while WE slept: stocks bounce back, USTs 'inch' higher; "US10Y yield: 2023-2025 is rhyming with 2015-2017"; why UST mkt has DEMAND problem; spec LONGer'er ...

…Jumping right in to the day and week ahead, today kicks off coupon supply with $69bb 2yr USTs (5s tomr and 7s Wed all due to month-end Friday) and so …

2yy: triangulating within narrowing range (4.30 - 4.20) …

… with red circle and arrow etched in to highlight daily momentum stretching into over BOUGHT territory as resistance respected … this to say that a dipORtunity may be welcomed …

… This ‘dipORtunity’ arriving within context of CME FedWatch Tool HERE helping the point Team Rate Cut has been making for quite awhile (and who may very well have Slok as a member soon) …

I’ll quit while I’m behind and skip ahead TO a snapshot OF USTs as of 615a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

Opening Bell Daily: Buffett's new wisdom. Warren Buffett keeps hoarding cash but he's still bullish on stocks long-term. Unpacking the Berkshire Hathaway CEO's annual letter…Berkshire ended last year as a net-seller of equities for the ninth consecutive quarter. Its cash reserves ballooned to $334.2 billion, up from $325.2 billion in the third quarter and $167.6 billion the year before…

QT could end earlier than the market expects if the Fed takes a conversative approach going into debt ceiling discussions.

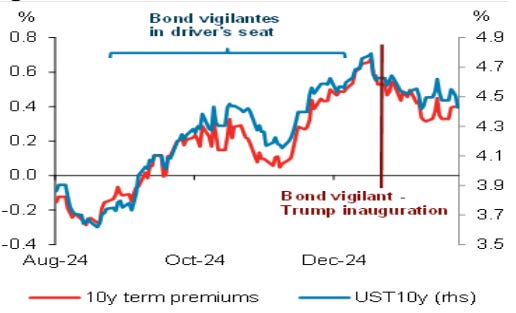

We continue to like 2s10s flatteners as a more bond-vigilant administration fights off bond vigilantes.

We like EUR shorts into the German elections, as we think the market prices in too much good news.

…Fig. 2: Bond-vigilant administration fighting off bond vigilantes

… and this

MS: Sunday Start | What's Next in Global Macro: Living in a Post-Tariff World

… The price/volume trade-off at the firm level translates into an inflation and growth risk at the macroeconomic level. We anticipate that higher sensitivity to growth and inflation will accompany material trade barriers. Because production cannot shift quickly, higher costs from tariff and other trade barriers will come into play. Our supply chain data show that across many goods, dependence on China and other geopolitically distant exporters cannot be easily reduced. The challenge may be particularly acute in the United States, where manufacturing-linked capital stock has been depleted and the investment required to rebuild will be substantial and take time. These challenges imply that solutions will take years not months, and costs could remain elevated in the interim …

Moving on to a couple / few things I stumbled on and which may be of some interest as the day / week gets underway …

…Rates: Hold soft long duration bias US: We hold a soft long duration bias. 10yT trade cheap vs fundamentals but only marginally cheap vs global yields => conditional short US vs EUR rates as hedge for our baseline view…

…Technicals: The ghosts of 2017 Marco markets are rhyming with 2017. If history continues to repeat, the 10Y yield double tops at 4.80% or 5% by Memorial Day and declines to Labor Day

…US10Y Yield: Double top at 4.80% / 5% by Memorial Day? We compare 2015-2017 with that of 2023-2025. If history continues to repeat/rhyme, the comparison suggests yield double tops by the US Memorial Day holiday in May 2025 and declines into the US Labor Day holiday beginning September 2025. Such a double top could be at about 4.80% (YTD high) or 5%. (Oct 2023 high). The primary difference is the tide. Now is a secular bear market while 2016-2017 was a secular bull market…

…US10Y yield: 2023-2025 is rhyming with 2015-2017 We compare 2015-2017 with that of 2023-2025. If history continues to repeat/rhyme, the comparison suggests yield double tops by the US Memorial Day holiday in May 2025 and declines into the US Labor Day holiday beginning September 2025. Such a double top could be at about 4.80% (YTD high) or 5%. (Oct 2023 high). The primary difference is the tide. Now is a secular bear market while 2016-2017 was a secular bull market.

