Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

They say a picture is worth a thousand words and I’m going to be real brief this weekend …

… a move higher, above 4% is thought to be a DipOrTunity by many (see or should I say LISTEN to, “In the Town of Strategy...” -BMO)

First UP, a couple / few things items from the week just passed where PPI was was hotter than expected or almost entirely benign …

Bonddad: September producer prices almost entirely benign; very little upward pressure in the pipeline

WolfST: After Large Up-Revisions, “Core” & “Core Services” PPI Inflation Not Benign at All. Whole Scenario Changed for the Worse

Six-month core PPI: +3.4%. Six-month services PPI: +3.7%. Year-over-year, both also accelerated further. But energy prices plunged.

ZH: UMich Sentiment Slips In October As Inflation Expectations Rebound

… THIS WEEKEND, a few things stood out to ME from the inbox …

… Machines learning Fedspeak …

BARCAP: FOMC Minutes NLP Analysis: Diverse discussion on monetary policy

Our NLP analysis points to differing views among participants on the outlook for monetary policy, amid extensive discussion of the size of initial policy recalibration, despite broadly shared views on inflation trending toward target and the outlook for activity viewed in solid expansion.

… same shop on INFLATION now that we know CPI, PPI …

BARCAP: US Economics (PCE inflation preview): September core PCE estimated to rise 0.26% m/m

Our translation of this week's September CPI and PPI estimates points to a 0.26% m/m (2.6% y/y) rise in core PCE prices and a 0.18% m/m increase (2.1% y/y) for the headline index. Our Q4/Q4 forecast for 2024 core PCE remains unchanged, at 2.7%.

… finally, this shop from UK asking the $64k question …

Knowing when to leave a good party may be a skill. Is it time for cash to shift into risk assets now that the Fed is lowering rates? We don't think so.

Households (HHs) and nonfinancial businesses (NFBs) have more sitting in cash (deposits and money funds) than at any time in the past 34 years. Much of this has accumulated since COVID.

The highest money fund returns since 2007 likely account for much of the $1.5tn in inflows since March 2023. But HHs and NFBs have increased their checking account balances. We think the latter reflects a shift in liquidity preferences that has increased the demand for precautionary safety buffers.

As a result, only a portion of the cash on their balance sheets may move into risk assets as interest rates fall. Even now, with blended deposit rates above 3%, there are few signs that this cash is ready to leave, despite better available opportunities in money funds.

We think the interest rate-sensitive portion of the roughly $1trn that has flowed into money funds since April 2023 could leave for higher return risk assets. But this would require lower interest rates and a decline in risk aversion.

We do not expect interest rates to re-test the zero lower bound. And with money fund returns unlikely to fall below 3%, there may be less reason for households or nonfinancial businesses to leave money funds or bank deposits.

The rotation into credit is unlikely for another six months or so. Money fund investors tend to rotate into riskier asset classes gradually when valuations are right and confidence rises. This usually starts into front-end investment grade corporates. The rotation is unlikely to happen now because money funds still yield more than front-end IG. However, this should change as the Treasury yield curve steepens. Treasury forwards imply that front-end IG should start to yield more than money funds in about six months.

For equities, we doubt that the foreseeable path of rates will create enough of a spread premium to encourage investors away from money markets and into stocks. The current S&P 500 equity risk premium (defined as 12m forward earnings yield over 10y Treasury yield) is 75bp; using post-Dotcom as a proxy for when a lot of cash moved from money markets into equities, we think 200bp is a good approximation of the trigger level. SPX would have to fall over 20%, to 17.5x NTM P/E, assuming that rates/yields follow the path priced in by forward markets, and we think that is unlikely, barring a market dislocation.

… Risk premiums aside, what if overall risk aversion falls? Over the past several decades, household cash holdings tended to decline once consumer sentiment stabilized or improved from the multiyear lows that are typically brought on by recessions. We think this could be a potential catalyst, albeit a weak one; consumer sentiment has already improved from the 2022 lows and household cash holdings appear to have merely moved from deposits into money markets. We think this is evidence of the structural shift toward higher precautionary balances and greater demand for safety discussed in a previous section, which could limit the amount of cash that moves toward risk assets spurred by improving sentiment alone.

