Good morning … stocks and bond yields FLAT ahead of PPI and bank earnings. TSLA’s Cybercab and BRKs selling of BAML shares garnering lots of headlines and in light of yesterday’s CPI — something for everyone — I’ll run through a few things only topically.

Before we got privilege of bidding on 30yr USTs yesterday we got a heaping dose of economic data … weather and storm impacts will continue to work through data and here’s a start …

… The consensus of economists coming into today was for a +0.10% rise in the seasonally-adjusted CPI. Now, energy this month was expected to be about a -0.17% drag on the number (it turned out to be 13bps rather than 17bps), so this low m/m print was scheduled to be mostly due to last month’s slide in energy prices. Still, decent optics especially with the last CPI we’ll see before the election. Economists saw +0.24% m/m on core. The actual figures were +0.18% m/m on headline CPI and +0.31% m/m on core CPI. This is unfortunate, because the y/y Core CPI number rose, instead of being flat, to +3.26% y/y. Moreover, the overall shape of the monthlies…well…see for yourself.

We have to be careful about the cognitive bias that makes us see stories and trends where there aren’t any, which is why it’s so very important to not focus on one month’s number. Or two. But if you look at this chart, it sure looks like the outlier might not be August and September, but May and June. Doesn’t it?

… And, as a result of wages refusing to moderate, ‘supercore’ (core services ex-shelter) also continues to refuse to slip back to the old levels.

The bottom line is that this number is not high because of any weird one-offs. In the same way that last month’s number was generally okay in a balanced way, outside of rents, this month’s number is generally less pleasant, in a balanced way. I don’t think we are at the start of another spike higher in prices. But we continue to aim for ‘high 3s, low 4s.’ …

… I’m stuck on SUPERCORE and this stuck leads well into BOSTIC commentary on possible PAUSE? … he is a voter, last I checked …

WSJ: Fed's Bostic Keeps Door Open to Skipping Rate Cut in November By Nick Timiraos

A Federal Reserve official said he was open to cutting interest rates by a quarter percentage point or standing pat at the central bank’s meeting next month depending on how the economic outlook develops.

“I am totally comfortable with skipping a meeting if the data suggests that’s appropriate,” said Atlanta Fed President Raphael Bostic in an interview Thursday…

CNBC: 10-year Treasury yield tops 4.10% as Fed’s Bostic says he’s OK with pausing rate cuts

… from that we went TO the days liquidity event …

ZH: Stunning Foreign Demand For Strongest 30 Year Auction On Record

… But the internals were where the auction truly shocked, because Indirects soared from 68.7% to a whopping 80.5%, the highest on record, as foreign central banks and various other entities just couldn't get enough paper.

And with less than 20% left for other participants, Directs took down just 7.6%, the lowest since 2018, leaving Dealers holding 12.2% of the final allocation, the lowest since July 2023…

NEWSQUAWK: US Market Open: US futures modestly lower as traders await earnings season and Chinese MOF update … USTs remain firmer following the strong US 30yr auction, Bunds dip with pressure sparked from unrevised CPI figures (but with internals holding a hawkish skew), Gilts outperform post-GDP ... USTs remain bid following on from the US 30yr auction, which was well received. Since then, they have faded slightly from best but remain within reach of today’s 112-09+ peak and therefore only a few ticks shy of Thursday’s 112-11+ best.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ … and in light of yesterday’s narrative ping pong type data, well … good luck deciphering as Global Wall tries to (not)pick a side …

BARCAP: September CPI: Limited relief even as shelter inflation retreats

Core CPI surprised to the upside, rising 0.31% m/m (3.3% y/y), led primarily by stronger-than-expected core goods prices, while core services inflation slowed modestly. The retreat in shelter inflation was offset by higher transportation and medical care services inflation. The data imply core PCE inflation of 0.23% m/m…

…We retain our call for a 25bp cut in the November FOMC meeting. Although core CPI surprised to the upside for the second month running, it appeared to be driven by some volatile components, while the sticky shelter category registered material disinflation. With September core PCE expected to round to 0.2% m/m, we think the FOMC will remain confident that the disinflation narrative is intact and that it will continue to view a gradual easing in the funds rate as warranted at the next two meetings. We view the bar for the FOMC not to cut rates at the November meeting as high, given its 50bp cut at the September meeting. Indeed, we think it would cut 25bp in November even if core PCE inflation were to show a stronger-than-expected 0.3% m/m print.

