Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

First UP, calling all of Team Rate CUT … This note contains an update from none other than Apollo Global’s (and former DB stratEgersit) which you’ll want to read, IF you hadn’t already.

…The incoming economic data remains strong. But… -Torsten Sløk, Apollo Chief Economist

Scroll down for the link IF you’ve not already subscribed. When the facts change, something something … a good read, pictures included but the change of tone is what should catch the attention.

THEN while you are ‘down there’ in the section of this weekends note, kindly find an updated note and visual of 10s from Bloombergs own Ed Bolingbroke who mentions a story from the SCMP detailing a NEW virus and as he says, as this report circulated, it added TO (flattening)bid for USTs … I’m dismayed BUT …

SCMP: Chinese team finds new bat coronavirus that could infect humans via same route as Covid-19 Research was led by Shi Zhengli, a virologist known as the ‘batwoman’, who is best known for her work on coronaviruses at a lab in Wuhan Published: 9:00am, 21 Feb 2025|Updated: 9:20am, 21 Feb 2025

AND for more …

ZH: China Reports New Coronavirus 'With Pandemic Potential' Discovered

Whether or not this was all / some / NONE of the actual reason for the price action (stocks, bonds, commods) Friday, well, the truth is I’ll never know.

I USED to be in a seat where I’d have seen / heard / talked with asset managers in REAL TIME and gotten read from them IF it was driving their buy / sell decisions and then I might have had more of a comment.

At this point, well, as an arm-chair QB … I do not…Worth noting as I begin this weekends journey, though and so, I’ll move on …

Moving on to the PRICE ACTION and specifically some interesting price / yield developments out the curve. Now, this may make more / less <please choose one> sense ahead of the supply in the week just ahead where we’ll see $69bb 2s (MONDAY), $70bb 5s (Tuesday) and followed up by $44bb 7s (Wed) with accelerated schedule due to month end Friday.

That 4pm close Fri (which again, is the not-so-new 3pm) will bring with it commensurate duration needs and with those in mind, a picture of 30s which speaks to me …

30yy DAILY: 4.70 (up)TLINE broken …

… momentum ALSO turned decisively bullish (albeit from underwhelming levels which wouldn’t have presented themselves as a dipORtunity…) and from here, 4.60 and 4.50% (psychologically important round numbers) would seem attainable if …

30yy WEEKLY: break FAR LESS CONVINCING and so, i’ve not yet turned the TLINE GREEN (as above on the daily…)

… momentum here REMAINS BULLISH and another WEEKLY close here / lower would be far MORE convincing …

… How / WHY might rates continue to trend lower / curve flatter in to the week ahead?

Stocks.

(new)Virus.

(front-end)Supply.

Many continue to adjust / modify forecasts and are NOW becoming bearish (as one of the more prominent economic optimists NOW acknowledging some weakness … )

A most funTERtaining setup and so, I’ll quit there AND in as far as some of the impetus TO the price action …

ZH: US Services Sector PMI Plunges Into Contraction For First Time In 2 Years

ZH: US Existing Home Sales Plunged In January As Mortgage Rates Rose

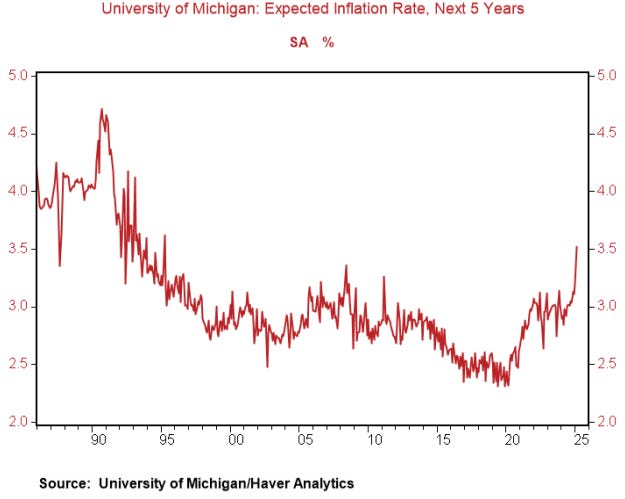

ZH: UMich Inflation Expectations Explode To 30 Year High

… Consumers said they expect prices will climb at an annual rate of 3.5% over the next five to 10 years, according to the final February reading from the University of Michigan. The rate is the highest since 1995, based on data compiled by Bloomberg. All five components of the index deteriorated, including a drop in buying conditions for big-ticket items. And more than half of consumers in the survey expect the unemployment rate to rise over the next year, the highest since 2020.

