while WE slept: USTs aggressively UNCH; mkts overconfident in easing while markets/econ have been resilient (DB); geopol events short-lived, Fed's NLP more dovish and thinking 7 CUTS in '26 (MS) ...

Good morning … bonds, he said … they look alright, he said …

30yy: 5.00 - 4.90 - 4.80 … here’s why I’m watchin’ all these levels …

… and doing so as bonds romance the (bullish)TLINE as (bearish)stochastics continue to grind … the longer-term (ie WEEKLY) may look ok which means to me, one should be watching for dipORtunities and keeping open mind — into the weeks auctions, perhaps bonds represent that port in a storm … to be determined…

Well, markets are handling the news NOT like I’d have thought.

That said, it was a bit different picture last night when futures opened and so, lets jump right in. Last nights early reflex would suggest a nothin’ burger …

ZH: Futures Slide, Oil, Gold And Dollar Spike But No Panic Moves

…that was then and again, this is now.

Things simply aren’t yet implied to be that bad or get worse. As we’ve seen these movies before, throughout history, likely I best head to the rest of this short note and get OUT the way but first … here is a snapshot OF USTs as of 650a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: Crude pares initial gap higher & USD firmer after US strikes, focus on potential Iranian retaliation … USTs began the week with gains, gapping higher from Friday’s 110-31+ close by a handful of ticks and then extended slightly further to a 111-04 peak, a tick higher than Friday’s best. Upside a function of the benchmarks trading as a haven, given the significant geopolitical escalation of Trump striking Iranian nuclear sites; details on the feed/see Commodities. However, the upside proved limited as while Iran has spoken about extensive retaliation they are yet to do anything particularly significant. The nation continues to strike Israel with missiles, and while Iran’s parliament has approved closing the Strait of Hormuz, the security body is yet to order it. Furthermore, no reported action against US-specific assets, though Iran says all options are on the table. Geopols aside, the docket today is busy with several Fed speakers due and Flash PMIs for June; the latter expected to fall slightly from the prior.

… Shrieks and shrugs meet alarming US debt pile For all the trepidation about America's gaping fiscal deficit, mounting public debt, credit downgrades and the precipitous dollar decline, the Treasury market appears to be doing just fine.

No one doubts the scale of eye-watering public debt metrics, which will likely be entrenched whatever version of President Donald Trump's "big beautiful" budget bill emerges from Congress this summer. Still, the bond market seems to view it as manageable.

Both the real and nominal U.S. 10-year borrowing rate has done very little for almost two years now - even though risk premiums have crept higher. And while elevated compared to pre-pandemic troughs, bond market volatility is also roughly near long-term averages.

Graphics are produced by Reuters.

Even in the tumultuous first half of 2025, exchange traded funds tracking Treasuries are little changed, much like major Wall Street stock indexes.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ … SOME of which was written / sent before bunkers were busted …

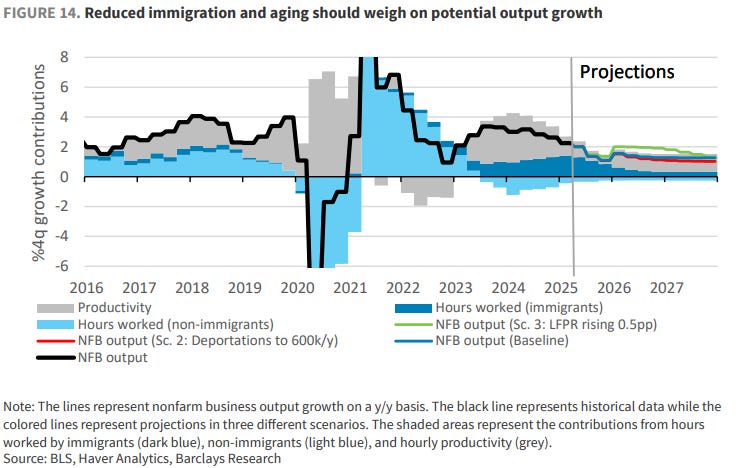

First up, something of a more macro read for the employment situation … Immigration and it’s growth impacts …

23 June 2025 Barclays: US Immigration Two mighty headwinds

From 2022 to 2024, immigration played a key role in boosting US employment and economic activity. With job market inflows now near zero and the non-immigrant labor force now declining, labor supply is set for significant deceleration, posing headwinds to potential real GDP growth.

