Overnight, the USA conducted more (4th) airstrike on Houthi rebels AND Pakistan has struck militant bases inside IRAN which, as you’d imagine, ‘… stokes regional tension’ (Reuters).

Shocking then to see a touch of a BID to US rates complex this morning? Specifically, just like in ‘the old days’, the front-end catching most of the F2Q flows (except to say there’s not ‘typical’ FLIGHT from equities … perhaps the ‘flight’ here is from sidelined cash — more on that from WSJ just below…!)

I’ve attempted to HIGHLIGHT (RED) uptrend which is being revisted (and comes in just NORTH of 4.25%) while momentum (stochastics) is firmly in ‘NO MANS LAND’.

THAT (all of yesterday … data and markets and this mornings geopolitical news) didn’t go exactly as any one planned. But then again, does it ever? Thats why they are called surprises, I suppose.

Now forgive me if I sound confused … A quick walk through some of the snark that was yesterday, via ZH as … well, one might have thought ReSale Tales STRENGTH was good as far as yesterday’s 20yr auction was to go …

ZH: Retail Sales Surged In 2023 Led By Autos & Food Services, Gas Station Sales Slumped

… But wait, not ALL was good news …

ZH: Capacity Utilization Hits 2-Year-Low As Downard-Revisions Flatter December Industrial Production

… all told, combined, it would appear NOT to have mattered as far as mustering up a bid for 20s …

ZH: Ugly, Tailing 20Y Auction Whimpers Out Amid Bond Market Rout

… Which was a great setting then of the table for … a BEIGE colored econ via Beige Book …

ZH: Beige Book Finds "LIttle Or No Change" In Economic Activity But Optimism Rises On Hopes Of Lower Rates

…and about those HOPES (not a strategy) then of economic optimism thanks to lower rates …

ZH: 'Good News Is Bad News' As Goldilocks Reality-Check Wrecks Dovish Dreams

Retail sales - strong; Housing - homebuilder optimism jumped; Industrial Production - better than expected.

'Real' economic data is rising once again as 'soft' survey data collapses (Empire Fed anyone?)...

…Nothing there screams "six rate-cuts or we all die" as the issue remains: the current growth trajectory of the economy does not suggest that rates need to come down at all.

And as this growth/rates tango persists, yields on 10-year Treasuries are creeping higher (up 4bp today to 4.10%), putting pressure on risk assets that are priced relative to rates.

Today's strong data, along with last week's slightly higher than expected inflation report may suggest to some that rate cuts may not be as necessary as urgently as markets have been pricing.. and Waller's comments yesterday pre-inforced that.

Sure enough, rate-cut expectations (timing and size) are tumbling...

… Those dovish dreams creeping back into lexicon a bit as rates complex better bid with front-end leading and so, here is a snapshot OF USTs as of 706a:

… HERE is what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are higher as Middle East tensions ratchet higher with Iran and Pakistan now lobbing missiles at each other. A downside miss in Aussie employment helped Treasuries too. DXY is modestly lower (-0.12%) while front WTI futures are modestly higher (+0.3%). Asian stocks were mixed but there was a late rally in beaten-down Chinese shares, EU and UK share markets are all higher (SX5E +0.8%) while ES futures are showing +0.4% here at 7am. Our overnight US rates flows saw Treasuries supported during Asian hours by an Aussie jobs miss (link above) though a weak JGB 20-year auction knocked some of the early froth off (as did a -3k TU block sale). In London's AM hours, an 8k block buy of TY futures supported prices and dip buying in 2yrs from real$ was noted too. Overnight Treasury volume was ~85% of average overall.

… and for some MORE of the news you can use » The Morning Hark - 18 Jan 2024 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

ONE THING TO MENTION …

WSJ: The $8.8 Trillion Cash Pile That Has Stock-Market Bulls Salivating

Wall Street hopes trillions in money-market funds will flow into stocks and bonds. Investors have varying plans.

… “Every month, I’m looking at inflation,” he said. “If I’m not earning at least 1.5% more than inflation, I have to think about different strategies.”

