Good morning … as the year grinds to a close and best I reckon, only UK ‘flation overnight in as far as a driver OF price action …

CNBC: UK inflation rises to 2.6% in November, in line with expectations AP: UK inflation increase solidifies expectations interest rates will be kept on hold

… I’ve very little to add TO market pricing mechanism (term structure of rates, equity futures) which, at the moment, appears to me to be aggressively UNCH heading in to this afternoons all important and final FOMC and <DOTS> GO of 2024…

I’ll begin with a look at 20s …

… and this — momentum overSOLD as (down / bullish)TLINE holding, on heels of yesterday’s UGLY auction …

ZH: Ugly, Tailing 20Y Auction Lifts Yields From Session Lows

… a question I’m contemplating … can / will a hawkish cut (SEP less cuts than priced?) support dip buying and ultimately be the (Fed) pause that refreshes (all markets)?

… AND a quick data recap which all occurred before the auction …

ZH: Surging Car Sales Spark Upside Surprise For Retail Spending In November

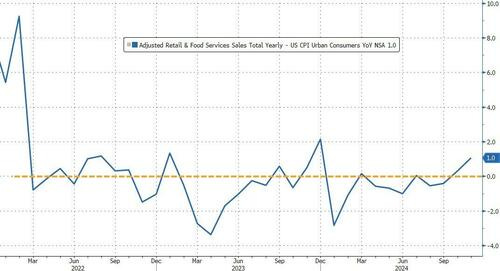

… Finally, as a reminder, retail sales data is 'nominal' so a quick sleight of hand using CPI data as a rough indication of inflation and we see that in fact, real retail sales have basically oscillated around the flatline for the last 30-months-plus...

So another data point for The Fed that clearly signals no need for rate-cuts! Does this look like an economy dealing with 'restrictive' rates?

ZH: US Industrial Production Tumbled For The 3rd Straight Month As Capacity Utilization Craters

… and a few other informative ReSale TALES related links …

Bonddad: Real retail sales on the cusp of breaking out of their multi-year doldrums Bonddad: Industrial production continues to slide CalculatedRISK: Retail Sales Increased 0.7% in November WolfST: The Fed Needs to Watch Out to Not Throw More Fuel on this Demand: Retail Sales Accelerated Sharply in the 2nd Half. It’s like someone turned on the spigot in July and forgot to turn it off.

… and in sum total, the day that WAS yesterday

ZH: Big-Tech's Pain Is Bitcoin's Gain; Goldman Warns 'Seasonal Gift Of Low Vol Increases Jan Reversal Risk'

… and so, with all THAT granular detail offered, a quick look at A TWEET (from The Chart Report) … which reads

The DJIA is working on its 9th straight down day. From a pure technical perspective, this is a make-or-break level for bulls.

…The Takeaway: After its longest losing streak in 40 years, the Dow is facing a critical level at $43k

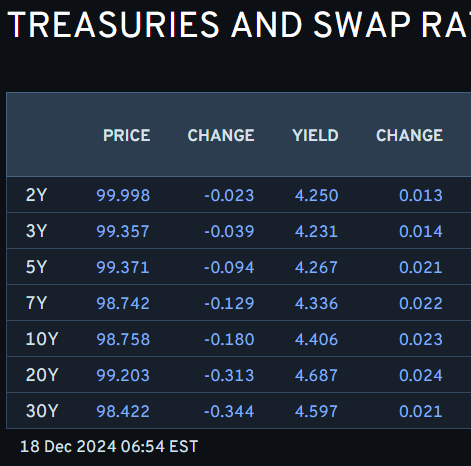

… AND I’m done. From here, it’s 100% up TO the Fed. There is more below (DB) on the S&Ps streak (not to be left out) and … here is a snapshot OF USTs as of 654a:

… and for some MORE of the news you might be able to use…here are some resources and curated links for your dining and dancing pleasure … kindly note bullet from PiQ (with link below) AND an excerpt (and visual)from Yield Hunting …

NEWSQUAWK: USD broadly firmer vs peers ahead of the FOMC; US futures edge higher … USTs are contained, Bunds dip lower and reside at session lows … USTs are relatively contained ahead of the FOMC. USTs are marginally in the red within a slim 109-25 to 109-30 band, which is entirely within Tuesday’s 109-17 to 109-31+ parameters. The FOMC is expected to deliver a 25bps cut; focus will be on the 2025 dot plots and forward guidance (FOMC Preview can be found at the top of the sheet).