… same shop offer legit defense over CLAIMS …

BARCAP: Initial claims jump, mainly on effects of Hurricane Helene

Initial jobless claims spiked last week, driven by Hurricane Helene and Stellantis layoffs. Last week's reading of 258k was 33k above the prior week. NSA data also showed a sharp rise above historical norms, indicating limited seasonal distortion in the rise seen today.

The recent surge in geopolitical tensions poses the risk of a material binary outcome in oil markets, pushing volatility higher. Notwithstanding the ongoing geopolitical drift, a sustained 1 mb/d supply disruption could drive oil prices at least $15/b higher.

… Global Wall’s best in show was nothing if not unmoved by different set of data yesterday …

BMO: Core-CPI 0.312%; Claims +33k (12.3k from NC/FL), 25 bp Cut Still a Go

… There is a concern that the recent storms have skewed claims higher (NC added +8.5k and FL added +3.8k), although the overall magnitude of the upside surprise is difficult to ignore. On net, this morning's data reinforces our expectations for a 25 bp cut in November…

… views shaken but not stirred … continue to see 25bps CUT Nov, over in France …

BNP: US September CPI: Measured disinflation means measured Fed cuts

KEY MESSAGES

Relative strength in non-housing services and goods inflation offset a pullback in shelter to deliver a second straight 0.3% m/m core US CPI reading in September.

While the report does not set off any alarm bells, it supports the notion that the inflation dragon is not quite vanquished yet and the return to the Fed’s 2% target will take some time.

We think this keeps the Fed on track to continue to cut rates, albeit by a more measured pace than in September. We continue to see 25bp cuts at both of the year’s remaining meetings.

… from Germany, a note on CPI, Claims AND a look at how to throw darts in unprecedented times …

… Ordinarily, an inflation release like that would have led investors to dial back their expectations for rate cuts. But just as that was coming out, we simultaneously had the weekly initial jobless claims, which were noticeably worse than expected. They moved up to 258k over the week ending October 5 (vs. 230k expected), which is the highest they’ve been since August 2023. Now to be fair, there are some weather-related factors that can help explain that, and the numbers are likely to remain volatile for several weeks as a result. But even so, the number was higher than expected, and given it’s quite a timely release, it pushed back against the more positive labour market narrative from last week’s jobs report. The chances are still high that it was heavily distorted though and with the current storms in Florida, getting a clean reading soon will be tough.

Nevertheless, with all that in hand, investors moved to increase the pricing of Fed rate cuts in the coming months, even as they priced in more inflation for the years ahead. The likelihood of a 25bp cut next month rose marginally from 83% the previous day to 85%, but having peaked at 95% intra-day after the data. The move was more sustained further out the curve, with the rate priced in for the December 2025 meeting falling by -8.2bps to 3.34%. The reversal in November pricing from the day's peaks came following a WSJ interview with the Fed’s Bostic, who left open the possibility of a pause in November, saying that “I am totally comfortable with skipping a meeting if the data suggests that’s appropriate”. On the other hand, comments from Williams, Goolsbee, and Barkin suggested they were largely unphased by the stronger CPI print.