Interestingly enough, and perhaps a sign of how America’s furious polarization may in part tinge economic attitudes, the spike was almost entirely driven by views among survey respondents who identify as Democrats.

Nevertheless, inflation expectations have taken on renewed importance as the prospect of trade wars is weighing on the outlook for prices paid by consumers. Economists have warned that, while Trump has only followed through on one of his tariff threats (against China), the threats themselves are hurting the economy by creating uncertainty …

… Alrighty, then.

I’ll move on TO some of Global Walls WEEKLY narratives — SOME of THE VIEWS you might be able to use. A few things which stood out to ME this weekend from the inbox

Here’s a look at the economic week ahead from a UK based shop…

… US Outlook 3.5 will turn heads at the FOMC Longer-run inflation expectations jumped to 3.5%, their highest level since 1995, and surveys point to some cooling in activity, on tariff fears. This complicates the FOMC's policy. The minutes of the January meeting indicate that participants are in no rush to adjust the policy rate.

In the week ahead, we’ll remain bullishly inclined toward the Treasury market as month-end comes into focus…Let us not forget that the January core-PCE print will cap the week and given the emphasis on the trajectory of inflation, one would be remiss to completely ignore the release – although the accuracy of the projections this far into the data cycle implies that it will be either a 'high' 0.2% or a 'low' 0.3% … With 10-year yields pushing toward the bottom of the range, it will be telling the extent to which the 4.40% level holds, or if investors are willing to push rates back toward the 200-day moving-average of 4.246% …

…Trading View Our short position in 5-year breakevens (entered 2/19 at 268 bp) has been trading in-the-money, and our initial target is set at the month-end close from January 31st at 260 bp, a level that aligns with the origination of the NFPinspired widening in 5-year breakevens…As for our other trades, our long position in 2-year notes (entered 2/12 at 4.36%) reached our target of 4.20% on Friday, and we were content to book profits and move to the sidelines….

… and for the AUDIO version, check out pod version HERE(or where ever it is you listen to those …), “A very long 28 days...”

…Episode 312: "Dodgin' the DOGE" is now available. This week, the team discusses the eventual end to QT as well as the potential revisions to SLR. We also consider the logical extension of Trump's pursuit of government efficiency and the implications in the event that such a sentiment spills over into the private sector.

Moving right along, some updated weekly thoughts from a former Bear Stearns economist who’s now with Brean …

In the attached Weekly we discuss what it means for monetary policy to be in a good place and what might cause policy to change down the road. We examine an inflation claim from the FOMC minutes and then three speeches/essays from Presidents Bostic and Musalem and Governor Kugler…

… So monetary policy is in a good place and on hold, for now. What would change that? The answer has to be the data but which data and how will the Fed respond to the data? Yesterday we had two thoughtful papers by these two Fed Presidents and a third fascinating and long lecture by Fed Governor Adriana Kugler with the intriguing title Navigating Inflation Waves: A Phillips Curve Perspective. It is worth digging into these papers because they represent thoughtful perspectives in monetary policy and inflation, while all containing the same baseline assessment that inflation is expected to return slowly to 2%. None of the papers, however, provide the support for this assertion but this is okay because none of the policymakers are arguing that policy should be adjusted until these hopes are validated…

…Hope is Okay if the Assessment of the Data is Honest…

…Today, the University of Michigan published the final estimate of medium-term inflation expectations held by consumers, which increased to 3.5% from 3.2% in January, which is the highest inflation expectation since April 1995. One would assume that Musalem is now more concerned about inflation expectations becoming unmoored and that if Bostic was giving his speech today, he might have made less sanguine comments on inflation expectations.

