BULLard dissent in his own words; o/n flattening flows; (3) TLINES worth 1000 words -BAML; buy the dip -JPM; "The Yield Curve Is Inverting. Are You Scared?" and QUAD WITCHIN'...

… The combination of strong real economic performance and unexpectedly high inflation means that the Committee’s policy rate is currently far too low to prudently manage the U.S. macroeconomic situation. Moreover, U.S. monetary policy has been unwittingly easing further because inflation has risen sharply while the policy rate has remained very low, pushing short-term real interest rates lower. The Committee will have to move quickly to address this situation or risk losing credibility on its inflation target.

In my judgment, given this constellation of macroeconomic data, a 50-basis-point upward adjustment to the policy rate would have been a better decision for this meeting. In addition, in my contribution to the Summary of Economic Projections, I recommended that the Committee try to achieve a level of the policy rate above 3% this year. This would quickly adjust the policy rate to a more appropriate level for the current circumstances. The Committee has successfully moved in this manner before. In 1994 and 1995, the Committee made a similar discrete adjustment to the policy rate to better align it with the macroeconomic circumstances at that time. The results were excellent. The Committee achieved 2% inflation on average and the U.S. economy boomed during the second half of the 1990s. I think the Committee should try to achieve a similar outcome in the current environment.

Although I disagreed with the Committee’s decision to raise the federal funds rate target range by only 25 basis points at this particular meeting, I look forward to working with my colleagues to fulfill the FOMC’s mandates of maximum employment and price stability in the meetings ahead.

A rare dissent and so … Trade/invest accordingly with another red-headline day ahead, I’ll continue to favor WEEKLY closes and one I’m watching is 30yy vs 2.50%,

My basic visual of rates aside, going TO the pros for what happened,

WHILE YOU SLEPT Treasuries are bull-flattening, moderate risk aversion weighing in the overnight session, with fading hopes of a quick breakthrough in Russia-Ukraine talks weighing on confidence and German (DAX -1%) and French (-0.7%) stock markets in particular. Bonds were supported with Gilts still outperforming after the BoE's "dovish hike" yesterday. The U.K. 10-year rate has corrected a further -5.8 bp to 1.50% this morning, the German 10-year is down -1.9 bp at 0.36%, while the U.S. rate is at 2.15%, -2.1 bp lower than at yesterday's close. On ~65% volumes, our futures desk cites better flattening flows in London (TU/UXY) and Asia real$ demand sourced in 20-30y paper overnight. S&P futures -30pts here at 6:45am, Crude +1%, 2s10s curve -1bps.

… Top News : Putin Is Likely to Make Nuclear Threats If War Drags, U.S. Says (BBG) Sec Blinken “The actions that we’re seeing Russia take every single day are in total contrast to any serious diplomatic effort” (FT) Chinese foreign ministry official meets with Russia's ambassador to China (FP) US to 'impose costs' on China if it backs Russian aggression (NN) Fauci Warns of Potential Rise in U.S. Covid Cases, BA.2 subvariant (BBG) BOJ announced no change to monetary policy, as expected ‘; BOJ downgrades overall economic assessment, cites Ukraine situation as a risk factor (FX) US Says Iran Nuclear Deal Can Be Revived 'in Coming Days' Despite Setbacks (Newsweek) Panic Buying in Europe leaves Shelves Empty, Again (FT) Traders Brace for a $3.5 Trillion ‘Triple Witching’ (BBG)

… and for some MORE of the news you can use » IGMs Press Picks for today (18 March) to help weed thru the noise (some of which can be found over here at Finviz).

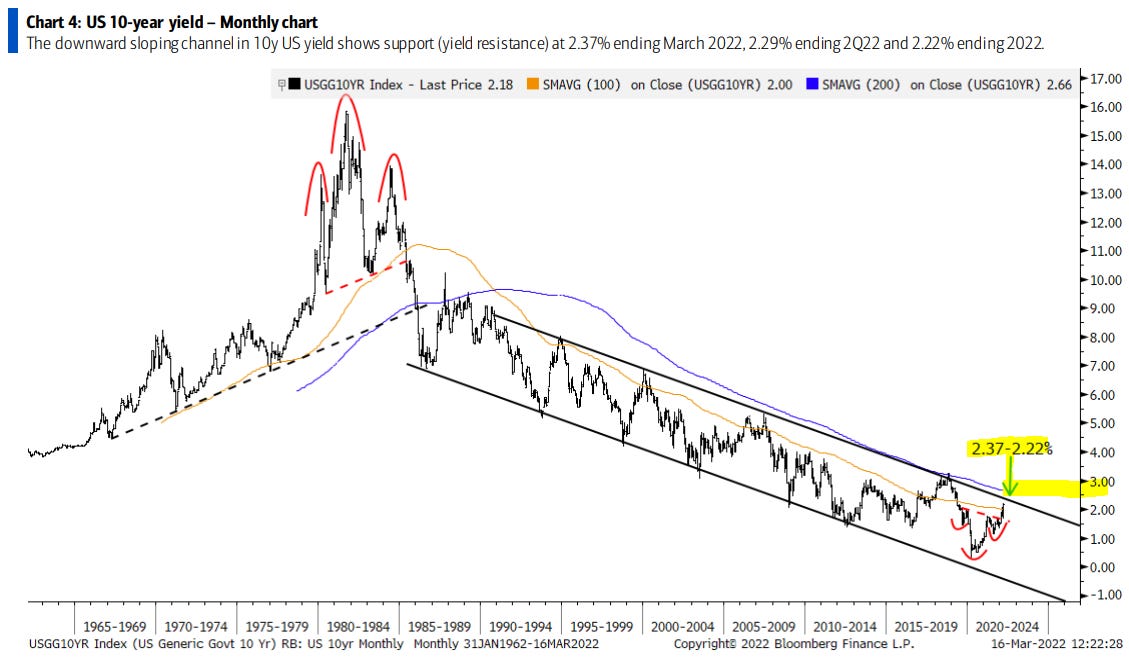

… Especially as it pertains TO rates (vigilantes) and the bond bull market being over. The short answer IS — it depends — on how it is you contextualize the longer-run. BAMLframes this all in context of the all-important (?) 100mo MA and 200mo MAs