… best in the biz ALWAYS worth slowing down to review … a note on PPI and a weekly essay …

BMO: PPI Mixed, Curve Steepens, Duration Remains Under Pressure

… Excluding trade, the move was 0.1% MoM with August revised down to 0.2% (was 0.3%). Portfolio Management costs were +0.3% and Airfares were +0.55% -- taking the edge off of higher core-PCE estimates, at least on the margin. Overall, this is a relatively benign update on producer prices and one that we doubt will materially shift policy expectations …

… At the end of the day, we anticipate that the Fed will look at the balance of risks and elevated uncertainty as reasons to follow-through with a 25 bp rate cut in November and, in all likelihood, another comparable move in December. While this outcome isn’t completely priced in, the odds are close enough that we’re comfortable characterizing it as the consensus at the moment …

… The coming sessions could readily challenge our expectations for dip-buying to become thematic as 10-year yields settle >4.0%. We’re all too cognizant that higher 10-year breakevens have the fundamental backing of the Middle East conflict’s potential impact on the energy complex as well as the implications from the upward surprise in the core-CPI series …

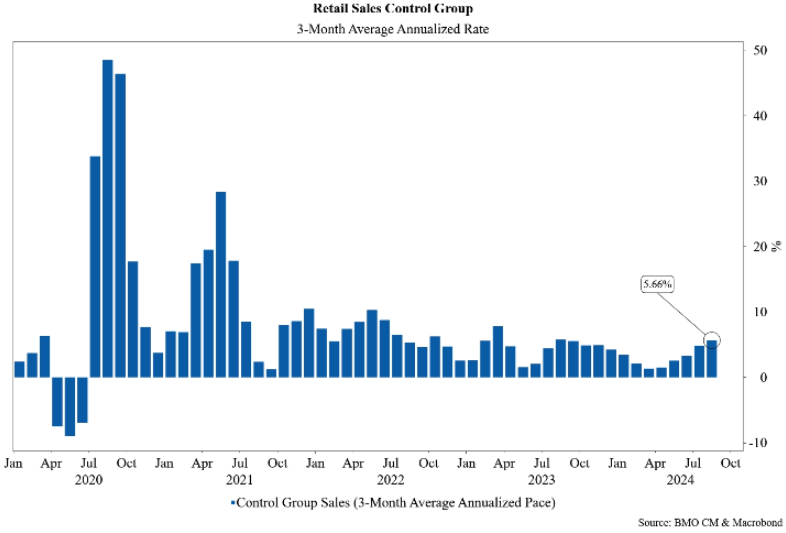

… The spending update is widely expected to uphold expectations for another quarter of resilient GDP growth and thereby give further hope to the soft landing outlook. As a more precise input for estimates of the consumption component of GDP, investors will be closely tracking the Control Group which is seen printing at a solid pace of 0.3% in September. For context, the index climbed by 0.289% in August and 0.392% in July. The three-month average annualized rate has climbed for five consecutive months and with the gauge currently at a 1-year high of 5.7% – US consumers appear well-positioned to continue serving as a pillar of the economic expansion – at least for now. …

… And from a large German shop, some thoughts and inflation, positions and flows which all matter …

DB: September inflation recap: Not too hot to stand in the way of further easing

Both headline CPI (+0.18% vs. 0.19% in August) and core (+0.31% vs +0.28% in August) were a bit stronger than our expectations. The year-over-year rate for headline ticked down a tenth to 2.4% while that for core actually picked up a tenth to 3.3%. Shorter-term trends in core remained well behaved, with the six-month annualized rate falling a tenth to 2.6%.

In terms of the breakdown within the expenditure basket, strength came from apparel, medical care services, and transportation services, which was partially offset by declines in medical care commodities and lodging away prices. Rental inflation also moderated closer to its June lows.

Friday's PPI data was also important, which, when viewed alongside the CPI data, point to a core PCE print slightly below its CPI counterpart. We are looking for core PCE to post a +0.28% gain in September, which would have the year-over-year rate remain roughly steady (2.64% vs. 2.68% in August), but it could tick down a tenth in rounded terms.

Our forecasts came up slightly in the near term, largely a function of price pressures from increased demand for vehicles in the wake of the recent hurricanes. Our initial read on the October core CPI data is that it will grow by 0.25% (rounding up). In turn, our 2024 Q4/Q4 core CPI forecast ticks up a tenth to 3.3%, while our 2025 and 2026 forecasts remain at 2.5% and 2.4% respectively. The analogous numbers for core PCE forecasts have similar updates: 2.8% (up a tenth), 2.2% (unch.), and 2.0% (unch.).

Taken together, this inflation data, though slightly stronger than expected, should not stand in the way of the Fed delivering a 25bp cut at the November 7th meeting. While our base case remains that the Fed will deliver three subsequent 25bps cuts (December, January, and March) before slowing to a quarterly pace for two more (June and September), there is the risk that they slow to a quarterly pace sooner.

DB: Investor Positioning and Flows - Sideways Positioning, Booming Inflows

Wells Fargo: Household Finances and Uncertainty Cloud October Consumer Sentiment

Summary

The University of Michigan's consumer sentiment index declined to 68.9 in October, as consumers increasingly report worries about both their household income situation and higher prices more generally. Inflation expectations in both the short and long term continue to remain well anchored.

