while WE slept: UST (futs)tight range, low (holiday) volumes; #GotSteepeners? unwind of TBILL bubble? not JUST UoMICH inflation fears, see 5yr infl swaps

With U.S. Treasury markets closed on Monday, Wall Street stocks are set to cruise on higher into the unfolding corporate earnings season - but may first have to take early direction from China's weekend stimulus update… -Reuters Morning Bid (below)

… and so with the bond market CLOSED and China news over the weekend making the rounds and helping shape shift the narrative ahead of bank earnings, I'll be brief.

I’ll skip right ahead TO some of the news you might be able to use…

NEWSQUAWK: DXY flat and crude underperforms following lack of stimulus details and soft data from China … Bunds are firmer but with specifics light, USTs cash trade is closed on account of Columbus Day … USTs are holding above 112-00, in familiar and very tight ranges, given the lack of cash trade on account of Columbus Day. The main update thus far was the weekend unveiling of China stimulus; however, the somewhat limited details meant the market reaction was fairly muted initially

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

First up on China …

ABAmro: China - More fiscal support confirmed, numbers still lacking | Insights newsletter

On Saturday, Finance Minister Lan Fo’an confirmed that the Chinese government is working out more fiscal support measures. For instance, local governments will be allowed to use the funds raised by issuing special bonds for buying homes from property developers. This could give more momentum to a property stabilisation initiative launched in May. He also confirmed that the central government has ample room to increase public debt, which could be used to strengthen the balance sheets of local governments and large state banks, provide direct income support to specific groups and support for the property sector. However, he did not put numbers to these plans, something that investors had hoped for. More news on this is expected now in late October or early November.

… some have deemed this the unwind from the TBILL bubble (note from last week…)

…The Biggest Picture: record week of inflows to China stocks, record inflows to EM equities, record week of BofA private client T-bill selling (Chart 2)…investors all aboard the risk train on Fed cuts and reversal of ABC "Anywhere but China" trade; BofA Bull & Bear Indicator surges from 6.0 to 7.0, heading once again toward "sell signal" of 8.0.

We believe that the tone of recent US data supports 25bp rate cuts at both the November and December FOMC meetings.

With the start of Q3 earnings season and the US election less than a month away, we continue to like owning equity optionality.

As markets prepare for the US election, we warn that final results may not be known by 6 November.

… However, should the Fed skip a meeting this year, it seems to us that December is much more likely than November. This is for two primary reasons. First, the labor data that the Fed will get ahead of the November meeting will be especially muddied by weather effects. To wit was last week’s step-up in initial claims to 258k from 225k prior. Claims were about 9k higher than normal in North Carolina and 6k higher than normal in other southeastern states, while the jump in claims in Michigan was likely auto-related. Ultimately we expect a similarly elevated level to persist this week as hurricane effects linger on account of Milton’s impact in Florida, which makes for a more difficult read-through on the employment statistics. Second, from a political perspective, it would be very difficult for the Fed to justify to Congress cutting by 50bp in the meeting immediately before the election, only to keep rates on hold in the meeting after. Thus it is possible that if the data continue to run very hot ahead of the December meeting, the Fed could skip a cut at the last meeting of the year, but our read of inflation continues to suggest that this is a risk rather than a base case…

…The highlight on the data front will be September retail sales on Thursday, which will likely continue to tell a story of a resilient US consumer. But there may be cross-currents beneath the 0.3% m/m headline result we estimate, as a 4% seasonally adjusted decline in gasoline prices will provide drag while a jump in new vehicle sales will contribute positively. We expect control group sales to rise by a healthy 0.3% (the same rate as in August). Solid income growth and wealth effect tailwinds continue to support the US consumer – we look for Q3 PCE to print 3.2% q/q saar …

… and now for something Team Rate CUT might not wanna read, from a large German institution …

DB: Mapping Markets: 5 reasons why inflation risks are mounting

Six weeks ago, we wrote how it was too soon to dismiss inflation risks (link here). And since then, several developments have raised those risks further, including faster monetary easing from the Fed and ECB, the increasingly tense geopolitical environment, and a further pickup in money supply growth.

