… While a slump in mortgage lending due to rising rates was a drag on consumer lending portfolios, credit card loans were way up, with JPMorgan and Wells Fargo both reporting a 17% jump …

Credit cards “WAY UP”. Think about that … ever check interest rate charged on your CC? I’m sure completely irrelevant as everyone using CC simply to rack up miles for their next revenge travel experience. Meanwhile, back at the ranch here in Monmouth Cty over the weekend, I spotted in a couple / few different locations something I’ve never seen outside of a major city — folks with signs begging for cash due to high / rising cost of rent and food.

This past weekend I had noted a few Sellside observations and offered a couple economic calendars (20yy auction Wed) noted HERE for those looking to plan their trades and trade their plans.

Finally, I also suggested a selloff in bonds might help as far as Wednesday’s liquidity event (aka 20yr vs 50dMA - 3.386% worth watching into / through auction). Here’s an updated look at 20yy

Note momentum (mentioned as overBOUGHT Sunday afternoon) has crossed so path of least resistance suggests concession ahead!

… here is a snapshot OF USTs as of 737a:

7777777777… HEREis what another shop says be behind the price action, you know,

WHILE YOU SLEPT Treasuries are lower and the curve is a hair steeper with volumes light ahead of a light week for US data and with Japan out on holiday. Firmer commodity and global stocks prices have bunds pacing the declines ahead of the ECB Thursday. DXY is lower (-0.7%) while front WTI futures are higher (+2%). Asian stocks, ex-Japan, were all higher, EU and UK share markets are showing decent gains (SX5E +1.5%, SX7E +3.25%) while ES futures are showing here at 7:25am. Our overnight US rates flows saw better buying in London's AM hours (especially 30yrs) from Asian and EU names. Overnight Treasury volume, with Japan out, was roughly 60% of average across the curve…

… UST 10yrs and where prices indicate the sellers have control (~2.71%) and the buyers have control (~3.50%), for now.

… and for some MORE of the news you can use » IGMs Press Picks for today (18 July) to help weed thru the noise (some of which can be found over here at Finviz).

Here are a few items inboxed to Global Wall St overnight …

Hot inflation data has made a 75bp Fed hike all but certain this month

… This week we expect the ECB to hike by 25bp and to announce details of its new tool to ensure orderly transmission of policy across the euro area. Several EM central banks delivered hawkish surprises last week; this week we expect BI to stay on hold, despite a weaker IDR. The SARB will likely hike by 75bp while the CBT holds and the CBR cuts 50bp. The BoJ should be unchanged.

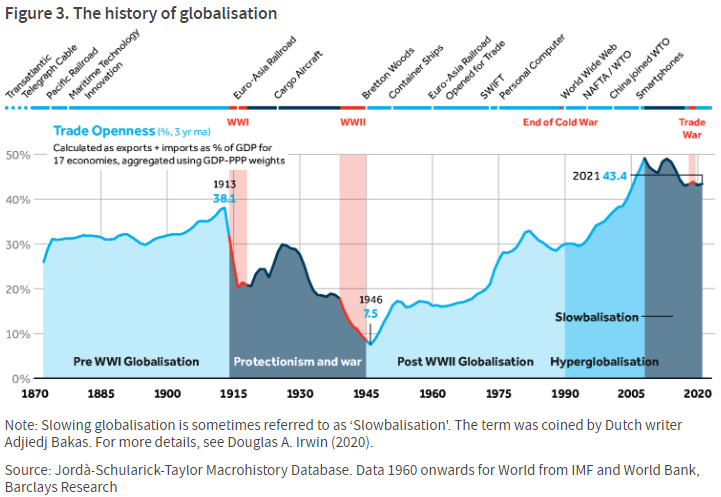

… Globalisation is in retreat. Governments and firms are examining global networks to minimise exposures to possible economic damage and social turmoil. Executives are using terms such as "re-shoring," while large S&P 500 companies are recruiting more in their home countries, noted Christian Keller and team. Deglobalisation: Homecoming, 13 Jul 2022

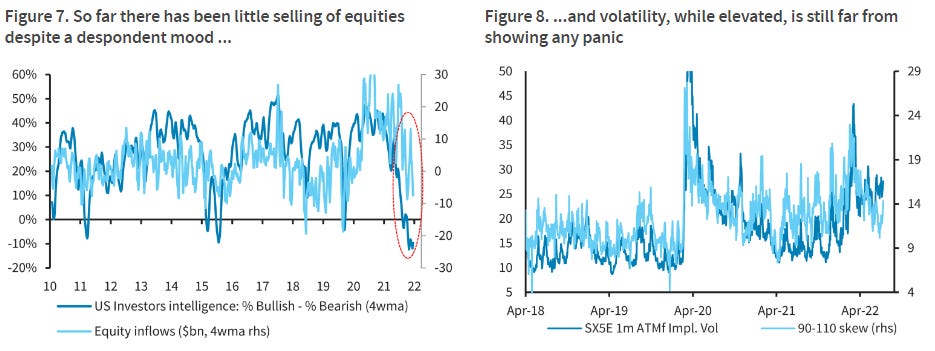

… Equity investors in the US are bearish but not panicking.Emmanuel Cau spent time on the road with US equity and macro clients, and found them frustrated but hopeful that things may not turn out to be as bad as feared. This attitude is consistent with our flows data showing no capitulation, and still-low levels of volatility. Still, weaker growth, tighter policy and messy geopolitics is not a good mix. We stay cautious. European Equity Strategy: Equity Market Review - Feedback from US clients - bearish mood, hopeful positioning, 15 Jul 2022