Turning TO Germany (unrelated to elections) for this next update on FLOWS … noteworthy given CALL VOLUMES …

What stood out this week: Equity positioning remains in an elevated but not extreme range (z score 0.68, 86th percentile); however, net call volume climbed taking the put/call volume ratio to late 2021 pandemic equity boom levels; heading into NVDA’s earnings release next week, positioning in mega-cap growth and Tech remains very elevated (97th percentile) and well above levels implied by earnings growth; the sharp rally in European equities over the last 5 weeks has seen another big fund inflow ($4bn), the largest since early 2022; in China (-$4.9bn) on the other hand, an even stronger rally has seen large fund outflows for a second week in a row; CTAs covered their short in EM equities and turned slightly long, they remain very long US and European equities; S&P 500 buyback announcements continue to climb, running at $340bn over the last 3 months.

AND an updated / CHANGED call caught my attention …

We've taken a cold look at our 5.5% call for the US 10yr and have on balance decided to trim it, to 5%. A combination of Doge, Bessent and talk of SLR adjustment(s) have managed to tame the prior de-rating of Treasuries versus the risk free rate. As tempting as it sometimes is, we can't blame everything on Donald Trump. So we won't. Some of this is actually good

Doge, Bessent and SLR talk contribute to a taming of extent of likely Treasury yield rises ahead

We don’t make calls on politics. But politics absolutely impact our calls on rates. When Donald Trump was elected president of the United States it marked a seismic shift, versus the previous regime, and even relative to the first Trump one. Once the dust settled on the outcome, we posed the question (here) – “Can the US 10yr yield top 5.5%?”. We answered “yes”. Of course it still could, but we’ve decided to tame the call to 5% area, removing 5.5% as the official call for end-2025.

We’ve done that for a two main reasons, and one minor but important one.

First, the Department of Government Efficiency; the doge-tracker.com site has logged US$55bn of “tax dollars saved” so far, 2.75% of the US$2tn goal. While it is true that we knew about doge beforehand, what we did not anticipate was the intensity of its application. It remains unclear how realistic the doge spending cut goal is. But still, it can’t be ignored as something that could help contain the fiscal deficit, and by extension Treasury issuance requirements.

Second, we can’t ignore Treasury Secretary Bessent’s remarkable laser focus on the 10yr yield, and his suggestion that it’s this rate that the Trump administration would like to get lower. While Bessent cannot control the 10yr yield per se, it’s clear that he has an overt ambition to get it lower. All Treasury Secretaries would of course like to have as low a 10yr yield as possible, but few have been as vocal as Bessent on it. Leaving the funding profile front-end-heavy reflects the same.

Third, potential adjustments to the supplementary liquidity ratio, in particular with reference to inclusion of Treasuries in the measure. During the pandemic the Fed implemented a temporary rule allowing banks to deduct Treasuries from their SLR calculation. Although since reversed, recently Chair Powell has voiced an openness to making such an adjustment again, but this time more permanent. This would free up balance sheet at banks, ultimately adding to liquidity in US Treasuries. And that in turn helps Treasury yields to trade lower than they would otherwise.

Treasuries have been re-rated versus the risk free rate

Source: Macrobond, ING estimates…

…That said, we're still structurally bearish on Treasuries. Now targetting the 5% area …