From a market perspective, we can already see how investors are pricing in more inflation for the years ahead. In fact, the rise in the 5yr US inflation swap over the last 5 weeks has been the biggest since early March 2023, just before SVB’s collapse. And in turn, that perception of growing inflation risk has contributed to higher yields, with the 10yr Treasury yield up more than 50bps from its intraday low in midSeptember, whilst gold prices have hit new highs as well.

So why are inflation risks still rising?

1. Near-term monetary easing has been greater than expected from the major central banks …

2. Recent weeks have seen a notable pickup in commodity prices because of the geopolitical situation in the Middle East and the stimulus announcements from China …

3. It’s becoming increasingly apparent that the US is likely not heading for a sharper downturn or recession …

4. The US CPI report for September came in stronger than expected last week …

5. Money supply growth has continued to accelerate, admittedly from a low base

In the US, M2 money supply growth was running at +2.0% year-on-year in August, the highest since September 2022…

… same firm with an inflation chart you likely don’t wanna miss (and may not wanna see … but seein’ is believin’)

Every action has an equal and opposite reaction. That's one reason that I’ve struggled to get my head around the most aggressive profile of Fed easing expectations seen over the last couple of months without there being a recession. At the peak just before the Fed cut 50bps in mid-September, around 260bps of cuts were priced in over 18 months. Today that’s closer to 200bps, including the 50bps we’ve already seen.

If the economy is in decent shape, a sizeable easing cycle surely increases inflation all other things being equal. Today’s CoTD From Henry Allen’s “Mapping Markets” (link here) shows that US 5yr inflation swaps have actually now seen their largest 5-week climb since just before SVB's collapse in March 2023, an event that shifted the narrative away from around 4 more hikes to imminent cuts for a period of time…

… global central banking as if it were a childhood game. AND same firm discussing data surprises supporting cyclical preferences …

The US and euro area are diverging on growth. And so could the pace of rate cuts by the Fed and the ECB.

A few months ago we published Divergent, convergent...it's about time, where we argued that the theme of convergence and divergence would continue, because while there are common global drivers of inflation, there remain clear differences for growth across economies. After months of convergence, the US and EA now seem to be starting to diverge again. The most recent data from the US suggest that growth remains resilient and inflation is gliding lower but not undershooting. In the euro area, weaker growth, elevated savings, and soft wage inflation all conspire to keep the divergence going.

In a repeat of swings we have seen recently, a handful of data have caused markets to swing like a pendulum. But that type of action is only to be expected. We have written frequently that in a soft landing scenario, inflection points are the norm, and so changes in expectations from each data point are to be expected. This past week, data in the US surprised to upside while those in Europe to the downside.

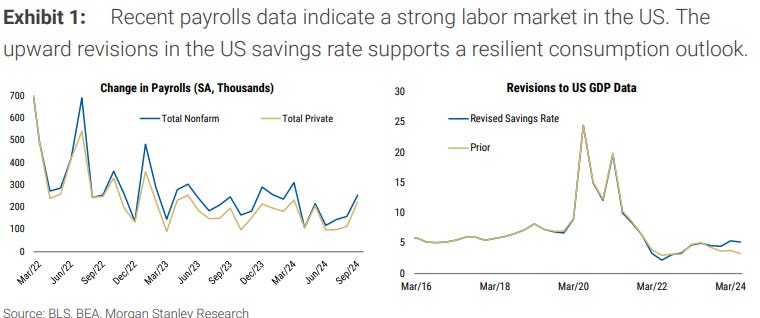

The shift in market expectations of the past two weeks reminded me of the game hopscotch - a playground game where you hop across boxes landing either on one foot or both as you progress. The US currently has two feet on the ground, with resilient real growth and falling inflation, a welcome contrast to the one-footed recession fears of the last couple of months. The US payroll data for September rebounded in line with our expectations, and firmed up expectations for a 25bps cut in November. The labor data has long been the missing link in what was otherwise a robust and resilient US economy. The strength of the US consumer continued to surprise to the upside, even as the market was focused on the labor data. The consumer outlook is arguably even more sustainable after revisions in consumption data showed the US savings rate is in a much firmer position than had been previously reported. The swing in sentiment was such that we have been fielding questions about whether Fed might in fact skip a rate cut. We fade that view, because inflation is still on its downward trend and even through growth is resilient, we still see some slowing to come…