Speaking of EQUITY INVESTORS IN THE US — bearish but NOT panicking — those not yet panicking might be setup defensively as chief stock jockey for MS notes,

Defensive Leadership Can Continue as Earnings Cuts Begin While Defensives are the clear leader, most investors aren't there, leaving more upside potential as earnings cuts begin. Counter-trend rally may continue, but make no mistake, we don't believe this bear market is over, even if we avoid a recession – the odds of which are increasing.

…Positioning Does Not Equal Price Or Sentiment Last week, we highlighted how extreme the 12-month price momentum weightings are for defensive sectors. Exhibit 1 illustrates that it is rare for this type of price momentum to occur outside of an economic recession. One potential reaction to this chart may be that a recession is priced based on this dynamic, and that defensive leadership is likely to reverse with something else taking the lead – like growth, or even cyclicals. We disagree, and believe defensive leadership will likely persist until we either enter a recession officially or the risk of a recession is extinguished definitively. In our view, the first outcome can only be achieved with a series of negative payroll data releases, something that still seems far away given last month's 372k new job additions.

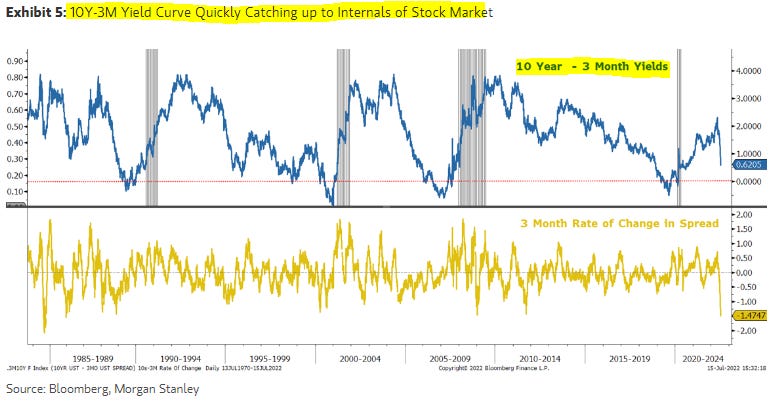

… In the very near term, equity markets seem to be digesting another hot CPI data point even as concerns rose that the Fed might raise rates as much as 100bps next week. Our view is 75bps is still the base case, and that should be plenty to take us into the late innings of the cycle. This hasn't been lost on the bond market, with the curve (10s-2s) inverting as much as 27bps, the most since 2000. Meanwhile, the real recession predictor (10s-3mos) is also falling at a rate rarely witnessed in any economic cycle (Exhibit 5). In short, the bond market is quickly catching up to where the internals of the stock market have been for months. The bullish take, which the market seems to want to try to run with one more time, is that the Fed can pivot before this recession indicator (10Y/3M curve inversion) that has a 100 percent track record gets triggered. Time will tell.

The other positive that has some investors excited again is the fact that the bank stocks had a strong rally Friday even as the results were mixed (with some results quite poor). While this kind of price action is a necessary condition for the bear market to be over, we would caution that 2Q results are likely to be the first of several cuts, not just for banks, but for the market overall. This is where our analysis can be helpful to investors who are ready to sound the all-clear. In the next section we lay out the case for why this is the first of several cuts, especially if a recession is the end game.

Wait, what? Bonds catching up to where STOCKS have been for months? Ok, well, we can agree to disagree — stock guy thinks stocks lead and bond guy (me) knows something of a different experience. We can agree to agree whats MOST important is whatever The Fed does / doesn’t do NEXT … Pivot?

If SO, think another COST-OF-LIVING-CRISIS (HIMCO). Another pivot also likely to be BEARISH BONDS (lack of commitment TO fighting inflation).

Finally, one last note from the Sellside … with The Fed officially in their self-imposed ‘blackout period’ before the next meeting and only Nicky T and GS (and other experts on the sellside) to guide us in as far as what next from The Fed, a useful tool from Wells Fargo

Summary We forecast that the FOMC will raise rates by 100 bps at its next policy meeting on July 26-27, but we acknowledge that the risks now appear to be skewed toward a smaller increase of "only" 75 bps. What will the Committee signal about future policy moves? We discuss our expectations in this report.

Bond and stock jockeys all watching for whatever NEXT. Nobody knows for certain — likely not even The Fed. Meanwhile, the trek towards a peak continues