Good morning … and another, another thing … Just kiddin’. Today’s note can and will be short given weekend notes. Jumpin’ in with a look at Bloomberg.com front page…

Trump SAYS, Carney’s IN and China struggles …

Bloomberg: Trump Says US Economy Faces ‘Transition,’ Avoids Recession Call

Bloomberg: Mark Carney Wins Canada Liberal Contest, Will Succeed Trudeau in Days

Bloomberg: China’s Struggles With Supply Glut Threaten to Extend Deflation

…and with THAT in mind, on heels of Friday’s NFP report …

Bloomberg: Wall Street Starts to Rethink Lofty S&P 500 Forecasts for 2025

JPMorgan cautions index may not reach bank’s target until 2026

Piper Sandler says still early for strategists to rip up calls

…“I don’t think anybody has more conviction today at all: more uncertainty, yes — a wider band of outcomes, yes,” Michael Kantrowitz, Piper Sandler’s chief investment strategist, said.

Indeed, Lakos-Bujas indicated the S&P 500 could swing anywhere from his original year-end projection to as low as 5,200 throughout 2025…

…At RBC Capital Markets, Lori Calvasina lowered her bear case for the S&P 500 to 5,600 from 5,775 by year-end based on new stress-test modeling that now reflects flat corporate earnings and a different inflation and interest rate scenario.

“Strong post-election vibes were an important part of the bullish consensus on 2025 for US equities, which has come under pressure,” Calvasina said in a note to clients. She also asserted that the risk of a “growth scare” in the S&P 500, defined as a 14% to 20% drawdown, has risen.

Still, strategists including Calvasina are sticking to their S&P 500 price targets for the year for now as the economy remains solid based on the latest employment data and remarks by Federal Reserve Chair Jerome Powell, who said Friday that the central bank does not need to rush to adjust monetary policy. On average, Wall Street expects the S&P 500 to close 2025 just above 6,500, based on a survey of estimates compiled by Bloomberg.

… and not a moment too soon as futures look to indicate another rocky ride (translation: selloff) at least in early, pre-market trading …

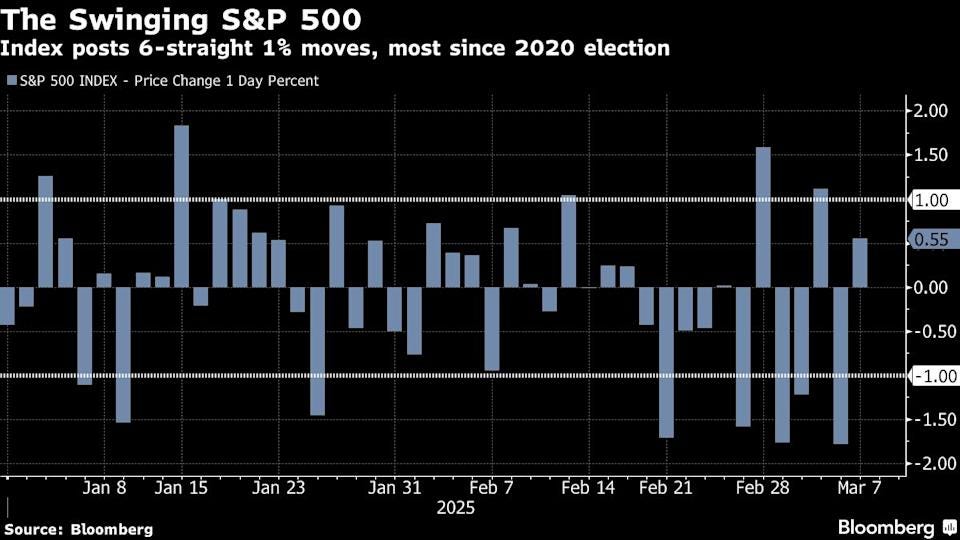

It’s becoming a pattern, of sorts …

Mon, March 10, 2025 at 5:55 AM EDT Bloomberg Markets Wrap: US Stock Futures Drop as Fears Mount for Economy

(Bloomberg) -- Wall Street stock futures dropped and Treasuries ticked higher as President Donald Trump’s protectionist policies and cuts to the federal workforce dented confidence in US economic outperformance…

… some serious ‘walatility’ !!

