while WE slept: little changed on solid volumes; NO March <cut> for you; #Got20s

Feb 01, 2024

Good morning.

Fed’s NOT gonna cut in March — not news for those playing along at home with me here (perhaps shocking to those thinking / BETTING on 6 cuts in 2024) and frankly, you can skip the rest of the note.

I’ve nothing much further to add.

What follows will be a visual of 20s, a few random thoughts, some ZH links followed by somewhat more from Global Wall as the Fed has (once again) shaken up the narrative creation machine — turning it on its head — and everyone’s got to attempt to right the ship and win the buy side flow biz.

Recaps, victory laps and I told ya so. Maybe I said March but now I mean MAY.

Great. Thanks. Thanks for that.

SO, for here and now … some (perceived lack of supply) inspired MONSTER moves in bonds (supporting HIGHER stocks?) which THEN combined with slowing jobs market (ADP) again supporting lower rates (and so, even higher stocks) THEN chased down by NO MARCH CUT (bad for stonks which was ALSO good for bonds ?? heads I win, tails you lose) and it all leaves me thinking …

#Got20s?

… and yes, here TOO I spy with my little eyes … nevermind and TO the point WHY I am leading with a look at 20s …

AND along with NO MARCH CUTS 4 U … well, summarized another way

… Yesterday as defined by a couple / few turns of events and links

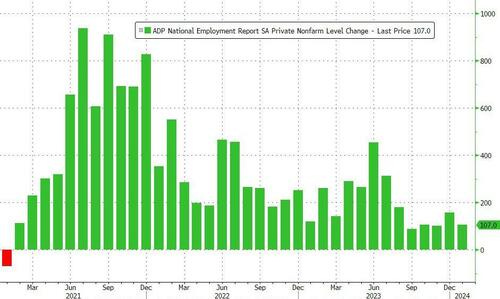

ZH: ADP Employment Report Job Gains Slowing (107k vs 150k e and 164k last)

… This is the second lowest monthly increase in jobs since Jan 2021's drop in jobs...

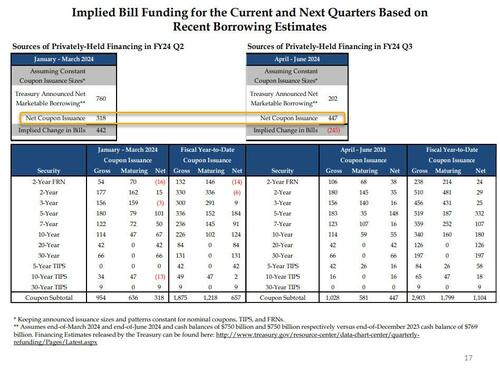

ZH: Treasury Increases Coupon Auction Sizes Again, Does Not Expect More Boosts For "Several Quarters"

ZH: Here Is The Scariest Chart In Today's Treasury Refunding Announcement

… In fact, as the chart below - which we have dubbed the scariest chart in the Treasury's presentation to TBAC today (link here) - shows, with Bills expected to fund some $442 Billion of the $760BN funding deficit in the Jan-March quarter (the balance of $318BN funded by coupons), in Q2 the Treasury now anticipates a $245BN DECLINE in net Bills outstanding (i.e., not only no incremental Bill funding but a quarter trillion maturity in Bills outstanding). In other words, while we expected a "sharply lower" Bill issuance in Q2, the Treasury is actually expecting a $245BN drawdown in Bills.