What Trivedi and others decide is key to what happens next in markets. Expectations that the Federal Reserve will cut interest rates later this year spurred big rallies at the end of 2023, driving major indexes near records. That heat is beginning to dissipate. Some investors say markets have little room for further gains and are already priced for a perfect scenario, in which inflation moderates without significant job losses.

… Investors also tend to tap money markets during periods of market stress, not necessarily when yields are higher. Assets in money funds peaked at nearly half of the overall money supply in 2008. There was a similar spike in 2001, the aftermath of the dot-com bubble.

… “If rates fall below 3.5%, I would probably cut the amount I’m putting into my savings and instead direct deposit to my investment brokerage or crypto,” he said…

AND there you have it … rates BELOW 3.5% = (moar)bullish CRYPTO! The new math!

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ … lot of ReSale Tales victory laps and i told ya so to get through so without further adieu …

BARCAP: US Economics: Retail sales: No Grinch here (bah humbug)

Consumer spending reaccelerated at the close of 2023, with headline and control group sales both registering outsized December gains on top of strengthening auto sales reported earlier this month. These data mark up further our Q4 GDP tracking estimate, and imply a strong carryover effect for the current quarter.

BNP: Front-end center: Diving deeper into Fed QT taper

We believe QT taper is not a precursor to an imminent halt to balance sheet runoff. Reserves are still plentiful and the Fed has an array of new tools at its disposal to identify early cracks in liquidity.

Upward pressure and volatility on funding costs are nonetheless expected as RRP facility balances reach zero and the Fed approaches an efficient balance sheet level.

Given recent widening, we see this is a good opportunity to enter into a 2y SOFR/FF tightener as the Fed enters a liability-driven floor regime and repo activity is exacerbated by added US Treasury issuance.

BNP: US rates: How soft core PCE could boost breakevens

Increased Fed emphasis on core PCE when there is a wide core CPI-PCE wedge creates upside risks to breakevens in our view.

If the market perceives there is less chance of the Fed remaining too tight for too long, it can be a tailwind to breakevens.

We like being long traded inflation on an outright basis and as an overlay to a steepening view.

Trade idea:Buy 5y breakevens (TII 2.375 10/28 vs T 4.875 10/28). Entry: 2.255%…

Goldilocks: Retail Sales Accelerate to End 2023; Industrial Production, NAHB, Core Import Prices Above Expectations; Boosting GDP Tracking

BOTTOM LINE: Core retail sales rose 0.8% in December, capping a year of at-or-above consensus readings. Spending rebounded in several brick-and-mortar categories and rose further for nonstore retailers, and the level of November sales was revised up by 0.1%. Industrial production increased by 0.1% in December and manufacturing production increased by 0.1%, both somewhat above consensus expectations. Both import prices and import prices ex-petroleum were flat in December, each above consensus expectations. Following this morning’s import price data, we raised both our December core and headline PCE inflation estimates by 1bp to +0.18%, corresponding to year-over-year rates of 2.94% and 2.61%, respectively. Business inventories decreased slightly in November, in line with consensus expectations, and the October growth rate was unchanged. The NAHB housing market index increased in January, well above consensus expectations for a smaller increase. Following today’s data, we boosted our Q4 GDP tracking estimate by 0.3pp to +1.8% (qoq ar) and our Q4 domestic final sales growth forecast by the same amount to +2.5% (qoq ar).

Inflation data exhibit outsized volatility and cyclicality in January as firms reassess pricing at the start of the year—a phenomenon we call the “January effect.” In today’s Daily, we test the January readings of core CPI and core PCE against a set of economic variables that could theoretically generate a January effect.

We find that the slower pace of unit labor cost inflation and the normalization of inflation expectations argue for a smaller January effect this year for both core CPI and core PCE: we estimate a temporary boost to month-over-month core inflation of 0.1-0.15pp, compared to a boost of as much as 0.3pp in January 2023. Coupled with a rebound in apparel prices and a boost from the strong stock market heading into January, we forecast core CPI will rise 0.40% and core PCE prices will rise 0.34% in January (mom sa).