After the 2024 US election, 10y yield dipped, then broke out higher rising 64bps…

After the 2016 election, 10y yield rose 85bps to retest a key high in Sept 2014…

AND we pause and acknowledge today in history, 5yrs ago with a relationship TO this past Friday …

… Five years ago today, global markets first began to panic after a weekend that saw 11 Italian towns emerge from it in Covid lockdown. Five years later we had a mini panic on Friday as attention focused on a report earlier in the week about a new coronavirus discovery in bats, from the infamous Wuhan lab, with similar properties to Covid-19. Note there has been no reported transmission to humans as yet and as far as we know it's just been found in a lab. We're all probably paranoid and it's difficult to know what to do with that information but ahead of a weekend, and with memories of that fateful weekend five years ago, it was no surprise people wanted to lighten up with the S&P 500 (-1.71%) seeing its worst day of the year so far, extending declines after earlier stagflationary data that we'll discuss at the end. In overnight trading, US stock futures are back up with those on the S&P 500 (+0.49%) and NASDAQ 100 (+0.48%) higher….

Friday's data on consumer inflation expectations showed the highest reading in three decades. However, these data have been volatile and subject to additional uncertainty given a methodology change. Moreover, this rise has not been uniform across measures of inflation expectations. To get a clearer read on the trend, we update our common inflation expectations (CIE) index, which is modelled after the Fed staff’s.

Our updated CIE showed inflation expectations were near pre-2014 averages at the end of 2024. However, the recent upturn in some measures of inflation expectations has lifted the CIE to 2.18%, its highest reading since late 2023. Indeed, excluding the post pandemic period, the CIE is the highest since 2008.

With the inherent uncertainty around the ultimate impact of tariffs, economic agents’ inflation expectations will be a key touchstone for the Fed. To the extent that they remain steady, the Fed may be able to respond to the downside growth risks from tariffs as they did in 2018. However, this ability would be significantly curtailed should inflation expectations drift higher and begin to show signs of unanchoring.

… and not THE bank of the land but from the best bank CEO in the land …

The minutes of the January FOMC meeting suggest the Fed retains an asymmetric easing bias. Further, the minutes highlight the risk of an earlier QT termination than both we and consensus forecast. Secretary Bessent’s comments also helped anchor intermediate yields by reducing WAM extension concerns

With OIS forwards pricing a Fed path that’s close to our forecast and yields at the lower end of their recent ranges, we do not recommend duration longs here. However, we look to add should 2-year yields retrace closer to the middle of the Fed funds target range

Recent commentary and actions from the Treasury Department warrant a lower term premium. However, our term premium proxies have unwound nearly half their rise since the fall and we do not recommend chasing this trend. Instead, we would look to fade a further compression in term premium, as we continue to think the growth of the Treasury market, against the backdrop of a sharp structural shift in the demand for Treasuries, should drive term premium higher over time…

…As we look ahead, the Fed’s asymmetric dovish bias should continue to act to dampen volatility and anchor Treasury yields, and in this context it’s no surprise that range vol at the front end of the Treasury curve has declined to the lowest levels since the fall of 2021 (Figure 13With eFdonlbut reaingdovsh bia,rnge volhasdecin tomuli-year lows,anchorig Teasury ields.). Despite this backdrop, we do not think valuations support duration longs at the front end in the current environment: OIS forwards are now pricing in a full 25bp cut by the July FOMC meeting and 47bp of easing this year, and 2-year yields are trading at the lower end of the range they have held since the Fed’s last ease in December (Figure 14.but yieldshav eclindto helwrnd oftheir cntaged wontfavr longsher). Thus, we do not recommend duration longs here, but would look to add should 2-year yields retrace back closer to the middle of the Fed funds target range.

