Good morning … AND survey SAYS … a hawkish cut for US. Don’t worry, futures are STEADY this morning after ‘the rout’ — more detail on said rout below. First up, a look at front-end of the curve for some perspective as 2s are STEADY …

2yy DAILY: TLINE broken bearishly BUT …

… there may be somethin’ (bullish) happenin’ here … what it is ain’t exactly clear … BUT I can / do see front end stable, momentum (stochastics, bottom panel) rollin’ over …

… and as 2s STEADY, further out the curve a bit troubled. For a much more competent writeup and view from THE premier techAmentalists out there (CitiFX) …

Said another way …

… AND with that in mind, the conversation which is, as usual, driven by … Timiraos? Today in WSJ …

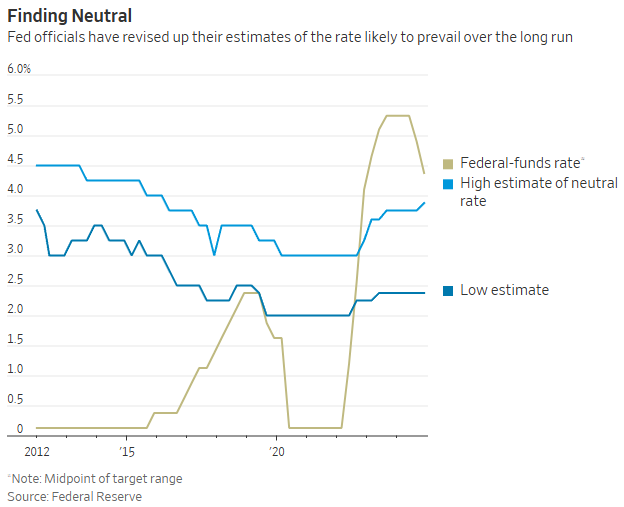

WSJ: The Next Big Fed Debate: Has the Era of Very Low Rates Ended? Fed officials are trying to figure out the just-right interest rate. Some think they might already be close to that destination. By Nick Timiraos Dec. 18, 2024 9:00 pm ET

… The debate over where neutral rests wasn’t particularly important earlier this year, because interest rates were at a level nearly all Fed officials deemed to be restrictive. That was intentional. Officials raised rates aggressively in 2022 and 2023 to lower inflation by cooling down economic activity.

But the question is front and center now because the Fed has cut rates by a full percentage point, or 100 basis points, and the economy appears to be in reasonably good shape. Like a captain who tries to avoid slamming into the dock as a boat nears its slip, central bankers could become more cautious in making cuts if they think they might be closer to their ultimate destination because the neutral rate has gone up.

“We don’t know exactly where it is, but … what we know for sure is that we’re a hundred basis points closer to it right now,” Powell said Wednesday. “From here, it’s a new phase, and we’re going to be cautious about further cuts.”

…Recent data pointing to an increase of labor productivity “signals to me that this is an economy that is fundamentally different than what was observed in the decade after the global financial crisis,” said Thomas. By next spring, more economic actors might “come to the realization that ‘higher rates were all due to the Fed’ is not a full explanation for what’s happened.”

If officials conclude that the neutral rate has moved up, then the Fed could be done cutting for quite some time, said Thomas.

“This last cut puts them low enough that they could say, ‘This might be the upper bound on where the neutral interest rate actually is, and we’ll just wait it out to see it,’” said Eric Rosengren, who was president of the Boston Fed from 2007 to 2021.

Now, is all this a giant lump of coal (Authers says YES, see below for more) OR something else? As with everything, MY beliefe is that is for you and your very own P&L to decide.

I can say specifically regarding CHART YESTERDAY — TLINE (of ‘support’) was greeted like a hot knife greets butter and there was no such thing in form of any …

… support dip buying and ultimately be the (Fed) pause that refreshes (all markets)?

… at least not here yesterday. And so, moving on TO a couple / few links for posterity sake …

BBG: Powell Signals Fed’s Focus Has Returned Firmly to Inflation

Powell says 2024 inflation forecast has ‘kind of fallen apart’

Officials’ forecasts signal just two rate cuts next year

ZH: Hawkish Fed Cut Rates As Expected; Signals Dramatically Less Aggressive Rate-Cut Cycle

WolfST: Fed Cuts by 25 Basis Points, to 4.25%-4.50%, Sees Only 2 Cuts in 2025, Sees Higher Inflation, Higher “Longer-Run” Rates. QT Continues. Energetic backpedal from the aggressive monster-rate-cut trajectory envisioned by the markets three months ago.