The US economy recorded solid growth in economic activity, employment and consumption through the end of 2024, boosted by a mighty tailwind from immigration from 2022 to 2024. This is about to change.

We expect the labor force and economic activity to slow significantly because of two mighty headwinds: 1) tighter immigration policies, and 2) a shrinking non-immigrant labor force as the population ages and older workers retire.

In our baseline simulation, monthly gains of potential private nonfarm payroll employment among immigrants slow from about 150k in January to around 40k at the end of 2025 and thereafter. Furthermore, absent significant increases in labor force participation from non-immigrants, effects of population aging imply that the US non-immigrant labor force will decline by about 30k per month in 2025 and 2026, weighing further on labor supply. In all, potential private nonfarm payroll gains are projected to slow to an average of about 60k/m in 2025 and to less than 10k/m in 2026 and 2027.

The slower labor force growth implies that potential real GDP growth diminishes to 1.4-1.6% y/y, with almost no contribution from aggregate hours worked in 2026 and beyond. At that point, growth is projected to be driven almost entirely by productivity gains, which are highly uncertain.

We consider two alternative scenarios. In the first, increased immigrant departures slow the pace of potential payroll employment gains and real GDP growth further. In the second, an increase in labor force participation delays, but does not eliminate, the slowdown in payroll employment.

…Finally, in the third scenario (green line), in which the LFPR rises 0.5pp through end-2026, NFB output growth ends the year at 1.7% Q4/Q4, rises to a strong 2.3% in 2026, then trends back down to 1.7% in 2027 as retiring US workers exert again drag on hours worked. This translates to potential real GDP growth rates of 1.5% Q4/Q4 in 2025, 2.1% Q4/Q4 in 2026, and 1.6% Q4/Q4 in 2027. This scenario illustrates the importance of the LFPR in affecting hours worked and potential output growth.

Taking all three scenarios together, NFB output growth ends 2027 in a fairly narrow range of 1.4-1.7%, corresponding to a potential growth rate for real GDP of 1.4-1.6%, with almost no contribution from aggregate hours worked. At that point, growth is projected to be driven almost entirely by productivity gains. While many observers are optimistic that AI will help boost productivity in coming years, so that they would provide an offset to the two headwinds considered here, there is considerable uncertainty about the timing and extent of its effects.

Last week’s Fed meeting suggested the policy hold, already six months old, could continue through “the summer,” meaning the first live meeting might be October.

We think the market is too complacent about the risk of escalation in the Iran-Israel conflict. While sharply higher oil prices which would assume significant disruptions in flows through the Strait of Hormuz is not our base case, every escalation increases the probability of this tail risk materializing.

The upcoming NATO summit will likely shift the market’s focus back to fiscal policy, reinforcing our bullish stance on Europe.

… We tend to think the view articulated by Powell at the press conference lines up with our assessment and with an ultimate outcome of no rate cuts this year: that monetary policy is not very restrictive now, that the labor market will prove resilient, and that risks to inflationary entrenchment are serious and could worsen with inopportune rate cuts. We also think the dovish faction’s view, reflected in the median “dot” forecast, does not entirely withstand analytical scrutiny and will evolve over time …

… Absent a compelling, evidence-based argument to move urgently, we think the FOMC will remain on hold through the summer as Powell indicated, and from there the data will be the committee’s guide. If inflation remains soft or the labor market weakens over the course of the summer, it becomes easier to envision rate cuts later this year, whereas if inflation rises sharply (due to tariffs or energy prices) and the labor market holds up, that will likely push rate cuts into 2026, as we expect …

Next, a couple of notes from a rather large German institution and couple of it’s fan fav stratEgerists with some CONTEXT of all the h’lines and hysteria of this moment in financial markets history …

… In terms of the economic impact, the US has turned into a net energy exporter in the last few years so any negative impact would be through deteriorating financial conditions or through higher for longer rates as the Fed have another reason to delay cuts. For Europe though, the impact is potentially more serious. Every $10/bbl increase in oil has the potential to add a quarter of a percent to HICP within a quarter and if sustained 0.4pp within a year. Growth could be lowered by around 0.25pp if such an increase was sustained. See our European economists' chart of the week here from Friday looking at which countries would be most exposed …

… and in terms of where ‘dipORtunities’ may / may not exist …

23 June 2025 DB: Mapping Markets: What are the biggest market dislocations? June 2025

… This month, a lot of our thinking stems around inflation risk, which investors seem to be underestimating. It’s true that recent US CPI prints have been underwhelming. But given the latest escalation in the Middle East and Iran’s promise to retaliate, the market reaction has been remarkably restrained.