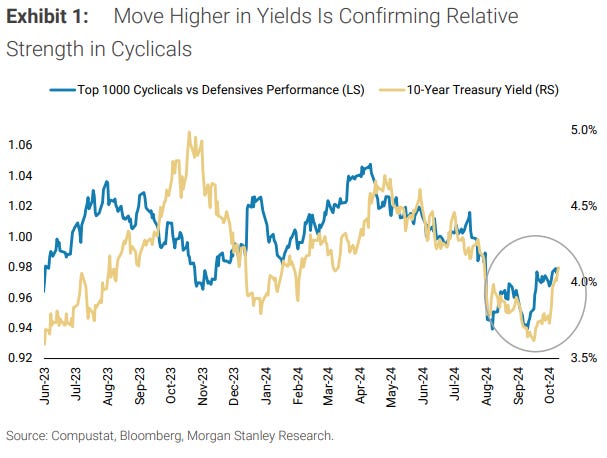

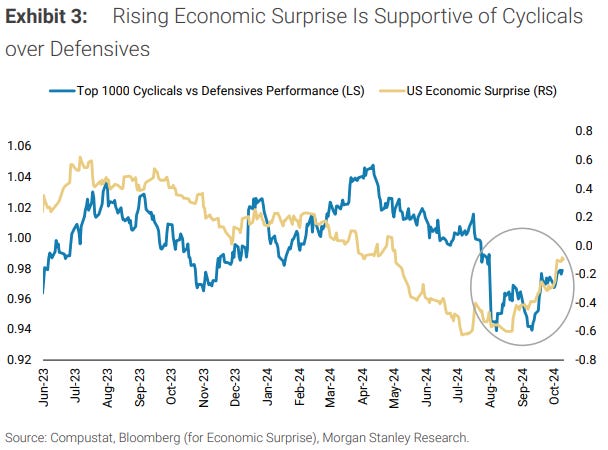

MS: Weekly Warm-up: Rates and Economic Data Surprises Support Our Cyclical Preference

Further stabilization in the economic surprise index should support quality cyclicals even if it comes amid higher yields. Today's note includes quality cyclical screens and commentary on election impacts. We continue to think the cadence of the business cycle matters more than the election outcome.

Rates and Economic Data Surprises Support Our Cyclical Preference...Importantly, the rates market is confirming the recent relative strength in cyclicals vs. defensives. Often times, the rates market tends to hold onto growth risks longer than the equity market. Thus, the recent move higher in yields following resilient data is also indicative of the idea that bond market pricing is shedding some of that growth concern. This confirmation gives us more confidence in our recent upgrade of cyclicals relative to defensives. Furthermore, our cyclical overweights at the sector level (Industrials, Financials and Energy) are exhibiting a positive correlation to rates. Conversely, defensives are exhibiting a negative correlation to yields. In other words, "good" macro data is still "good" for many large cap cyclicals, while it's "bad" for defensives. Thus, further stabilization in the economic surprise index should continue to support quality cyclicals' relative performance even if it comes amid higher yields. Today's note also includes stock screens focused on quality cyclicals and a summary of our recent micro/macro roundtable where our analysts across the department discussed key trends in their coverage industries…

… We re-enter 5s30s steepeners as we expect further rate cuts, carry has become less prohibitive, forwards are extremely flat, and election uncertainty could bring additional steepening risk …

… The key risk to our trade is data holding up better than expected in the near-term, leading the Fed to slow the pace of rate cuts. This could lead the market to pencil in a higher terminal rate, but with terminal pricing already rising to 3.4% from a recent low of 2.8%, the market has already adjusted significantly.

