyst, Michael Kantro, below) and markets never lie SO … a quick check in with the (somewhat)longer-end of the curve …

10yy MONTHLY (w/daily inset): watching close vs 4.50% (TLINE, psychological) …

… daily momentum has been / remains overSOLD and there are some indications of a rolling over BUT I’d prefer to ‘trust but verify’ and have some sort of weekly confirmation …

… I’ll angle to have a look at WEEKLY chart(s) over weekend, weather and time ‘permitting’ … the visual, though, helps offer some context as to where we’ve been and as far as where we may be going … well, one is a known and the other an unknown BUT I can / will say ahead of NEXT weeks index extension, with duration ‘on sale’ and lots of ‘5s’ on offer. the ‘mystery buyer emerged’ may actually not be all that mysterious?

I’ll quit while I’m behind … here is a snapshot OF USTs as of 701a:

… HEREis what this shop says be behind the price action overnight…

… while YOU slept: Treasuries experienced one of the quieter sessions for USTs in Asia this week as the market prepares for a Memorial Day holiday weekend and month-end extension week following. UST futures saw a brief dip alongside JGBs on the Tokyo open, before a quick recovery post-Japan CPI release (modestly higher than expected). During the LND morning session, duration bottomed out, with some steepening pressure alongside a rise in crude oil and weaker USD. Our desk saw scattered selling from real$ in 10s and 20s, countered by micro flattening interest in the front end. S&P futures are flat here at 7am, Crude +0.3%, Gold +1.1%, DXY -0.6%, and 2s10s curve +0.75bps.

…TLT ETF - approaching a significant multi-decade support at 82.42 (the 2024 & 2006-2007 lows).

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: USD continues to slip while Bonds edge higher awaiting Fed speak; Trump is pushing the EU to cut tariffs or face extra duties … USTs are on a firmer footing, venturing as high as 110.03+ with the next target coming via Wednesday's peak at 110.10+. After a soft start to the week on account of the Moody's downgrade and concerns over the deficit impact of Trump's Tax/Spending Reconciliation bill, US paper is attempting to recover off the lows. Fresh US newsflow is relatively light after yesterday's passage of Trump's bill, which will now move to various Senate committees before being debated and voted on by the Senate floor. Today's Fed docket includes remarks from Goolsbee, Musalem, Schmid and Cook.

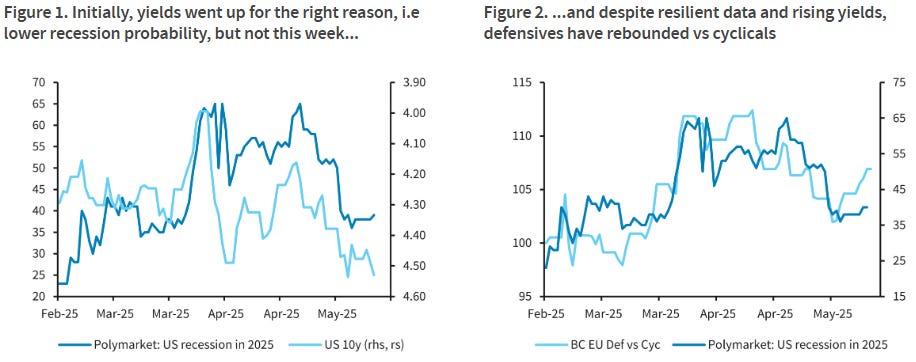

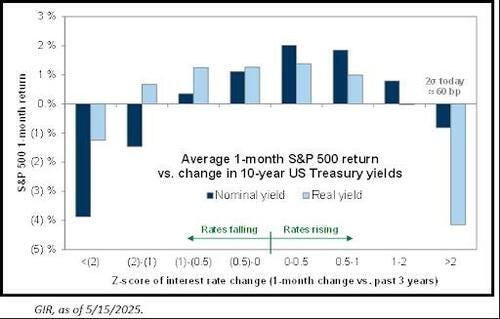

The positive correlation between yields and equities broke this week amid growing debt sustainability concerns. As bond vigilantes may keep equity markets on edge, Eurozone (Germany) looks relatively well positioned. Lower growth and higher rates should benefit quality balance sheet stocks.