Bond traders have been boosting options and futures wagers that the Federal Reserve is about to signal deeper interest-rate cuts next year than the market anticipates. (BBG)

… The Fed is attempting to walk the tightrope between figuring out the neutral rate in the post-pandemic economy (where deficits are massive), and policy shifts -specifically in tariffs, immigration, deregulation - effects on inflation.

Nick Timiraos from the WSJ (no paywall) summed it up nicely:

Powell is (again) trying to find the right gear for monetary policy amid signs the labor market is less wobbly and inflation is a touch firmer than they appeared in September. He faces misgivings from some colleagues over continuing to cut and less conviction from others who strongly backed those first two moves. Given current market expectations of a cut, the path of least resistance would be to cut by a quarter point, and then use new economic projections to strongly hint that the central bank is ready to go more slowly on the reductions.

Core CPI remains 'suck' in the low 3s and will need to come down to at least the mid-2s before the Fed claims 'mission accomplished'. That will take a big reduction in government spending AND a slowdown in the labor market. The latter is already occurring, just very slowly.

In CEFs, we remain fully invested. There were some comments about Muni CEFs and their performance.

The Muni CEF ETF tracker is up almost 10% so far in 2024. That is a decent return though below my expectations as inflation has been stickier than expected, especially in the last few months.

Muni CEFs along with long-term investment grade bonds will be inversely related to the movement in the 10-year bond. The 10-year has been moving up and down in a cyclical fashion for most of the last two years. The chart below shows the last year and the movement up, and then down, and back up.

When the rate is up, Muni CEF NAVs are going to fall as well agency MBS and other longer-duration bonds. Meanwhile, your credit exposure, like BBB- 5 year bonds (think your BDC notes) will do well as equities rise and spreads tighten…

Opening Bell Daily: Markets drive the Fed. The Fed is about to cut rates with inflation moving in the wrong direction. CPI hit a five-month high in November and asset prices are smashing records.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ … mostly victory laps and data recaps in / around ReSale TALES which, then beg the question posed above IF rate CUTS completely necessary …

BARCAP: November retail sales: Another strong month

Retail sales rose 0.7% m/m in November, propelled by a jump in auto sales and a strong Black Friday tally at online retailers. The control group rose 0.4% m/m, with online sales offsetting softness elsewhere. With the data strong, as expected, we are tracking a 2.6% q/q saar gain in GDP in Q4 2024.

… Although spending fundamentals remain supportive for now, we expect income to become a headwind in coming quarters as immigration limits bind. Data show that limits on the number of asylum seekers implemented by the Biden administration in June have been followed by noticeable declines in the pace of inward migration in recent months. In our view, this will begin to weigh on the pace of labor supply entrants in the coming quarters, thereby contributing to deceleration in labor market income. This dynamic will likely weigh on retail sales, and consumer spending more broadly, as the US economy proceeds into 2025 …

… same shop with an interesting note on (AI) stocks …

Thus far, most of the value from AI has accrued to Big Tech and Semis. More recently, optimism around the new Agent AI wave has powered software valuations, moving value up to the 'application' layer. AI monetization driven earnings growth will be a key barometer for Tech stocks in 2025.

… and a few words from everyone’s fav stratEgerist on today’s FOMC meeting…

… Moving onto the Fed, it is widely expected that they'll be another 25bp cut today, so the bigger question is what they’ll signal in their dot plot for next year, as there’s been speculation they could pivot in a more hawkish direction. Last time in September, the dots pointed to a further 100bps of cuts in 2025. But since then, the inflation prints have been a bit stronger than expected, so the consensus (and DB’s own forecasts) expect the FOMC to only pencil in 75bps of cuts for next year.