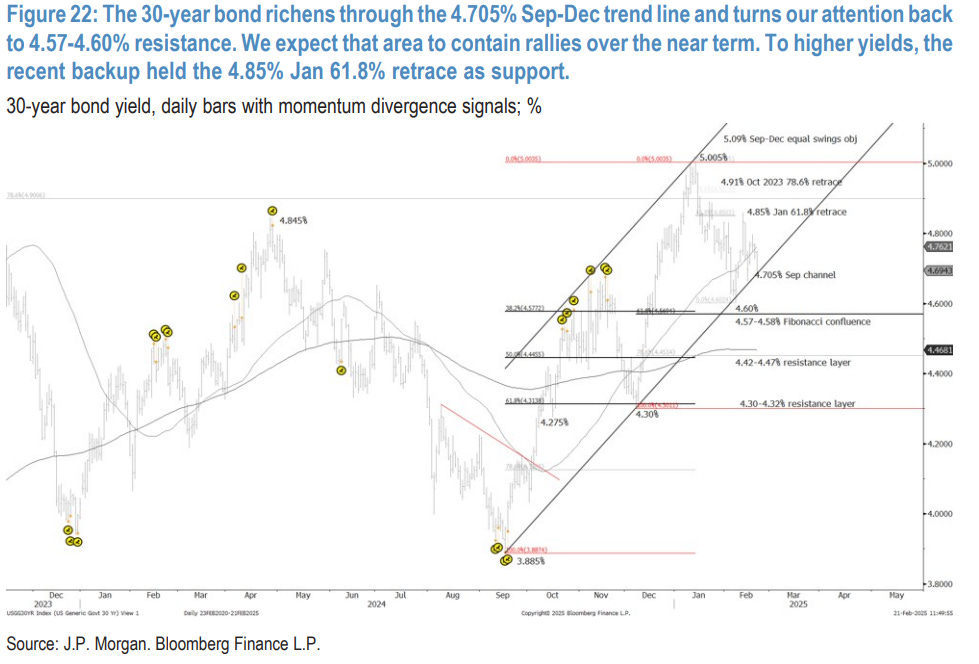

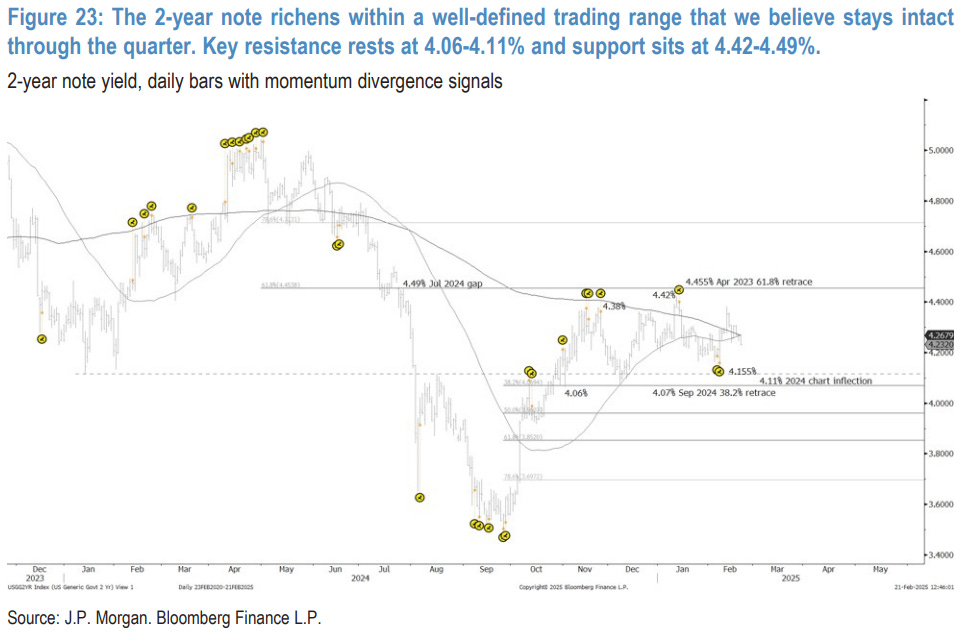

…Technical Analysis

A mix of economic data keeps the Treasury market range in February. The 30-year bond rally through 4.705% Sep channel resistance opens the door for a retest of the 4.57-4.60% resistance zone. We believe the rally will fade there, but need to see the expected technical conditions come together as the market reaches that resistance before we would suggest fading the move...

… The front end has a more well-defined trading range with key resistance at 4.06-4.11% and support in the 4.40s…

Ever ask, WHY we’re so consumed with immigration? Welp …

Restrictive immigration policies are an underappreciated risk.

For US economic growth, immigration policy deserves more attention, even as tariffs have dominated the headlines, fiscal policy is being debated in the Congress, and deregulation has yet to take shape. Net immigration surged in 2023 and 2024, allowing substantial GDP growth and yet falling inflation. As labor force growth outpaced employment gains, wage and price pressures moderated. Immigration had peaked and was slowing, but the new restrictive immigration policy is set to accelerate that decline and pose downside risks to growth and upside risks to inflation.

Last week, our US economics team laid out a framework for analyzing immigration. Using data on different types of immigration, including unauthorized admissions, we estimate that net immigration will slow from 2.7 million in 2024 to about 1mn this year, and 500,000 next year.

This slowdown in net immigration will damp growth, boost inflation, and present a thorny choice for the Fed. Based on the last couple of years, we think it is clear that the supply effects have outstripped the demand effects. This view is corroborated by the fact that immigrants on average are younger, lower income, and have higher labor force participation and employment rates. Relative to no change in immigration, our baseline assumption of 1mm in net migration this year could reduce the level of real GDP by 0.4-0.6pp this year and next. Given the uncertainties in forecasting, our US team also presents a scenario where net migration falls closer to zero, where the level of real GDP would be a full percentage point lower than our baseline….