Rates have touched the pain threshold for equities. The rates-equity correlation flipped to negative this week, as the market narrative shifted from tariffs de-escalation relief to debt sustainability concerns. While Moody's US rating downgrade is unlikely to have come as a shocker to most investors, the timing was not ideal amid tense tax bill negotiations in Washington, just when the equity market had recovered most of its post-Liberation day losses. As we warned a week ago (see Equity Market Review From tariffs to deficits, 16 May), the closely watched US 10-year yield moved into the danger zone for equities, which most pundits see to be above 4.5%, and the 30-year yield went above the 5% threshold as well. This time, yields are no longer moving up for the right reason, but largely because of rising term premia, which is not something equities are happy about. Indeed, despite the latest economic data staying broadly resilient (IFO, PMI, claims) and rates rising further, the equity market leadership turned defensive again after several weeks of Cyclicals' rally - i.e. bonds were for sale but bond proxy stocks & sectors were bid.

…Fixed income funds ($25bn) see most inflows since Oct'21. US treasuries see most inflows since liberation day, along with strong inflows in US IG and HY. In Europe, bonds saw outflows this week, after eight weeks of inflows. European IG received most inflows since Feb'25, as HY saw most inflows since Oct'24. MM funds are seeing alternating flows for the last six weeks, with inflows of $16bn this week

With long bond yields above 5%, we revisit equity reactivity at varying levels of inflation and UST yields. Our work suggests that yields rising further from here are likely to be a material headwind for equities, particularly alongside slower growth & higher tariffs.