Moreover, that inflation risk isn’t just coming from geopolitical events and higher oil prices. We still have the threat of fresh US tariffs, with the 90-day reciprocal tariff extension running out on July 9. There’s significant fiscal stimulus coming in Europe, particularly for higher defence spending. And with the major central banks having cut rates in recent months (which will hit with a lag), there’s still plenty of price pressures in the pipeline…

…1. Despite an array of inflation risks in Europe and now a fresh geopolitical escalation, the reaction of Euro inflation swaps has been incredibly muted relative to other shocks.

…2. In the US, futures markets have consistently over-priced how dovish the Fed would be in 2022, 2023, 2024, and 2025 so far. So given the FOMC’s latest forecasts, the US economy’s broader resilience, and the repeated dovish bias of markets, the confidence in two further cuts this year is striking…

…3. Gold prices have been remarkably restrained given events in the Middle East over recent days and ongoing inflation risks. They’ve followed a very different pattern to oil, which has been much more reactive to geopolitical risk…

…4. In Japan, core CPI was above expectations last week, the Bank of Japan remain in a tightening cycle, and multiple global inflation risks are swirling. Yet the country’s 5yr government bond yield is still beneath 1%…

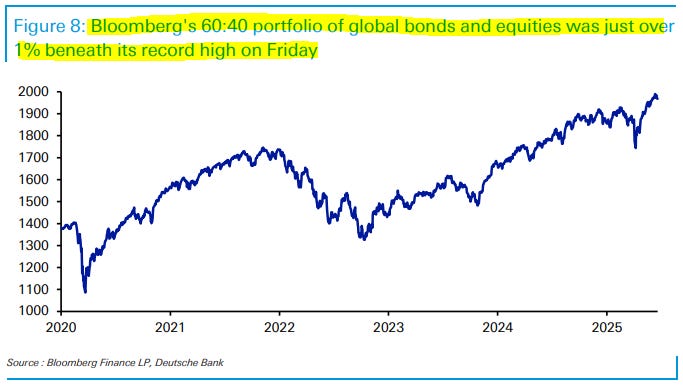

…5. This year has seen a succession of shocks for markets, including higher tariffs, the escalation in the Middle East, and growing fears about fiscal policy. Yet on a multi-asset basis, financial markets have proved strikingly resilient. Could that stability breed complacency?

…Yet amidst all that, the performance of several assets has been very resilient as we nearly hit the halfway mark for 2025. Indeed, on Friday before the US strikes, Bloomberg’s global 60:40 portfolio was just -1.1% beneath its alltime high…

Global Wall all asking / answering the same questions today …

23 June 2025 ING: US strikes on three nuclear facilities in Iran: What it means for macro and markets

While the broader impact of the US strikes on Iran’s nuclear facilities remains uncertain, markets have so far responded with caution. What is clear, however, is that the strikes are likely to heighten economic uncertainty and put upward pressure on oil prices …

…No safe-haven effect, yet What has been remarkable so far has been the lack of flight-to-safety in bonds. Right from the initial strikes through to 12-13 June, the market reaction showed minimal movement into traditional safe havens - neither Treasuries, Bunds, nor rates markets more broadly saw significant inflows. Bond markets quickly moved on. Should things turn dramatically more sinister in the coming days, there must be a route for this to flip, and for cash to fly out of risky assets and into core bonds.

If yields were to lurch lower in the near term, it could reflect a growing market discount for significant risks to the broader global macroeconomic outlook.We have two sizeable wars ongoing, with minimal expectation for containment. That, plus the negatives coming from the tariff tax wedge in the US, has a feedback loop that absolutely can result in a flight out of risky assets and into bonds.

That said, and given what we know, market rates will likely be primed to discount two things. First, a “positive” outcome, in the sense that a so-called bad actor has had its nuclear bomb-making capability severely downsized. Second, even on such an outcome, the rates market will fret about any inflation sting in the tail through upward pressure on energy prices amid wider regional angst. Given that, the dominant reaction should be some curve steepening pressure, likely from the long end. Professional investors can read more here.