China’s much anticipated economy ministry press conference over the weekend did not give much detail. There were hints, and suggestions, and promises, but few clear proposals. International investors are looking for fiscal support because if consumers are restricting spending out of concerns for the future, monetary policy easing is unlikely to offer much help.

China’s September consumer and producer price data were both a little weaker than had been hoped. Food prices (mainly vegetables and pork) pushed up consumer prices, but not enough to overcome other disinflationary trends. Today there is the release of China’s import and export data. These numbers do not correlate well with other countries’ data (China exports 16% more to the US than the US buys from China, for instance). They should be treated with caution as signals of global demand.

The US marks the Columbus Day holiday. Meanwhile, Trump Campaign donor Bessent suggested that former US President Trump’s 20% universal tariff should be considered a bargaining tactic. This is what international investors want to hear (and it may fuel confirmation bias)…

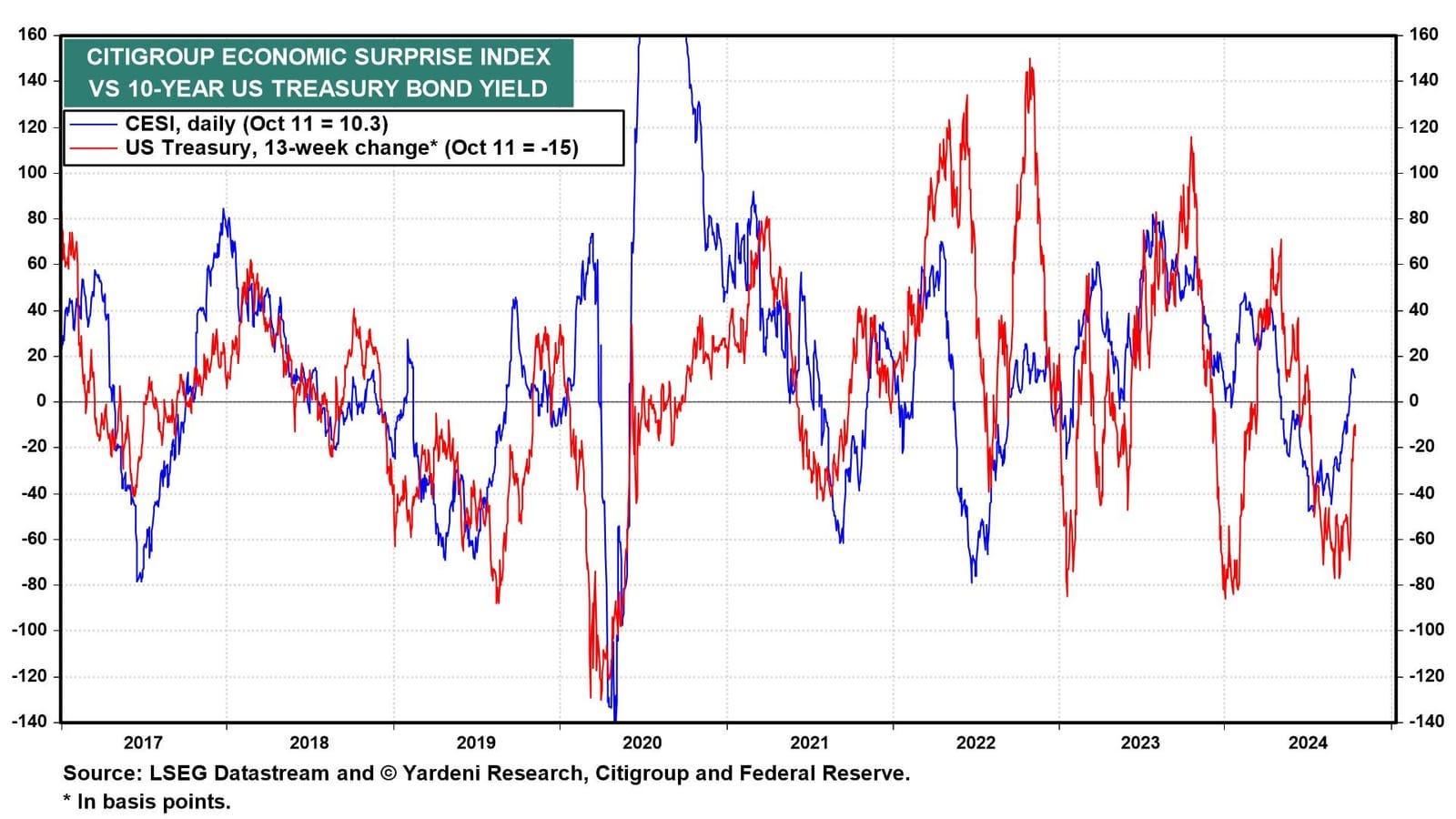

… and another economic calendar to help as you prepare for the week ahead as the good doctor shows economic surprises and 10yy are joined at the hip …

The economic week ahead will likely confirm that consumer spending continues to shine, while manufacturing production remains lackluster. Meanwhile, as earnings season kicks off with the S&P 500 at a record high and valuations relatively stretched, the onus will be on company managements to deliver better-than-expected earnings, which should be relatively easy since expectations are low.