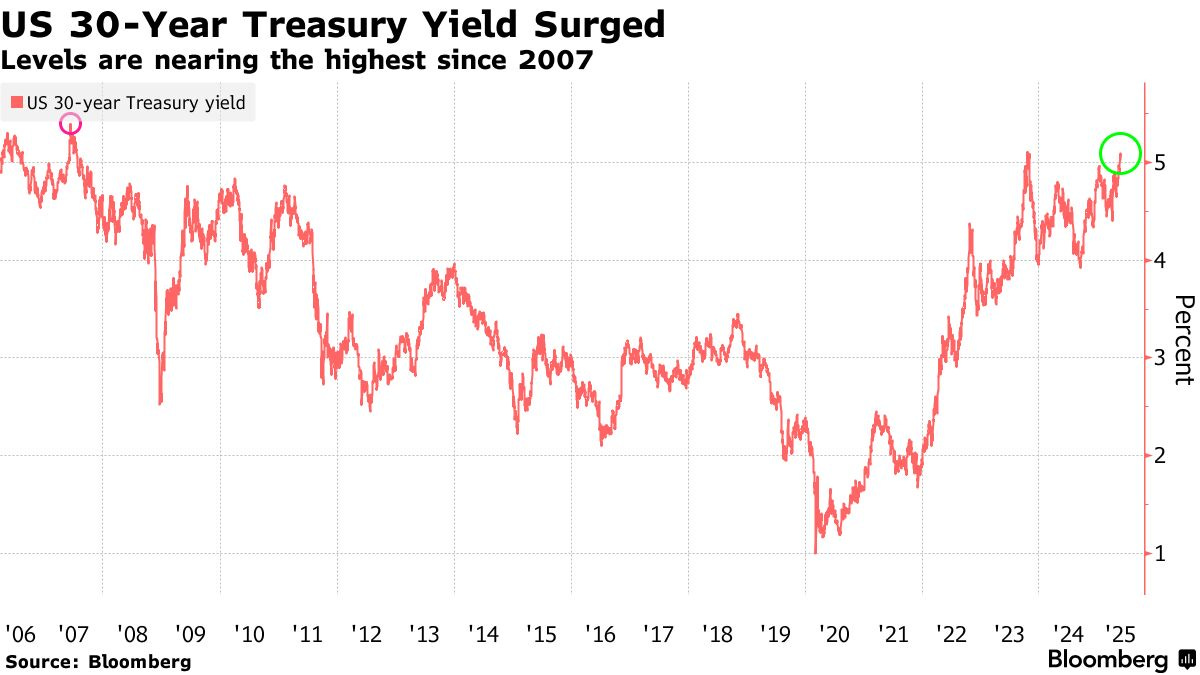

…The bond bears pushed long bond yields well above 5.0% on deficit and supply concerns in a move that saw 5s/30s above 100 bp for the first time since 2021. It was an impressive move that we’re still reluctant to fade in any meaningful way. We came into this week wary of a disproportionate response to non-data developments and that’s precisely what has unfolded as it pertains to the US budget process. We’re not arguing that the developments were bond-bearish, rather that the severity of the move reflects a broad-based apprehension regarding duration both domestically and overseas. The combination of inflationary pressures associated with the new tariff regime as well as the prospects for a foreign buyers’ strike due to the trade war all point toward higher yields. The uncertainty is how much higher yields will need to be to appropriately reflect the new global trade reality and inevitable reflation that is expected to become evident over the summer months.

A quick glance at the last 20 years reveals that long-bond yields have only been above 5.0% on three other occasions. First was mid-2006 (peak was 5.341%), followed by mid-2007(as high as 5.437%) – and we all recall the financial crisis that quickly unfolded. This isn’t to imply that higher yields triggered the mortgage crisis, although tighter financial conditions surely didn’t help. The most recent occurrence was in October 2023, when investors were similarly concerned about larger auction sizes requiring larger yield compensation to move further out the curve. One key difference between the current selloff and 2023 is that auction sizes aren’t expected to increase this year, although most market participants have February 2026 penciled in for the timing of larger 10s, 20s, and 30s. While it’s unclear whether Bessent will be able to avoid growing auction sizes that long, pricing in the prospects this far in advance implies that investors are leaning more heavily into the potential for a near-term pause in overseas demand for US Treasuries.

Suffice it to say, there will come a point at which dip-buying intensifies, although we struggle to envision a complete reversal of the recent bearish repricing. Nonetheless, once the selling pressure subsides, we anticipate that 30- year yields will drift back below 5.0% – albeit not back to the sub-4.50% levels seen in early-April in the absence of a meaningful fundamental trigger. The combination of ongoing solid economic data and Trump’s tariff pauses has pushed back against concerns that the US is currently slipping into a recession. Today’s jobless claims print only further contributed to the perceived resilience of the labor market…

… thinkin’ about ‘5.00%’ readily available for next weeks index extension certainly does / should make one pause and consider … Moving along and now that rates move has shocked the world and bonds are (again) topical …

22 May 2025 BNP US equity derivatives: Hedging higher rates

Hedging higher rates: Wednesday’s weak UST 20y auction sparked the first >1% SPX down day in the past month, adding to market concern over US debt sustainability with the 30y yield rising +12bp to one-year highs. In recent history, defensive sectors are typically most negatively correlated to higher long-end yields. However, in an environment in which higher rates are combined with slowing nominal growth, regional banks and small-/mid-caps look particularly vulnerable. With the March 2023 SVB turmoil still fresh in mind, further long-end volatility could drive investors to sell lower-quality, cyclical parts of the market first and ask questions later.

As a tactical downside expression, we would consider July KRE and IWM hedges, additionally capturing macro data that will first start to contain residual tariff impacts. Both KRE and IWM implieds screen as attractive to own versus SPY. The ratio of KRE/SPY 2m 25dp IV is at the 8 th% post-SVB. RTY vols on average across the surface at -0.7 z-score vs SPX over the last 2y. Wednesday’s spot underperformance led to skew steepening back towards two-year highs across both sectors (2m normalized skew the 94 th% & 92 nd% over 2y for IWM and KRE respectively). This lines up put spreads as an attractive expression to hedge a retracement back to April spot lows…

They say BONDS have more fun. These days, they (bonds) are getting more attention and so, a couple notes from German shop …

