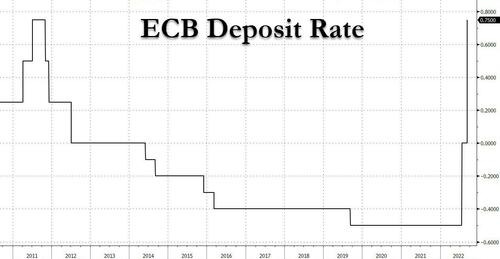

And we have the answer: after lots of heming and hawing, moments ago the ECB hiked its deposit rate by 75bps from 0% to 0.75bps, the first time European rates are positive in over a decade (since July 2012) noting that "the Governing Council’s future policy rate decisions will continue to be data-dependent and follow a meeting-by-meeting approach." Of note, the ECB said that following the raising of the deposit facility rate to above zero, "the two-tier system for the remuneration of excess reserves is no longer necessary" and "the Governing Council therefore decided today to suspend the two-tier system by setting the multiplier to zero."

And since today's hike is paltry when compared to Europe's runaway inflation which is almost in the double digits, the central bank said - not once but twice - that it expects over the next several meetings to raise interest rates further "because inflation remains far too high and is likely to stay above target for an extended period" and "to dampen demand and guard against the risk of a persistent upward shift in inflation expectations."

Remarkably, the ECB is hiking even as it writes the following in its statement:

After a rebound in the first half of 2022, recent data point to a substantial slowdown in euro area economic growth, with the economy expected to stagnate later in the year and in the first quarter of 2023. Very high energy prices are reducing the purchasing power of people’s incomes and, although supply bottlenecks are easing, they are still constraining economic activity. In addition, the adverse geopolitical situation, especially Russia’s unjustified aggression towards Ukraine, is weighing on the confidence of businesses and consumers. This outlook is reflected in the latest staff projections for economic growth, which have been revised down markedly for the remainder of the current year and throughout 2023. Staff now expect the economy to grow by 3.1% in 2022, 0.9% in 2023 and 1.9% in 2024.

In short, the ECB is hiking not into a recession but a full-blown depression, and it knows it.

here are the other highlights from the statement …

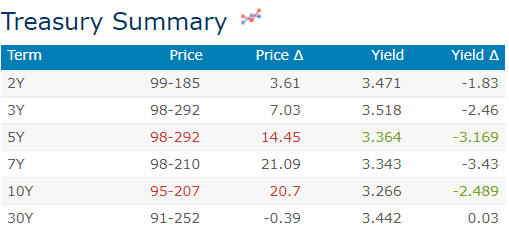

And now we know … what to expect come Sept 21 FOMC … here is a snapshot OF USTs as of 727a:

… HEREis what another shop says be behind the overnight flows in a morning commentary titled, ”Concession Watch”

… OVERNIGHT FLOWS Treasuries were modestly richer overnight with the 7-year sector leading the bid. Overnight volumes were low with cash trading at 88% of the 10-day moving-average. 10s were the most active issue, taking a 40% marketshare while 5s were a distant second at 24%. 2s and 3s combined to take 21% at 12% and 9%, respectively. 7s managed 10%, 20s 1%, and 30s 4%. We’ve seen light buying in 2s, 3s, and 5s.

… and for some MORE of the news you can use » IGMs Press Picks for today (9 Sep) to help weed thru the noise (some of which can be found over here at Finviz).

First Nick T of the WSJ, then GS and then everyone else. This morning, a large French bank joins ranks of everyone else,

We now expect the FOMC to hike rates 75bp at its coming September meeting (versus our prior expectation for a 50bp move).

Fed officials have not pushed back on market pricing aligned with a 75bp hike, and with an “overarching focus” on bringing down inflation, likely want fed funds comfortably at short-term neutral levels before broaching a discussion of a downshift.

With fed funds now set to hit 3.25% at the September meeting, we expect the Fed to proceed more cautiously toward the terminal rate—highly sensitive to evolving economic conditions.

We expect the Fed to hike a further 25bp in both November and December before holding fed funds at a 3.75% terminal rate through 2024.

But wait, there’s even MORE … yesterday, via JEFFeries.

■ Until recently, we had thought that the moderation in inflation and inflation expectations would allow the Fed to slow the pace of hikes to 50bps at the September meeting. ■ However, the recent uptick in growth momentum, reinforced by improving survey data, create a problem for the FOMC which wants to see growth slow, not accelerate. The recent JOLTS data are also problematic as they suggest the Fed has made very little progress narrowing the supply-demand imbalance in the labor market. ■ In light of the above, we expect the Fed to continue front-loading hikes and deliver another 75pb increase at the next meeting. This will likely be followed by a 50bp in November and 25bp in December. ■ We are not changing our estimate of the terminal rate, and still expect the funds rate to peak 4-4.25%, now likely to be reached in January (vs. March under our previous base case). The dollar is likely to deliver an additional 100bps of tightening, so a 4% terminal rate will feel more like 5%, knocking off more than 2 ppts from 2023. We believe this is enough to put the US economy in recession by 2H'23 and ultimately bring inflation back to 2% (though not until 2024).