But wait, there's more: because while the market was expecting some pro rata decline in coupon issuance to go with the slide in net Bills (we were not) in Q2 to justify the sharp drop in long-end yields, it was not meant to be. In fact, just the opposite, because as highlighted in the chart above, net Coupon issuance in Q2 is actually expected to increase by $130BN to $447BN from $318BN in Q1. This is a huge shift in higher duration supply, and is hardly what all those who were buying 10Y bonds on Monday were expecting, and yes, that too was to be expected: with Bills now well above the "comfortable" ceiling of 20% as a percentage of total debt outstanding, the Treasury had no choice but to roll it back, especially since the Reverse Repo is already mostly drained. And sure enough, in its presentation, the Treasury no longer anticipates a flood of Bill issuance in the future…

ZH: Hawkish Fed Hammers Dovish Market: No Cuts Imminent, Removes 'Banking System Soundness' Comment

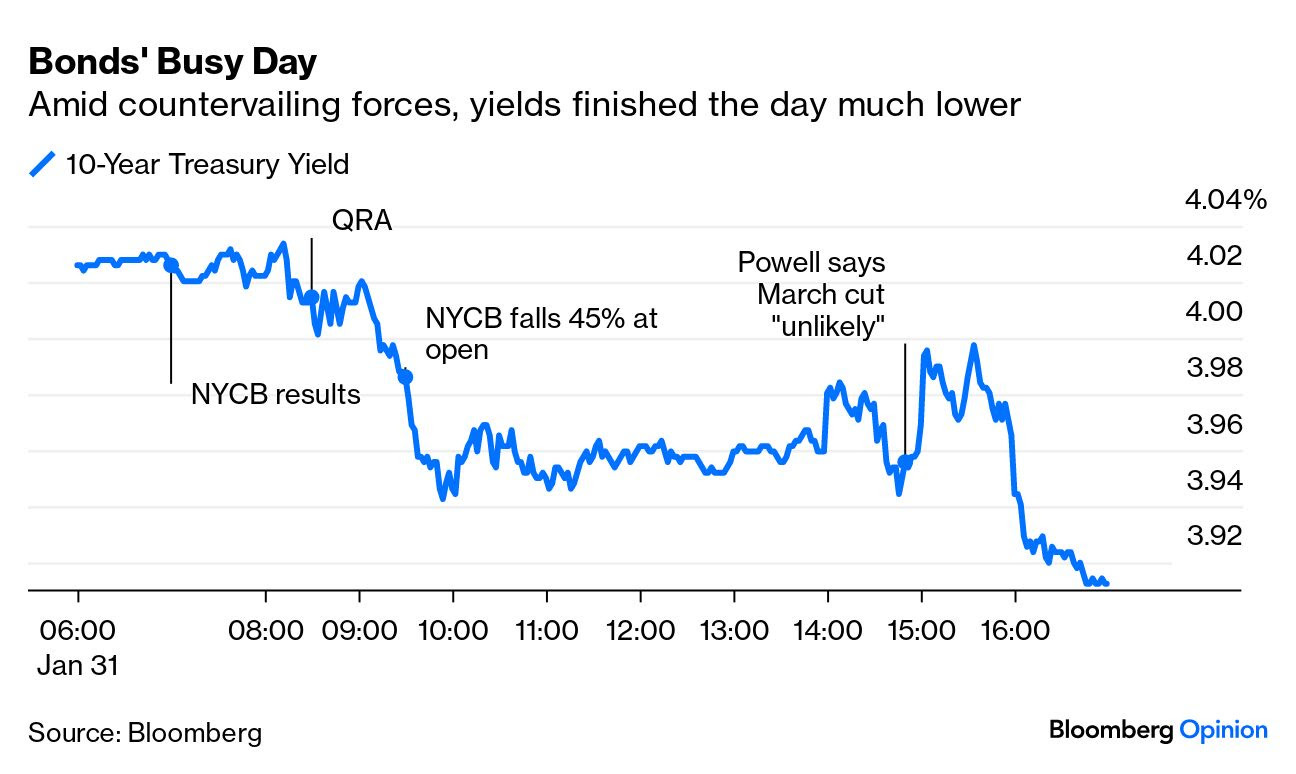

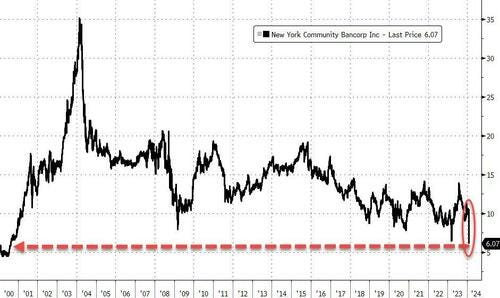

… And finally, right in the middle of The Fed's meeting NYBC blows up, sending rate-cut expectations soaring (as traders reached for safe-havens like gold and bonds), putting The Fed in the awkward position of likely having to push back against the bullying market (after all the jawboning of the last month was wasted)...