… bearish but not SO bearish? Okie dokie. Noted and moving along …

A global MACRO (daily) note from a better-than-average shop with great content…

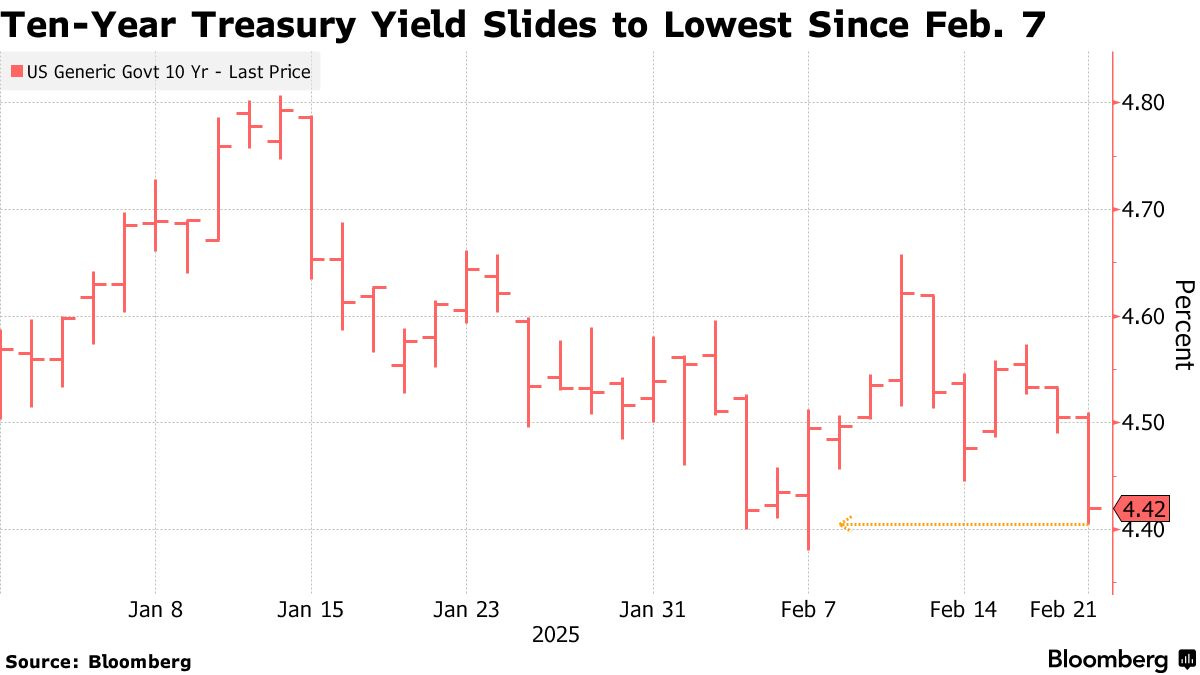

Risk-off environment sends US equities lower; soft economic data and safe-haven bids support USTs; JGBs rally after BoJ's Ueda's remarks; miss in France PMI; BoC's Macklem warns of economic impacts from tariffs; CGBs sell-off as local equities gain; DXY at 106.65 (+0.3%); US 10y at 4.431% (-7.4bp).

Risk-off sentiment overtakes the market with the S&P 500dropping -1.7% lower amid concerns around consumer demand, inflationary pressures, and a potential new virus.

USTs rally after an unexpected fall in the Services PMI alongside downward revisions to the University of Michigan Consumer Sentiment survey; flight-to-quality bids accelerate the rally (10y: -7bp)…

…United States: A variety of catalysts spurred a risk-off environment in macro markets with momentum sending US equities sharply lower and spurring a sizeable bid for global duration.

Government bond yields initially fell due to soft economic data. During the London session, the France Composite PMI unexpectedly fell to the lowest level since September 2023 due to a sharp decline in the Services PMI which fell to the lowest level since November 2020. Although the weakness in France was offset by strength elsewhere in Europe, which kept the Euro Area Composite PMI steady, momentum in Europe remains weak. Accordingly, European duration rallied alongside declines in EUR.

The bull-flattening in USTs continued overnight, as yields fell alongside the rally in bunds. The rally accelerated after the US Services PMI unexpectedly fell and optimism about the coming year fell sharply. The PMI report noted that the deterioration in February was primarily a reflection of "increased uncertainty about the business environment, especially in relation to federal government policies related to domestic spending cuts and tariffs." Additionally, concerns around higher prices were also cited as a factor in the decline.

Final University of Michigan Consumer Sentiment data painted a similar story. Consumer sentiment was revised down to 64.7 (Preliminary: 67.8; January: 71.1), while 5-10y inflation expectations were revised up to 3.5% (Preliminary: 3.3%; January: 3.2%), the highest level since 1995.

Treasury yields fell sharply following the data releases amid concerns around the US economic outlook alongside potential price pressures that could weigh on consumers. These concerns also weighed on US equities with consumer discretionary stocks continuing their decline.

The risk-off behavior accelerated in the NY afternoon which some attributed to reports around a potential new virus. US equities continued to fall throughout the NY session, as safe-haven bids supported USTs. Momentum ahead of the weekend and positioning adjustments likely accelerated these moves. Ultimately, the S&P 500 fell -1.7% in its worst session of 2025. All major sectors aside from consumer staples ended the day in the red.