… Far more below but for now, keeping in mind how well global equity markets have done YTD, and so to say there’s plenty of profits still to be booked IF / when Global Wall (sell AND buy side) agree it is time.

Look out below?

… A couple / few other links of the day that was …

ZH: Renter Nation Returns? Multi-Family Building Permits Soared In November

… housing, schmousing as the dust settled from JPOW & Co …

NEWSQUAWK: US Market Open: US equity futures gain, DXY gives back some of post-FOMC strength, JPY hit post-Ueda … US yield curve steepens, JGBs outperform post-Ueda, Gilts lag pre-BoE.

Yield Hunting: Daily Note | December 18, 2024 | TSI Special, Muni NAVs Decline/Buy Ideas, PCF

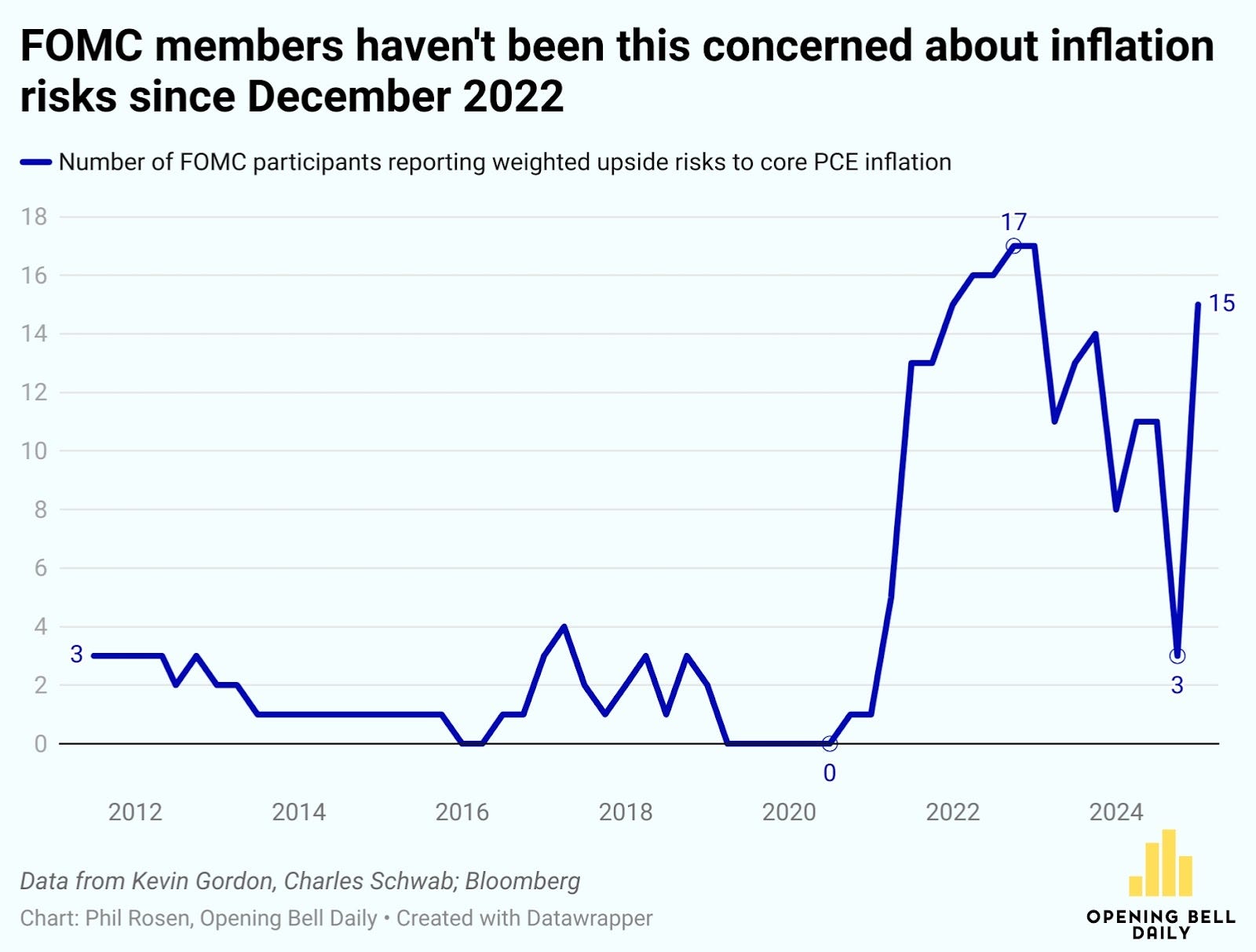

… Meanwhile, the number of FOMC participants who reported seeing upside risks to inflation rose from three to 15, according to data from Charles Schwab strategist Kevin Gordon.