… AND here is a snapshot OF USTs as of 705a:

… HERE is what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly lower with the curve little changed after mixed BOE verdict and ahead of another brace of upper-tier US data. Asian stocks were mixed, EU and Uk share markets are little changed on balance (SX5E FLAT) while ES futures are showing +0.4% here at 7:10am. Our overnight US rates flows saw a bear flattening into Tokyo's open despite block buys going through in intermediates. Our Tokyo desk also saw better real$ buying in intermediates into the downtick. During London's AM hours, better buying in the belly was noted alongside fast$ interest to steepen 5s30s. Overnight Treasury volume was solid in our sheets (~160% of ave), at odds with desk anecdotes again. (will sort this schism out) …

… The good news is that despite Powell's brushback pitch under the noses of those banking on a March rate cut, 10 year Treasury yields have pulled away from their recent, 4.10% to 4.12% magnet. We show in our first attachment this morning that the tactical set-up (next week, say) still appears on-balance bullish to our eyes. Our earlier thoughts that the price pattern since October may a big Bull Flag remains valid and, if true, then a return to the rate move lows near 3.80% seems a conservative target. Moreover, daily momentum aims lower still and is far from being 'overbought' yet- a sign that the balance of flows still favors lower rates (more on this at the end).

… and for some MORE of the news you can use » The Morning Hark - 1 Feb 2024 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ … mostly about QRA and FOMC

BARCAP Federal Reserve Commentary: January FOMC: Raising the bar for a March rate cut (facts change, I change, what do you do, sir…?)

The tightening bias was removed from the statement, as expected, but the bar was raised for a March rate cut. We change our rate call, with a first cut in May after Powell said the FOMC needs to see "more good data" to gain "more confidence," and suggested that a cut was not likely in March.

… In terms of wages, Job Stayers saw an increase of +5.2% YoY while Job Changers improved +7.2% YoY (lowest since May 2021). Overall, it was a marginally disappointing ADP print, but nothing that will meaningfully change the perception that the labor market remains resilient all things considered. Treasuries improved marginally on the data with the front end of the curve benefiting as a March cut remains the primary debate…

BMO: Feb Refunding: Auction Sizes as Expected, No further Boosts Anticipated

… Most importantly looking forward, "Treasury intends to continue gradually increasing coupon auction sizes in the February to April 2024 quarter and believes that these cumulative changes will leave Treasury well positioned to address potential changes to the fiscal outlook and to the pace and duration of future SOMA redemptions."

BMO: FOMC: Seeking Greater Confidence on Inflation Trend

The FOMC statement saw a lot of changes that, in the context of what 'could' have been said is being interpreted as a hawkish hold…Ahead of the statement, the Treasury market had already rallied with 10-year yields at 3.96% immediately before 2pm. Since the headlines hit, the front-end sold off as the market's read was that it wasn't as dovish as it could have been…

Treasury announced its third and final round of coupon auction size increases at the February refunding. This will take duration supply to the market to an all-time high.

The May start date for the buyback program means that it won’t be in place to dampen TGA swings around the April tax date. We see this as a factor supporting the case for an April start to QT taper.

The supply and liquidity outlook continue to tilt risks towards upward pressure on secured funding costs and headwinds to spreads.

Bloomberg BNP US January FOMC: Powell fades March cut, subtly opines on pace

KEY MESSAGES

Chair Powell leaned firmly against the prospect of a March rate cut in his January post-FOMC press conference, but signaled that the committee was nearing the confidence level necessary to justify the start of the cutting cycle.