If monthly inflation indeed picks up, we would nonetheless expect the sequential pace to slow in February and March once these start-of-year adjustments have been implemented…

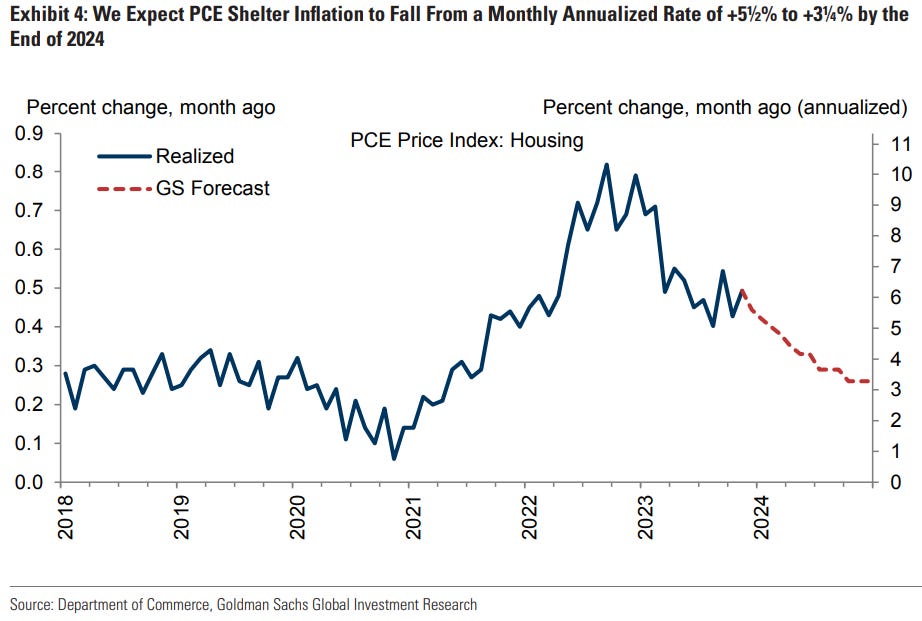

Goldilocks: Shelter Inflation: Back to the Pre-Pandemic Pace (it’s the what NEXT which matters more … some — Atlanta Fed, for ex — say the next part won’t be so ‘arduous’)

… The combination of a now-modest catch-up effect and a benign outlook for new-lease rent growth suggests that official shelter inflation is on course to return to pre-pandemic levels later this year, as the gap closes completely. We expect official shelter inflation of 3.9% on a year-over-year basis in 2024, with the sequential pace falling from 0.44% in December 2023 to 0.26% in December 2024—a touch below the 2016-2019 average of 0.28%. We expect shelter inflation to remain slightly below the pre-pandemic pace in 2025, though the outlook at that horizon is particularly uncertain.

JEFF: Dec Retail Sales Rise +0.6%, Control Group +0.8% as Consumers Refuse to Put Down the Cards

■ Headline retail sales rose +0.6% in December, with the control group +0.8%. The increases exceeded expectations. The 0.8% increase in the control group is the biggest sequential m/m increase since January 2023 (which was fueled by a nearly 9% increase in Social Security checks), and it comes off a larger base as November was revised to +0.5% from +0.4%. ■ The consumer spent money like there was no tomorrow in Q3, and we expected payback in Q4. We didn't get it. We don't yet know if this is just the last gasp of consumer strength fueled by traditional credit and buy-now-pay-later, or if this is a case of higher-end consumers picking up the slack from their less fortunate counterparts, but either way, consumer demand has been durable. ■ January sales will be boosted by another increase in Social Security checks, but the increase is going to be about 1/3 of the increase last year. We will be watching closely to see if the pullback that we anticipated in the holiday season instead manifests in Q1. ■ The increase in the control group this month, along with the upward revision to October, suggest that PCE will be up +0.4% m/m in December in nominal terms, and +0.2% m/m in real terms. This implies a +2.5% annualized increase q/ q that should drive GDP growth of 2.1% in Q4.

MS: Do US Elections Change Fed Policy in Election Years? (stratEgerists SAY NO…)

Do upcoming elections in the US influence FOMC monetary policies during election years? We think the answer is "no" – an uncommon answer to a common question. We offer two perspectives from inside the walls of the Marriner S. Eccles Federal Reserve Board Building.

Key takeaways

The election in November does not change our baseline view that the Fed will lower rates starting in June and at every meeting from September to December.