USTs ended the session ~7bp lower across the curve, while STIR pricing pulled forward cuts implying an additional ~6bp of Fed easing in 2025. The risk averse price action also resulted in a bid for the USD with the DXY USD Index up 0.3% d/d….

The deadline is approaching for a potential government shutdown. We expect a shutdown would lead to ~0.1pp per week direct drag on quarterly annualized real GDP growth, but this should reverse once the shutdown ends. The debt ceiling will also be topical for QT.

Key takeaways

Congress needs to pass either a continuing resolution or full-year appropriations in the next few weeks to avoid a government shutdown.

Federal furloughs of nonessential employees during a shutdown would have direct drags on 1Q real GDP growth, with potential indirect impacts as well.

For the debt ceiling, we expect the X-date in 3Q, though this is uncertain. The Fed minutes give us more confidence in our base case for QT to end in June.

Another note from the UK caught my attention given a ‘forecast update’ … just in time, too where those who have been more ‘bearish’ or optimistic on the economy are just NOW changing tune (Apollo) and evidence of another virus popping up in conversations … IF it weren’t for bad timing, I’d have none at all. Good to see I MAY not be alone??

…US Rates: We think that current market pricing underweights scenarios in which the Fed is obliged to defend its inflation mandate. We are changing our US rates forecasts to reflect a higher probability of a scenario in which sticky inflation and above trend growth prevent the Fed from easing further and increase the odds of a hawkish change in bias. While the hurdle for actual additional tightening is quite high, Fed guidance along the lines of “current conditions do not warrant further easing” would be sufficient commentary to re-shape the probability distribution of short rate outcomes away from further easing, and toward tighter policy…

…In our forecasts, we have imposed a flattening bias on the term structure. In our view, this is consistent with a Fed that is defending its inflation mandate, and with investors enhancing returns by “monetizing” the term premium via extending Treasury holdings out the curve. Specifically, we have flattened our empirical term premium proxies by 1.5 monthly standard deviations (about 30 bp) for the end of Q3 and have then allowed a modest retracement at Q4 2025. In our forecasts, 2s10s re-flattens but does not invert, while 5s10s, 5s30s, and 10s30s invert in the back half of the forecast window. The maximum inversion in 5s30s is -25 bp at the end of Q3, which is consistent with past seasonal curve behaviour.

… just in time, too where those who have been more ‘bearish’ or optimistic on the economy are just NOW changing tune (Apollo) and evidence of another virus popping up in conversations … IF it weren’t for bad timing, I’d have none at all. Good to see I MAY not be alone??

“The Gunfight at Dodge City” is a 1959 Western film. After his brother the sheriff is murdered, Bat Masterson is elected to the job of sheriff and is determined to find the killer and make Dodge City safe. Today, there are gunfights going on in DOGE City to restore law and order to fiscal policy. Will the new sheriff in town get the job done, or will the Bond Vigilantes do it?

The Department of Government Efficiency (DOGE), led by Elon Musk (who reminds us of a superhero on a mission to save humanity), is scrambling to uncover waste and fraud in the federal government. That should be easy. The question is whether he and his team—a.k.a. the DOGE Boys—can find enough waste and fraud to make a big difference to the federal budget outlook if eliminated.

The reason the boys are scrambling is that the Democrats are regrouping and coming to DOGE City for a gunfight. The Democrats have rounded up a posse of Democratic district attorneys from all around the country to stop Musk’s muckrakers by filing motions in courts to block them from raking the muck they find.

Treasury Secretary Scott Bessent probably also alerted the DOGE Boys that the Bond Vigilantes might be coming to DOGE City for a shootout if the Trump administration doesn’t convince them there’s no need for a gunfight because the President will deliver fiscal discipline and resist telling the Fed to lower interest rates.

After all, the Fed did lower the federal funds rate (FFR) by 100bps from September 18 through December 18 last year, but the Bond Vigilantes immediately expressed their dismay that monetary policy was stimulating an economy that didn’t need to be stimulated and enabling fiscal excesses. They did so by pushing the bond yield higher by 100bps (Fig. 1 below). In the past, the Fed lowered the FFR from cyclical peaks because the peaks were followed by recessions (Fig. 2 below). There has been no recession this time.