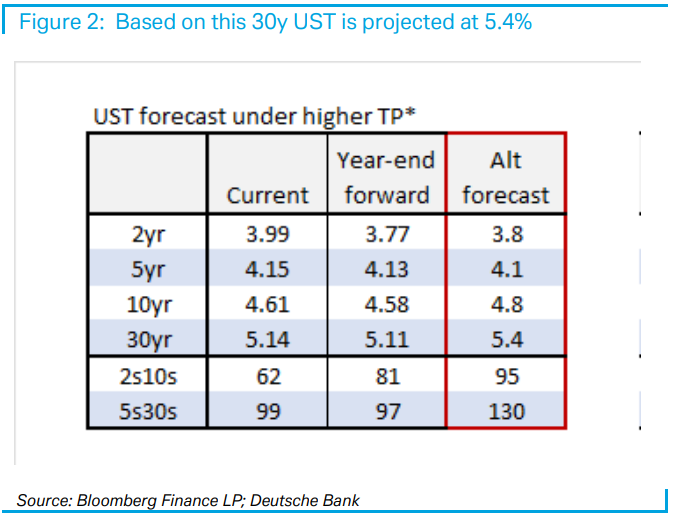

Our current forecast for the 30y Treasury (UST) yield – published a month ago – is 5%. It was bearish at the time. But with the long-end now above 5% amid focus on the US fiscal outlook, we discuss two alternative benchmarks.

The first is based on our rates forecasting approach. With the same Fed path as in our baseline but higher yet plausible assumptions for term premia, the projected 30y yield is 5.4%.

The second approach comes from a macro model of 5s30s UST as a function of economic conditions and global bond supply. This approach points to 30y UST below 5%, but also suggests only a modest increase in global deficits and free float over our projection from late last year would justify current 30y levels. Since that projection, global fiscal policy is on a significantly easier course.

Our takeaway from these alternatives is that meaningful deviation from long-run historical dynamics isn't needed to justify a 30y UST range of 5-5.5%. This is especially true given weaker foreign demand for USTs ahead…

After a heavy selloff on Wednesday, markets began to stabilise again over the last 24 hours, despite investors’ ongoing fears about the fiscal situation. In particular, long-end Treasury yields started to fall again, with the 30yr yield (-4.3bps) moving down to 5.05%, whilst the dollar index (+0.37%) also recovered. But even so, there were still several signs of concern, as the 30yr Treasury yield had moved as high as 5.15% on an intraday basis, and a similar pattern was being echoed globally. For example, Japan’s 30yr yield (+3.3bps) moved up to 3.18% yesterday, the highest since that maturity was first issued in 1999. And in the UK, the 30yr yield (+3.2bps) moved up to 5.55%, closing just shy of its highest level since 1998.

Those moves came as the US House of Representatives narrowly passed the tax bill yesterday, with an incredibly tight 215-214 margin in favour. As a reminder, that would extend the Trump tax cuts from his first term, which are currently due to expire at the end of this year, and it also includes a $4tn increase in the debt ceiling. However, there’s still some way to go before passage, as it also has to pass the Senate, which is expected to make changes to the bill. For instance, fiscal hawks in the Senate are unhappy about some of the measures, with Senator Rand Paul having said “I’m not voting to raise the debt ceiling $4 trillion to $5 trillion”, whilst Senator Ron Johnson has described the deficits from the House bill as “completely unacceptable”…

… One factor helping US assets to stabilise was some stronger US economic data, which continued to point away from a recession. For instance, the flash composite PMI for May was up to 52.1, up from 50.6 in April, and above the 50-mark that separates expansion from contraction. Moreover, the weekly initial jobless claims also remained in their recent range, coming in at 227k over the week ending May 17 (vs. 230k expected). So again, that showed no sign of a deterioration in the labour market, with the numbers still within their pre-Liberation Day range.

The rally also got a fresh boost from the decline in bond yields, with the 2yr Treasury yield (-2.8bps) falling back to 3.99%, whilst the 10yr yield (-7.0bps) fell back to 4.53%. In part, that followed comments from F ed Governor Waller, who suggested that if the tariffs were closer to 10% and that was done by July, then the Fed would be well placed “to kind of move with rate cuts through the second half of the year”.