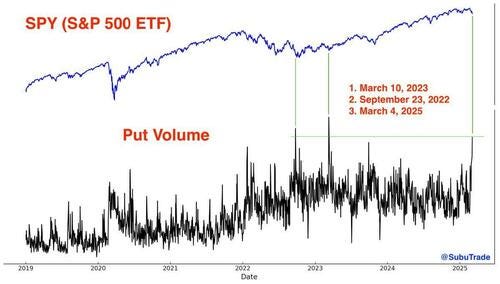

In concert with all of this, a note (and visual) of record activity in the week just passed ALSO should catch ones eye …

ZH: This Week Saw The Biggest Put Option Volumes, Ever Monday, Mar 10, 2025 - 02:35 AM

Stop us if you've heard this (spoiler: you have). According to Goldman's derivatives desk, after a week that saw a ton of pain and risk transfer in equities, the equity volatility market is starting to flash some signs of stress…

…Which brings us to the most remarkable chart in the latest Weekly Rundown note: as Garrett notes, the levels of put option volumes (on a 5-day moving average) were unprecedented, underscoring the record flow on the downside this week.

Goldman goes on to point out that SPY put volumes spiked on Tuesday to the 3rd highest in history. What is notable here is that the previous 2 put spikes were bottoms for the S&P 500... yet this week stocks continued on to make new lows later on.

AND .. the table was / IS set for the week ahead …. the problem with all this is it injects a (F2Q)BID for bonds as we head into the week filled with UST supply ($58bb 3yr tmrw, $39bb 10s on Wed and $22bb bonds on Thurs) — oh well, perhaps a concession (from richer levels) can be had in hours ahead.

CPI and UoMISSagain be damned … lets get this party started, shall we … here is a snapshot OF USTs as of 711a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are firmly bid with the belly richening (2s7s30s -3bps) as WH comments on "a period of transition" for the US economy added to concerns about a potential growth slowdown. This leaves S&P futures -1% at 7am, modestly under-performing Eurostoxx (-0.6%) as the UST-Gmy differential further tightens with EURUSD +0.3%. Crude is +0.3%, Copper -0.5%, and Gold -0.3%. Our desk has seen light buying interest, but limited conviction from the account base to chase the move and early LDN price action was completely bund-led. Into US hours, we've seen light selling from EM and credit accounts in 10s.

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWKUS Market Open: Downbeat sentiment with US equity futures in the red, whilst USTs gain … Bonds are propped up by a deterioration in sentiment, offsetting initial Bund pressure on fiscal-related developments … USTs picked up at the reopening of trade, given the pressure in US equity futures and as the benchmark acknowledged the soft Chinese inflation data on the weekend. The risk-off tone has intensified further with USTs outperforming and at a 111-03 peak, resistance at 111-11+ and 111-15 from last week. Market focus is firmly on tariffs/trade with new measures set to come into play on metals on Wednesday and the prospect of reciprocal tariffs being implemented imminently. Furthermore, President Trump’s sights seem to have turned back to the EU, with him labelling the bloc as a terrible abuser. Finally, focus is also on fiscal matters as the Friday deadline to pass a funding bill to avoid a federal shutdown fast approaches. The House Republicans released their CR on the weekend and following this Punchbowl writes that it does not feel as if a shutdown will occur.

…Although the weekend was relatively quiet we did hear from both Bessant and Trump and they seem to be telling us that they are prepared for some pain to reorientate the economy. Bessent said, “Could we be seeing that this economy that we inherited starting to roll a bit? Sure. And look, there’s going to be a natural adjustment as we move away from public spending to private spending,” “The market and the economy have just become hooked. We’ve become addicted to this government spending, and there’s going to be a detox period.” Meanwhile Trump told Fox that “There is a period of transition, because what we’re doing is very big. We’re bringing wealth back to America. That’s a big thing.” “What I have to do is build a strong country. You can’t really watch the stock market,” “If you look at China they have a hundred-year perspective". So taken at face value these quote suggest that their pain level is higher than most would have believed a few weeks ago.