Figure 1

Figure 2

Now, consider a few of the recent developments that led up to the trouble brewing in DOGE City:

(1) Summer 2024. Elon Musk floated the concept of DOGE in discussions with Donald Trump during the summer of 2024 as the then-former President campaigned for a second term. In an August campaign event, Trump said that, if elected, he would consider giving Musk an advisory role on how to streamline the government. Musk immediately tweeted, “I am willing to serve.”

(2) October 27, 2024. Elon Musk first declared that DOGE would cut $2 trillion from the federal budget on October 27, 2024, during a Trump rally at Madison Square Garden. Over the 12 months through January, the federal government’s budget deficit totaled $2.14 trillion (Fig. 3 below).

Figure 3

…There is lots of pushback by Democrats, who are challenging the legality of the DOGE Boys’ flipping through government files. Douglas Holtz-Eakin, who had served as the director of the Congressional Budget Office, compared DOGE to the former Grace Commission, which had zero of its 150 proposals enacted.

… Moving along TO a few other curated links from the intertubes, which I HOPE you’ll find useful …

First UP, an important tenor change from one of the more optimistic out there …

The incoming economic data remains strong. But we are starting to worry about the downside risks to the economy and markets from: 1) the impact of DOGE layoffs and contract cuts on jobless claims and 2) persistently elevated policy uncertainty weighing on capex spending decisions and hiring decisions.

Specifically:

1) The consensus expects total DOGE-related job cuts to be 300,000, and the number of people filing for unemployment benefits has been rising in Washington, DC, but not in Virginia, Maryland, and Washington, DC combined, see the first two charts. Total employment in the United States is 160 million, with 7 million unemployed. Also, about 5 million people change jobs every month. In that context, 300,000 federal jobs lost is not much. However, studies show that for every federal employee, there are two contractors. As a result, layoffs could potentially be closer to 1 million. Any increase in layoffs will push jobless claims higher over the coming weeks, and such a rise in the unemployment rate is likely to have consequences for rates, equities, and credit.

2) Credit spreads have not responded the way they normally do to rising policy uncertainty. Economic policy uncertainty is spiking higher, but credit spreads are not widening, see the third chart. The question is if persistently elevated policy uncertainty will begin to have a negative impact on capex spending and hiring decisions.

The bottom line is that the incoming data remains strong, see the fourth chart. But the near-term downside risks to the economy and markets are growing.

Our chart book with daily and weekly indicators for the US economy is available here.

Positions. Lives. Matter. None other to refresh and reread than EBB. This weekends link actually dropped into inboxes last night and … unfortunately … is the first time I’ve read / seen / heard of a new <gulp> virus …

Bloomberg: Surge in US Treasuries Sends 10-Year Yields to Two-Week Low

Ten-year yield declines as much as 10 basis points on Friday

Traders eye weak economic data, report on a coronavirus study

A late rally in the US Treasury market on Friday pushed the yield on 10-year notes lower for a sixth-straight week as traders hunt for safety ahead of next week’s $183 billion auction slate and a reading of the Federal Reserve’s favored gauge of inflation.

The yield on 10-year notes declined in Friday afternoon trading in New York by as much as 10 basis points after unexpectedly weak economic data and an uptick in consumers’ long-run inflation views to the highest since 1995. The moves extended and stocks fell as an earlier South China Morning Post report on a new bat coronavirus study made the rounds with traders.

On a Friday afternoon, the circulation of that report “is sparking some safe haven and risk reduction,” said Brad Bechtel, global head of foreign exchange at Jefferies.

The 10-year yield on Friday fell as far as 4.4%, the lowest since Feb. 7, before slightly paring the move. It’s on pace for a sixth-straight week of declines. The Bloomberg Dollar Spot Index was higher by 0.2%.

Traders also priced in more interest-rate cuts by the Fed this year, putting approximately 28% chance of a 25-basis-point reduction in May compared to 16% priced at Thursday’s close. They’re now pricing in the central bank’s first 2025 cut in July rather than September.