In other Fed-related news, yesterday evening the US Supreme Court said that the Federal Reserve was an exception when it comes to the President’s ability to remove officials, referring to the Fed as a "uniquely structured, quasi-private entity" that was different to other independent agencies. So that offered a bit more certainty on the position of senior Fed officials, and whether Chair Powell might be removed before his term as Fed Chair ends in May 2026.

Sentiment turnin’ (back) down … MARKET sentiment and, ‘bout that Fed sentiment …

May 22, 2025 MS: Cross-Asset Brief: MSI Turns Negative

Our Market Sentiment Indicator (MSI) has turned negative, exiting the positive reading it has held since April 10, 2025. This regime has been associated with below-average one-week forward returns for global equities.

Key takeaways

The MSI signal has turned negative/risk-off, a regime that's usually associated with below-average one-week forward returns for global stocks.

A stretched level of MSI and negative changes in 6/10 metrics have caused a reversal in sentiment to the downside, triggering the negative signal.

While the MSI signals a tactical risk-off, over the next 12M we are OW US equities. For more, see Global Strategy Mid-Year Outlook: All Eyes on US.

What could change the signal? The MSI level can stay stretched for some time, but improvements in sentiment data may cause the signal to shift to neutral.

We post daily updates to Bloomberg – MSI level (MSXAMSIL Index) and signal (MSXAMSIS Index). For weekly summaries, see our Cross-Asset Spotlight.

May 23, 2025 MS: US Economics Weekly: Fed speak: Later and right is better than early and wrong Michael T Gapen

A number of Fed speakers took to the airwaves this week. The message is tariffs are likely to create risks on both sides of the Fed's mandate. The right response is to wait. Cuts later this year are possible, but it would take clear evidence of transitory inflation.

Key takeaways

The Fed is still waiting for policy changes to have an effect on the real economy. The net effects of policy changes remain highly uncertain.

The Fed still retains an easing bias, but is unwilling to "look through" tariff-induced inflation to ease preemptively. Proof is in the eating of the pudding.

Atlanta Fed President Raphael Bostic said the Fed may have to "wait three to six months to see how the uncertainty settles." We forecast no rate cuts in 2025.

Covered wagon folks on housing and affordability …

May 22, 2025 Wells Fargo: Existing Home Sales Dip in April Housing Market Headwinds Prevail

Summary Some Positive Developments for Buyers, But Affordability Conditions Remain Unfavorable Existing home sales slipped 0.5% in April, marking the third decline in the last four months. This downward streak is emblematic of the affordability issues plaguing the housing market. Although mortgage rates dipped slightly in the months preceding April sales, they remained elevated above 6.5%, presenting a challenge for homebuyers. Rates have since moved even higher, surpassing 7.0% according to Mortgage News Daily. Ongoing price appreciation is an added challenge. However, April’s 1.7% annual increase in single-family resale prices marked the slowest pace of price appreciation since July 2023. All told, softer price appreciation and growing resale inventories are positive developments. However, inventories remain scarce compared to pre-pandemic levels, and unfavorable affordability conditions will likely prevent a meaningful resale recovery in the near-term.

Finally, Dr. Bond Vigilante on the bond elephantS market in the room …

The elephant is as good a metaphor as there is for the US government bond market. Its scale, power, memory, emotional intelligence, and tendency to live in complex family groups—just like the broad array of debt instruments—are right on the nose . . . er, trunk.

Yet this week, we saw that the room in which the bond market operates has more than one elephant. The other large mammal in question is the Republican Party, which may be picking a fight with the bond market. Just days after Moody's revoked Washington's AAA rating, the GOP in the House passed Donald Trump's "big, beautiful bill" today. The fact that it will add trillions of dollars to the primary federal deficit has agitated bond investors.

