Good morning … little in the way of news overnight and Global Wall is aggressively UNCH ahead of this mornings inflation report. Likely much more to say / think this time tomorrow and so …

Let’s review. 10s came and went …

ZH: Near Record Foreign Demand For Tailing 10Y Auction

… Curiously, the internals were not bad at all, perhaps as foreign central banks sought to load up on US paper now that yields are back over 4%, and the Indirect takedown rose to 77.6%from 761%, and just shy of the all time high hit in Feb 2023 when indirects took down just under 80%…

… and this was then followed up by FOMC minutes …

ZH: FOMC Minutes Show Fed Considerably More Divided Over Size Of Rate Cut

Since the last FOMC meeting on September 18th, bonds have suffered a bloodbath while gold, stocks, and the dollar are all up modestly...

… and by days end …

ZH: Stocks Up, Yields Up, Dollar Up, China Down As Hawkish Minutes Hit Ahead Of CPI

… and with the benefit of knowing the data and inflation trajectory / narrative, thisweeks supply of durationcomes to a conclusion a little bit later on today, with $22bb reopened 30s …

30yy DAILY: at / near ‘top of the range’ (?) and watching 4.40% …

… momentum has shifted from overBOUGHT to oversold and with a couple TLINES / levels of support, i’m wondering if one should / might / WILL buy further concession or tail after the auction …

… and for somewhat more from someone with a Terminal …

NEWSQUAWK: US futures trade tentatively ahead of US CPI … USTs are modestly lower potentially pressured by FOMC Minutes/30yr concession; Gilts lag after IFS analysis … USTs are pressured with the FOMC minutes potentially weighing alongside a mixed 10yr auction and concession into the 30yr. Thus far, USTs at a 112-01+ trough, a couple of ticks below Wednesday’s base to a fresh WTD low. US CPI is also on the docket, which is expected to cool slightly from the prior pace.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

…. ‘bout those FOMC minutes …

BARCAP: September FOMC minutes: A lukewarm 'substantial majority'

The minutes indicate that all FOMC participants agreed to cut rates at the September meeting, and that a substantial majority supported the 50bp cut, even though this appears at odds with the latest dot plot. We retain our call for two more 25bp cuts in 2024 and three in 2025.

…USD rates: Yields to fall gradually with Fed rate cuts Data points to a gradual easing cycle and modest fall in front-end yields: Data over the past month has pointed to a resilient US economy accompanied by a gradual easing cycle. Core PCE inflation is basically at the Fed's target with the 3mma running at 2.1% y/y. The labor market continues to indicate strength with 254k in added jobs in September, 72k in upward revisions for the prior two months, the unemployment rate falling to 4.05% and job openings rising. Finally, GDP and personal savings have been revised higher, showing strong household and corporate balance sheets.

That is why we have seen a shift in rhetoric from the Fed, where Chair Powell has put much emphasis on supporting an already-strong economy by lowering rates gradually. Although the Fed did cut by 50bp in September, this reflected not the weak July NFP but rather inflation running at target when Fed policy was already restrictive.

Therefore, we still expect a 25bp cut at the November and December meetings to reach 4.50% fed funds by year-end, and a further 125bp of easing in 2025 to settle at a terminal rate around 3-3.25%.

In response, front-end yields should continue to come down, but less than the market now anticipates. The bar for another 50bp cut is quite high and likely makes it difficult for spot yields to outperform forwards.

Long-end of the curve is prone to stickiness: The long-end of the curve faces similar hurdles, but also term premium drivers such as economic strength/neutral rate expectations, elevated UST supply and funding constraints

Our base case is for annual deficits to run at 6-7% of GDP in the long-term with interest expense making up roughly half. Additionally, the potential for a presidential election sweep could see bigger upside risks to the deficit in a Treasury market that is already absorbing record duration supply.

Moreover, dealer balance sheets are their most constrained since 2020 while QT is still ongoing, which is putting upward pressure on repo/funding markets. This makes funding Treasuries more expensive, which is why swap spreads have cheapened so much across the curve.

The above confluence of factors should make 10y yields stickier, hovering at our 4% fair value in the near-term.

… how’s about them ‘24 DOTS especially in wake of minutes …

In the September SEP, the median fed funds rate projection for this year-end was 4.38%, pointing to a baseline of two more 25bp cuts this year, as Chair Powell has highlighted in recent remarks. But there were nine (of 19) dots at 4.63% or above …

… We’ll be looking to the minutes this afternoon for perspective on how to read those dots and the implications for Fed policy over coming months. To the extent the close nature of the decision and dispersion in the near-term policy outlook is emphasized, cut pricing through December may moderate further.

… nothing like setting the bar for data too high …

US September consumer price inflation should show a slower rate of growth in the headline measure. Now that the Federal Reserve has finally started its easing cycle, this matters a little less to markets, but it is still important. Critically, middle-income inflation is running at about half the headline rate, and that gives the group an important degree of spending power.

