Good morning. JPOW has spoken and the bond market (and curve) is listening.

Global Wall St is, as usual, playing catch-up and recently issued forecasts and TLINESwill be adjusted and redrawn. Stops will be triggered. Financial conditions will tighten…TWITTER and FT.com

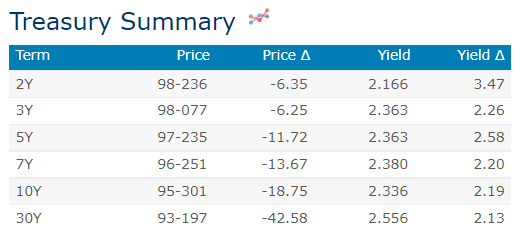

And then … something breaks and it is in this context, I’ll END this mornings brief rant with a reminder that, as shown over history, bonds do NOT suck…In the meanwhile, here is a snapshot of UST rates, prices and moves as of 745a

HEREis what is said to be behind the price action, you know,

…WHILE YOU SLEPT Treasuries are lower and the curve little changed after hawkish comments from Chair Powell yesterday took any remaining wind out of the sails in bonds and perhaps today's slate of Fed speakers too. DXY is higher (+0.2%) while front WTI futures are little changed. Asian stocks were mostly higher, EU and UK share markets are all modestly higher while ES futures are showing +0.25% here at 7:20am. Our overnight US rates flows saw Japanese investors in the same gobsmacked boat as me: missing yesterday's heave-ho in bonds while on break. We did see some real$ selling in the long-end out of Asia with some credit-linked buying noted in their afternoon too. Overnight Treasury volume was about 110% of average overall with the highest relative average turnover seen in 2yrs (150%). Our dashboard hints that futures markets appeared to see a lion's share of last night's activity, versus cash markets.

… The Treasury 2s5s curve has been relatively stable in recent weeks- spending some time near the 20bp area as you can see in the next picture. We'd spot the potential levels of consequence in 2s5s at 30.6bp above and 7.7bp below, as illustrated.

… an updated look at the Treasury 2s5s10s 'fly in a daily chart. This 'fly has 'stabilized' in the past 5-6 sessions and just below the 4 1/2 month range lows (~24bp) taken out late February. So 24bp appears to be your local resistance with support in the low single-digit bps area- the early March and September 2021 low prints.

… Overnight Flows Treasuries were decidedly cheaper yet again during the overnight session with the curve continuing to flatten. Overnight volumes were near the norms with cash trading at 99% of the 10-day moving-average. 5s were the most active, taking a 28% marketshare while 10s were second at 24%. 2s and 3s combined to take 36% at 21% and 15%, respectively. 7s managed 9%, 20s 1%, and 30s 3%. We’ve seen two-way flows in the 2-year sector…

… and for some MORE of the news you can use » IGMs Press Picks for today (22 March) to help weed thru the noise (some of which can be found over here at Finviz).

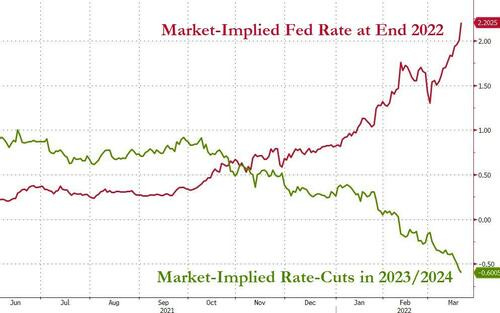

As markets (and Global Wall Street) races to repriceTO whatever the updated // new and perceived Fed reality (somewhat more below on how many 50s are on way) brought about an updated and technical FI OUTLOOK from 1stBOS

Chart of the Day: 30yr US Bond Yields are testing the 2021 high at 2.515/535%, which we view as a major support level. A closing breakout above here would reinforce the case for further weakness, with the next minor supports at 2.57%, then 2.635%, which is the 2017 low, with the “measured objective” to the large 9-month bearish “wedge” continuation pattern at 2.75/765%. Near-term resistance is seen at 2.36%.

In as far as what they are suggesting // DOING about it, well, they would be sellers turning tactically bearish AT RESISTANCE (5s and 10s) while STAYING bearish 30s:

5yy: We would turn tactically bearish at resistance at 2.30%, with next support at 2.475%, where we would turn tactically neutral. Resistance below 2.30% is seen at 2.24%.

10yy: We would turn tactically bearish again at resistance at 2.245%, with support then seen at 2.50%, where we would turn tactically neutral. Resistance below 2.245% is seen at 2.18%, below which we would also turn tactically neutral.

30yy: We stay tactically bearish from resistance at 2.40%, looking for a move to support at 2.675%, where we would turn tactically neutral. We would turn tactically neutral below 2.335%.

As always, keep your friends close and your stops closer?

With little to add TO the markets response TO JPOWs words yesterday, here are a few links / distractions / recaps of what happened yest as well as a few items from the Global Wall St inbox

Barclays: Retail Investors Pile into U.S. Equities

Surprisingly, U.S. equity markets welcomed a more hawkish Fed. In fact, retail investors piled $30bn into U.S. equity funds last week, even as internationally focused funds saw outflows. Asset managers remain cautious, and demand for protection has started to pick up with SPX skew steepening last week.

… Powell said that the Fed would “move to more restrictive levels if that is what is required to restore price stability”. That implies the possibility (not the certainty) of deliberately pushing growth below trend. This is where recession risks come in. The global economy has significant structural change, and US economic data is notably less reliable today. Delicately positioning the US economy below trend, but above recession, would be harder than in the past…

WolfStreet.com: Mayhem in the Treasury Market as Powell Adds 50-Basis-Point Rate Hikes (Plural) to Menu, QT “As Soon As” May

ZH: April 2020 But In Reverse: One Bank Warns We Are About To Witness A Historic Short Squeeze Eruption In Oil

And finally, from BBG last night (5 things HERE), there is real potential for UST Index to experience their worst quarterly return EVER,

… Federal Reserve Chairman Jerome Powell may have just set the seal on Treasuries’ worst-ever quarter. U.S. bonds were down 4.6% since Dec. 31 even before Monday’s speech when he put a half-point hike for May smack bang in the middle of the table. After the savage selloff that followed, there’s an excellent chance the first three months of 2022 will end up surpassing the 5.5% collapse at the start of 1980 that’s the current record decline for the Bloomberg U.S. Treasury Index.

Part of the reason Treasuries are so vulnerable is that the massive easing over much of the past 13 years had left bonds with historically low yields. As well as increasing the potential that prices would drop as yields recovered, it also left investors lacking much of the usual protection bonds offer because the fixed income they now provide is minimal. It may also make it harder to expect the sort of stunning rebound the assets delivered in the 1980s.

With that in mind, I cannot help but remind myself that all is NOT lost, at least not yet, when it comes to playing the odds as they relate TO ones bond portfolio.

Most of the interest rate hike expectations for the tightening cycle are priced in when the first interest rate hike materializes…if you had bought the 5-year or 10-year US Treasury the week the Fed raised rates for the first time in December 2015 (or the second time in December 2016), you would NEVER had a negative total return on your investment. Also, you would have had excess total returns for nearly the entire cycle – meaning that yields did not rise over the presumed neutral rate for multiple years…Overall, this may appear counterintuitive because of the Fed’s goal of raising interest rates, but the evidence again speaks for itself over the past 40 years.

That said, if we cannot laugh about what it is we’re living through, well, what are we doing here, then, right? Investing.com on