while WE slept: 'Bonds are incrementally firmer'; only thing certain is uncertainty (NFIB?);"Short Treasury Bets Emerge as Big Rate Cut Expectations Vanish"

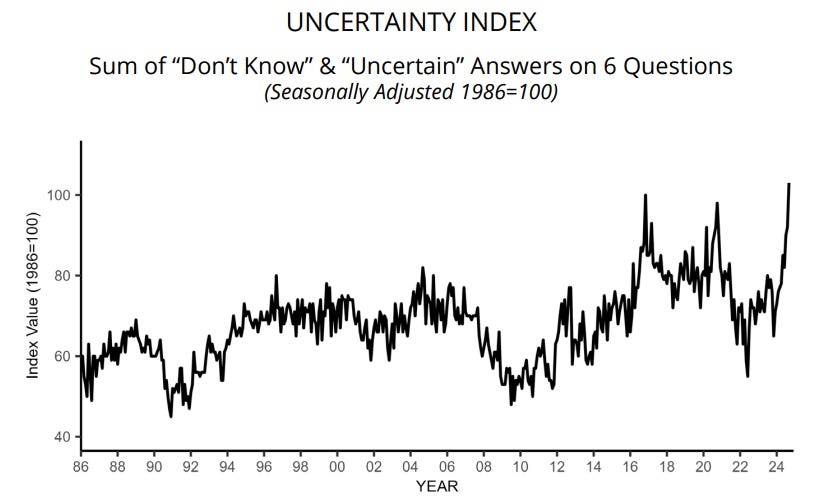

Good morning … bonds are better bid, shorts are back en vogue and uncertainty is at record highs (NFIB, below) as Uncle Milton set for landfall …

Let’s review — 3s came and went …

ZH: Gruesome, Tailing 3Y Auction Sees Plunge In Foreign Demand As Buyers Flee

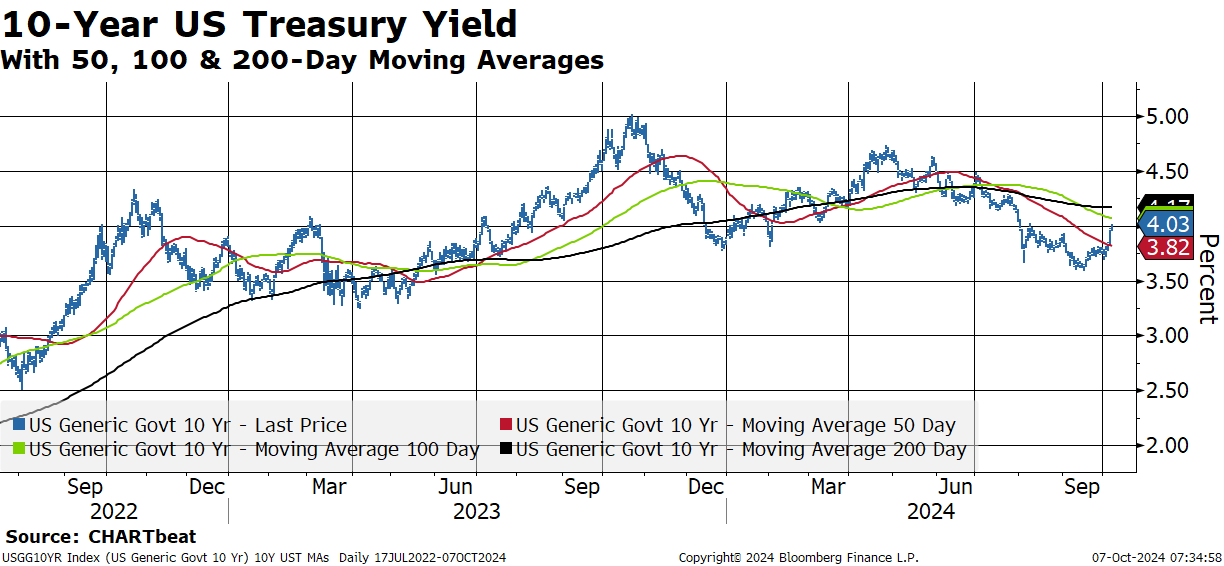

… and thisweeks supply of durationcontinuing today with $39bb reopened 10s … depending on your framework, you may be buyin’ this dip or planning to sell whatever the RIP, on a medium to longer term time-frame … here’s what I mean …