Also over the weekend the House Republicans propose a stopgap funding bill taking us to the end of September, attempting to avert a shutdown on March 15th (this Saturday). There will be a vote tomorrow with some House Republicans not that keen to vote for a stopgap that doesn’t contain permanent spending cuts. However the tougher challenge will be when the bill hits the Senate as it will require moderate Democrats to support it for it to pass. One of the issues is that the bill explicitly gives DOGE the licence to carry on what’s it’s doing which may be a struggle for Democrats to support. So one to watch…

…Over the weekend Chinese inflation fell -0.7% YoY, below the consensus -0.4% and the -0.5% last month. Core inflation fell -0.1% YoY, the first decline since 2021. PPI printed at -2.2% YoY against -2.1% expected and -2.3% the previous month. Overall there was likely some distortion due to the timing of Lunar New Year so we'll get a better read next month…

Same shop on CREDIT (a proxy for risk, and so, stocks … and a graphic / caption which caught MY attention) …

DB: The US Pinball Machine Flashes Tilt? 10 March 2025

…In our view, this certainly implies rising rate volatility. The shift to a reactive central bank posture greatly lowers the odds of getting “risk-friendly rate cuts”, which is ultimately needed to justify today’s credit valuations. For the most extreme example: $HY yields of 7.3% are only 280bps higher than the current Fed Funds rate of 4.5%. This is near the lowest on record, going back to 1988 (Fig 1). We would need 7 additional risk-friendly Fed cuts through the cycle, for current $HY yields to provide an average risk premium over cash (going back to 2014). It is far more likely to us that $HY will simply sell-off, for a normal risk premium to start being restored…

… on a growth risk which matters to stock jockeys …

Price action supports our long-standing view that policy would likely be sequenced in a more growth-negative way to start the year before lower deficits/rates and less crowding out of the private economy benefit the market later in the year. Relative value trades offer the best risk-reward for now.

No Pain, No Gain...Policy uncertainty, fiscal drag, DOGE, immigration enforcement and the lagged impact of higher rates and a stronger dollar have come together to pressure earnings revisions. As a result, we've seen choppy index performance that has been contained below the ~6,100 level on the S&P—in line with the views we laid out last November. Our work on the tariff risk to earnings and fiscal headwinds suggest that the low end of the first half range is ~5,500. Our year-end 2025 base case price target remains 6,500, though the path is likely to be volatile as the market continues to contemplate these growth risks for the time being. This fits with our long-standing view that policy would likely be sequenced in a more growth-negative way to start the year before lower deficits/rates and less crowding out of the private economy benefit the market later in the year—No Pain, No Gain.

A Familiar Pattern...The 10-year yield has come down by about 50bps since the middle of January which suggests that the economic surprise index should start to turn higher again over the next several weeks based on the historical relationship between these two series. Further, dollar strength (a headwind during 4Q earnings season for multinationals) has now reversed as the DXY is now down 6% since the middle of January. Finally, seasonals for both earnings revisions and index performance improve over the next few weeks. The combination of all three factors could provide support later this month near the lower end of our trading range (~5,500).

Relative Value Trades...The quality factor is outperforming YTD, and we think it makes sense to stay up the quality curve as the market continues to digest policy uncertainty (relevant screens are in last week's note). We see outperformance of Consumer Services over Goods continuing as tariff risk has led to a further breakdown in the relative performance of Discretionary Goods. Our Software over Semis trade continues to show positive price momentum. Software earnings revisions continue to show relative strength, and the industry is in a strong position to drive both revenue growth and cost efficiencies through GenAI solutions. As Keith Weiss, our lead Software analyst, noted in his TMT Conference Wrap-Up: "We believe the combination of GenAI product cycles supporting durable growth and margin expansion potential creates a compelling FCF generation story for Software stocks."

… AND a view of the world impacting a set of f’casts …

As new facts about Germany, China and the US emerge, we revisit our forecasts.