A domestic shop economist offered some words on Earl yesterday morning …

June 22, 2025 MS: Sunday Start | What's Next in Global Macro: War and Oil

… Around the world, our economics teams have estimated the pass-through of oil prices. For the US, the story for inflation is quite modest. History suggests that a 10% permanent increase in oil prices moves core inflation by only a couple of basis points, an amount that easily gets lost in the noise. Moreover, the US is the largest oil producer in the world and flirts with being a net exporter of oil. Even if the national income implications are close to a wash, the distributional effects imply softer consumer spending and thus growth. Higher oil prices feel inflationary, but they could ultimately mean downside risk for the Fed …

… For now, we wait to see how long-lived the oil price movement is, and clearly broader questions arise. Could a continuation or escalation weigh further on global sentiment, dampening capex and consumer spending? Does the overall calculus change and in what ways if the news reports about possible US direct involvement come true? As I started with, uncertainty has been a hallmark of this year, and that theme is set to continue.

… Same shop with an equity mkt preview …

June 23, 2025 04:01 AM GMT MS: Weekly Warm-up: Balancing an Improving Earnings Backdrop with Geopolitical Risks

We're still focused on EPS momentum and positive operating leverage as tailwinds for stocks. History suggests most geopolitically-led sell-offs are short-lived/modest. Oil prices will determine whether volatility persists. Our OW in Energy and UW in Consumer Goods offer hedges for higher oil prices.

Positive Operating Leverage Should Support Earnings Growth...

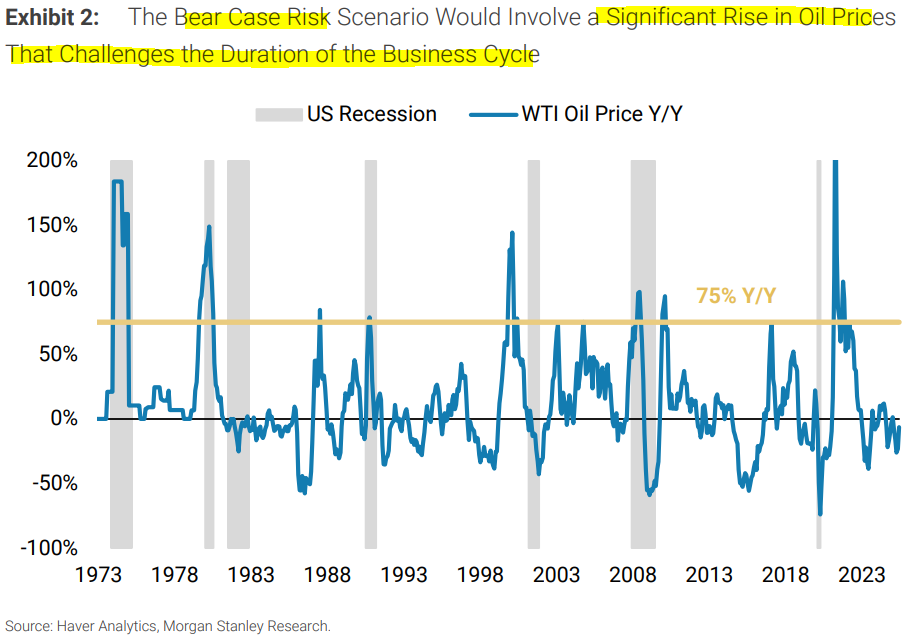

Geopolitical Uncertainty...Prior geopolitical risk events have led to some volatility for equities in the very short term (i.e., next few days), but 1/3/12 months post these events, the S&P 500 has been up 2%/3%/9%, on average. The bear case scenario for equities tied to the recent events in the Middle East would be that oil prices rise significantly, thereby posing a threat to the business cycle. History suggests that such a rise in oil would need to be (1) in the range of +75% on a year-over-year basis ($120+/bbl) and (2) in a late cycle context in order to materially raise the probability of this outcome. Through last week, the year-over-year rate of change on crude was negative. Thus, while we're respectful of the risks, there's a long way to go on this basis. Our Commodities Strategist Martijn Rats thinks it would take sustained supply disruption in the Strait of Hormuz in order to drive oil prices significantly higher (i.e., closer to +75% year-over-year). Our overweight stance on Energy and our underweight stance on Consumer Goods (sensitive to potentially higher fuel costs) offer hedges against moderately higher oil prices.