Not only is that the highest number of concerned members since December 2022, but it’s the biggest-ever jump from one meeting to the next.

“Members of the FOMC have resorted to the fact that the inflation beast will be a bit tougher to slay,” Gordon told me after the press conference. “In the context of relatively strong growth, that isn’t a bad thing, but it was bad enough news to tip the market over — mostly because of how frothy sentiment was heading into the decision.”

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ … mostly today you’ll find a variety of recaps, victory laps and I told ya so’s …

I’ll begin with …

BARCAP Federal Reserve Commentary: December FOMC: Phase 2 and a hawkish cut

The FOMC cut rates 25bp and signaled a slower pace of rate cuts ahead, suggesting a likely pause in January. The SEP shows two rate cuts in 2025, two more in 2026, on significantly higher inflation projections and a slightly stronger growth and labor market. The median dots now align with our call.

… We retain our baseline projection that the FOMC will cut rates only twice, by 25bp, next year, in March and June, with core PCE inflation rising again in H2 25 amid increased import tariffs and tighter immigration restrictions. We then expect the FOMC to resume its rate-cutting campaign around mid-2026, with two 25bp cuts that year, bringing the target range to a modestly restrictive 3.25-3.50%. The median dots for 2025 and 2026 now align with our call …

… so, ‘I told ya so’ …? Hard to pay attention and perhaps too much information (here in entirety) is NOT a good thing? Everyone apparently told us so … Odd as if the entirety of Global Wall was right, why such an outsized reaction in markets. Oh well … And now, same shop w/something NOT FOMC related …

Our post-election outlook anticipates that tighter immigration and tariffs will most likely be headwinds to growth over the medium term. Optimists argue that productivity gains from deregulation and animal spirits can offset this drag. We discuss why we view this as possible, but unlikely.

… consistent with our expectations … aka, they told us so … from French operation who’s reiterating NO rate cuts in 2025

The FOMC halved its projection for easing next year and signalled sharply higher upside risks to inflation at December’s meeting.

In our view, the FOMC is struggling through one of the greatest communication challenges it has ever faced: repositioning monetary policy for the policies of the new Trump administration, without exposing itself to criticism that it is doing just that.

Today saw an important step forward in this respect, coupled with greater candor about the sharp upside risks to inflation related to President-elect Trump’s plans for higher trade tariffs and tighter immigration policy.

The FOMC appears to have begun a pause in easing of undefined length, consistent with our expectations. While Fed chair Powell turned the spotlight primarily on backward-looking data to justify this, we see the move in the FOMC’s inflation projections as consistent with an anticipation of inflation from tariffs and immigration policy.

We maintain our out-of-consensus call for no rate cuts in 2025 and think the bar for a cut in January 2025 is high.

… interrupting regularly scheduled and direct FOMC recap with some charts — ie eye candy …

The hawkish FOMC decision leaves multiple key technical levels being tested, and some being marginally edged past. While we acknowledge that year-end could mean that we see a tactical reversal of the moves, we think techs suggest risks are tilted in favour of an extension instead, especially given the current momentum in price action.

DXY: Tested resistance at 108.07 though we did not close above. We think there is room for an extension towards 108.97 (61.8% Fibonacci).

US 2y yields: Very strong resistance at 4.37-4.39% means that a move higher could be limited. However, we saw an outside day candlestick posted, and IF we see a weekly close above, it would suggest a potential extension towards 4.50%.

US 10y yields: We closed above the key resistance level of 4.50%. Weekly slow stochastics is ticking higher again, and IF we close above 4.50% on a weekly basis, we could see an extension towards ~4.64%

US 30y yields: It is a similar picture in 30y yields, with weekly slow stochastics crossing back higher. IF we close weekly above 4.68%, we could see an extension towards 4.84-4.88% (April high, 76.4% Fibonacci).