The risk that we actually go the other way is something we pointed out in our curveballs chartbook (link here). 2024 is the third year in a row that markets have over-estimated the Fed’s dovishness. Indeed at the start of this year, futures were pricing in over 150bps of cuts for this year, but after today it looks as though we’ll only end up with 100bps. And when it comes to next year, our US economists think the same will likely happen again, as their baseline sees a much more hawkish path than the futures curve. They think that after today’s cut, a skip in early 2025 could turn into an extended pause, and they don’t see the Fed cutting rates at all next year. See their full preview for today’s meeting here …

… AND a break from FOMC precap for a few words on ReSale TALES …

Retail sales rose 0.7% in November (+0.8% including revisions to prior months), narrowly beating the consensus expected increase of 0.6%. Retail sales are up 3.8% versus a year ago.

Sales excluding autos rose 0.2% in November, lagging the consensus expected +0.4%. These sales are up 3.2% in the past year.

The largest increases in November, by far, were for autos and nonstore retailers (internet and mail-order). The largest decline was for miscellaneous store retailers.

Sales excluding autos, building materials, and gas rose 0.2% in November and were up 0.3% including revisions to previous months. If unchanged in December, these sales will be up at a 4.2% annual rate in Q4 versus the Q3 average.

Implications…As a whole, retail sales are up 3.8% on a yearto-year basis. “Real” inflation-adjusted retail sales are up 1.0% in the past year but still down from the peak in early 2021. This highlights the ugly ramifications of inflation: consumers are paying higher prices today but taking home fewer goods than they were three years ago. And while the Fed looks set to cut interest rates by another quarter percentage point at the conclusion of the meeting tomorrow, it is not at all clear that inflation problems are behind us. We hope they have the resolve to stomp out the embers of inflation even if economic troubles come. In other recent news, import prices rose 0.1% in November while export prices were unchanged. In the past year, import prices are up 1.3% while export prices are up 0.8%.

… more ‘bout todays rate cut …

ING Rates Spark: A 25bp cut this time, but will they pause in January?

From Wednesday's FOMC meeting, a key question is whether the Fed shows a tendency to pause the rate cutting from the January FOMC meeting. We think they'll indeed pause; the question is whether they want to telegraph that. Meanwhile, Germany's issuance plan confirms plenty of supply to absorb in 2025. And, Gilt yields are set to remain elevated

… one more to consider into the ‘rate cut scrum’ …

US inflation has fallen this year. A lot of this is due to the fantasy owners’ equivalent rent price, which no one pays. Declining fantasy prices do not help consumers’ spending power. However, rightly or wrongly (the answer is “wrongly”), Fed Chair Powell pays attention to inflation measures including OER. If rates were raised on a fantasy, they should be cut on a fantasy—and we see a rate cut today.

The Fed was late in reducing rates this year. Having caught up with itself, the Fed can indulge in a slower pace of rate cuts next year. President-elect Trump’s seeming determination to impose significant sales taxes on US consumers adds uncertainty. The Fed should ignore first-round tariff effects on inflation, but respond if second-round effects (lower competition, profit-led inflation) emerge…

… covered wagon folks weigh in on yesterday’s data …

Wells Fargo: Auto Sales and Ecommerce Drive Outsized Gain in Retail Sales

Summary The November jump in retail sales owes much to the largest category of spending. Auto sales jumped 2.6%. The next-largest category, ecommerce, also notched a stout gain of 1.8%. No other category posted a gain of more than 1%, leaving our 3.3% holiday sales forecast right on track.

…This Will Give Policymakers Something to Talk About For the sixth month in a row, retail sales came in better than expectations in November, this time for a gain of 0.7%. This comes as the FOMC is convened in Washington today for day one of their two-day meeting in the lead-up to tomorrow's rate decision. Financial markets widely expect another 25 basis point cut, but the impulse to remove restrictive policy could be growing less urgent. Discussion among policymakers is apt to include the strange combination of a cooling in the jobs market even as consumer spending continues to show solid growth. Recent upward revisions to productivity data make these seemingly counterintuitive developments make a little more sense, but big spending and a wobbly labor market do not typically go hand-in-hand.