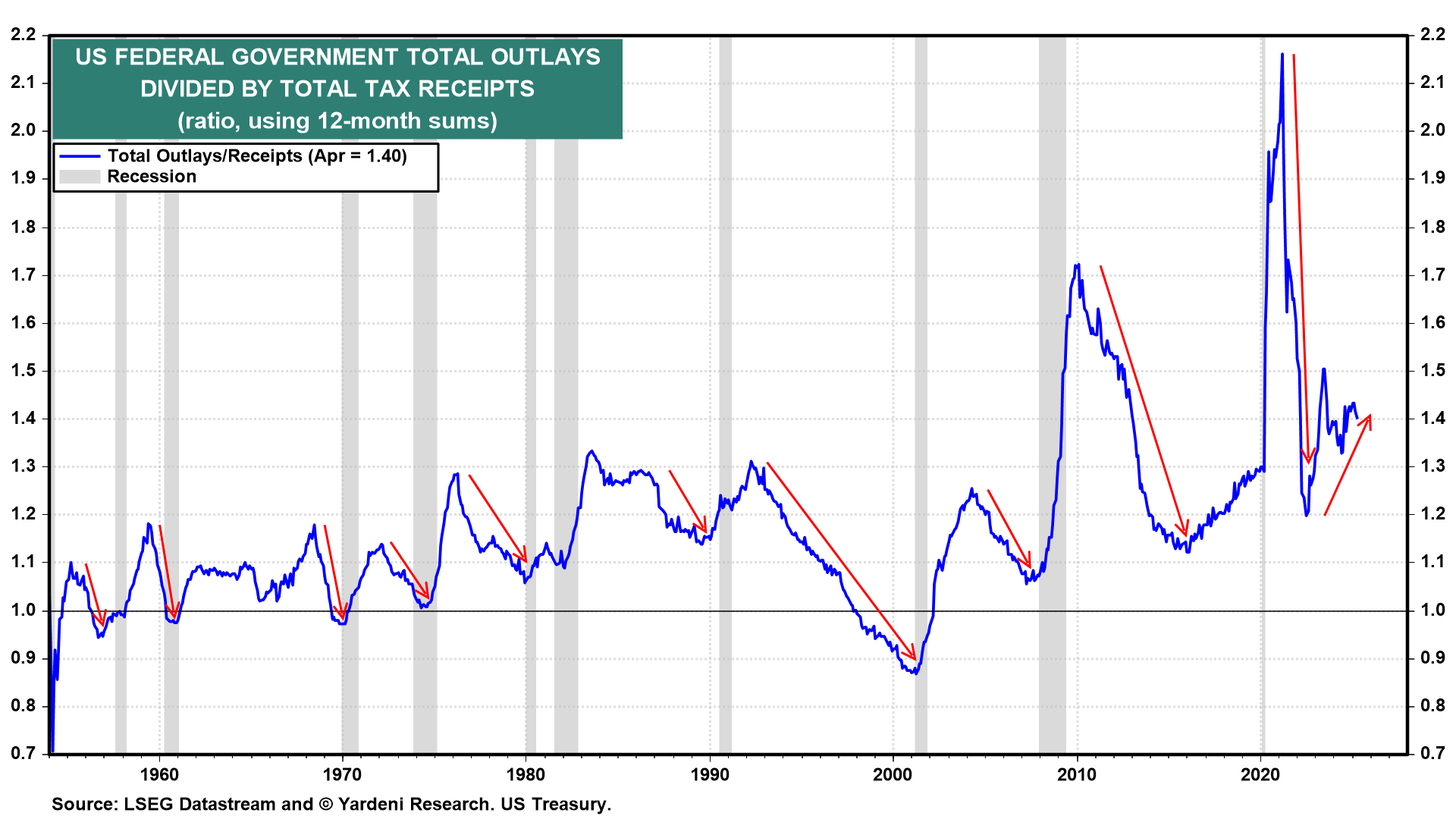

Suffice to say, Treasury Secretary Scott Bessent really has his work cut out as his boss, President Donald Trump, pushes his deficit-bloating bill through the Senate. If Bessent isn't careful, his 3% target for the ratio of the deficit to GDP—less than half what it was in the fourth quarter—will get trampled (chart).

To regain credibility on Washington's fiscal trajectory, Bessent must stop outlays from stampeding faster than tax receipts while the economy is expanding (chart). Obviously, that feat would become even harder in the case of a recession.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

AllStars on TLTs … a buyable bottom?? Different this time …

at JC_ParetsX

Bonds rally every time TLT has been down here. Are you betting that this time is different?