… AND, I told ya so …

DB: December FOMC recap: Inflation back on the naughty list

The Fed delivered a 25bp rate cut at the December meeting in what Chair Powell described as a "closer call" but sent a more hawkish signal about the policy path ahead. The statement inserted language around the "extent and timing" of additional adjustments – in line with our expectations – and the median dot showed only 50bps of reductions in 2025. Punctuating the hawkish signal, fourteen out of nineteen officials expected two 25bps rate cuts or less next year.

A dramatic increase in officials' inflation forecasts motivated the hawkish guidance. The median inflation forecast for 2025 rose to 2.5% and does not anticipate inflation returning to 2% until 2027. In addition, officials saw a significant shift in the distribution of risks around their inflation forecasts towards the upside. Powell noted that "some" officials began to factor policy changes into their forecasts, which likely lifted these projections.

Today's meeting reinforced our baseline view that a skip at the January meeting could turn into an extended pause in 2025. We continue to view the nominal neutral rate around 3.75% and a need for the Committee to stay restrictive relative to that level. As such, we reiterate our view that the fed funds rate is likely to remain above 4% next year, with a base case of no additional reductions. For a full discussion of our outlook for the economy and the Fed, see our latest publication: "Trump II: Growth too fast, inflation too furious for Fed cuts".

… asking questions, leading to some hypotheticals …

… What Powell didn’t get much of in today’s press conference was real pushback on the hard questions. Why has the Fed abandoned the “SuperCore” inflation metric they prioritized two years ago? Why has the Fed continued to ignore the money supply in their analysis when it outperformed virtually any other measure in predicting the inflation the Fed said would never occur? How is the Fed running operating losses of more than $100 billion per year and still paying for nonmonetary research? We didn’t expect any reporters to step up to the plate and press Powell, but these are questions that need answers.

The stage is set for an epic battle in Washington over the year ahead. Tax cuts and deregulation stand to boost businesses, while a clamping down on government excess could slow the outsized deficit spending that has propped up economic growth. What will we be watching? If M2 growth remains modest, both inflation and economic growth will slow, but the Fed will have room to continue cuts. If, however, rate cuts lead to a rapid rise in M2 growth, the Fed has shown an active neglect of the warning signs that would have preempted this inflation debacle to begin with.

… if, as John Boehner used to say, ‘IFs, Ands and BUTS were candy and nuts, every day would be Christmas’ …

… and, general reCAPathon continues …

ING: Fed confirms a slower and shallower rate cut story for 2025

We got another 25bp policy rate cut from the Fed, but updated projections and Chair Powell’s press conference confirms that the Fed is going to be much more cautious next year with sticky inflation and President Trump's policy mix meaning a higher hurdle is required to justify rate cuts in 2025

ING: Rates Spark: Long-end rates look too low post the FOMC

Noteworthy here is the upside shift in the market expectation for the effective fund rate for end-2025. It’s essentially flat to the current 10yr SOFR rate. Something is mis-priced here. Most likely, long tenor rates are too low. Compared to the Fed, the ECB has more flexibility to cut rates if needed, posing downside risks to the EUR front-end

… so some good news is policy uncertainty era has come to an end … well, ALMOST … an updated call (so, no victory lap and ‘I told ya so’ here…)

MS: FOMC Reaction: Policy Uncertainty Stops the Fed in Its Tracks (Almost)

The Fed signaled a pause in rate cuts is at hand and the bar for further rate cuts may be higher. We now expect only two rate cuts in 2025, in March and June. Our strategists stay neutral on UST duration and curve shape, and maintain long MBS basis.

Key expectations

The FOMC lowered the fed funds rate by 25bp to 4.375%. Its statement signaled the Fed is intent on pausing before resuming rate cuts. The Summary of Economic Projections (SEP) shifted to only two cuts next year instead of four, with inflation not reaching the 2% target until 2027.

The dramatic firming of the inflation path was a result of participants incorporating expectations of policy changes, inflation inertia, and – in our view – uncertainty about what the drivers of inflation are at present.

We change our outlook for Fed policy. We now only look for two rate cuts next year, in March and June. Uncertainty about the timing and magnitude of any potential changes to trade and immigration policies leaves us more confident about the March cut than the June reduction.

Our rates strategists suggest investors remain neutral on US Treasury duration and yield curve shape, but remain positioned for a 25bp rate cut at the January FOMC meeting, as a hedge against the data surprising to the downside relative to investor expectations.