… Year-ahead inflation expectations soured, with the median response expecting 2.9% inflation in a year, up from 2.7% in September (chart). Though the uptick in consumer inflation expectations is certainly not a welcome sign for the Fed, short-term expectations still remain broadly well anchored and in a considerably better place than the 3.3% reported in the May release. Long-term inflation expectations (5-10 years ahead) declined to 3.0% in October from 3.1% a month prior. This measure remains well anchored as well, as responses have remained between a band of 2.8%-3.2% for the entirety of the last two years.

… Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW …

… a weekly run through random economic stats with a clearly leaning narrative …

Going to a Broadway show can cost up to $200, and the latest weekly data shows that consumers are still happy to pay this discretionary expense, see the first chart below.

More broadly, GDP growth in the second quarter was 3.0%, and the Atlanta Fed GDP estimate for the third quarter is 3.2%, see the second and third chart.

Why is the economy so strong? Because of lower interest rate sensitivity for households and firms because of locked-in low interest rates, strong AI spending, and strong fiscal spending driven by the CHIPS Act, the IRA, and the Infrastructure Act. Combined with high stock prices and tight credit spreads, these forces are offsetting the long and variable lags of monetary policy.

See our chart book with daily and weekly indicators.

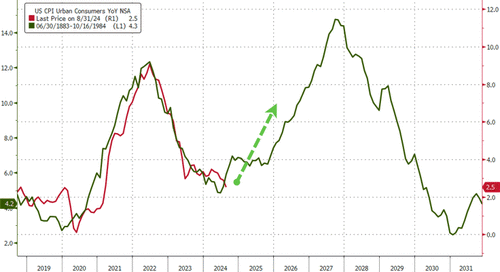

HERE is one on the ‘boiling frog’ concept where inflation is, well, in the pot…written / sent / viewed on The Terminal prior to PPI …

Bloomberg (via ZH): The Market Is Not Positioned For the 'Unwatched Inflation Pot' To Boil Over

… Price pressures had already begun to boil in the late 1960s, and it was the “bad luck” of Nixon closing the gold window in 1971, the Arab oil embargo in 1973 and the Iranian Revolution in 1979 that turned the decade into the Great Inflation.

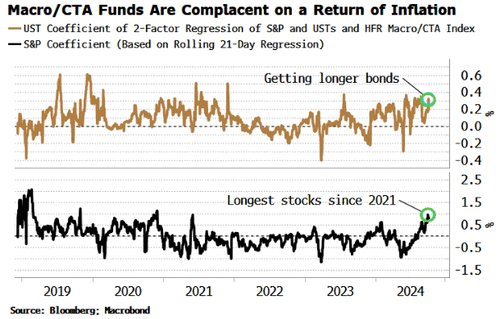

For September’s PPI data today (and following yesterday's CPI), it’s clear positioning is not expecting any big upside shocks, or more concernedly, not prepared for inflation that starts to trend higher again.

The chart below shows inferred positioning for CTAs based on HFR’s indices. A multiple regression on CTA returns versus the S&P 500 and Treasuries shows that they are likely long and getting longer stocks and bonds.

The CTA fund data is not perfect, but we see corroboration elsewhere.

The DBi Managed Futures ETF shows it has been getting longer 2-year and 10-year note futures as well as long-bond futures…

… someone who has a thought / (TV)visual on 10s …

SpectraMarkets: Friday Speedrun ... Goldilocks n, Bigfoot 0

… Interest Rates

No recession here The bond bulls scramble away Narrative shifts fast

The Fed communicated low confidence that the 50bp cut in September was the right move and now you have guys like Bostic saying November might be a skip. NFP came in roaring. Trump odds are moving higher. Bond bears hit the trifecta in the past 10 days as everything that bond bulls thought they knew proved incorrect.

That said, we are about to bump against major trendline resistance in yields at 4.15% and then above that there is the last major high before the August yield crap out at 4.50%.

The chart and the newly embraced short bonds narrative suggest to me that we consolidate next week. I would guess 3.90%/4.18% kinda thing. There isn’t much juice on the US economic calendar, other than Waller and Retail Sales, so it would probably take something ginormous from China to get yields through 4.20%. We have done enough work now, and bonds should take a rest for a bit.

The ECB announces their interest rate decision next week, and I expect that one to be boring as the 25bp cut is fully priced and there is no incentive for them to precommit from here.

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

FASCINATING interviews of DMB and Daniel LaCalle w/Keith at Hedgeye last wk!

Wow