The more dovish Fed pricing contributed to a rally in front-end yields that pushed the 2yr Treasury yield down -6.5bps to 3.96%, while the 10yr yield was down a more marginal -1.1bps to 4.06%. This comprised of sharply diverging moves in real yields and breakevens, especially at the front end. While 2yr breakevens (+9.8bps) rose to their highest since early July, 2yr real yields (-16.3bps) posted their sharpest daily fall since the December 2023 FOMC. So signs of market pricing turning in a slightly more stagflationary direction…

DB: US Economic Perspectives - A practitioner's guide to forecasting in unprecedented times

This report presents an analytical review of one of the most challenging and intense – indeed frightening – five-year episodes in US economic history: the Covid 19 pandemic and its aftermath. Our review is written through the lens of practitioners who served on the front lines of macroeconomic forecasting, striving daily to make sense of what was happening in order to form a view for our clients of what would come next over the months and even years ahead. The challenges were great because the initial shock and subsequent responses of policy makers, households, workers, firms, and markets were all largely unprecedented.

… ‘bout that ‘supercore’ …

FirstTrust: The Consumer Price Index (CPI) Rose 0.2% in September

The Consumer Price Index (CPI) rose 0.2% in September, above the consensus expected +0.1%. The CPI is up 2.4% from a year ago.

Food prices rose 0.4% in September, while energy prices declined 1.9%. The “core” CPI, which excludes food and energy, rose 0.3% in September, above the consensus expected +0.2%. Core prices are up 3.3% versus a year ago.

Real average hourly earnings – the cash earnings of all workers, adjusted for inflation – rose 0.2% in September and are up 1.5% in the past year. Real average weekly earnings are up 0.9% in the past year.

… But a subset category of prices the Fed used to tell investors to watch closely but no longer seems to mention – known as the “Supercore” – which excludes food, energy, other goods, and housing rents, rose 0.4% in September and are up 4.3% in the last year, worse than the 3.8% reading in the year ending in September 2023. No matter which way you cut it, inflation is still running above the Fed’s 2.0% target, now for the 43rd consecutive month. We have said for some time that easing in inflation will come should the Fed have the resolve to let the lagged effects of tighter monetary policy do its work. Recent economic data suggest the Fed is much more likely to cut rates by a quarter point the day after the election, not a half …

… attention all Goldilocks MUPPETS …

Goldman Sachs: The probability of a US recession in the next year has fallen to 15%

The likelihood of a US recession in the coming year has declined amid signs of a still-solid job market, according to Goldman Sachs Research.

Our economists say there’s a 15% chance of recession in the next 12 months, down from their earlier projection of 20%. That’s in line with the unconditional long-term average probability of 15%, writes Jan Hatzius, head of Goldman Sachs Research and the firm’s chief economist, in the team’s report.

The battle between the US jobs numbers and the inflation data with regards to the outlook for Fed policy remains unresolved. As such policymakers will need to tread carefully, but our base case remains 25bp rate cuts in November and December

… Canadians have opinions on our Fed, too, you know …

RBC: Firmer U.S. September price growth lowering the odds of aggressive Fed cuts

…Bottom line: The (small) upward surprise in September price growth isn't likely enough to prevent the Fed from following through with additional interest rate cuts, but further lowers odds of a repeat September's 50 bp reduction that already fell dramatically after September's strong payroll report last week. We continue to expect, as a base-case, that broader inflation pressures will continue to ease as a gradual softening in labour markets continues (the spike higher in initial jobless claims separately reported this morning was likely distorted by the impact of hurricanes and strikes). But stickier inflation readings over the last two months and resilient labour markets to-date are consistent with our expectation for a gradual and limited additional fed rate cutting cycle into next year (just three additional 25 basis point cuts assumed per Fed meeting into January of 2025)

US September consumer price data signaled disinflationary trends. Food prices have disproportionate political importance, but around 40% of the monthly increase in food prices was due to eggs. Can an election be swayed by an egg? Some key states saw food prices fall compared to August. Voters remember price levels, and tend to have an idea of a “fair” price for food items that would have been fixed in their minds many months ago. The political impact of this price report is probably marginal.