The minutes of the last Federal Reserve meeting signaled that there was quite a lot of disagreement over the size of the last rate cut. Markets are likely to conclude that sizable rate cuts are unlikely to be repeated, and that the Fed will cut twice this year to try and make up for lost time—but that it will cut by 25bps each time. The “account” of the last ECB meeting is due, but is less likely to attract drama…

… And from Global Wall Street inbox TO the WWW,

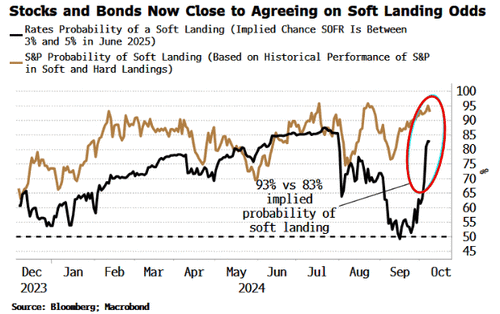

… and that time stocks AND bonds agreed …

Bloomberg (via ZH): Stocks & Bonds Back In Agreement On (Low) Recession Risks

… Ideally though, both assets should agree on the outlook, and either be wrong or right together. Lately that’s not been the case, with rates markets making a recession virtually their base case, while stocks were pricing in a negligible chance of that outcome.

With Treasury yields back at 4% and rates markets selling off - while stocks have been fairly steady - both markets now largely agree on the economic outlook for the first time since early summer.

The chart above shows the implied odds SOFR is between 3% and 5% in June next year -- a rates market proxy for the Federal Reserve achieving a soft landing. To infer stocks’ imputed chance of a soft landing, I look at the S&P’s best and worst performances through historical hard and soft landings and compare to its recent performance to imply a probability.

Are stocks and bonds correct to assume a soft landing is a base case?

Yes, but with two very important caveats….

… once again I ask … did someone say, ‘BOND TRADERS’ …

Bloomberg: For Bond Traders, It’s Wait Till Next Year (Again) This was supposed to be the year of the bond. It wasn’t.

A return to lower yields has been every bond fund manager's dream since the nightmare of 2022. But now, with expectations dashed that they’d get their wish this year, it appears they’ll have to hang their hopes on 2025.

Last Friday's bumper US non-farm payroll report is just the latest in a succession of head fakes over where we might be in the US economic cycle. The biggest fallout since has been in the shortest maturities, wiping as much as 50 basis points off Federal Reserve rate-cut expectations. Only a 25 basis point move is now priced in for the next Fed meeting Nov. 7 and one lessrate cut in 2025. It's been a proper repricing, not aided by the impending presidential election and rising geopolitical uncertainty. So risk reduction is uppermost until clarity emerges. Certainly there is little stimulus coming from the rest of the world…

… when ‘official’ accounts produce / send stuff, we’re almost obligated to slow down and read …

Liberty Street Economics: A New Indicator of Labor Market Tightness for Predicting Wage Inflation

… The chart below demonstrates the fit of the HPW Index visually by plotting it against wage growth, measured using a three-period moving average of the three-month growth in the ECI (both series are normalized to have a mean of zero and variance of one for ease of comparison). We compare our measure against a common measure of labor market tightness: the Conference Board’s survey measure of consumers’ perception of job availability. Both the Conference Board measure and the HPW Index track wage growth well in the pre-pandemic period. However, in the pandemic period, our measure performs significantly better.

…Concluding Remarks In summary, the HPW Tightness Index of quits and vacancies per searcher performs well in summarizing labor market tightness for the purposes of determining wage inflation, consistent with theoretical results in Bloesch, Lee and Weber (2024). The relationship remained strong during the COVID period and recovery, suggesting that the empirical relationship documented is robust to even large, unusual economic shocks.