Markets change. Plans change. Expectations change…and sometimes in the blink of an eye. New information means we have to question our forecasts. When asked what typically causes plans to change, former UK Prime Minister Macmillan responded, “events, my dear boy, events.” For the three biggest economies around the world, one now looks stronger, one about the same, and one a bit weaker…

…We continue to think the market is placing too little emphasis on immigration restrictions. Headlines do not tell the full picture, and we cannot yet conclude by how much immigration will fall this year, but we remain convinced that restrictions will both boost inflation and slow growth. Because the Administration has leaned into this policy, those risks seem to have grown since the beginning of the year, as well.

The timing remains uncertain, but all of these policies would skew negative for growth does now seem to be more accepted by markets. Recent market moves are consistent with this view, but some of the market reaction to soft data was likely overdone, in our view.

Overall, last week saw a crossroads of policy directions: the US is choosing disruption; Germany seems to have found itself a new credit card; and China seems happy to patiently wait to see how the policy experiments in the rest of the world play out before making a dramatic shift of their own.

Same shop with a thematic note — everyone’s talkin’ credit, so …

A quick rundown of key global credit research, including a downgrade of US growth, our concern about credit's resilience, a looming US government shutdown, attractive hedges, why more Fed cuts is not necessarily better, how AI spending gets funded, and our latest single-name credit research.

Weaker US growth and stickier inflation... Previously, our forecasts saw the solid US growth and moderating inflation of 2024 continuing through 1H25. Following more aggressive tariff policy, our economists now see weaker 2025 growth, stickier inflation, and a high bar for rate cuts or a policy 'put'.

...challenge the resilience of credit: Credit has been impressively low-beta. While this was previously our expectation, we are losing faith that it can persist, given the scale of the divergence and our forecast changes.

Not too late to hedge: We see a variety of attractive hedging opportunities, and discussed them in detail in a recent report…

A few words on inflation (USA) and deflation (China) …

China’s consumer prices moved into deflation in February. Some of this is due to the timing of the lunar new year, and some of it is the impact of warmer weather on food prices (food has a higher weighting in China’s inflation calculation than in developed economies). However, markets are concerned that the low inflation environment does not suggest robust domestic demand.

US President Trump faces a different problem, conceding that there may be higher inflation ahead. While tariff retreats have been rapid, the threat may still allow companies to sell a story of necessary price increases. Some companies may also increase prices in anticipation of tariffs that never actually happen. The New York Fed’s survey of inflation expectations is due—not reliable as a prediction, but perhaps signaling whether consumers are concerned.

Trump also failed to rule out a recession. After the 2024 soft landing, markets are getting more concerned about economic growth risks. As the pandemic illustrated, supply chain disruption can be create growth problems. Disruption to trade and government both raise risks…