More from The Terminal.com

Bloomberg: Steve Cohen ‘Negative’ on US Economy, Citing Tariffs and DOGE

Bloomberg: Pimco, Allspring Bet on Mortgage Bonds That Look Cheaper Than Corporate Debt

From the man who invented the bond market vix (aka MOVE index) … a few thoughts on duration and convexity … not 100% sure if I’d have gone with this opening picture but it does make some amount of sense…

In 1938, Frederick Macaulay (1882 – 1970) solved an actuarial problem that bedeviled insurance companies for centuries: How does one efficiently balance the maturity gap between their assets and liabilities ?

An actuary’s job is to estimate when the company might have to make a payout (liability) and then advises which bonds (assets) to buy to match. Macaulay optimized the process by calculating the weighted average time until a bond’s cash flows are received; he called it “Duration” and it is measured in years.

Bond traders had “Ozempic moment” when they realized that “Macaulay Duration” had a more useful purpose; it could be a proxy for how much a bond’s price would move given a one-percentage point change in interest rates. The price of a 4.5% ten-year bond (with a Duration of 8) would increase from 100 to about 108 if interest rates declined from 4.5% to 3.5%…

…NOTE: The only Wall Street book I recommend is: “Inside the Yield Book” (1972) by Sidney Homer and Martin Leibowitz; the Salomon Brothers gurus who preceded the infamous characters of Michael Lewis’s “Liar’s Poker” (1989). It is the bond bible, and is a must read if you want a job in finance…

…Concurrently, the recently issued -rautini line- UST 30yr bond was trading near a price of 102 in early 2020. At the peak of the panic, this bond touched a price of 135, a 32% price jump. The shorter Duration UST 10yr rallied nearly 15%.

This is the reason thoughtful portfolio construction concentrates on Duration and will often increase the Duration allocation as a risk shock absorber.

…The Macro View and Concluding Comments It is said of President Trump to take him “seriously, but not literally”; and we will soon see if this is the case. I will say I do not know if changes to Tariff and Tax (personal and corporate) policies are bullish or bearish; in fact, it is unclear if one buys or sells a Constitutional Crisis (such as it is).

But what I know for sure is that if the US Government tries to deport more than the perhaps 75,000 illegal immigrants who have been convicted of a crime since 2017, we will have a hard landing, period.

No matter your politics, we should all agree that there is a strong link between the number of workers and GDP; and fewer workers means lower GDP.

Separately, I am still orthogonal to Team Transitory (kisses to @profplum99) as I am with Jim Bianco in the “higher for longer” camp. As detailed prior, the demographic of Millennials spending more to support their families juxtaposed with Boomers retiring early will thwart the FED’s hopes for lower inflation.

This opinion does not contradict the prior 7 pages, rather I will say the Bond Bull is simply a more efficient manner to access Duration.

The Bond Bull is the “151 proof” of duration assets; a 15%-dollar allocation will match the duration of the Aggregate Bond Index.

Instead of the standard 60%/40% portfolio, consider 70% stock, 10% Credit, 10% Commodities, and 10% the Bond Bull.

For Hedgers, one should use the Bond Bull not because you know rates will decline, but rather because you are bearish, and might be wrong.

Remember: For most investments, sizing is more important than entry level.

Harley S. Bassman February 19, 2025

TIME they say, is of the essence. It was always and remains MY view that it’s the most under appreciated commodity of all time. Perhaps that is changing and is getting recognition it deserves … whether this should leave with a thought on BUFFETS NET WORTH, well … that remains up for debate but …

First Trust: Three On Thursday - Time: Our Most Precious Asset

William Penn, the Quaker leader and founder of Pennsylvania, saw time as a divine gift—precious yet often squandered. In 1693, he captured this wisdom in Some Fruits of Solitude, a collection of reflections on life and virtue, where he famously observed, “Time is what we want most, but what we use worst.” In an era where life was uncertain and often brief, his words served as a call to live with intention. Today, they remain just as relevant—while we constantly wish for more time, it is finite. In this edition of “Three on Thursday,” we examine different aspects of time…

…Warren Buffett’s Net Worth

It’s not about timing the market—it’s about time in the market that truly matters. This often surprises people, but Warren Buffett didn’t become a billionaire until he was over 50. Today, his net worth is around $150 billion, meaning over 99% of his wealth was accumulated after turning 50. Buffett started investing at just 11 years old, putting $114.75 into a natural gas company called Cities Service. His success is a testament to the power of time and compound growth. The earlier you invest, the sooner compound interest works its magic, potentially turning modest early investments into substantial wealth over time. Wealth-building isn’t exclusive to financial wizards—it’s accessible to anyone with patience, discipline, and time on their side.