The Fed May Be in "Wait and See" Mode, but the Equity Market Is Thinking Ahead...Last week's FOMC meeting was largely as expected. The SEP showed projections for lower growth and higher inflation this year, the median number of expected cuts for 2025 remained at two, and Chair Powell appeared to take a "wait and see" approach to adjusting the policy rate. Looking ahead, our economists see 7 cuts from the Fed next year, a more dovish stance than the bond market is pricing. We also think it's interesting that Bloomberg's Fed Sentiment Natural Language Processing Model is getting more dovish in rate of change terms. That dynamic seemed to be echoed by Fed Governor Waller on Friday when he said that the Fed could cut as early as this July. Our view has been that the lagging hard data is likely to slow this summer, but that this type of moderate slowdown in growth has already been priced in the equity market. Unless we were to see an accelerative rise in the unemployment rate or a string of significantly negative payroll numbers (not our house baseline view), we don't think the equity market will become preoccupied with softer macro data this summer. In fact, a moderate slowdown in growth absent an unemployment cycle is likely constructive for stocks as it pulls forward rate cut expectations. The fact that the correlation between equity returns and bond yields just turned negative suggests that we may be entering a "bad is good" environment.

… The bear case scenario for equities tied to the recent events in the Middle East would be that oil prices rise significantly, thereby posing a threat to the business cycle. History suggests that such a rise in oil would need to be (1) in the range of +75% on a year-over-year basis ($120+/bbl) and (2) in a late cycle context in order to materially raise the probability of this outcome ( Exhibit 2 )…

… Last week's FOMC meeting was largely as expected. The Summary of Economic Projections (SEP) showed forecasts for lower growth and higher inflation this year, the median number of expected cuts for 2025 remained at two, and Chair Powell appeared to take a "wait and see" approach to adjusting the policy rate. Looking ahead, our economists see 7 cuts from the Fed next year, a more dovish stance than the bond market is pricing (4-5 cuts through the end of 2026). We also think it's interesting that Bloomberg's Fed Sentiment Natural Language Processing Model is getting less hawkish/more dovish in rate of change terms ( Exhibit 7 ). That dynamic seemed to be echoed by Fed Governor Waller on Friday when he said that the Fed could cut as early as this July. History is clear that falling fed funds rate regimes (excluding recession periods) are bullish for equities ( Exhibit 8 ).

… Same shop with a WORLD view …

June 23, 2025 MS: The Weekly Worldview: Enough uncertainty to go around

The interplay of country and sector tariffs, legal considerations, and trade deals will keep the level, timing and composition of tariffs uncertain. We discuss the read across of this uncertainty for the Federal Reserve.

… AND on the One Big Beautiful Bill Act (OBBBA) …

June 23, 2025 MS: US Public Policy: The Senate's Spin on the OBBBA

The Senate Finance Committee released text with changes to portions of the House-passed One Big Beautiful Bill Act (OBBBA), including Medicaid, IRA tax credits, Section 899 and remittance taxes. We offer our puts & takes on the key changes, as well as relevant impacts for key sectors & asset classes.

Key takeaways

Following a Senate vote, the bill must go back to the House for approval, but the early August timeline for final passage still appears reasonable, in our view.

Tempering Sec 899 and remittance taxes is supportive for securitized product securities, but we still see meaningful concerns around FDI given the policy mix.

For US equity investors, IRA and Medicaid changes will impact individual sectors, along with permanence and retroactivity for key corporate tax provisions.

The potential for the SALT cap to remain at 10k is not a negative for home prices in high tax areas, but we expect that provision to change again in the House.

In terms of directional deficit impact, proposed changes cut in both directions – namely, more Medicaid cuts while other offsets were watered down (IRA repeal).

I thought Switzerland was supposed to be neutral … this guy is anything BUT …

We live in a world of political polarization and soundbite economics. That encourages sensationalism. Deckchair generals will offer extreme opinions on the US attacks on Iran. Both supporters and opponents the attacks are likely to dramatize events. Investors should be cautious of knee-jerk overreactions.

Investors’ principle concerns are oil supplies and non-oil shipping. While there have been casual threats to close the Strait of Hormuz, Iran does need oil revenue and does not need the anger of oil-exporting Gulf states. Attacks on shipping by terrorist groups might be more likely. However, US trade taxes pose a far bigger threat to shipping volumes than events in the gulf.

US President Trump’s ruling out near-term attacks immediately before attacking might be tactical, but their suggestion of regime change in opposition to official US policy causes uncertainty. That raises trust issues relevant to trade negotiations. Even modest oil price increases will raise US gasoline prices just as trade tariffs push up other prices, and may add to profit-led inflation too. Tourism in the gulf region is already at risk, with flights being canceled.