TLT has $50+ billion in assets and is a good proxy for short-term thinking and trading in the bond market.

Yesterday, when the poor 20-year auction tanked the bond market, TLT saw huge inflows of $870 million.

As the labels show, this was the fourth-largest inflow day since last summer. The three larger inflow days were not particularly good buying opportunities.

As the old market saying goes, never try to catch a falling knife. It appears that bond investors, yet again, tried to catch the falling knife.

Good luck to these traders.

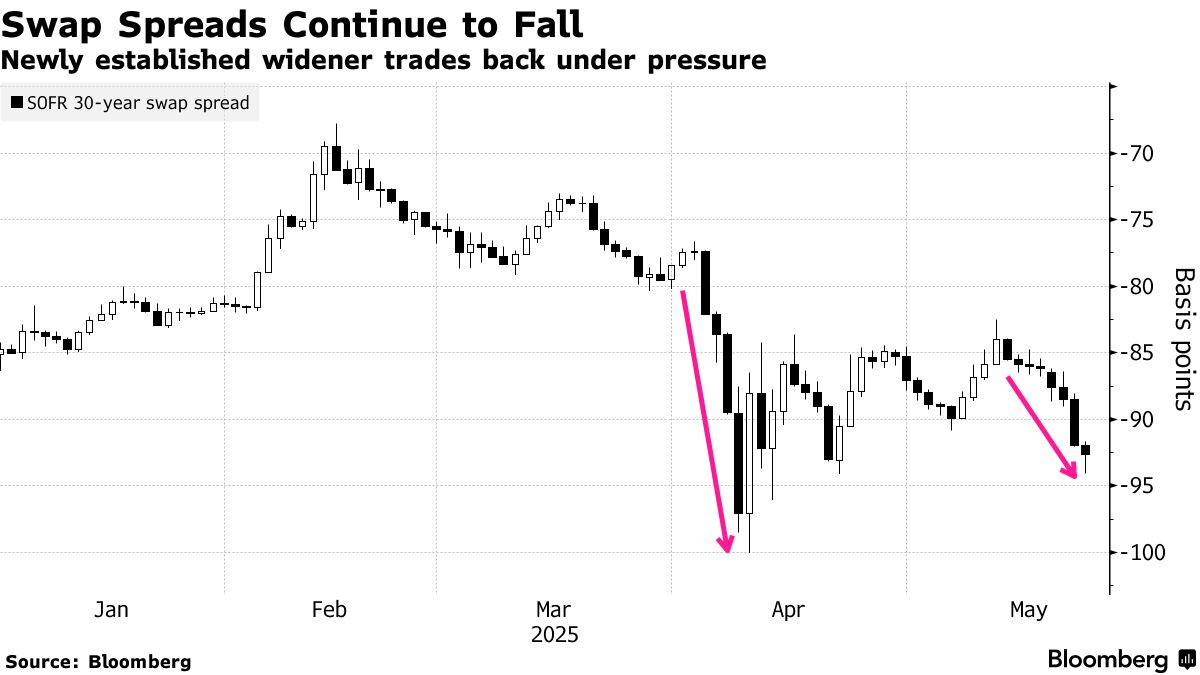

Bonds all the rage and not just ‘goat for weaker stocks but also worth noting swap spreads and HFs …

May 22, 2025 at 4:22 PM UTC Bloomberg: Bond Investors Threaten Popular Hedge-Fund Bet on Swap Spreads By Edward Bolingbroke

A surge in long-term bond yields is once again threatening to upend a crowded hedge-fund bet that Treasuries will perform better than interest-rate swaps.

The trade is at risk of falling apart as borrowing costs for the world’s biggest economies soar, diminishing the returns in US government debt against the swaps. That’s a problem for hedge funds and other traders who piled into the bet in recent weeks, as well as the chorus of Wall Street strategists who’ve been recommending it.