Our FX strategists shift to a neutral view on the US dollar in line with the US economics team’s fed funds call adjustment.

On the agency MBS side, our strategists remain overweight mortgages, but with lower conviction given lower expectations for marginal demand and increased bear-flattening risks.

… interrupting normal recap / victory lapping of the FOMC meeting to bring you a chart …

MS: Cross-Asset Dispatches: 2024 Year End Wrap-Up - Top of the Charts!

Investors have come to us throughout 2024 for various charts and data requests - here are the top five most-requested charts from the cross-asset strategy team, what they show, and why we think they matter.

Market Sentiment Indicator (MSI) - Are We Risk-On Or Risk-Off?

US Cycle Indicator - Where Are We In the Market Cycle?

Money Market Flows - When Will We See Rotation Out Of Cash Into Equities?

Money market funds (MMFs) were closely watched all year amid expectations that the start of Fed rate cuts would see the beginning of MMF net outflows, fueling equity and fixed income markets.

However, previous cycles saw considerable lags between the first Fed cut and MMF net outflows; we expect inflows to continue next year, albeit at a slower pace, as MMF yields likely remain attractive relative to other cash alternatives. In other words, Fed cut-driven MMF outflows is a tailwind, but it's a tailwind to come, probably not until 2H25.

Valuations 'Violin' - Just How Stretched Are Valuations?

US versus RoW - Will US Equities Continue to Outperform?

… NOT, repeat, NOT another ‘I told ya so’, as detailed by the ‘delayed our call’ …

The Fed cut rates by 25 basis points as widely expected, but also signaled more a more gradual easing cycle going forward alongside upwardly revised growth and inflation forecasts.

That’s broadly in line with our own forecast, that expects much of the ongoing resilience with domestic demand will persist into the new year, and that interest rates will need to stay elevated to offset resulting inflationary pressures.

Our base case projections expect one more 25 basis point cut in January before pausing at a 4% to 4.25% range for the rest of the year.

… do we really think there’s ANY reason to believe or guess ‘bout 2026? I’ve got a bridge to sell ya … and speaking of bridges sold, this Swiss stratEgerist is quite popular despite or because of his disdain for the USofA (my view only)…

The Federal Reserve cut rates as expected, but hawkish forecasts and press conference language surprised markets. The pace of rate cuts was always expected to slow in 2025, but the Fed is clearly more focused on the inflation threats of some of US President-elect Trump’s policies (fiscal, mass deportation, and taxing consumers).

Every major central bank followed the path of inflation this year, keeping real rates generally stable. That continues next year, but clearly the Fed’s perception of inflation risks is shifting. There are also downside threats—mass deportations may risk recession. After some social media posts from Trump, risks of a government shutdown are rising.

The Bank of Japan left rates unchanged today, in line with earlier media leaks and so not a surprise for investors. The BoJ is likely to raise rates next year (March seems likely), but more modest inflation pressures and US uncertainty have stayed their hand for now.

The Bank of England is always an interesting central bank to watch as (unlike some central banks) it is headed by economists—always the perfect model of leadership. No rate cut is expected today, with inflation not expected to decline in the near term. Fictional housing measures and the peculiar energy price structure are adding to price levels.

… AND covered wagons chime in with an ‘I told ya so’ (ie, as expected) …

Wells Fargo: FOMC Cuts Rates, but Pace of Easing Ahead Likely Will Slow

Summary

As widely expected, the FOMC cut the target range for the federal funds rate by 25 bps at today's meeting. However, one Committee member, who preferred to keep rates on hold, dissented.

Wording in the post-meeting statement was changed to signal that further easing may proceed at a slower pace.

The median dot for 2025 in the so-called "dot plot" was raised by 50 bps. In September, the median FOMC member looked for 100 bps of policy easing next year. The median forecast today looks for only 50 bps of rate cuts next year.

The wide dispersion in the dot plot for next year may reflect some uncertainty regarding the policy agenda that the incoming administration may pursue. Notably, the range of core PCE inflation forecasts for 2025 widened considerably.

… In sum, today's FOMC meeting leads us to believe that, barring some dramatic unexpected development, the Committee likely will keep rates on hold at its next meeting on January 29. However, we believe the FOMC will continue to ease policy next year, albeit at a slower pace than over the past few months. Chair Powell seemed to support this expectation when he noted in his presser that the stance of monetary policy is "significantly closer to neutral" than it was previously, but that policy is "still meaningfully restrictive."