WEEKLY: momentum here has moved from overbought to about middle of the range and so, not as much a medium term BUY signal as maybe the daily above is as a shorter-term one

MONTHLY: 4.00% inflection point as momentum here, on longer-term basis, remains overBOUGHT …

… and for somewhat more from someone with a Terminal …

NEWSQUAWK: Bourses choppy, while the Dollar, Crude and Bonds are firmer ahead of Fed minutes & speakers … Bonds are incrementally firmer, UK auction garnered solid demand but the tail was still large sparking some modest pressure in Gilts … USTs are firmer but with upside relatively modest in nature though, with USTs shy of Tuesday’s and Monday’s respective highs of 112-24 and 112-28+. FOMC Minutes and a slew of Fed speakers are due.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ … it’s slim pickings today … starting off with a couple from a large German bank …

… Those geopolitical risks stayed front and centre yesterday, as investors waited to see what form Israel’s response against Iran might take. Amir Ohana, the speaker of the Knesset, said yesterday that “discussions are still taking place at the highest levels regarding the outline of the response — but it will be significant, and it will come”. In turn, Iran have also warned that they would respond to any attack, with foreign minister Abbas Araghchi saying yesterday that “We advise Israel not to test our will”. So there are still significant fears about how the current situation could escalate. Later on, there was renewed uncertainty over future steps by Israel as the US Pentagon confirmed that a planned visit to Washington by Israel’s defence minister Yoav Gallant had been postponed. Bloomberg and other outlets reported that this came due to last-minute objections to the trip by Israel’s PM Netanyahu.

The latter news caused a decent spike in oil intra-day but the overall market tone was still one of a moderation in geopolitical risk pricing, in part following earlier comments by Hezbollah’s deputy leader that it backed efforts by Lebanon’s officials to reach a ceasefire. This saw Brent crude (-4.28%) fall back to $77.47/bbl, whilst WTI (-4.63%) posted its biggest daily decline of 2024. So that ends a run of five consecutive daily gains, in which oil prices saw their largest increase over 5 sessions since Russia’s invasion of Ukraine began in early 2022. Broader volatility also fell back, with the VIX index coming down -1.22pts to 21.42pts…

Market fixings are currently pricing September CPI at 2.37% vs 2.3% consensus YoY, 2.31% consensus Index NSA and 2.38% DBecon. Given consensus distribution around headline and core CPI MoM (0.1% and 0.2% MoM), as well as DB economists' forecasts and our market-implied energy modelling, markets appear to have converged towards 0.25-30% MoM for core CPI.

… everyone’s fav British economist (?) on the Fed …

The minutes of the last Federal Reserve meeting are due, and should be fascinating. This meeting cut interest rates by 50bps, and had the first Fed governor dissenting in over two decades. Dissents may possibly be managed as part of the theater of the Fed—a single high profile dissent may mask wider disquiet at the scale of the rate cut. Certainly Fed Chair Powell’s dependence on dodgy data is looking a questionable strategy in the wake of recent (inevitable) data revisions.

The tone of the Fed minutes should not change expectations of further rate cuts—the Fed is still scrambling to catch up with inflation slowing in the US, and started cutting rates late. But expectations about the pace of easing may be set by the minutes…

… lower rates leads to increased consumption, right ? … ummm …

Wells Fargo: Lower Rates May Not Provide Much Lift for Consumer Spending

Summary Consumers went the full 12 rounds with the Fed in this cycle and never suffered a knock-down. But if higher rates were insufficient to slow consumer spending, why should lower rates be the magic elixir to make spending grow faster?

… The revised data paint a picture of a consumer that has not only spent more than previously reported, but had done so while saving more out of each paycheck than first reported as well. That divergence perfectly describes why this easing cycle is different. The Fed is not acting to correct policy to swiftly stimulate growth, but rather reduce the amount of restriction imparted on the labor market by higher rates. Get it right and the FOMC can avoid a more pronounced slowdown, or even the possible recession that often comes with sharp upticks in unemployment. The odd part is how consumers have continued to spend even as evidence mounts that the burden of higher rates was making consumer debt more expensive. The relatively restrictive stance of monetary policy of the past two years has led rates higher for an array of consumer loans (Figure 1). The Fed deems it's time to remove some of that restriction.