Trouble for the trade has come as concern mounts about the ability of governments — including in the US — to cover massive budget deficits, pushing long-term yields higher. That angst is overshadowing a key driver of the swap-spread bet, which hinges on a potential move by the Trump administration toward adjusting the supplementary leverage ratio, or SLR, to allow banks to hold more Treasury bonds.

Speculation on Wall Street surrounding possible SLR tweaks had, in recent weeks, renewed interest in the wager. Deutsche Bank strategists Steven Zeng and Matthew Raskin wrote in a note earlier in May that they expected more clarity on SLR reform as soon as June, with implementation possible before the end of the year. So far, official details on possible changes remain slim.

Still, strategists from Barclays, Goldman Sachs and Societe Generale, among others, had all recommended the trade recently.

That made Thursday’s market move especially painful for believers in the bet. Thirty-year US yields were above 5% and just shy of the highest since 2007, causing the spread against comparable-maturity SOFR swaps to shrink for an eighth day to as tight as negative 94 basis points…

… also on The Terminal, a few words from BAML on BONDS (short version: buy ‘em)

May 23, 2025 at 9:45 AM UTC Bloomberg: BofA’s Hartnett Says Buy the Dip in Treasuries as Yields Top 5%

Investors should buy the selloff in long-dated Treasuries as the government is likely to heed warnings from bond vigilantes to bring its debt under control, according to Bank of America Corp.’s Michael Hartnett.

The 30-year Treasury note is at a “great entry point” with the yield above 5%, the strategist wrote. Bond investors are “incentivized to punish the unambiguously unsustainable path of debt and deficit,” he added.

US bond yields have surged this week as President Donald Trump’s tax cut plan has ignited concerns that it would add trillions of dollars in coming years to already bulging budget deficits, at a time when investor appetite is waning for US assets across the globe. Sentiment toward Treasuries has also taken a hit since Moody’s Ratings stripped the US of its top credit grade late last week.

The 30-year yield rose to as high as 5.15% on Thursday, just shy of a two-decade high. Long-dated bonds in Japan, Germany, Australia and the UK have also been under pressure, while US equities and the dollar have retreated.

Hartnett has recommended bonds over equities this year. The strategist said in the note dated Thursday that Treasuries are now reflecting the drivers of a bear market, with 10-year annualized returns from long-term government bonds falling to a record low of -1.3% in January.

We have been. I now count 8 narrative rotations in bond markets since late 2022. Recession… no landing … soft landing … no landing … recession … no landing … recession … etc. Flips every 4-5 months or so. Narrative volatility is here to stay in today’s Bifurcation Nation.

Finally, THE question many / most are

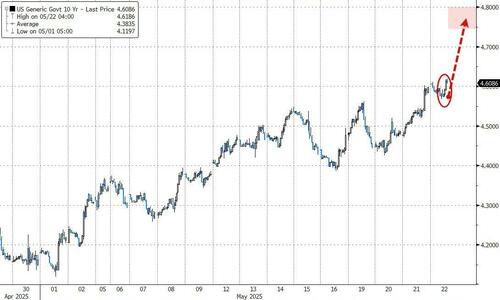

ZH: As 10Y Yields Surge, At What Rate Do Stocks Break?

…Chaos in the Japanese bond markets and hot UK inflation are not helping global yields, but the big question everyone wants to know is simple:

"when do equities care about bond yields"

The answer - according to Goldman Sachs - is NOW!

Historically, its speed that matters rather than the level.

Equities tend to care when yields rise ~2 std dev over 1 month.

This is roughly 60bps so around 4.75-4.80% on US10yr.

In other words, we are getting very close!!

… with bonds closing early today (2pm) ahead of the holiday long weekend, in the case you thought Monday was national BBQ Day … Thank you to all who served and your families for your sacrifice …

Thanks to MY dad, ret NAVY (Go NAVY, BEAT Army) and to any / all out there still awake, reading, feel free to shout out and tell me ‘bout your service !!

Hope to have something out over weekend, guessing there will be little from Global Wall given holidays (get what we get and we don’t get upset) … … THAT is all for now. Off to the day job…

{kind=link}

The "mystery" buyer made some great trades....

Was it the Fed ???