… what up with FI? lets see …

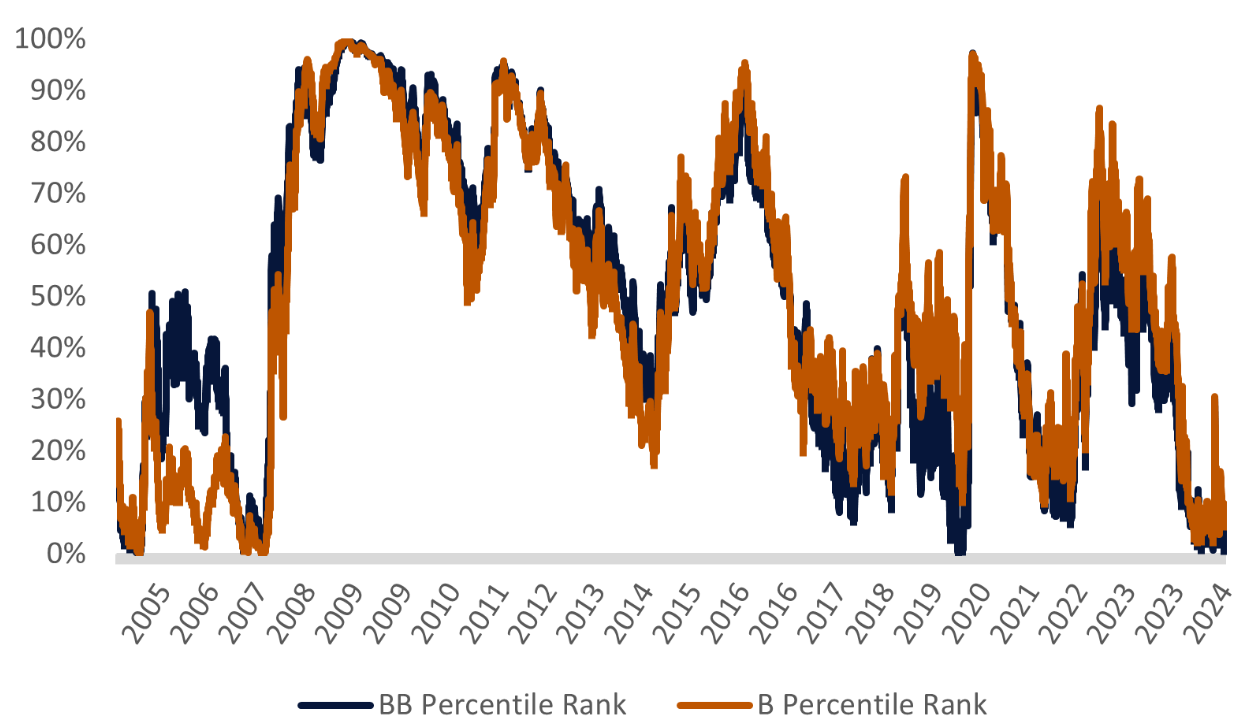

LPL: What’s New With Fixed Income? LPL Research discusses how the fixed income landscape has evolved and where certain positioning makes the most sense.

… The chart below highlights the historical percentile rank of the option adjusted spreads on BB and B rated corporate bonds during the last 20 years. Spreads are near two-decade lows, trading at the 2nd and 7th percentiles, respectively, meaning spreads have been higher 98% and 93% of the time, respectively.

Historically Tight Credit Spreads

…Conclusion While some things like projected future interest rates have changed, other areas of the bond market such as credit spreads have remained entrenched. LPL Research believes a step back into a neutral tactical asset allocation bond positioning can help lock in gains on strong performing sectors, wait out a rangebound rate environment and weather potential economic and geopolitical headwinds. For those looking to tactically deploy proceeds from such a move we view alternative investments as an attractive choice. In particular, Global Macro alternatives can provide robust diversifying effects and Multi-Strategy alternatives can offer advantageous, dynamic, uncorrelated investing. The Fed has enacted the catalyst for change in the fixed income landscape, and the market has begun to sketch its roadmap.

… post NFP some are sayin / thinking one and done …

Topdown Charts Chart of the Week - One and Done How markets react to short Fed rate cutting cycle

… I identified situations where the Fed either brought interest rates down by a small amount or over a short cycle. Every instance followed at least one and often many rate hikes, and every instance concluded in a return to rate hikes. I identified 9 such instances over the 1955-2024 period.

Firstly, that tells us that it’s not entirely uncommon, and actually about half of all rate cutting cycles fall into this category. It’s partly a combination of the Fed getting it wrong and wrongly cutting rates, partly due to external developments and other things derailing the rate cutting cycle, and of course partly due to the Fed just doing its job well and rate cuts actually helping and reviving growth/inflation.

But as to how the stockmarket tends to trade — it typically rallied over the 18-months prior, wobbled into the rate cut (often these cutting cycles were triggered by some event or scare), and then generally trended higher thereafter.

So a return to rate hikes or a situation of one-and-done might be a good thing.

Key point: Stocks tend to do well during small/short rate cutting cycles.

Bonus Chart: What about Bond Yields?

As you might guess, 10-year treasury yields tended to drift lower into the first rate cut, but in basically every instance bond yields pushed higher in the subsequent 18-months. This would have reflected the fact that short/sharp/small rate cutting cycles would most likely have been cut short by a resurgence in inflation or just generally better growth and market conditions.

… did you smell that? …

WolfST: Bond Market Smells a Rat: On Eve of CPI Inflation Data, 10-Year Treasury Yield Jumps to 4.08%, +43 bps since Monster Rate Cut

Fed is seen as deprioritizing inflation fight, while a tsunami of supply heads for markets.

These articles are fantastic!!!

I always learn so much reading them.

It's amazing to read what the big brokerage houses are saying.

Thank you..

For those who want news on Israel and their war, watch Stakelbeck Tonight and Joel Rosenberg on TBN(Trinity Broadcast

Network) and on YouTube