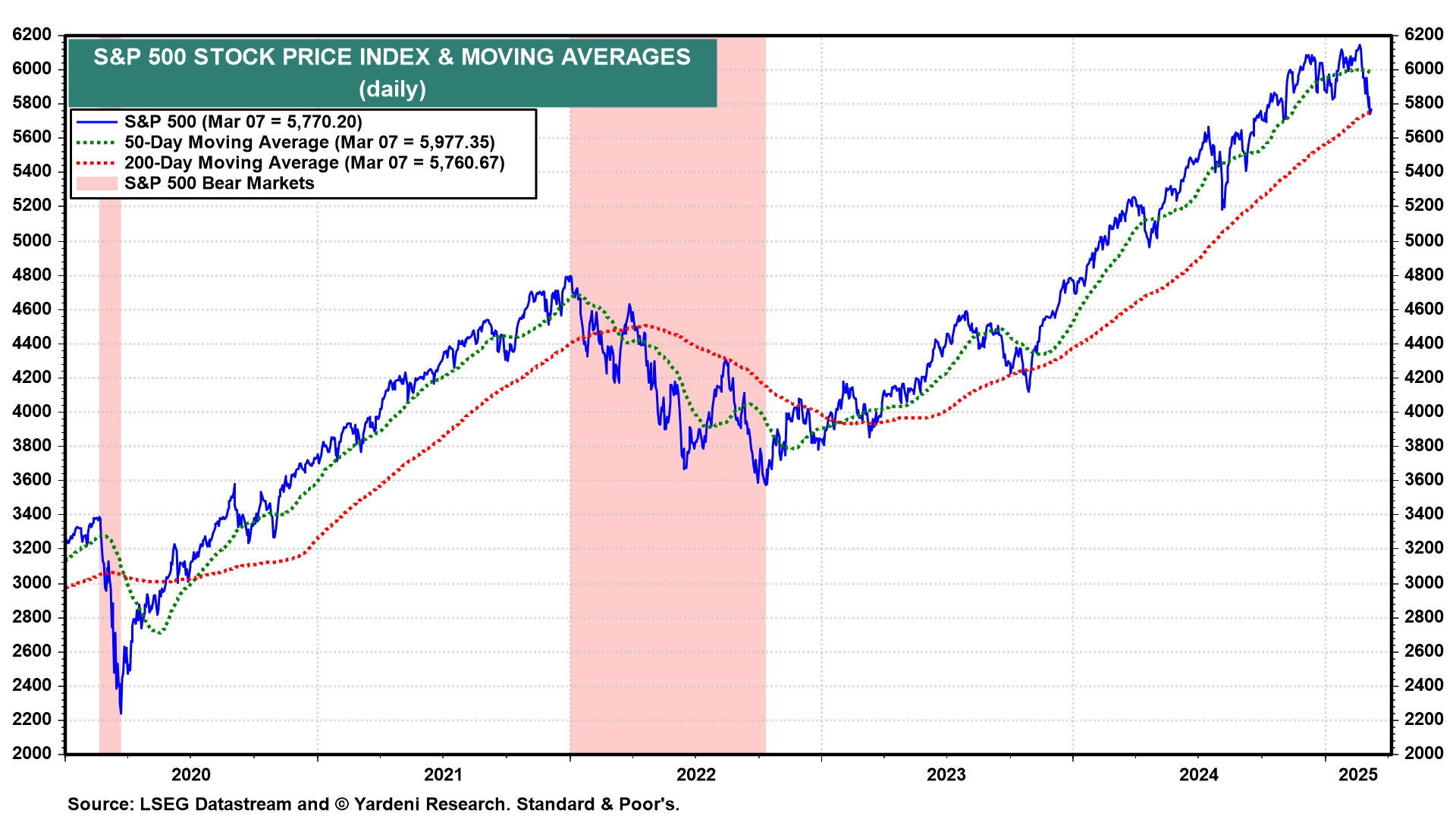

Anything is possible in Trump World. We can't rule out the possibility that a bear market started on February 20, the day after the S&P 500 rose to a record high (chart). It could be like the "flash crashes" that occurred during 1962 and 1987. It could happen quickly and reverse just as quickly. So the selloff could provide buying opportunities, especially in overvalued names that are now less so.

For now, the problem is that the Trump administration's rapid-fire policy initiatives are stress-testing the economy, which has been remarkably resilient so far, and raising fears of a recession.

Trump officials have heightened those fears in recent days. Today, in an interview with Maria Bartiromo on Fox News, the President himself refused to rule out a recession this year and said that the economy is in "a period of transition." He also acknowledged that tariffs might fuel inflation. On Friday, US Treasury Secretary Scott Bessent said that the US economy may slow as it transitions away from public spending toward more private spending, calling it a "detox period" needed to reach a more sustainable equilibrium.

The administration's policies that are currently being implemented (federal job cuts and tariffs) increase the risk of a stagflationary outcome. We give that scenario a 35% subjective probability, which we raised from 20% last Wednesday. But the stock market seems to be signaling that stagflation is even more likely than we think given how quickly stock prices have dropped since February 19…