As earnings surprises turned increasingly negative during the summer, so too did industry analysts regarding Q3 company earnings. By the end of August, the Citigroup Economic Surprise Index (CESI) sank to one of its most negative readings in several years. Just as Q3 ended, it turned positive, boosting bond yields and stock prices too (chart).

But the analysts haven't revised their Q3 earnings expectations for the S&P 500 any higher after lowering them significantly over the past few months…

US households have experienced significant gains in stock prices and home prices over the past 15 years, and Fed hikes have generated significant cash flows to owners of fixed income.

As a result, the debt-to-income ratio looks much better for US households compared with other countries, including Canada and Australia, see the first chart below.

At the same time, credit card debt for US households is at very low levels and declining, see the second chart.

The bottom line is that US household balance sheets are in excellent shape.

Combined with strong job growth, solid wage growth, rising asset prices, and the Fed cutting rates, there is no recession on the horizon.

… a couple visuals (of inflation / BREAKS, UoMICH, stocks vs bond) from The Terminal (OpED) caught my eye …

Bloomberg: Markets Return to a Trump Tipping Point

The narrative has shifted to where a Republican sweep must be considered. If inflation reignites, it won’t go smoothly for stocks.

… The five-year inflation breakeven, calculated by the difference between fixed-income and inflation-linked securities, has also sneaked up significantly, after briefly falling below the 2% target. Doubt is starting to seep in as to whether inflation is truly beaten:

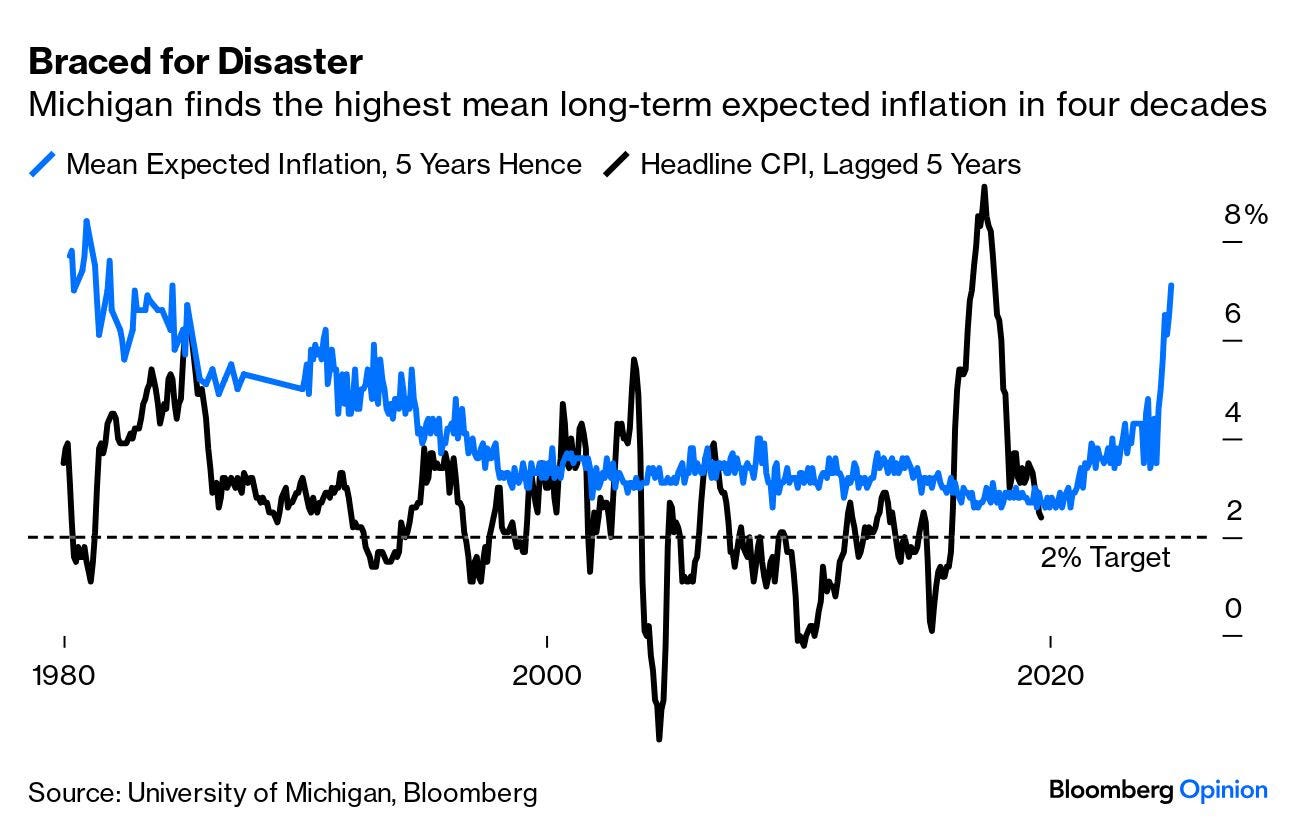

Meanwhile, the latest Michigan sentiment survey continued to show an extraordinary rise in the mean estimate of inflation over the next five years. This is distinct from the median, and is driven by a significant coterie of respondents who think inflation is going to take off in a big way. It’s also possible that Michigan’s shift to online surveying has affected the outcome. But still, if the average consumer thinks inflation will be 7% in five years’ time, that looks like trouble. With such sentiment, tariffs jolting up prices would have a big psychological impact:

If this sentiment-based estimate is right (it probably isn’t), then the fed funds rate won’t drop much further. It also, incidentally, shows tellingly how trust on inflation has been ruptured.