This next note offers another more bearish take (higher ‘flation) which again, could very well be mis timed …

The US CPI figures for January suggest that the negative contribution from goods inflation is behind us. Going forward, we expect the US goods inflation to rise, resulting in higher US interest rates…

…Figure 2: CPI Goods and Bloomberg Commodity Index

…Figure 5: Inflation Expectation 5-10 year

… great pictures as always but … food for thought.

CHARTS and an intriguing Friday ‘speedrun’ topic / title …

Spectra Markets: Stagflation is a bad word Even a whiff of stagflation risk should make you concerned.

…Rising inflation and rising unemployment are a rare pair. Take a look at the regional Fed surveys and Prices Paid vs. Core CPI and PCE. Here are a couple of charts. We’ve got limited February economic data so far, but the Prices Paid components of the regional Fed surveys are moderately alarming:

…Interest Rates Yields are flying around and going nowhere as the upward pressure from inflationary worries is offset by downward pressure from worries about the economy. This will probably resolve to lower yields at some point, but it’s going to be messy as long as commodity prices stay up here. If commodity prices release to the downside, then yields should buckle massively.

10-year yields are testing the cloud and look ready to dump back towards 4.15%/4.20%.

This next, from the Wolf of the Street …

WolfStreet: Treasury Yield Curve Flattens as 10-Year Yield Falls while Short-Term Yields Stay Put: Fed’s Pivot to Wait-and-See in Inflationary Times. But Mortgage Rates Stay Near 7%

Long-term yields matter to the economy. So how to get the 10-year yield down? Not with rate cuts, obviously. That flopped and had the opposite effect. But with a three-pronged strategy.

Yahoo news on BUFFET …

Yahoo: Warren Buffett says Berkshire Hathaway 'did better than I expected' last year in latest letter to shareholders

…Writing in his 2024 annual letter to Berkshire shareholders published Saturday, Buffett said these record profits came despite more than half (53%) of the company's operating businesses reporting a decline in earnings last year…

…At the end of the year, Berkshire's pile of cash and other cash-like securities, such as Treasury Bills, stood at $334.2 billion, almost double the $167.6 billion seen at the end of 2023. The value of Berkshire's equity portfolio stood at $272 billion at year-end; at the end of 2023, these holdings were valued at $354 billion…

… um, so … ca$h is STILL king and getting king’ier … by the moment??

Finally, from Zero …

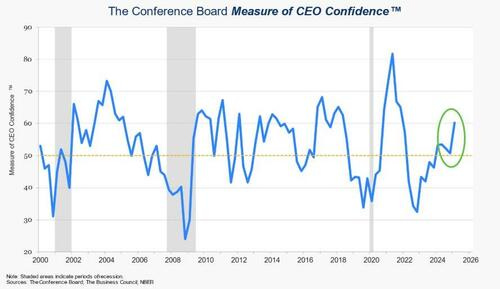

ZH: US CEO Confidence Increases Sharply From Cautious Optimism To Confident Optimism

Optimism among American CEOs surged in the first quarter of this year from the previous quarter, with concerns about various business risks easing down, according to a new survey from the think tank The Conference Board.

The “Measure of CEO Confidence,” an assessment of the U.S. economy from the perspective of U.S. chief executives, rose by nine points in the first quarter of 2025 to 60—the highest level in three years—the think tank said in a Feb. 20 statement. This is the first time since early 2022 that the index scored a value “well above 50,” suggesting that CEOs were moving away from the cautious optimism from last year to a more “confident optimism.” The survey was conducted among 134 CEOs.

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar …

A lot of great articles

Convexity Maven for one