It has been a hallmark of the current expansion that consumer vitality has been a mixed blessing for policymakers: Good in the sense that it sustained the expansion during periods when many were braced for recession. Bad to the extent that robust demand sustained price pressure making the Fed's 2.0% inflation target an elusive one. That said, the worst of the consumer-related price pressure is on the services side of spending, which gets only modest representation in the retail sales report. Bars & restaurants saw sales fall 0.4% in November, though the category is still up 1.9% over the past year.

Higher financing costs have not materially slowed spending in the service sector, although earlier on in this cycle they have taken a toll on big-ticket durable goods. That dynamic is less true lately. A key factor in today's out-performance is the 2.6% jump in auto sales (chart). Excluding autos, retail sales rose just 0.2%, which was half the expected gain.

Wells Fargo: Third Straight Drop for Industrial Production in November

Summary The expected bounce in industrial production was a no-show in November. If you look closely enough, there are some rare examples of growth, but overall production is down 0.7% year-to-date and manufacturing capacity utilization is at a seven-year low (excluding the pandemic).

… Stocks were a bit lower today, mostly because investors are waiting for the FOMC's interest rate decision and updated quarterly economic forecasts tomorrow. Regardless of what the Fed does, as long as companies continue to grow their earnings, they're likely to keep hiring new employees and to increase real wages (chart). Lower interest rates, higher worker productivity, another corporate tax cut, and deregulation all suggest that this year's solid growth will continue into 2025. Indeed, the Atlanta Fed's GDPNow model is tracking 3.1% real GDP growth this quarter, with real consumer spending up 3.2%. We're expecting annual real growth between 2.5% and 3.5% next year …

… And from Global Wall Street inbox TO the WWW …

First UP from Bloomberg a read through on positions into years end with a hat tip towards getting jump on 2025 …

Bloomberg: Bond Traders Target Deeper 2025 Fed Rate Cuts Than Market Expectations

SOFR options bets anticipate more than half-point of 2025 cuts

Fed funds futures trading wagers on cuts in next two meetings

… With inflation proving sticky, however, Wall Street banks have started to anticipate that the Fed will forecast perhaps one fewer cut next year, meaning three-quarters of a point in total. And some predict the central bank may pencil in just a half-point, a level that’s broadly in line with what swaps markets are pricing in.

But in interest-rate options, some traders are betting that the market’s view is too hawkish, and that the Fed will hew more closely to what it projected in September: the equivalent of four quarter-point cuts in 2025, driving the implied fed funds target rate down to 3.375%.

These traders may have in mind how potential signs of labor-market fragility could boost wagers on steeper Fed easing, and how Treasuries rallied earlier this month on data showing an unexpected jump in the jobless rate.

In options linked to the Secured Overnight Financing Rate, which is highly sensitive to Fed policy expectations, demand has focused on dovish bets targeting early 2026 on structures expiring early next year. These positions stand to benefit should the central bank’s policy forecasts be more dovish than markets expect.

Along with this, traders are increasing positions in fed funds futures. Open interest has risen to a record in the February maturity, pricing on which is closely linked to the Fed’s December and January policy announcements. Recent flows around the tenor have skewed toward buying, indicating fresh wagers that would benefit from a December rate cut and then additional easing priced into the following decision on Jan. 29.

The bullish activity seemed to get a boost from Morgan Stanley’s buy recommendation this month on the February fed funds contract. Investors should position for a higher market-implied probability of a quarter-point cut on Jan. 29, strategists said. There’s now a roughly 10% chance priced in for such a move next month, assuming the Fed delivers what’s expected on Wednesday.

… AND same site, an OpED with other POSITIONS in mind …

Bloomberg OpED (Authers): Smart vs. dumb money — how exuberant about Trump are you?

Professionals are approaching the current exuberance for stocks with a colder eye than it may seem.