FOMC participants understand, but dismiss the "conventional wisdom" among investors that elections might interfere with policy decisions.

FOMC participants often discuss the uncertainty that elections bring to consumers and businesses and the economic impact before and after elections.

Economic recessions distract from elections, e.g., 1990 and 2008. Fiscal policies put focus on elections, e.g., 2012 (fiscal cliff) and 2016 (fiscal expansion).

FOMC transcripts confirm that while the Fed may discuss elections when fiscal policy is in focus, there’s no evidence it acts in anticipation of an outcome.

UBS: December core PCE tracking lower, strong retail sales

Core PCE price tracking nudged down after import prices: 0.15%…

Retail sales strong in December; prior months revised up…

US import prices flat in December as fuel stalls…

UBS: Beige Book reveals holding pattern, Waller balances risks

According to the Federal Reserve's Beige Book — a summary of anecdata and surveys of regional business contacts — US economic activity was little changed relative to the prior reporting period. The report, which reflected data collected on or before January 8, stated that three districts reported modest growth, one (Kansas City) reported a moderate decline, and the remaining eight noted no or negligible growth. The prior survey ended on November 17 and was more downbeat, indicating that activity, especially consumer expenditures, had "slowed."…

UBS: The inflation impact of the spike in global shipping costs is likely (very) small (wow, good to read just not sure i’m buying in but still … what a relief, just HOPING they are right)

The disruption to global sea freight is significant…

And our global supply chain tracker has deteriorated by nearly 1½ stdev…

But this is very different from the Pandemic supply chain stress…

The impact from shipping costs alone to inflation is likely very small Although freight costs skyrocketed during the pandemic, these had relatively little to do with the inflation surge. As we show in Figure 9, the cost of freight and insurance, as a % of total US import costs for instance, increased from roughly 2.7% to just 4.1%, despite a 700% increase in global shipping cost at the peak (and a 5-fold increase on the specific shipping routes shown in that chart). Roughly speaking, the historical relationship is that for every 10% increase in freight costs, overall US import costs increase by only 3.2bp. In the last 2 months, US freight costs are up roughly 64%. So 64 * 0.0032 = 20bp. However, to gauge the impact on CPI one needs to see what share of consumption is imported. Answer: the level of monthly goods imports equates to 16.5% of monthly consumption (those imports are not just for consumption but also capex/production but let's assume full pass-through of intermediate cost to final consumption). So multiply 20bp * 0.165 = 3.3bp worth of monthly inflation. However, even this is an overstatement as less than 50% (47% in 2022) of trade enters the US by ship. So multiply 3.3 by 0.47 and you have less than 2 basis points inflation impact for the increase in freight costs so far. There are other indirect effects like higher energy costs or the impact of delivery delays, but the freight cost impact itself is small.

UBS (Donovan): Never short the hedonism of the US consumer (see what I mean…)

Markets seemed surprised that US December retail sales were stronger than expected. This is weird—some part of US retail sales data surprised positively every single month during 2023. Never go short the hedonism of the US consumer. The Federal Reserve’s Beige Book suggested leisure travel also benefitted. However, unlike 2021/22 this spending is unlikely to be indifferent to prices— but instead to be a response to price discounting.

The US consumer is important in preventing a soft economic landing from becoming a hard economic landing. This data is still consistent with a soft landing this year. However, a soft landing requires a neutral monetary policy (stable real interest rates), not monetary stimulus—which makes the more extreme bets on US rate cuts unlikely…

Wells Fargo: Moderation in All Things... Except Consumer Spending

Summary Today's retail sales report for December showed consumer spending picked up speed in the final month of the year. Not all the dollars spent found their way into holiday spending categories, but a surge in control group sales means upside risk for Q4 PCE forecasts.

… And from Global Wall Street inbox TO the WWW,

Apollo: Will 2024 Be a Repeat of 2023? (learning from history or being doomed to repeat it?)

The story in markets in 2023 was that US growth expectations were first revised down and then revised up after the easing in financial conditions following SVB in March, see the first chart below.

With the significant easing in financial conditions since November, we are beginning to see the same pattern in 2024, see the second chart.

The performance has been different in Japan and Europe, where growth expectations have been steady in Japan and revised significantly lower in Europe.