Same shop with an equity preview …

MS: US Equity Strategy: Weekly Warm-up: The Debate Turns to Growth

The lagged impact of elevated back-end rates coupled with tariffs, new immigration policy and DOGE are clouding the growth backdrop. Quality remains our preferred hedge against this uncertainty. Consumer Services performance has been strong relative to Consumer Goods, and we expect this to continue…

… However, recently, the 10-year yield has fallen below 4.50%, and yet that ~6,100 resistance level has continued to hold back the index as well as lower quality and expensive growth stocks. We think this more recent development is due to the reason why rates are falling—softer growth prospects alongside limited progress on inflation which is preventing the Fed from cutting more aggressively than assumed just a few months ago. This also fits with our long-standing belief that rate sensitivity for stocks would decrease if the 10-year yield were to settle below 4.50%. In line with our view, yields ended Friday at 4.43% and the equity return versus bond yield correlation entered positive territory for the first time since early/mid December. Should the 10-year yield remain below 4.50%, we would expect this new correlation structure to persist, which means the return of a good is good/bad is bad environment from a growth standpoint. As we alluded to above, an important dynamic at play here is the reflexive, lagged impact of higher rates on growth. As Exhibit 2 shows, rates have tended to lead economic surprise by 60 days. Thus, the upside in yields we saw from mid-September to mid-January is having a lagged effect on economic surprises and earnings revisions…

AND finally, Dr Bond Vigilante economic week ahead …

The week ahead will feature Nvidia's earnings report after the market closes on Wednesday. That may be more important to the stock market than any of the economic indicators to be released during the week. Last week, Elon Musk's artificial-intelligence startup, xAI, unveiled its latest AI model, Grok 3, claiming it outperforms DeepSeek and OpenAI models across various benchmarks. The firm utilized 200,000 GPUs to run the model! That suggests that the demand for Nvidia's number one product remains strong …

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

Positions are important … and one component OF them is supply vs demand dynamics and on that note, a few words …

02/20/2025 09:28:00 [BFW] Bloomberg First Word Bloomberg: The Treasury Market Has a Demand Problem: MacroScope By Simon White

(Bloomberg) -- Deficits, inflation, political uncertainty – whatever you want to pin the blame on, US Treasuries look like they have an increasingly entrenched demand problem.

It wasn’t supposed to be like this. Buyers that can normally be relied upon to step in to the Treasury market when the yield curve disinverts have not so far done so to a meaningful degree. Two immediate impacts are structurally higher yields, and a greater risk of funding flare-ups as primary-dealer balance sheets become more congested with unsold Treasury inventory.

The tranche of securities accumulated on dealer balance sheets – the bulk of which are Treasuries – has risen to all-time highs in outright terms and relative to the financial assets they hold.

…Foreigners are losing their appetite for Treasuries — specifically, foreign central banks. Official holdings of Treasuries relative to the total outstanding have been in a steady decline since the GFC, the pace of which picked up after the pandemic. Private holdings of USTs, on the other hand, remained roughly stable until early in this decade, rising only marginally over the last three years.

Private foreign holders of Treasuries recently overtook official holders relative to the total debt outstanding, based on the TIC data. The question is: will private holders be able to keep taking up more slack when many emerging market countries are less willing to hold Treasuries, and many developed countries have significant borrowing of their own to undertake? With fiscal deficits around the world still elevated and Europe’s defense spending about to swell, it seems more unlikely each day…

… Once again all roads lead back to DOGE. If it can achieve meaningful savings, at the margin this may encourage some buyers to buy more US sovereign debt. But with expected odds barely more than one-in-three that the department can cut at least $250 billion in the budget this year – still barely a pinprick in the deficit – the Treasury market is likely to have a demand problem for a while yet…

ALSO from The Terminal, continued evidence that HOPE springs eternal …

Bloomberg: Fed-Favored Inflation Gauge Is Set to Ease to Seven-Month Low

Euro area’s top economies also publish consumer-price numbers

South Korea central bank to cut rate, Israel predicted to hold

The Federal Reserve’s preferred inflation metric is expected to cool to the slowest pace since June, but glacial progress on taming price pressures overall will keep policymakers cautious about lowering interest rates further.

The core personal consumption expenditures price index — which excludes often-volatile food and energy costs — probably rose 2.6% in the year through January in Commerce Department data due on Friday. Overall PCE inflation likely eased on an annual basis as well, according to the median estimate in a Bloomberg survey of economists.

The decline will probably come from categories that were relatively tame in separate wholesale inflation data that feeds through to the PCE, according to Bloomberg Economics. But components that registered strong increases in the consumer price index will keep the PCE running above the Fed’s 2% target…

Positions are important and another aspect to be aware of is that they are getting longer of the long end the curve … Longest, in fact, since March … of 2018 …

Hedgopia CoT: Peek Into Future Through Futures, How Hedge Funds Are Positioned