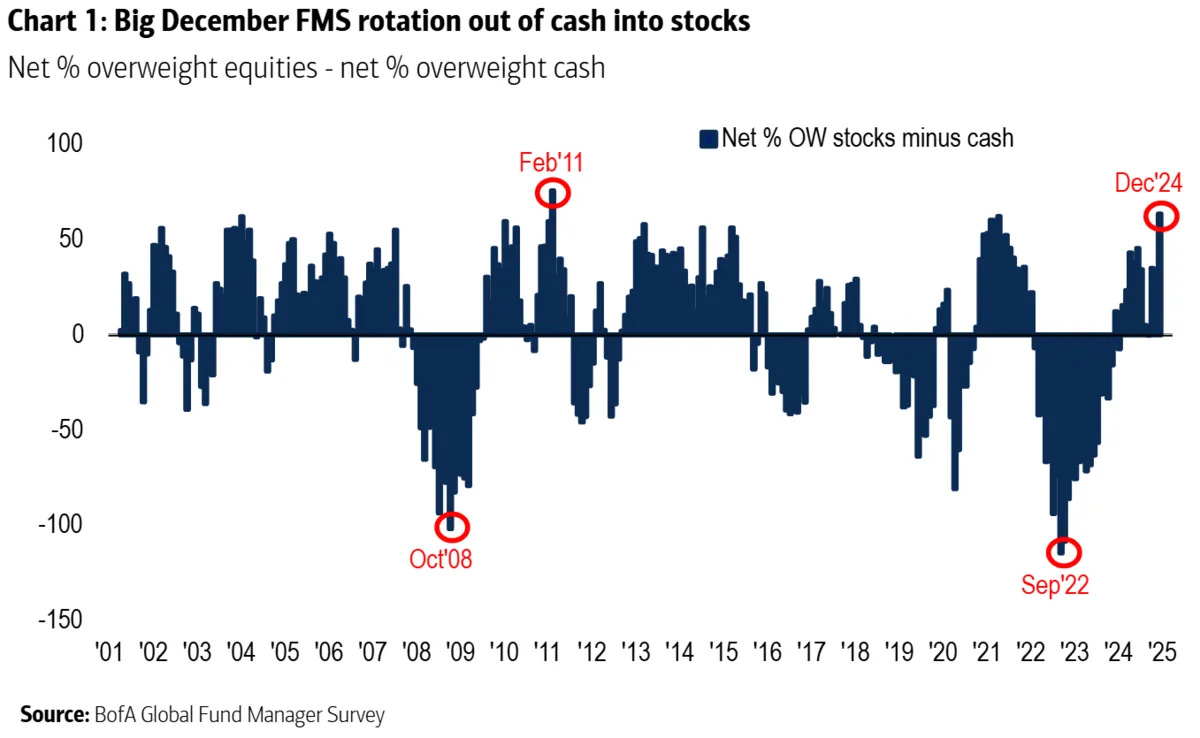

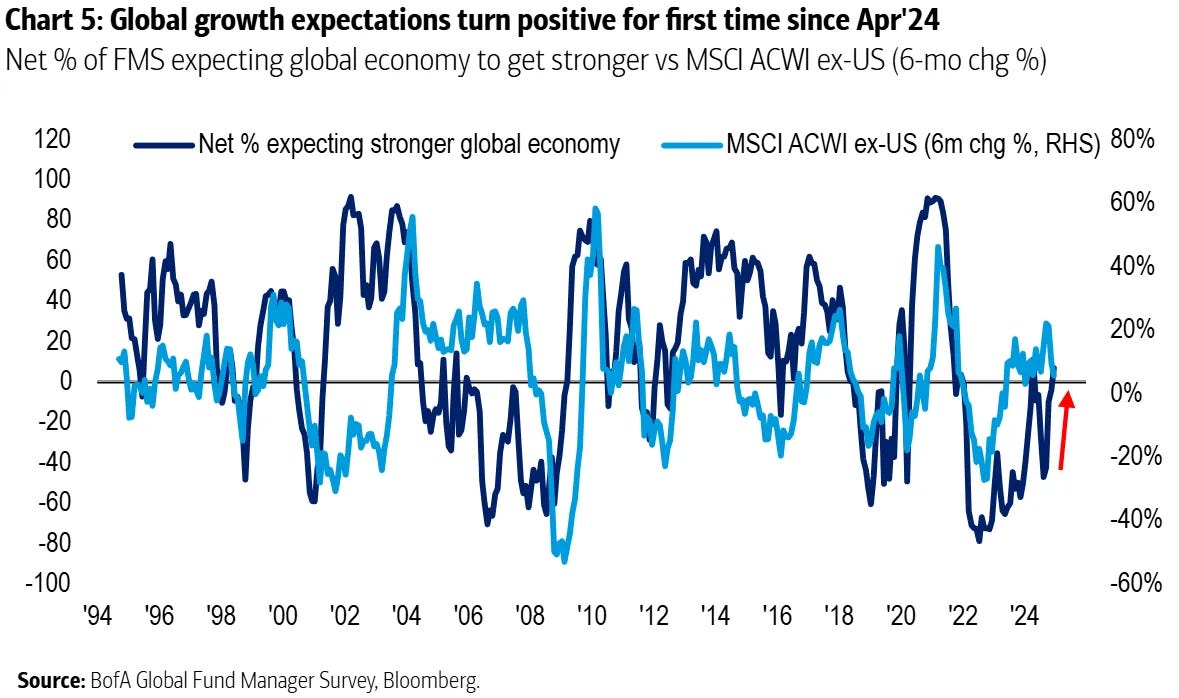

… So the Trump boomlet in US stocks should be viewed in the context of a trend that was already looking complete. That makes the way professional money managers responded to the election look excessive. Bank of America Corp. has just published its first monthly survey of global fund managers since the vote. It shows a huge switch out of cash and into stocks. In the past, that has tended to be a contrarian signal to get out of stocks:

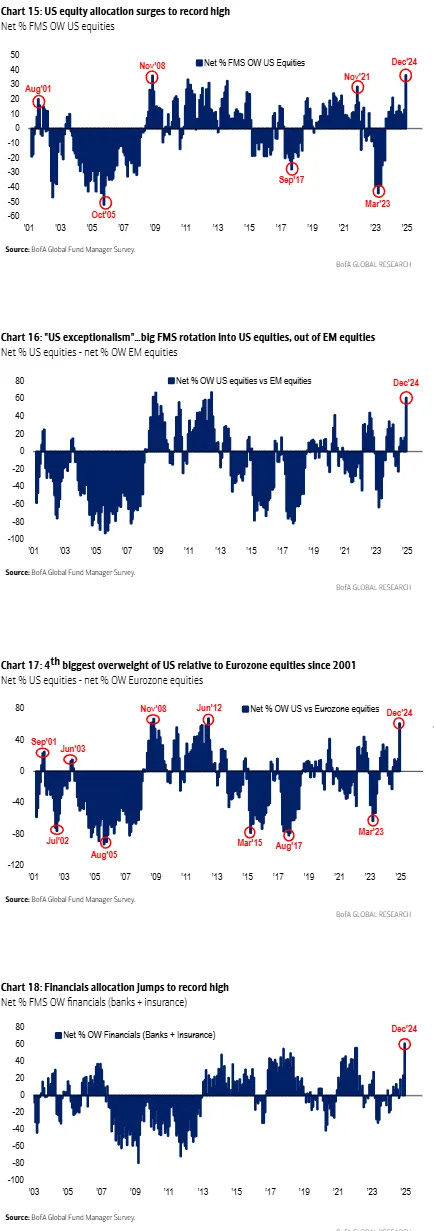

On a series of questions, the big money managers interviewed by BofA suggested that they had never before been quite so bullish about the US. As shown below, the numbers overweight in US equities rose to an all-time high, and there were massive rotations out of the euro zone and emerging markets and into the US on a scale not seen in more than a decade. Financials also seem at last to have recovered from the GFC, with BofA finding the biggest allocation on record, a sign that promised deregulation is exciting money managers:

But not everything is consistent with a zero-sum view of the world in which the US vacuumsup growth from everyone else. This has some of the elements of a “rational bubble,” in which investors take on a position because they feel forced to do so by the lack of any good alternative, rather than the kind of speculative bubble that can burst in a damaging way. Absolute Strategy Research undertakes a similar survey of asset allocators, run by David Bowers, who previously established the BofA survey. It found a sharp increase in bullishness toward American assets, from Europeans as much as from US-based managers, but this was driven primarily by the belief that the political shifts left them with no choice:

There is no alternative to US equities, according to our panel. They have adopted the most positive stance on US versus non-US equities since our survey began, with an implied probability of 63%. When we look by demographics, our European panelists are almost as positive (65%) on US versus non-US equities as North American-based panelists (68%). There has also been a loss of confidence in emerging markets versus developed markets, where the implied probability of the former outperforming the latter has fallen seven percentage points from 50% in the third quarter.

The proportion expecting the global economy to strengthen rose sharply as well. This generally portends good things for stocks outside the US:

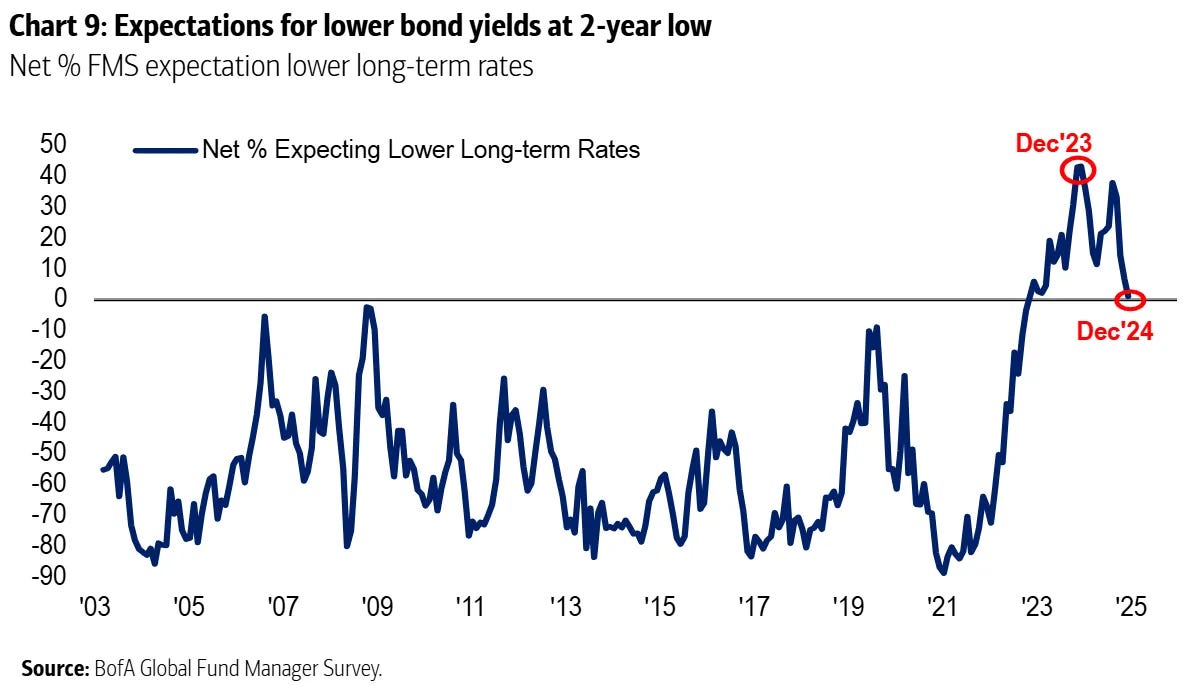

… It doesn’t look a great time to buy, but it doesn’t scream irrational exuberance. The BofA survey also reassures that the professionals are alert to the risks with Trump, as well as the opportunities. The proportion expecting lower long-term bond yields has collapsed (and that could create a big headwind for stocks):

… this next link offers funTERtaing and informative visuals and the one on MARG DEBT made me pause …

Hedgopia: Amidst Plenty of Overstretched Valuation And Sentiment Measures, S&P 500 On Pace For Back-To-Back 20%-Plus Gains

The S&P 500 is up north of 27 percent year-to-date – the second consecutive year of gains of north of 20 percent. Buybacks and margin debt are cooperating, but several other measures are pointing to extended conditions.