The Federal Reserve is very unlikely to change its policy path after this data—and several Fed officials said as much overnight. There is producer price information due out today which should also show disinflationary tendencies…

Summary The September CPI report came in slightly hotter than expected, but not enough to meaningfully change the outlook for U.S. inflation. Headline CPI rose 0.2% in the month, while excluding food and energy prices consumer price inflation was a tenth stronger at 0.3%. A 4.1% drop in gasoline prices helped restrain overall inflation, although a 0.4% rise in grocery store prices served as a partial offset to the respite at the pump. Core goods prices rose 0.2%, ending a six-month streak of goods deflation. Higher prices for new and used vehicles as well as apparel were the culprits for the increase in core goods prices. On the services side, slower inflation for shelter costs in September was offset by a jump in prices for airfares, motor vehicle insurance and medical care.

Today's data bring the year-ago change in the core CPI to 3.3%, with prices over the past three months increasing at a 3.1% annualized rate. For context, core CPI inflation averaged 2.2% in 2019, suggesting that the underlying pace of inflation at present is about one percentage point above what prevailed before the pandemic. Looking ahead, we expect the disinflation trend to continue, albeit gradually rather than sharply. The ongoing cooling in the labor market and lagging service sector components should help reduce core inflation a bit further in the months ahead. As a result, we expect the FOMC to continue normalizing monetary policy. We still anticipate two 25 bps rate cuts from the Federal Reserve at the two remaining FOMC meetings of the year.