And now a few words from UBSs Paul Donovan, touching on The Queen, China CPI, ECB and JPOW

Economics stresses the importance of having the right person, in the right job, at the right time. Her Majesty Queen Elizabeth II was born at the end of the second industrial revolution, and reigned over the third and the early years of the fourth industrial revolutions. The value of Her Majesty’s consistent leadership, inclusivity, and adaptability across an era of so much change has been considerable.

China’s August producer and consumer inflation data slowed. This reflects weak domestic consumer demand. While US and European consumers have been willing to use savings to support consumption, Chinese consumers have tended to hoard savings as a precaution against zero-COVID policy measures.

ECB President Lagarde is set to speak, but is unlikely to add anything new after yesterday’s press conference. The euro strengthened a little overnight—had there been weakness, there may have been additional comment from Lagarde. Some signals were given as to a relatively limited duration of policy tightening.

Fed Chair Powell’s speechwriters gave a hawkish tone to comments yesterday. The June policy errors mean that markets can have limited confidence in guidance, when a rogue statistic can clearly change the Fed’s policy stance. Tightening expectations are entrenched, and market attention is more on how significant the risk of a slump is.

And here are a few words from GALLUP (via ZH w/link)

Finally, from the CHARTS department, a couple things crossed my inbox which I thought might be of interest. First, whenever a retail related site out selling AllStarCharts touches on yields, well, you KNOW it is true. Nothing (higher rates) happens without consequence …

After Federal Reserve Chair Jerome Powell’s remarks this morning, the market is pricing in an 86% chance of a 75-basis-point hike later this month.

Meanwhile, rates continue to accelerate at the short end of the curve. That’s been the story for months now.

But will the middle and long end of the curve head higher as well?

According to the two-year US Treasury yield, the answer is a resounding “yes!”

Short-duration rates offer plenty of valuable, leading information regarding US Treasury yields.

We’ve leaned on the five-year yield throughout the current cycle as an early indication of the direction of the 10- and 30-year. It’s proved a beneficial practice.

Today, we’re going to drop it down a notch, extending the same logic to the two-year yield.

Here’s a quad-pane chart of the two-, five-, 10-, and 30-year US Treasury yields:

Starting in the upper-left corner, the two-year is well above its former 2018 highs and hitting levels not seen since November 2007.

The rest of the pack has also reclaimed their prior cycle highs marked by the 2018 peaks. But year-to-date highs remain a hurdle.

If the two-year is any indication, those former highs only represent a temporary obstacle.

But there’s more evidence overseas hinting that rates are on the rise across the curve.

If the bond market is flashing “sell” signals, we’re making the bet that rates will continue to climb.

As long as this is the case, we want to position ourselves in areas of the market that reap the most reward from rising rates, such as materials, energy, and financials…

ALSO from the CHARTS department from a Swiss bank which used to be domiciled in Beantown,

…10yr US Bond Yields need to break below 3.195/18% to confirm a short-term top, with key short-term support moving to 3.365% and then more importantly at 3.50%.

… Short-term Strategy: We turn tactically neutral on our tactically bullish bias from 3.20%

And an update on tactically bullish call out the curve …

30yr US Bond Yields remain capped by the 2022 highs at 3.495/515%, however a break of 3.31% is needed for a more decisive rejection.

… Short-term Strategy: We turned tactically bullish at support at 3.395/40% and we see scope for a move to resistance at 3.05%, where we would turn tactically neutral. Next support above 3.40% is seen at 3.50%, a close above which we would also turn tactically neutral.

WATCHING … One last thing I’m watching is REALZ and specifically, noted by BBG HERE, the rate at which they have increased,

…Central bankers are mostly busy delivering the rapid policy tightening they gave fulsome notice was on the way when they met at Jackson Hole. Those at the ECB were perhaps the most noticeable as they matched Canada’s in hiking by three-quarters of a point this week. They’re even willing to do the same again next month, it seems. Fed Chair Jerome Powell delivered a speech within hours of the ECB decision to make it clear the US central bank has every intention of going similarly large later this month to retain leadership of the global deluge of outsized hikes.

Global bonds extended this year’s rout as a result, with Europe a particular laggard as the ECB removed a cap on how much interest government deposits can earn, seeing as rates are now above zero for the first time in a decade. A slew of yields popped to fresh highs, with the 30-year Treasuries rate reaching the most since 2014 and 10-year UK gilts surging past 3% to a decade-high. US benchmark real yields jumped to the highest since 2019 with the record pace of their increase piling the pressure on risky assets such as credit and stocks. The pain is even spreading to South Korea’s famously elite Gangam districts, with apartment prices there beginning to buckle.

The lingering concerns that rapid tightening will spur recessions did start to gain traction with some central bankers. The Reserve Bank of Australia hiked by half a point for a fourth-straight month early in the week, but a couple of days later Governor Philip Lowe signaled it may soon be time to slow down. And Poland already eased off to a quarter-point move as its economy sags. For now though, jumbo hikes remain the fashion, even as Fed researchers warned of the domestic and global damage the US central bank’s battle to tame inflation can do.

And as far as nothing without consequence (evidenced by latest Consumer Credit highlights above by ZH), here’s how every finance department conversation goes when attempting to buy a home / car