Powell repeatedly cited the need for more resolute confidence in the inflation trajectory as a critical precondition for cuts.

The committee appears poised to respond asymmetrically to activity data. A stall could pull cuts forward, but stronger activity is not necessarily viewed as jeopardizing the inflation trajectory (likely based on the experience of recent quarters).

We view the January FOMC communications as reinforcing our expectation of the first rate cut coming in May, followed by a steady cadence of cuts (25bp per meeting) through year-end.

Powell also suggested the committee was prepared to engage in a robust, detailed discussion of balance sheet policy at the March meeting—which we view as being consistent with our expectation of a QT taper starting in April.

US 10y yields: Yields broke decisively back below the 55w MA and the psychological 4% support level. We are now on track to post a weekly evening star formation (signifying a potential reversal).

Why it matters: IF we can sustain this on a weekly basis, we think the move lower we had called for earlier in yields will be back on track. We expect short term support at 3.78% (December lows).

In the medium term, we continue to see a 55-200w MA setup signaling a potentially larger move lower.

Technical indicators:

Close below 55w MA as well as the psychological 4% support level

Potential weekly evening star formation

Resumption of 55-200w MA setup that we had flagged.

OTHER TECHNICAL DEVELOPMENTS WORTH NOTING

US 2y yields: We could see a potential weekly evening star formation for US 2y yields. The key support level to watch is 4.12% (Jan lows). IF we close weekly below that, the next major support level will be at 3.95%-4% (76.4% Fibo retracement, psychological level)…

The January FOMC meeting solidified the Fed's dovish pivot. Revisions to the meeting statement were as expected, with the Committee dropping its explicit tightening bias. This change opens up the potential for rate cuts at coming meetings. However, the statement indicated that further confidence is needed that inflation is moving sustainably to 2%. Moreover, Chair Powell made clear that, at this point, the Committee does not think this will be achieved by the March meeting.

On QT, Powell indicated that the Committee planned to have a more "in-depth discussion on balance sheet issues at our next meeting in March." There was little new information about the balance sheet beyond this timeline.

With two more CPI reports, along with the release of updated CPI seasonal factors all ahead of the March meeting, continued progress on disinflation could still lead to a cut at that meeting. But today's meeting raised the bar for that outcome. While our baseline remains that the first cut will come in June, we see risks skewed towards an earlier reduction in May.

Goldilocks: Employment Cost Index Below Consensus Expectations in Q4; ADP Employment Below Expectations in January

BOTTOM LINE: The employment cost index rose 0.9% in 2023Q4 (not annualized), below consensus expectations for a 1.0% increase. Our wage tracker now stands at 4.1% on a quarterly annualized basis in Q4 (vs. 4.3% in Q3) and 4.6% on a year-over-year basis (vs. 4.4% in Q3). According to the ADP report, private sector employment rose by 107k in January, 43k below consensus expectations. We do not place much weight on the ADP miss because of ADP’s negative correlation with BLS private payrolls since the introduction of the new methodology. We left our nonfarm payroll forecast unchanged at +250k ahead of Friday’s release.

Goldilocks: January FOMC Recap: Pushing Back the First Cut from March to May

Amidst an otherwise dovish FOMC press conference, Fed Chair Powell gave a strong signal that a March funds rate cut “is probably not the most likely case.” Given this comment—as well as our expectation of solid growth in Q1 and a temporary firming in sequential inflation in January—we have pushed back our forecast of the first cut from March to May.

However, we continue to expect 5 cuts in 2024 and 3 more in 2025 because we expect core PCE inflation to fall at least a couple of tenths below the FOMC’s 2.4% median projection this year, with further declines in 2025. We now expect the FOMC to deliver four consecutive cuts at the May, June, July, and September meetings before slowing to a quarterly pace and adding a final cut this year in December. Our revised probability-weighted average Fed forecast is similar to our baseline in 2024 but a bit more dovish in 2025, though it is a bit less dovish than market pricing of about 6 cuts in 2024.