Skipping right ahead TO the all-important MONTHLY 10yy chart,

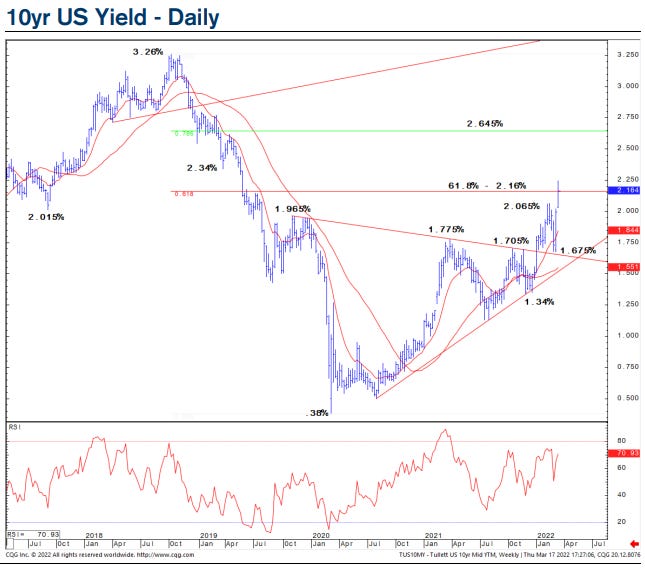

I’d ALSO note the latest levels/ideas from 1stBOS who leads off with look at 10yr swap spreads (pushing WIDER).

They suggest a tactically NEUTRAL stance 5s and, “… have turned tactically neutral at 2.16/18%. We would turn tactically neutral again at 2.075% for a move to 2.34%. We would also turn tactically neutral below 1.99%.”

… and are, “…tactically bearish at resistance at 2.40%, looking for a move to support at 2.63%, where we would turn tactically neutral. We would turn tactically neutral below 2.335%.”

Technicals and LEVELS aside, a couple other items from the inbox which may be of interest and help you pass the time from here / now until the tournament resumes around noon.

An interesting IDEA from DB …

Reducing bearish duration risk into the PMIs - Several factors, including downside risks to the eurozone's PMIs next week, lead us to reduce our bearish duration risk for now. We also enter a EUR10y - GER30Y steepener. The trade is motivated by both macro and RV considerations.

…Downside risks to the PMIs in Europe: The Eurozone economy entered the Ukraine war on a very strong footing. However, the combination of the war and further restrictions in China will likely weigh on the PMIs, at least in the short term. Leading indicators are consistent with a sub-50 composite PMI next week. Assuming some stabilisation in Ukraine in the next month, the downside shock to the PMIs should be temporary in nature, especially as it should be compensated by an aggressive fiscal response…

The novelty of this week’s FOMC message is not so much that the Fed consented to the curve shape, but their explicit endorsement of its further inversion. This is terrain that has never been accessed before in such a way. Generally, curve inversion is not deliberate. It is a part of the discovery process of neutral rates during the fight with inflation. We have seen curve inversion in the past, but not one that is premeditated. The Figure below shows the policy gap over different horizons as the distance between the terminal rate of the tightening cycle (5Y5Y) and short rate expectations 1Y – 3Y out. The gap is a cross-sectional estimate of the range the short rate is expected to traverse during the cycle. As such, it starts wide and compresses as the end of the cycle approaches (past cycles are highlighted in the chart). What makes the current configuration unique is that gap tightening is starting from unusual initial conditions which coincide with the terminal shape of the curve in previous cycles (horizontal dashed line).

Our call a year ago for a shorter cycle appears to be playing out. We're hurtling toward an environment of tighter policy, decelerating EPS growth, and more tempered risk asset returns. This argues for lighter positioning in portfolios (EW equities and credit) and a defensive bias in US Equities.

Finally, in closing, a few words from JPM via ZH because, well,

I should stay away from any / all further commentary on stonks (and should never have completed any brackets). I should ALSO stay far away from any / everything like this, from ZH on today’s QUAD WITCHIN

And while there’s ‘lotta gamma to unclench’, I will continue to watch WEEKLY yield closes and the charts noted above (as well as5s10s Fed’version noted yesterday) and leave you with one more link.

… “The market is pricing in a higher recession risk and you can see that with the inversion between five- and 10-year yields,” said Andrzej Skiba, head of U.S. fixed income at RBC Global Asset Management. “The Fed is sending a strong commitment to fighting inflation.”

The potential problem for the yield curve’s track record is that just looking at the U.S. economy, things aren’t that bad. Inflation is at a 40-year high, but the labor market is strong and policy makers were abundantly clear on Wednesday that they plan to get price pressures under control.

That will come at the expense of growth at some degree, but Fed officials still expect the economy to expand by 2.8% this year and 2% in 2023 — a historically healthy pace…

I hope you had a nice St Patty’s day and … that’s all for now. Off to the day job…