In other words, the lack of a slowdown in 2023, which surprised the Fed, the consensus, and markets, was only a US story, and we are starting to see the same pattern play out again in 2024.

Atlanta FED: Business Inflation Expectations Decreased Significantly to 2.2 Percent – January 17, 2024 (well THATs good news and worth at least 6 cuts, right?)

Inflation expectations: Firms' year-ahead inflation expectations significantly decreased to 2.2 percent, on average.

Current economic environment: Sales levels and profit margins "compared to normal" increased. Year-over-year unit cost growth significantly decreased to 2.7 percent, on average.

Quarterly question: Firms' sales levels (compared to "normal" unit sales levels) decreased to 5.3 percent below normal.

Special question: Firms were asked about their most pressing concerns looking ahead into 2024. They were also asked about their turnover rate. A breakdown of the results can be found in the special questions section below.

Bloomberg (via ZH): Stocks Are Still Blinded To Risks By Rate-Cut Optimism (before ReSale TALES)

Bloomberg(via ZH): Fed Pressing Higher-For-Now Against Market's Lower-And-Sooner (well after ReSale Tales and before auction)

FirstTrust: Data Watch - Retail Sales Rose 0.6% in December

… Implications: Retail sales beat expectations in December, rising 0.6% for the month, while nine of the thirteen major categories moved upward…The problem remains that one of the key drivers of overall spending is inflation. Yes, retail sales are at record highs unadjusted for inflation, but in “real” (inflation-adjusted) terms, they have been stagnant. Real retail sales peaked back in April 2022 and have since declined by 1.9% from that peak. It has been forty years since the US had an inflation problem, so it is important to remember that it can distort data. Our view remains that the tightening in monetary policy since last year will eventually deliver a recession. Expect more deterioration in real retail sales into 2024 as tighter credit conditions along with higher borrowing costs take their toll. In other news this morning, import prices were unchanged in December while export prices fell by 0.9%. In the past year, import prices are down 1.6% while export prices are down 3.2%, a sign of the tightening of monetary policy versus a year ago.

ING: US resilience suggests the Fed will wait until the second quarter before cutting rates

The jobs market is tight, inflation is above target, consumer spending is holding up and recent Fed commentary suggests they are in no hurry to loosen policy. As such we continue to favour May as the start point for interest rate cuts rather than March as the market currently favours

Investopedia Chart Advisor (clearly someone out there with a Terminal…)

… 4/ A Counter-Trend Bounce for the 10-Year Yield

For over a year, breadth, or the trend for the average stock, has had an inverse relationship with the direction of interest rates, specifically the 10-year. As yields dropped during the fourth quarter, small caps ripped higher, and the percentage of stocks above key moving averages expanded. As we flipped the page to a new year, yields were oversold, and stocks overbought, setting the stage for the current consolidation phase. The question then becomes, how much higher will rates reset? Chart 4 shows we can track a move to 4.25%, just about the 38.2% retracement level on the 10-year. Along the way, most folks will watch if the 50 DMA will be sustained (4.15%). At present, it is too early to call for a sharper move beyond 4.30%, let alone 4.5%, but the yield has been a helpful proxy for risk-on/risk-off sentiment; the longer it builds value above the 50 DMA, the stiffer the headwinds will become, and the continued consolidation in stocks.

5/ A Steeper Yield Curve is Weighing on Risk Sentiment

With the 10-year moving higher, we have the 2/10 curve at the steepest level since Halloween. A key technical theme of ours this year is whether the "momentum buy" signal on the monthly charts will lead to the curve turning positive and the impact it will have on risk sentiment. Turning the curve positive has led to higher stock values looking out one year later, but the degree to which it steepens becomes problematic. In the past, 40bps or more have been associated with equity market corrections/bear markets and a recession. We are nowhere near that, but folks are starting to alter positioning.