Powell also noted today that the FOMC will begin in-depth discussion of balance sheet issues at its March meeting. We think this probably means a staff presentation on options for slowing the pace of balance sheet runoff in March followed by a committee decision to slow the pace in May that will be implemented shortly thereafter.

Treasury’s 1Q24 refunding announcement contained no major surprises. Coupon auction sizes were raised by the same amount as in the November meeting, in line with our expectations, except for 30y TIPS auction sizes where the Treasury plans to maintain the auction size unchanged at $9bn (vs GS $10bn).

In line with Monday’s borrowing estimates, Treasury appears to have lowered its near-term deficit projections modestly, but this does not change the broader picture that deficit projections remain wide over the rest of the decade. We expect the Treasury to maintain the current auction sizes for some time.

Treasury continues to target elevated cash balances of $750bn. Reflecting the timing shift of deficits and our new buyback projections, we adjust our bill issuance projections to ~ $378bn and -$250bn in 1Q24 and 2Q24 (from $444bn and -$250bn previously), and expect bills as a share of outstanding USTs to remain above the TBAC-recommended 15-20% range over the next two years…

JEFF: Feb Refunding Review: One More Coupon Auction Size Bump for Good Measure

■ Treasury announced increases in coupon auction sizes for the coming quarter that were exactly in-line with the increases announced in November, and in-line with our expectations as well. Treasury continues to term out the debt following a historically heavy period of bill issuance, though they are being cautious about increasing sizes at the long-end of the curve. ■ Alongside the increased coupon issuance, Treasury offered guidance that they do not expect to increase auction sizes in May. ■ The combined context of the coupon announcements today and the financing estimates from Monday suggest that bill issuance will level out in the coming months and that paydowns will begin in Q2. ■ Small-value buybacks will begin in April "with a limited population of securities to test processes and infrastructure". Treasury intends to announce details of a broader buyback program in May.

JEFF: FOMC Extends Pause, Drops Tightening Bias, But Powell Torpedoes March Cut

Key Points ■ The Fed left all target and administered rates unchanged, as expected. ■ The policy statement went through an extensive re-write that shifted the skew of risks into better balance. References to additional policy firming were dropped. ■ Despite the pivot in the view on risks, the Committee made clear that they need greater confidence in the path of inflation continuing down to the 2% target before they are comfortable cutting rates. ■ Powell was careful to maintain a balanced approach to policy in the press conference, but his comments caused wild swings in the market's perception of the odds for a March rate cut, right up until he said that such a move was "probably not the most likely case". ■ With 2 employment reports, 2 CPI reports, and annual revisions to both payrolls and the CPI due out before the next meeting, we remain open to the idea that the Committee might find this "greater confidence" in lower inflation that they need to justify a cut by the next meeting. Data dependence remains the name of the game.

MS FOMC Reaction: March Is Out, B/S Discussions to Begin (… i thought the “BS” discussions have already begun … at the beginning of FOMC time …? regardless, staying LONG 5s)

According to Chair Powell, it isn't likely the Committee would be confident to cut by March. The Fed will be cutting rates this year, but is in no hurry. We continue to call for a June start. Our strategists stay long duration via 5y UST, and long agency MBS.

Key Takeaways

Rates decision: The FOMC held the policy rate in a range of 5.25-5.50%, where it has remained since July 2023. Year-over-year growth in core PCE inflation was 2.9% in December, and so the Committee has seen "good progress" toward its goals, but inflation is still "elevated".

Outlook:"Almost everyone" favors cutting rates this year, suggesting there has been no change in views since the December SEP. But the Committee is in no hurry to get started and Chair Powell was confident enough to rule out March. We continue to expect the first rate cut in June. Powell noted the Fed will begin in-depth discussions on the balance sheet at the March meeting. We expect a slow taper of QT to begin in June, end in 1Q25.

Rates: Our rates strategists think headline around the March cut, or timing of the first cut in general, has limited consequences for duration overall, and the totality of the Fed's communication is conducive to being long duration. They maintain long 5y USTs.