The Federal Open Market Committee (FOMC) cut the federal funds rate (FFR) by 25bps today, as widely expected. That takes the target range for the overnight rate down from 5.25%-5.50% to 4.25%-4.50%, a full percentage point lower since the Fed's rate cutting cycle started on September 18. A cut was all but guaranteed. Yet the S&P 500 fell almost 3%, while the Nasdaq dropped 3.5%. The 10-year yield jumped 13bps to 4.51%, its highest since May.

What gives? The Fed's updated Summary of Economic Projections was quite hawkish. When including the nonvoters on the committee, the dot plot shows that four FOMC participants were in favor of not cutting the FFR today (chart). Newly appointed Cleveland Fed President, Beth Hammack, dissented in favor of no cut….

… And from Global Wall Street inbox TO the WWW …

First up is a note which landed in the inbox YESTERDAY … just before 10th down day in a row (longest such streak since ‘74) …

Investors are extremely bullish on the stock market, and a record-high share think that there is less than 10% probability of a crash over the coming six months, see chart below.

Source: Yale School of Management, Robert Shiller, Apollo Chief Economist

… here’s a VIEW (OpED) from The Terminal …

Bloomberg: Fed drops a lump of coal in Trump market's Christmas

Powell rebuffs notion that tariffs weighed on calculations for fewer cuts, but a showdown may be looming.

Oh Say Can You FOMC!

Every so often, things happen just as expected. That’s what happened Wednesday when the Federal Open Market Committee announced their widely telegraphed and oxymoronic “hawkish cut.” Rates came down, and guidance strongly suggested that there might not be too many more cuts to come.

And yet, this turned into one of the biggest Fed-induced shocks in years. As Bloomberg colleague Ye Xie illustrates in this chart, the 10-year yield hasn’t leapt so much in response to a Fed announcement since the notorious Taper Tantrum of 2013. Quite a response to a cut:

That brutal response was refracted throughout markets. Risk assets turned down when the news came out, and then fell much further as Federal Reserve Chair Jerome Powell gave his press conference. Volatility shot upward. Pressure on emerging market currencies was particularly severe:

Having established that the markets think this was a big and very negative deal, it’s worth looking at what bothered them. The biggest problem was the Survey of Economic Projections, or “dot plot,” in which each FOMC member offers predictions marked with a dot. This shows an increase in expected inflation and in projected growth, and that led almost all of them to scale back where they expect fed fund rates to be at the end of each of the next three years. Using my usual low-tech illustration, which appears to be effective, these are the side-by-side projections from the last dot plot in September and the latest edition. There are far more outliers on the upside of rates for next year, while estimates of substantial cuts in 2026 have very significantly reduced. The direction of travel for rates is unmistakably upward (as indicated by the arrow):

Looking at the median, committeemembers now expect only two cuts of 25 basis points each for next year, down from four. If we look instead at averages, we get the following picture. The midpoint for the fed funds rate is now down to 4.375%; the average expectation is that this will fall next year only as far as 3.84%, or two cuts. There will be some catch-up in 2026, but that’s a long way off:

That’s a move in a sharply hawkish direction. Investors were generally hoping for predictions of three cuts next year, not two. To illustrate just how much expectations have shifted, the following chart, produced by the World Interest Rate Probabilities function on the Bloomberg terminal, shows the course for the fed funds rate that futures were discounting on the eve of the September dot plot, and where they are now:

Was the Market Ready for a Pullback? It’s a big move in a short space of time, but there’s a need for perspective. The 10-year yield has just jolted upward but is still well within recent ranges. It’s just topped 4.5% but has been there a few times in the last two years, briefly reaching 5%. This is a troubling development, but not a transformative one:

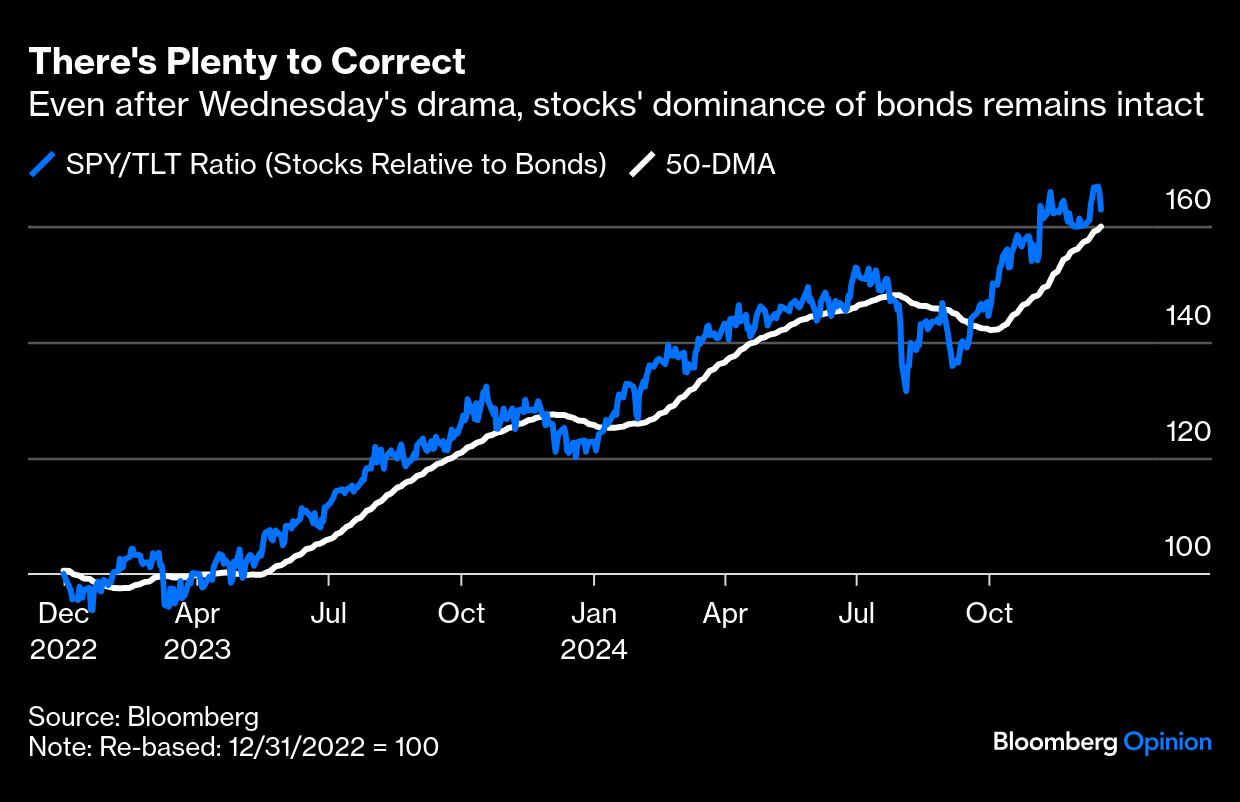

It’s also fair to say that the rally in stocks was overheated, and overdue a correction. Proxying the relationship of stocks to bonds with the popular ETFs tickered SPY (tracking the S&P 500) and TLT (tracking 20-year and longer Treasuries) shows that even after Wednesday’s mayhem, the stock/bonds ratio is still above its 50-day moving average. The disquieting part is that there’s further to fall, but this does show that there’s nothing too unhealthy about a stock selloff at this stage:

… AND once again interrupting FOMC recap / victory lapAthon for a quick and hot tech take on 2025 and 10yy …

IGM: Technical Analysis ChartWatch: G10 Outlook 2025 FX | 10-Year Yields

…US 10Yr Yield – Reversal From 5.019 Signals Risk To 3.248/2.514

Extended the steep yield advance to 5.019, before easing to range over 3.595

Deteriorating studies suggest risk towards 3.248/3.259, perhaps 2.514

… so, an offset from the ‘10s TO 6%’ call of THE OTHER DAY??

The FOMC today cut rates by 25bps, but acknowledged that is was a close call. The number of rate cuts was reduced from 4 to 2 for 2025, paired with inflation being revised markedly higher.

… from BCA research via ZH …

ZH: The Real Reason To Own Bonds, And When To Buy Them

https://youtu.be/IdklYxInyL4?si=TI5iI64lXB-YPMMo

Fed Cuts Rates for 3rd Time This Year — DiMartino Booth Breaks it Down with Charles Payne of FBN

https://youtu.be/s6eSFDWgU5o?si=bEB_yxJmEEWYp5XH

Jim Bianco joins Bloomberg to recap yesterday’s FOMC Meeting & give his outlook for 2025