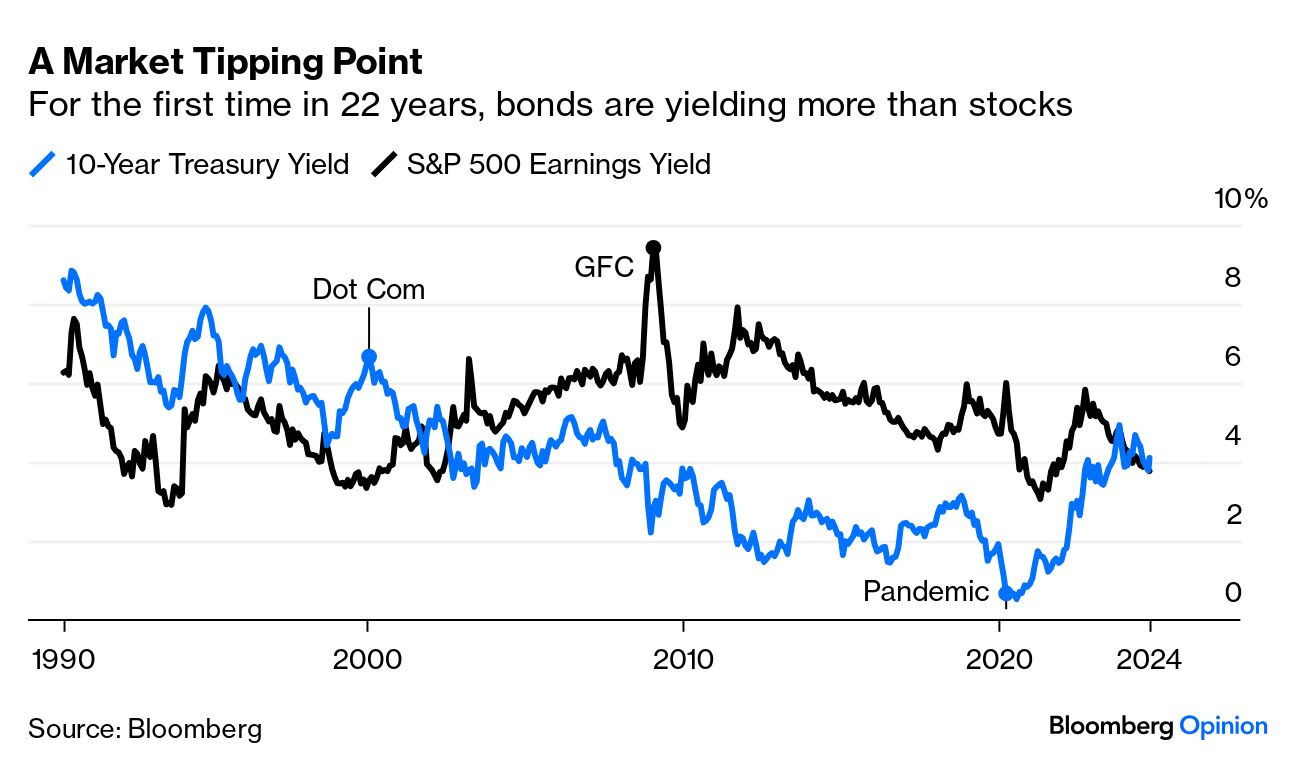

Are such nerves about rising prices consistent with a stock market at record levels? In a word, no. One of the simplest rules of thumb in finance is to compare the earnings yield on stocks (the inverse of the price/earnings ratio) with the 10-year Treasury yield. When stocks offer much more yield than bonds, it’s hard not to buy them — the ironclad truth that has propelled them forward ever since the Global Financial Crisis. But the earnings yield has dropped, and Treasuries are back to offering a higher yield with much less risk:

Big gaps between the two measures are unusual. When in stocks’ favor, they signaled historic buying opportunities (as in early 2009 when the worst phase of the GFC was coming to an end, and again during the 2020 pandemic lockdowns). The last big gap in Treasuries’ favor, in early 2000, signaled correctly that it was time to get the heck out of stocks.

For decades, it was the norm for bond yields to be higher. There’s no reason to predict a big equity selloff from the crossing of the lines. But if bond yields rise significantly from here, and inflation recurs — which is exactly what should be expected after a Republican clean sweep — it will be hard for stocks to continue their advances. That’s not in the price yet, but if the current political narrative continues, it will be.

… hard, soft or NO landing … ?

WolfST: What If There’s No Landing at all, But Flight at Higher Speed and Altitude than Normal, with Higher and Rising Inflation?

That scenario is re-emerging as a real possibility in recent economic data.

… THAT is all for now. Bonds are CLOSED (futs are open) and I’m off to the day job…

Great content, always appreciate