FX: The USD shows a close relationship to the pace of cuts priced by the Fed and by central banks abroad. A large rise or decline in the implied pace of rate cuts in the US and abroad (either above six or below two in six months) in the US and abroad would likely boost USD. A continued modest pace of cuts implied for the Fed and other central banks (roughly three to five in six months) will likely weigh on the USD relative to yield differentials.

MBS: Our MBS strategists maintain their neutral index positioning, suggesting that the 2019 cutting cycle is the right framework, and they think the index should trade between 40bp and 55bp.

… Bottom Line: The Fed is still concerned that inflation could reaccelerate with the economy running hot. But inflation has been slowing and labour markets have shown signs of moving into better 'balance', to-date through a slowing in excess hiring demand (eg. lower job openings) rather than significant increases in the unemployment rate. We continue to expect the unemployment rate to edge higher in the first half of this year and for inflation to continue to ease back towards the 2% inflation objective. Chair Powell said directly that a rate cut in March is "not the most likely case." But we continue to expect a pivot to interest rate cuts by mid-year.

… Over the four quarters of 2023, the ECI rose 4.2%, not far from the increase in average hourly earnings (charts below), and down from the 5.5% peak two years ago…

ADP private employment up 107K in January …We noted in our preview Friday that ADP has disappointed the past few January's so that seasonal pattern repeated. We would also note that ADP estimates last January's private employment gain to be 119K, far short of the BLS estimate of 353K. Despite ADP estimates being closer to the BLS estimates in recent months, for 2023 as whole the correlation between the two estimates of private employment was -0.2, not even positively correlated over the 12 months…

…Implications for Friday and the FOMC Looking ahead to Friday's release of the BLS's January employment report we continue to expect an outsized gain in nonfarm payroll employment due to what we have been calling "sunbelt seasonality" - essentially a reduction in seasonal amplitude in some economic activity due to summer and winter in the US economy…

…We also do not think such a gain would dissuade the FOMC from a 25 bp rate cut at the March FOMC meeting if inflation data unfolds as we expect …

Chair Powell not declaring victory and March cut not a base case Chair Powell said quite flatly that the Committee's base case was not a March cut, but ultimately they would be data dependent. He also said that the Committee's inflation forecasts would likely be lower now than at the December FOMC meeting. With another Summary of Economic Projections in March, and the ability to use that for forward guidance, we are still inclined to think that the FOMC reduces the target range for the federal funds rate at the March meeting. However, we see the risks that the Chair needs to see more information and gain more confidence that inflation is improving before deciding the Committee can move as soon as March…

Wells Fargo: Labor Cost Growth Falling into Line for Fed's Inflation Fight

Summary The Fed's preferred measure of labor costs shows inflationary pressure from the jobs market rapidly easing. The Employment Cost Index (ECI) rose 0.9% in the fourth quarter, which was the smallest quarterly increase in over two years. The outturn was a tick softer than expected and came despite a meaningful rise in compensation costs for unionized workers. On an annualized basis, the ECI rose 3.5% in Q4, in the range of what is consistent with the Fed's 2% inflation target.

Wells Fargo: FOMC Removes "Bias" To Tighten, but Don't Expect Imminent Easing

Summary

As universally expected, the voting members of the FOMC decided unanimously at their meeting today to make no changes to the Fed's policy stance, keeping the fed funds target range at 5.25-5.50% and maintaining the current pace of quantitative tightening.

The FOMC also removed its implicit "bias" to tighten further. That is, the Committee dropped its reference toward "any additional policy firming that may be appropriate..."

But we are not convinced the conditions will yet be in place to induce the FOMC to cut rates as soon as its March 20 meeting. The statement indicated that "the Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent."

A rate cut in March is not out of the question, but it would likely take another small increase in core PCE prices in January, in conjunction with soft data on economic activity, to compel the Committee to move in March.

We look for the FOMC to cut rates by 25 bps at its meeting on May 1 and then another 100 bps by the end of 2024.