With 10 sessions of trading remaining this year, the S&P 500 is up 27.3 percent – on pace for a best year in five (Chart 1). This comes after last year’s 24.2-percent jump. From the lows of October 2022, the large cap index is up an astounding 74 percent…

…Equities are also drawing support from margin debt, which took a back seat for a while before picking up momentum last month. In November, FINRA margin debt jumped 9.3 percent month-over-month to $891 billion, which is 5.1 percent from the record $936 billion set in October 2021 (Chart 3).

Margin debt tends to have a tight correlation with small-cap stocks. The Russell 2000, which peaked in November 2021, waited three long years before surpassing that high last month. Small-caps are treated as a way to measure investor willingness to take on risk. On that score, post-November 5th presidential election and Donald Trump’s win, the Russell 2000 has come alive. As has willingness to take on leverage.

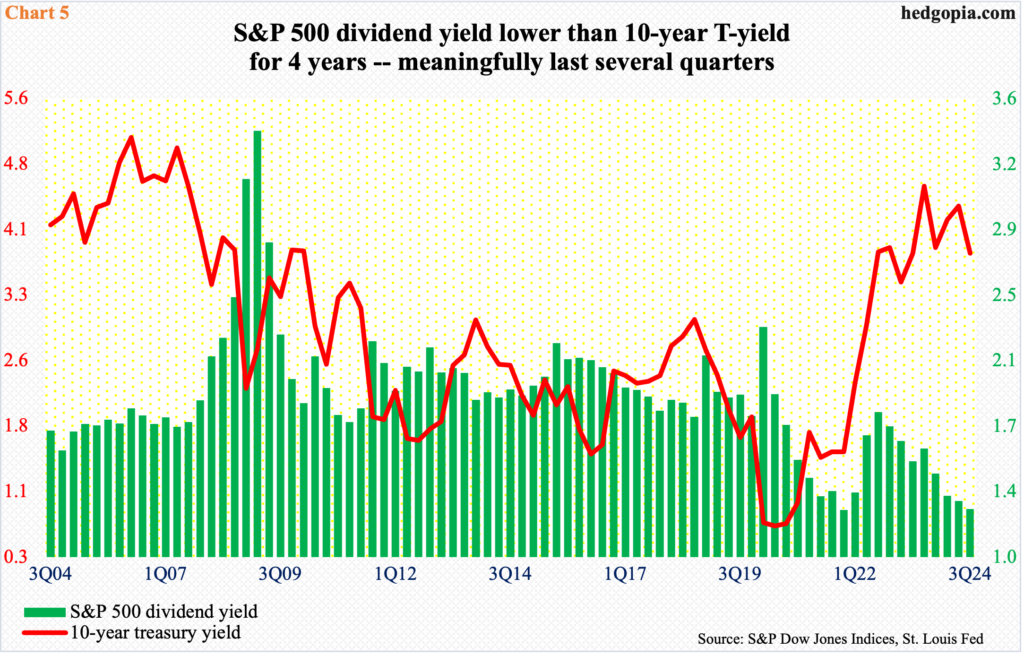

… The picture looks similarly pricey comparing the S&P 500 dividend yield with the 10-year treasury yield (Chart 5).

At the end of the September quarter, the S&P 500 yielded 1.27 percent, matching the low from 4Q21. Yield has not been this low going back to 4Q00.

In contrast, after remaining sub-one percent for several quarters, the 10-year treasury yield began to rise in 2021, as the long end of the yield curve anticipated a rise in the fed funds rate, which went from a range of zero to 25 basis points in March 2022 to between 525 basis points and 550 basis points by July last year. The benchmark rates are currently between 450 basis points and 475 basis points, with a 25-basis-point cut tomorrow all but certain.

The 10-year yield rose as high as five percent in October last year before coming under pressure to bottom at 3.6 percent this September, with the quarter ending at 3.81 percent. These notes are currently yielding 4.4 percent, which strictly from the yield perspective offer more than 300 basis points more than what the S&P is yielding.