… and finally, a look at the economic week ahead from Dr. Bond Vigilante …

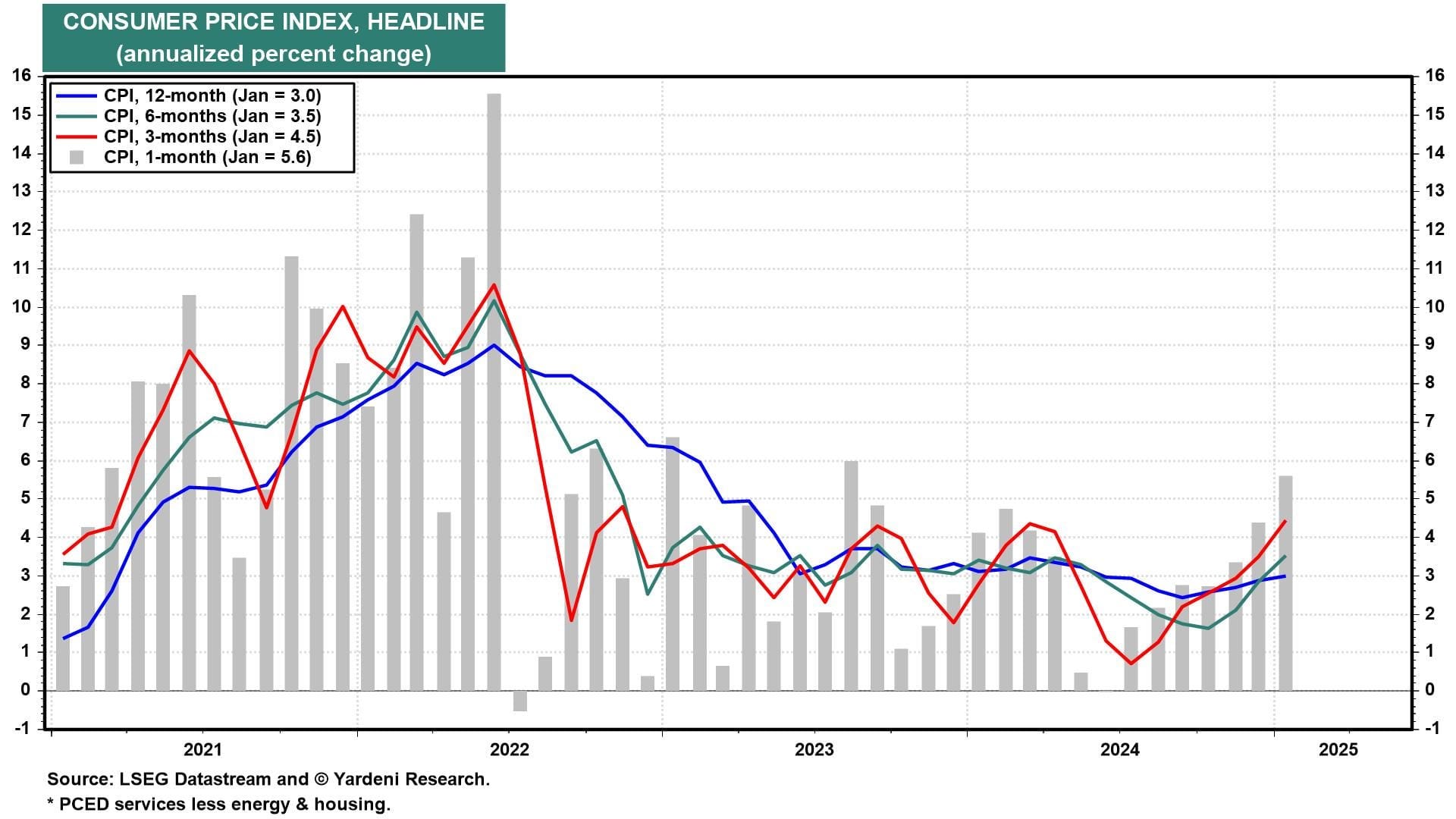

After several weeks of a growth scare, the attention this week will shift back to inflation. The new scare could be stagflation, which is the risk to our more upbeat economic outlook. CPI inflation has been reaccelerating since last fall when the Federal Reserve cut interest rates by 100bps (chart). Businesses may have raised prices in February in anticipation of tariffs.

If CPI services inflation remains sticky at January's rate of 4.2%, then reviving goods inflation could raise overall inflation in coming months. While the market expects three Fed rate cuts this year, we continue to believe inflationary pressures will keep the Fed on pause for the remainder of the year (chart). We also expect the economy to remain more resilient than widely expected currently, though we did raise our odds of a recession from 20% to 35% last week.