… and finally, is there a doctor in the house … why, yes … yes there is …

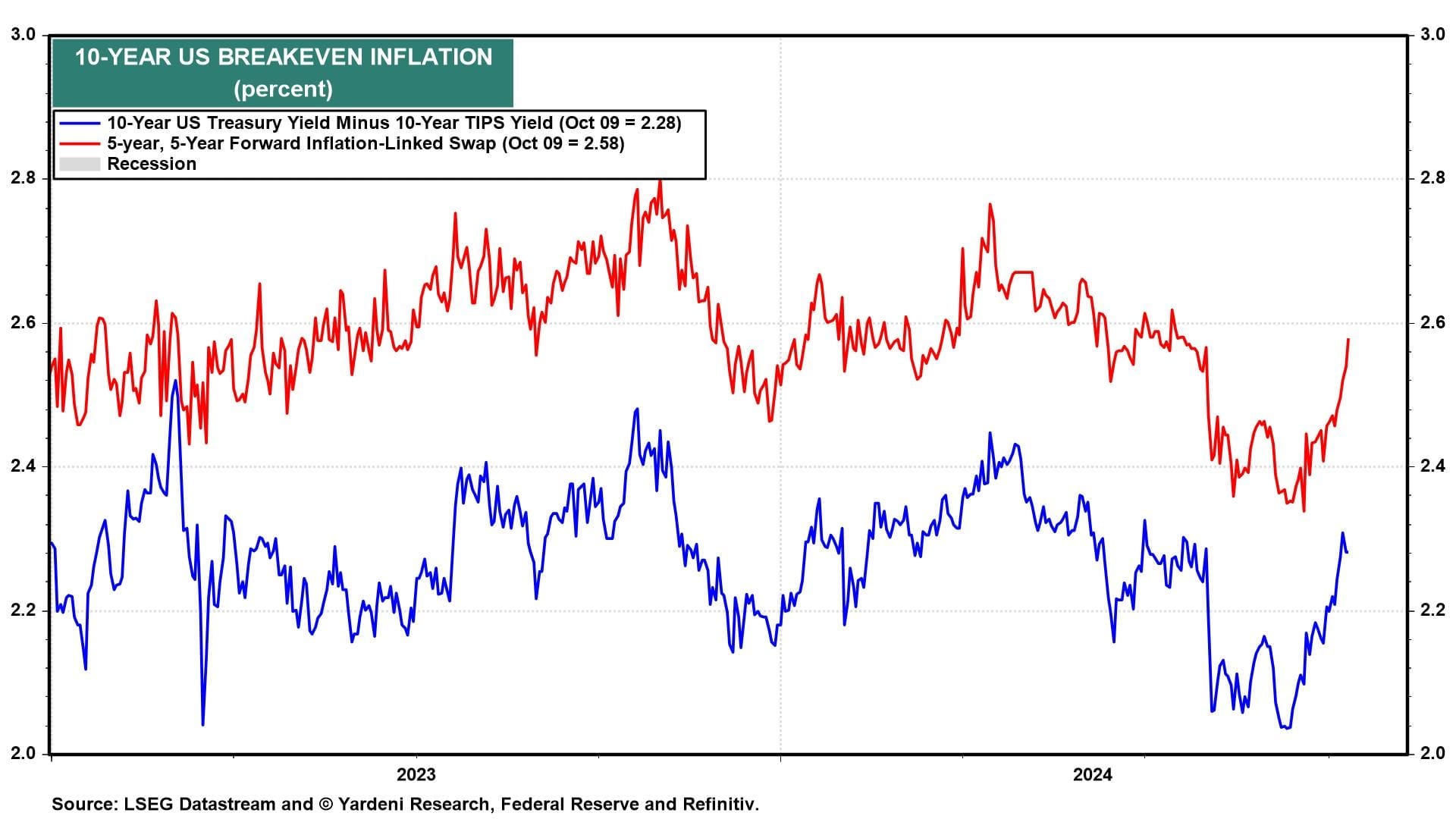

… Today's CPI data support our story that the Fed shouldn't cut the federal funds rate (FFR) at its two remaining meetings this year. The bond market has been signaling the same since the Fed's 50-bps rate cut on September 18. The 10-year yield has risen from 3.63% to 4.11% today thanks to increasing inflation expectations (chart). Meanwhile, stocks edged only slightly lower off their new record highs set yesterday. Any additional rate cuts would increase the odds of a stock-market meltup. Here's more on today's data:

(1) Supercore inflation. In late 2022, Fed Chair Jerome Powell pointed to so-called supercore inflation (core services inflation, excluding housing) as possibly “the most important category for understanding the future evolution of core inflation.” Today, supercore CPI inflation ticked up from 4.3% to 4.4% y/y. That's a far cry from "mission accomplished."

… And from Global Wall Street inbox TO the WWW …

… they say all opinions are created equally and that is in theory. in practice we KNOW how some are MORE equal than others …