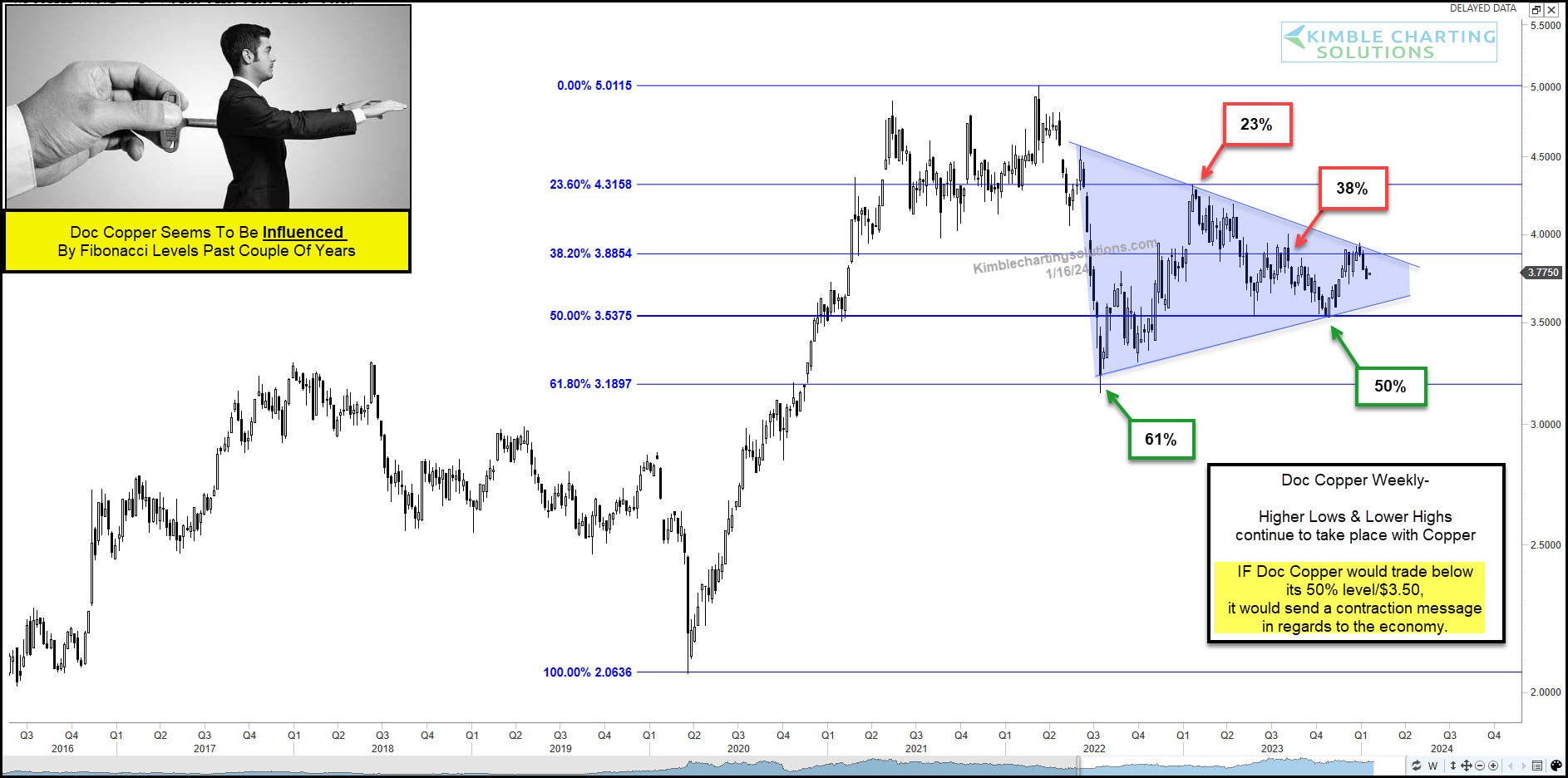

KimbleCHARTS: Is Copper About To Send A Macro Economic Message To Investors? (he reports, you decides)

WolfSt: Our Drunken Sailors Push Back Against Rate-Cut Mania (ReSale Tales recap)

Armed with income increases that outran inflation by a wide margin in 2023, they continue to splurge, no matter what.

Finally in light of the recent BTC ETF introduction, I thought this one from the intertubes was funTERtaining …

The Retail Sales number are not adjusted for Inflation....

Thus, Unit Sales Growth, not as strong as it looks....