… And from Global Wall Street inbox TO the WWW,

AllStarCharts: Why It’s Time To Short Stocks (hint: bonds)

… It’s the rotation into defensives that is the make or break for this bearish approach to the market:

To me it’s that simple.

If Consumer Staples relative to the S&P500 are above those December lows, we want to be short equities.

…Below is a look at the S&P 500's intraday path throughout today's trading day compared to the index's average path across all Fed Days since Powell has been Fed Chair. Note the pump-fake spike between 2:30-3 PM ET followed by a sharp sell-off in the final hour of the day. Based on the stock market's action, it was a pretty bread and butter Fed Day if you ask us.

Bloomberg: Fed’s Powell Cements Pivot But Pushes Back on Timing of Cuts

Bloomberg: That March Fed rate cut? Pretty, pretty unlikely (Authers’ OpED)

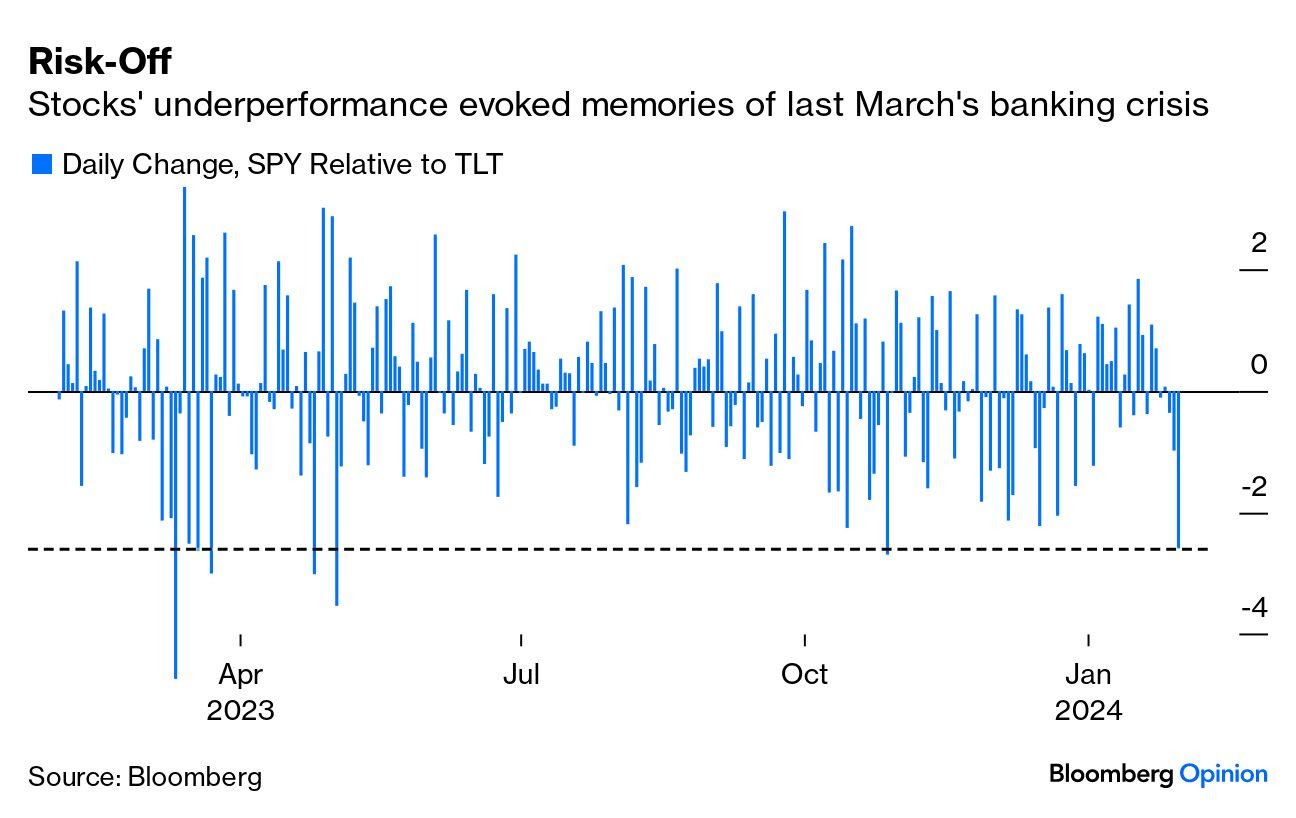

… The stock market appeared to have put more weight on imminent cuts than anyone else. A busy day had already included: results from Alphabet Inc. and Microsoft Corp., news of serious difficulties for New York Community Bank that pushed its stock down 45%, an announcement from the Treasury that it was going to be auctioning over the next three months somewhat more longer-term bonds than had been expected, and macro news suggesting the labor market might be cooling down a bit. Despite all of this, the circumstantial evidence is that it was Powell’s words on a March cut that substantially did all the damage:

Stocks had the worst day in some months. Meanwhile, bonds enjoyed a rally, swallowing the bond supply news without difficulty. Instead, the fears around New York Community Bank sent people rushing to buy Treasuries, largely on the theory that renewed banking trouble would force the Fed to ease. Yields rose during Powell’s press conference, without getting back to their previous high, and then sank as traders shifted positions for the end of the month:

This was a vintage risk-off day, with money moving out of stocks and into bonds. The problems at NYCB, which took over some of the assets of the failed Signature Bank last year, played a big role. A loan-loss provision of $550 million, mostly for real estate, came as a nasty shock, and drove a big asset-allocation move. If we use the SPY and TLT exchange-traded funds as proxies for the S&P 500 and for Treasury bonds of 20 years or more, we find that this was the sharpest risk-off day since the sudden raft of bank failures last March:

There were plenty of cross-currents, but the nerves over Big Tech also mattered a lot.