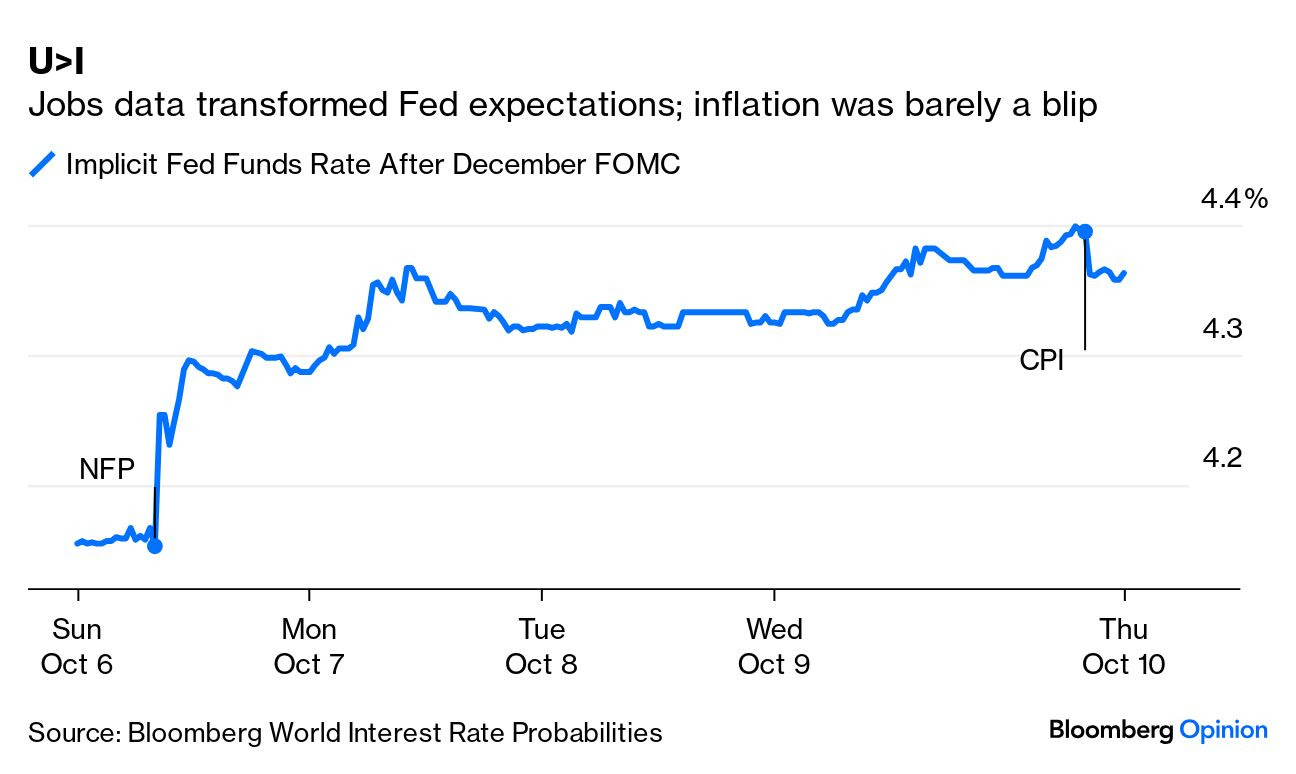

Bloomberg OpED: Inflation is finally losing its power over markets The stubbornness of services still needs grinding down, but the Fed has won this war of attrition.

… For the first time in a few years, Thursday’s announcement of September inflation made no discernible impact on markets. The S&P 500 dropped 0.2% for the day, while the 10-year Treasury yield shed one basis point. These are piffling examplescompared to the convulsions that inflation reports have often caused over the last three years. That’s in large part because it had minimal impact on expectations for the Fed. This is the implicit rate predicted by the fed funds futures market since last Friday, when unemployment figures were announced (my apologies that it appears incorrectly marked on the chart as Sunday):