Cuts Both Ways: I’m Earnin’ Here We are not economic heretics: lower rates obviously have a stimulative effect on the economy. As the Fed lowers the federal funds rate, that translates to lower rates that banks charge on consumer loans and will indeed cause households' personal interest expense to eventually head lower as well. As seen in Figure 2, there is a fair bit of correlation between personal non-mortgage interest expense and the federal funds rate over time.

…Conclusion Lower rates not only mean lower payments, but lower income. In plain English, the extra income households have enjoyed amid the highest rate environment in 20+ years will gradually fade as the Fed cuts, and at least in terms of the macro landscape, the lost income will likely be bigger than the savings conferred when households spend less to finance their debt. Lower rates will still free up cash flow to spend elsewhere and should be somewhat stimulative. While any given household’s reaction to rate cuts will depend on their financial situation, the aggregate impact of rate cuts on personal disposable income could actually be less money in consumers’ pockets.

… forget lower rates, at least small biz are more optimistic …

Wells Fargo: Small Business Optimism Ticks Up in September Despite the Slight Improvement, Sentiment Remains Bleak

Summary Economic Woes and High Uncertainty Dent Small Business Outlooks Small businesses owners remain fairly downbeat on the economy. The NFIB Small Business Optimism index rose 0.3 point to 91.5 in September. Although the outlook for business conditions has improved significantly over the past few months, so has economic uncertainty. The uncertainty index capturing the share of firms answering "don't know" or "uncertain" to at least six questions jumped to its highest level on record dating back to 1987. The upcoming election is certainly a large influence, however a number of economic factors are also playing a role. Sales, capital expenditures and inventory investment all weakened in September. Although looser labor market conditions are improving the availability of workers and reducing compensation pressures, job openings continue to decline on trend. On the upside, the descent in hiring plans seems to have stalled, remaining essentially unchanged over the past five months. NFIB survey responses also remain consistent with downward-trending inflation.

Source: NFIB and Wells Fargo Economics

… may be somewhat more optimistic but at same time, small biz are most uncertain EVER …

NFIB: Small Business Optimism Index Main Street Uncertainty Reaches All-Time High

… The Uncertainty Index rose 11 points to 103, the highest reading recorded…Uncertainty is at a historically high level. The election will trigger adjustments to plans once the results are known…

… And from Global Wall Street inbox TO the WWW,

… POSITIONS …

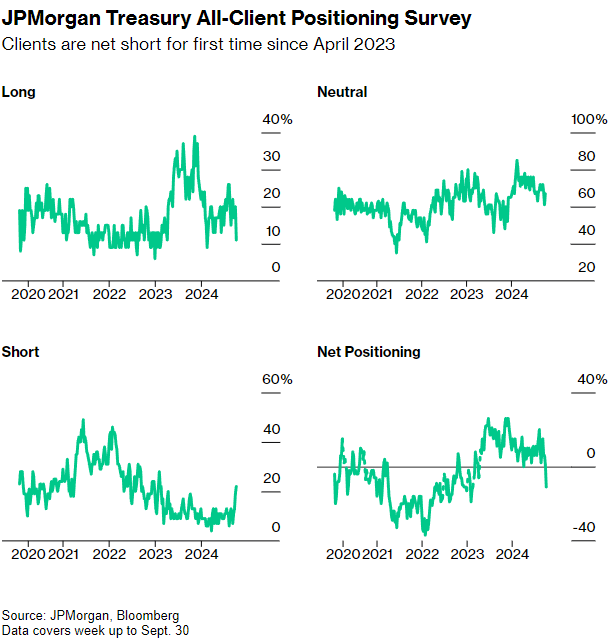

Bloomberg: Short Treasury Bets Emerge as Big Rate Cut Expectations Vanish

Open interest across SOFR futures collapsed since payrolls

JPMorgan clients are net short for first time since April 2023

(Bloomberg) -- Traders are beginning to bet on losses in the US Treasury market as they price in a more gradual pace of Federal Reserve interest-rate cuts ahead.

At the same time, short wagers are starting to emerge. The move has led to the biggest outright short position in the cash market since February 2023, according to a survey of JPMorgan Chase & Co. Treasury clients.