Assorted central bankers speak, including ECB President Lagarde. South Korean trade data showed strong exports to Europe, and some increase to the US ahead of presumed trade tax increases.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

The. Terminal. Dot. Com … for things like this …

June 23, 2025 at 10:00 AM UTC Bloomberg: What Mike Tyson and the Bond Market Can Teach Trump on Debt Treasury buyers will be the ultimate arbiters on whether MAGA math adds up.

“Everyone has a plan, till they get punched in the face,” the former heavyweight champion and ear gourmand Mike Tyson once said. Swapping the boxing ring for the government arena, everyone has a plan for whittling down America’s debt, until they get punched by the bond market…

… At some point, though, the unstoppable force of MAGA energy runs into the immovable object of deficit math, and something has to give. Trump inherited a deficit that in 2024 amounted to 6.4% of the country’s gross domestic product, compared with an average of 3.8% over the previous half-century—a period that includes the budget-busting global financial crisis and Covid-19 pandemic. Factoring in the savings generated by Elon Musk’s so-called Department of Government Efficiency and the revenue from tariffs, Bloomberg Economics is forecasting this year’s gap won’t drop much below 6% of GDP.

In other words, Trump is moving the deficit dial, but not enough. Here are four reasons why, on the current trajectory, the US is pork-barreling toward a debt crisis…

…Last but not least, the bond market is starting to throw punches. One theory of Trump’s electoral success, popular with Democratic pundits, is that eroding trust in traditional media and the rise of social media echo chambers have left low-information voters with a distorted view of reality. Information bubbles might be an issue for some swing-state voters, but not for the Treasury market. Holders of US government debt have a clear-eyed view of America’s debt dynamics, and they don’t like what they see.

In May, Moody’s caught up with S&P and Fitch in downgrading the US sovereign credit rating. In what acronym aficionados will view as a missed opportunity, it took the rating from the top Aaa rank down a notch to Aa1, not the BBB that the Big Beautiful Bill calls to mind. The move didn’t spark a meltdown, but there were signs of a buyers’ strike, with 30-year Treasuries briefly trading at a yield above 5%.

Higher yields also reflect the remorseless logic of supply and demand. To fund historically elevated deficits, the Treasury needs to sell more debt, which means more supply. The appetite for US debt from China, Saudi Arabia and others, meanwhile, isn’t what it once was, which means less demand. The combination of the two means the Treasury will have to offer investors a richer reward for holding its paper. Higher interest rates will themselves add to the deficit. In 2021 interest payments on the national debt equaled 1.5% of GDP. By 2034, Bloomberg Economics calculates, they could be close to 6%.

Here, an OpED which you can tell must have been VERY hard to write … for a variety of Team Rate CUT(s) and other reasons …

June 23, 2025 at 4:00 AM UTC Bloomberg: Trump Doesn’t Always Chicken Out If there’s a model for hope how, it may lie in how quickly the 1991 Gulf War ended.

… Yet the regime has no choice but to retaliate if it wants to maintain its hold over its own people. Doing nothing would guarantee regime change. If it is to fall, it would far rather do so with a bang than a whimper. Closing the Strait, however, would be a desperate measure that might not last long. Tina Fordham of Fordham Global Foresight in London points out that parliament voted in a “consultative capacity”:

Such a move would have to be approved by the Supreme National Security Council... It is not clear at this time whether this action will be implemented or is a kind of protest vote from the parliament. Long regarded as Iran’s “nuclear option” for the global economy, any move to close the Strait could be undermined by the US carrier (and likely US Navy SEAL) presence in the region — the likelihood is that the US response would be swift and severe.

Such an escalation would evidently create further risks, and until they have been contained as convincingly as they were by February 1991 after the Kuwait invasion, risk assets face a headwind. To quote Larry McDonald of Bear Traps Report:

Iran has little downside to talking up the closure of the Strait of Hormuz. The real pain is the closure itself, which affects China, their cash cow, far more than the rest of the world. Bottom line: Oil prices will likely be elevated for the rest of the summer.

That would make it harder for the Federal Reserve to ease rates, and dampen economic activity. And that would in turn mean hits to commercial real estate, private credit, CCC-rated bonds, housing, and the US consumer.

For now, what’s happened is a headwind for global equities. It’s little more than that as yet, but TACO-happy investors might want to take some money off the table.

Some American Exceptionalism,

over the weekend...

Following Israel's Exceptionalism..

7 cuts in 2026......What ????

WS can sure get carried away, when comes to Rate Cuts...