…In our opinion. the Fed's primary focus should be on not cutting rates too aggressively or prematurely, which could reignite the inflation problem like the Fed did on multiple occasions under Chairman Arthur Burns in the 1970s. The economy is still growing, but we think it falls into recession before the year is out and that real GDP growth significantly lags the predictions of the FOMC members. Given that the Fed has now signaled 75 bps in rate cuts even in an environment of moderate growth, if we are right about slower growth, it will be very difficult for the Fed to resist generating higher inflation in 2025 and beyond.

ING: Slowing US employment costs offers more hope for interest rate cuts

Employment costs are cooling broadly despite the tight jobs market. Nonetheless, with the quit rate falling it suggests the jobs that are on offer are not especially attractive, implying less incentive to pay more to retain current staff. This cooling labour cost environment offers the Fed the room to cut interest rates meaningfully to neutral levels

The Fed held the Funds rate unchanged and reiterated it remains data dependent. The Fed needs more confidence that inflation has sustainably returned to 2% before lowering rates. March is not the base case for a first cut according to Powell.

WolfST: Wow, Fed’s Statement Pushes Back against Rate-Cut Mania and End-of-QT Mania, Holds Rates at 5.50% Top of Range, QT to Continue as Planned

ZH: Is NY Community Bancorp The Canary In The Fed's QT-Ending Coalmine? (funTERtaining to think ‘bout esp on heels of FOMC meeting)

The price of shares in New York Community Bancorp - the regional bank that purchased deposits from Signature Bank last year - are crashing this morning, below SVB crisis lows, after reporting a surprise loss for the fourth quarter and a cut to its dividend.

Management had previously said asset quality was strong, so “something has clearly changed in their tone,” Jon Arfstrom, an analyst at RBC Capital Markets, said in a note to clients.

“This was a material negative surprise.”

As Bloomberg reports, the bank lowered its quarterly payout to shareholders to 5 cents. Analysts had predicted the dividend would remain at 17 cents. A worsening credit outlook contributed to the unexpected loss, as the company boosted its loan-loss provision more than expected…

… Finally, with all this said and in mind, asking IF you thought this one aged well …

I heard the Chief Eco from Santander say No Cuts until after US Elections

"And frankly you can skip the rest of the note"

HAAAA!!