… same shop with a h/t to Yogi … and bonds …

Bloomberg: China, whatever it takes is a lot more than this Markets have thin patience after years of uninvestability. Authorities need to get their messaging under discipline.

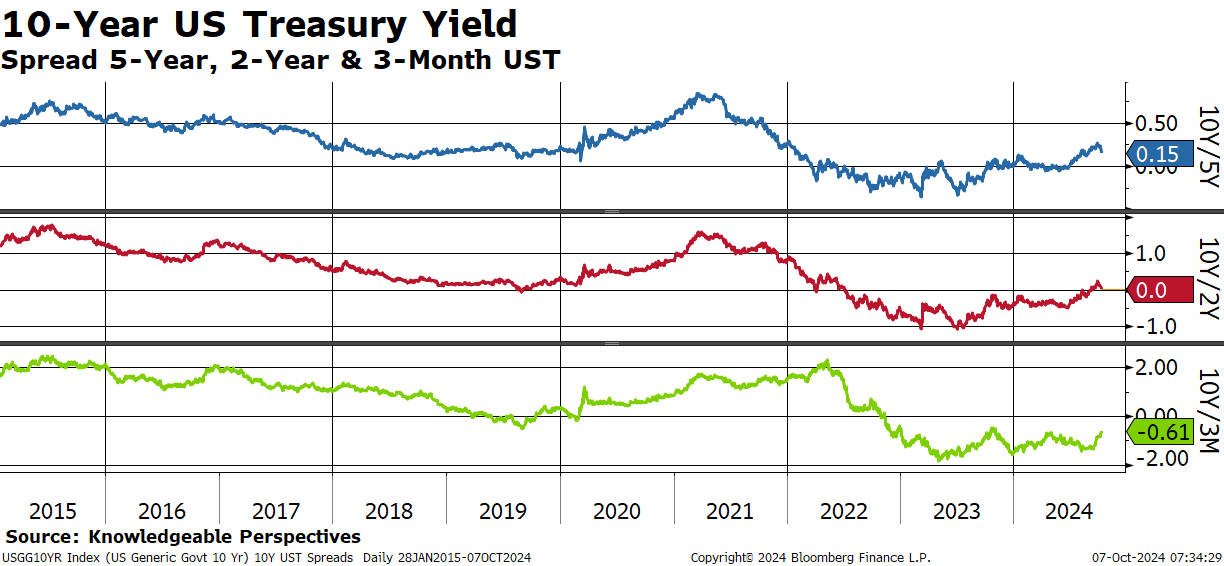

… The Fork in the Road Where to next? Treasury bonds appeared to be locked into a new bull market (meaning yields declined) as everyone declared victory over inflation and waited for lots of interest rate cuts from the Federal Reserve. That assumption is now in question once more, with the 10-year yield back above 4%.

Treasurieshave a historic tendency to settle into long-running trends. The last secular bull market saw the yield decline steadily for almost four decades, from the era of Paul Volcker at the Fed in the early 1980s until the pandemic. Since then, it’s plainly broken out of that downward path and arguably established a new upward trend. Since early April, however, it has appeared to be headingdownward. Technical analysis shouldn’t be taken too seriously, but it can have a big impact on traders’ behavior. As this terminal chart shows, the yield has now reached a point where both the upwardtrend since 2020 and the downward onesince April remain intact, while the yield is close to crossingits 200-day moving average. Edge much higher and sentiment could easily tip once more. The bear thesis would be seen to be confirmed:

Thursday’s inflation data could have a big impact. So could the increasingly scary international situation. The week’s most important new data point so far — on filling jobs — cut either way. The National Federation of Independent Business’s long-running survey has been a great leading indicator in the past. The proportion who say that they’re finding it hard to fill jobs has now dropped sharply and returned to pre-pandemic levels. That suggests the labor market has still been substantially tamed, and with it the inflationary pressure that it might produce. But jobs are still harder to fill than they were for much of the three decades before the pandemic, which might argue for continued high rates:

Away from the data, let’s concentrate on two measures that have had slightly less attention. First, there is a bullish case to be made from the mortgage market. Arguably, the rock-bottom rates available through most of 2020 and 2021 are skewing perceptions. The average 30-year mortgage rate tends to move in line with long Treasuries and appears to be declining from levels that imply extreme pain for anyone owning or wanting to buy a home:

This makes it look as though conditions have already eased substantially, even if mortgage rates remain higher than they were during the extended quantitative easing era of the last decade. Thus, debatably,there’s little need for further easing by the Fed.