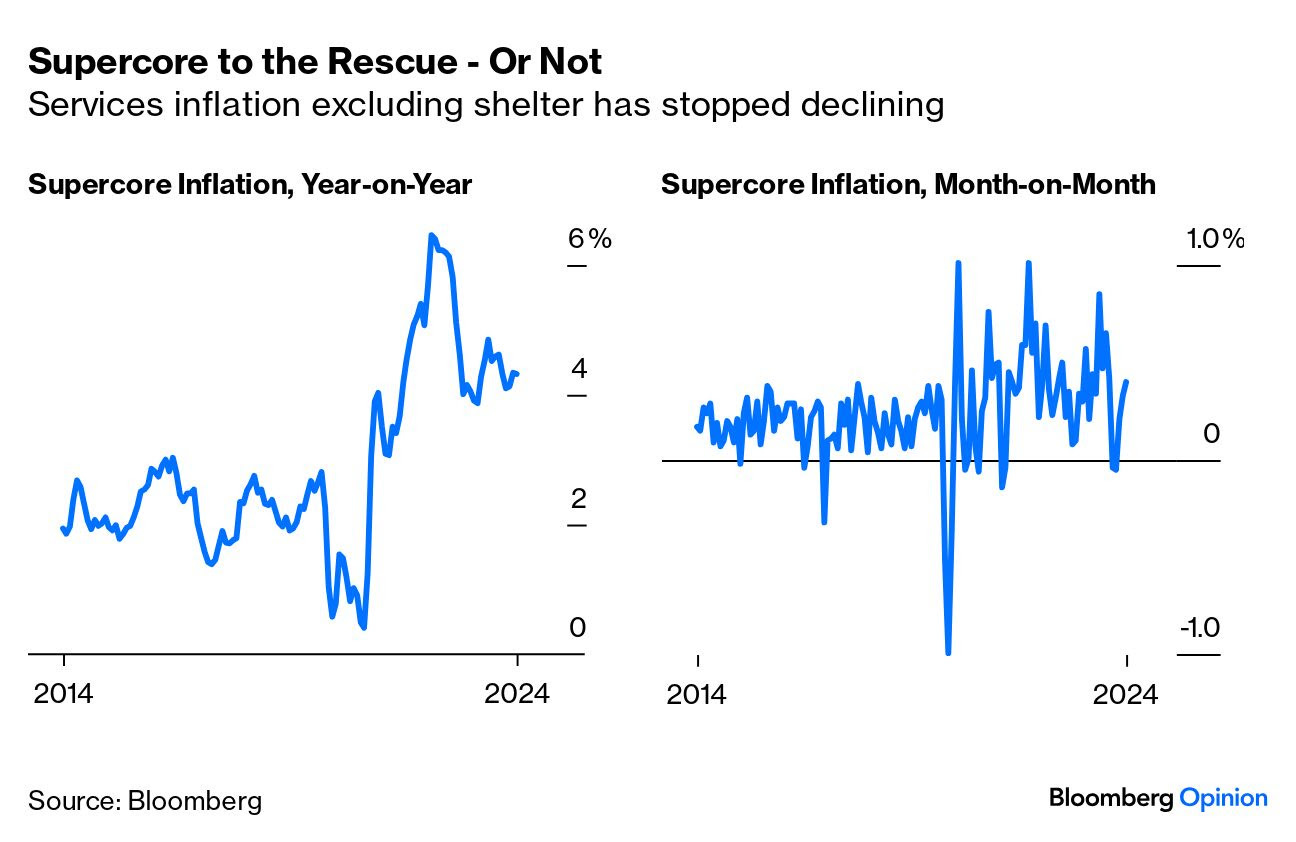

… the Fed’s favored “supercore” measure of inflation, of services excluding shelter prices, has some bad news. It’s ticking up again, and the annual rate remains above 4%. That would make continued jumbo interest rate cuts difficult:

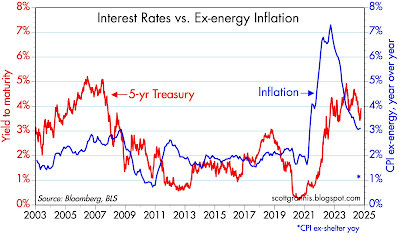

… Chart #4 compares the 5-yr Treasury yield to the year over year change in ex-energy inflation. I like to use this version of inflation, because as noted in #1 above, energy is far more volatile than any other component of the CPI. Here we see that interest rates tend to move with inflation, but with a noticeable lag. And with ex-shelter inflation now at 1.1% (note the blue asterisk at the bottom right-hand corner of the chart), there is plenty of room for Treasury yields to decline.

Short-term yields are falling while long-term interest rates and inflation expectations are on the rise once again.

This reflects a Federal Reserve that is cornered, needing to suppress short-term rates to alleviate the government's debt servicing costs, while potentially allowing inflation to run higher and pushing up long-term rates, in our view.

We believe this combination is likely to create the ideal conditions for a much further steepening of the yield curve.

… somewhat MORE on CPI from the Wolf …

WolfST: Beneath the Skin of CPI Inflation: “Core CPI” Accelerates for 3rd Month on Sharp Flip of Used Vehicle Prices, Sticky Services Inflation. Gasoline...

Surging homeowner insurance and other homeowner costs fuel OER CPI, which is now hotter than rent CPI.

… meanwhile, how I view inflation guy offering to talk / lecture anyone who wants to listen on … inflation

AND … THAT is all for now — HOPE to have more over weekend. Off to the day job…