Here's more on what to expect in the week ahead..

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

An OpED from The Terminal …

March 10, 2025 at 8:30 AM UTC Bloomberg: The Fed’s Fixation on a 2% Inflation Target Is Risky The central bank needs to be open to reconsidering what’s appropriate in a world where adverse supply shocks are more common. By Mohamed A. El-Erian

…The bottom line is simple. The world’s pre-eminent central bank must have the potential to act as a durable bulwark of price and financial stability and a purveyor of maximum employment and lasting economic well-being. To preempt any internal review of its inflation target is imprudent. It risks more than unduly damaging jobs and incomes. It can also inadvertently result in an erosion of the Fed’s institutional credibility and political autonomy.

Another OpED from The Terminal (with a few words on Friday’s NFP…)

March 10, 2025 at 5:01 AM UTC Bloomberg: The ECB Won’t Escape Europe’s Earthquake ‘Evolving’ monetary policy needs to cope with greater German borrowing and the tremors it will send. By John Authers

…Fork in the Road Is the US really sliding into a recession? Such fears have plainly taken hold in recent weeks, and February’s jobs report was the latest test to come back from the lab. It at least suggests the patient doesn’t have much to worry about. That won’t mean that we can ignore worrying signs that cause genuine concern, such as softening consumer confidence, mass federal job layoffs, economic policy uncertainty, and rising inflation expectations. But the report suggests that the infections that might lead to a recession diagnosis remain at the latency stage, even if all the main measures are gently trending in the wrong direction:

The biggest market concern is about the chance of a recession. Unemployment tends to rise slowly and then surge. The Sahm Rule, named for Bloomberg Opinion colleague Claudia Sahm, holds that when the unemployment rate is more than a half percentage point above its low for the previous year, a recession ensues. That threshold was triggered last year, contributing to a scare. Now, it suggests little reason to worry:

A revision of the Sahm Rule by BCA Research’s Dhaval Joshi (dubbed the Joshi Rule) looks at the three-month moving average of the unemployment rate of “job losers not on temporary layoff,” or “bad” unemployment. When it rises by 0.2% from its low during the previous 12 months, it means a recession is coming. This measure, as Joshi shows, has eased even more dramatically:

This helps explain why markets generally responded with muted relief to the jobs numbers. But there were warning signs in more long-term unemployed people, fewer federal workers, and an increase in those working part-time for economic reasons. People working multiple jobs reached a record of nearly 8.9 million. But overall, nonfarm payrolls were up 151,000 in February following a downward revision to the prior month, continuing a “Goldilocks” trend in which jobs rise, but not too fast:

The headline fell short of estimates, but that could be attributed to weather disruptions, and to job cuts from Elon Musk’s Department of Government Efficiency. Negligible revisions for the previous two months were also reassuring. But the numbers didn’t reverse the growing concern in recent weeksabout a recession. This is how the forecast by Bloomberg’s World Interest Rate Probabilities, derived from futures, has moved since Jan. 2:

The change in interest rate expectations is unmissable. However, the latest jobs report seemed to arrest the trend:

For rates to fall this much, the Fed will need to be be convinced that employment faces a significant deterioration. Oxford Economics’ Nancy Vanden Houten argues that this report wasn’t enough to move the Fed off the sidelines. Glenmede Research’s Jason Pride adds:

Given uncertainties regarding trade policy, June may be a live meeting for them to consider restarting the rate-cut process if they judge a material impact on aggregate demand. The base case is now ~3 rate cuts this year, but those expectations may be volatile until the size and scope of trade policy come into greater focus.

The impending fork in the road for the Fed makes for an interesting watch. Bank of America’s Shruti Mishra argues the disappointing household survey and solid wage growth are consistent with mild stagflation. With inflation already above target, however, Mishra argues that the Fed won’t cut further — although markets may worry about the risk that if it’s too slow to act, that may exacerbate the eventual downturn.

Have a great start to your day and the week ahead. Good luck as you plan your CPI trades and TRADE your CPI plans … THAT is all for now. Off to the day job…