However, Peter Berezin of BCA Research offers the effective average mortgage rate, derived by dividing total interest payable by the total volume of mortgage debt in force. This takes into account the many mortgages still in effect from 2020 and 2021. While the latest 30-year rate is about 6.2%, the average is only 3.9%:

Berezin points out that this changes the picture for the Fed, as the average rate that people are paying will rise very substantially even if the fed funds rate stays constant. Cuts are necessary, along with falling bond yields, to avoid an effective tightening:

If mortgage rates do not change, the average rate will eventually converge to the current mortgage rate as older, lower-rate mortgages are paid off and replaced by newer, higher-rate mortgages. As a share of disposable income, this would increase mortgage payments by 1.6 percentage points, forcing homeowners to cut spending on other items.

So that’s an important element in the case for a continuation of the bull trend in the bond market. The needs of the US housing market and the impact on consumer spending will not permit anything else.

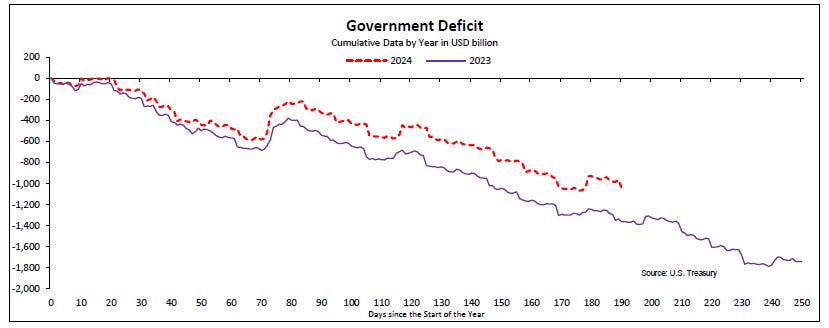

To counter, Vincent Deluard of StoneX Financial declares that the Fed’s jumbo rate cut last month has ushered in a new bond bear market. The extent of the deficit, and the likely pressing need to raise issuance, is key to this. Surprisingly strong tax collections this year mean that the US deficit is not quite as steep as it was at this point last year:

He argues that this should “normalize” over the next three months, “as spending has picked up in the summer and should surge due to extraordinary spending caused by the wars in the Middle East and the floods in the South.” That would translate into higher bond supply, and higher yields. Deluard also highlights the incongruity of the current market expectation that the fed funds rate will bottom just below 3% next year, and that recession will be avoided. The average low for fed funds in cycles where recessions are averted, he says, is 4.2%.

The Global Financial Crisis was 16 years ago, and the number of people active in finance both then and now is beginning to dwindle. It’s understandable that many are assuming that the new normal will be a return to the typical post-GFC norm, in which case a fed funds rate of 3% or lower seems to make sense. But they’re probably wrong, and if so, the chances are that the bear market in bonds will continue.

… CONSTRUCTION …

EPB Research: Residential Construction Backlogs - How Much Longer? Measuring the existing backlogs in the residential construction sector and analyzing the future impact on employment within this critical industry.

… Currently, the two sectors are averaging job losses of 5k to 10k, a significant factor contributing to the weakening labor market trends but not substantial enough to spark a recessionary spiral.

Backlogs in the residential construction sector still exist and will remain for another 2-3 months before reaching a historically average level of completed inventory. Job gains in the sector will become more difficult at that point, and sharp job losses are a high risk in 6-8 months if current trends persist and push completed inventory north of 30%.

In the meantime, the durables manufacturing sector is shedding jobs, and an increased pace of job losses from here risks the recessionary warning zone, even without negative contributions from residential construction.

Watching the trends in residential construction and durables manufacturing employment is vital to navigating the Business Cycle and future recessionary risk.

… elections have consequences and so …

LPL: Stock Markets: What To Expect When We’re Electing

…Stocks Tend to Dip Before Election Day, Before Strong Performance into Year-end S&P 500 | Daily Progression (1950-2024 YTD)

If Trump is elected, expect the BLS to become much more negative on the NFP numbers....

Right now, the BLS NFP numbers are not believable.....