while WE slept; JPOW @ 11a 'unlikely to sound as dovish as Waller'; financial conditions largest EASING in last 40yrs; "The chart we love to hate"; GDI (from Wed)

Good morning and thank you for your patience as I needed some ‘time off for good behavior’ yesterday. Lets jump back in to what I missed and where / why we are, here and now…

ZH: WTF Chart Of The Day: Chicago PMI Beats Expectations By 13 Standard Deviations...

… SO yesterday put more wind in the sales of DISinflation’istas (dare I call them TRANSITORIANS??) while at the same time adding fuel to the higher for longer campers with Chicago data keeping us all on our toes and guessing?? Who will be right (RenMAC or guys like Bianco — you’ll have to decide as they BOTH make compelling arguments and have data yesterday supporting their differing views).

Meanwhile as the month came to a close and ahead of this WEEKS close,

… arguably diggin deep here to try and find a chart with any relevance and while momentum is approaching overBOUGHT on WEEKLY (more medium term) and as yields have dropped ~40bps in such a short period of time one takes a step back puts moves in context and there COULD be plenty of room for yields to move lower IF one in the RenMAC de / dis inflation camp … I’m not quite there YET but again completely understand data is, at least for now, cooperating (unless you view some of the other data where it isnt) … for NOW we’ll bask in the glory of a good year this past month and …

ZH: Mo'vember Marks Best Month For US Bonds In 40 Years; Global Markets Add Over $11 Trillion

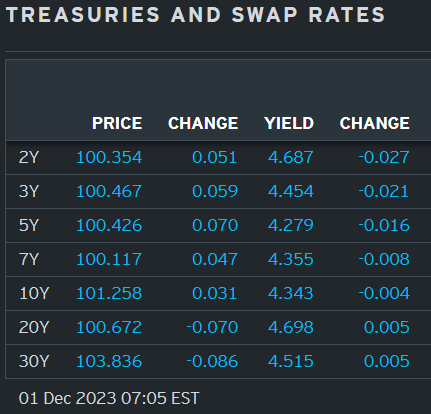

… here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… NY Open - Speak Now High anticipation for Chair Powell's speech today meant muted moves to start the month. G10 FX trades in tight ranges, while select high-betas retrace Thursday's losses (ZAR, MXN). Overnight, while CNH traded flat, an unusual PBoC yuan fixing, and a surprise beat in Caixin China PMI caught our eye. Korea trade balance surprised, with a strong beat in exports, though KRW underperformed as it played catch-up to recent USD strength. Oil prices trade flat after a disappointing OPEC+ meeting on Thursday.

Our economists think that Chair Powell (11:00 EST) will unlikely sound as dovish as Waller, any reiteration of "higher for longer" would send yields and USD higher, which we should ultimately fade. ISM manufacturing precedes Powell at 10:00, we expect a small rebound. Canada expects an employment report (08:30 EST) and Manufacturing PMI (09:30), neither should shift BoC pricing much. Latam countries await Manufacturing PMI, BRL also watches IP at 07:00, PEN sees CPI at 10:00…

… Treasuries traded broadly flat overnight, with the highly anticipated Powell speech later today. Our Asia desk notes the key theme has been de-risking ahead of Powell speech. CTAs are flipping long in 2s, 5s, and 10s, but there is room for more inflows.

… and for some MORE of the news you can use » The Morning Hark - 1 Dec 2023 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

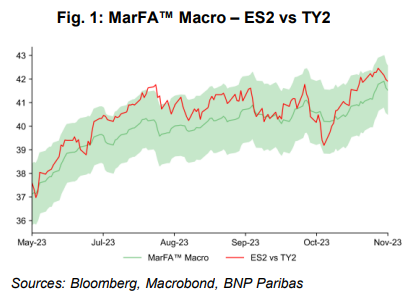

BNP: QTOW: Short SPX vs long US 10y reaches target (from Wed morn AFTER hitting send)

We take profit on our short ES2 vs long TY2 position as it reached its target this morning. The trade has benefited from this week’s decline of US 10y Treasury yield against a backdrop of a stable S&P500.

We entered the trade idea on 20 November to benefit from the divergence of asset valuations: MarFA™ flagged that S&P500 appeared overbought, while the bond appeared oversold. The fair value for the ES2/TY2 ratio has risen over the life of the trade, resulting in a smaller gain (0.6%, USD 180k) than originally expected (2.5%).

The rationale for this trade also provides an insight into why the S&P500 has not reacted to comments from Fed Governor Waller – it already appeared rich heading into the start of this week, while bonds appeared cheap.

Looking ahead, we maintain our positive view on risk, with our metrics highlighting:

Risk sentiment has scope to improve further, as our global risk premium index (BNPSGRP Index) has moved towards a more neutral level.

US credit spreads remain near their tightest level of the year. These are identified as a key explanatory and leading factor, according to MarFA™.

Lower global yields are supportive for risk-asset valuations

To position for this view …

DB: The chart we love to hate (curious how this one continues to come back to us)

Every so often, we are reminded of the intriguing yet dubious relationship between Fed liquidity and risk asset prices. The latest iteration, shown in today's chart, suggests that changes in bank reserves (a stand-in for Fed-supplied financial market liquidity) explain S&P returns over the last three years. We are skeptical of any argument that attempts to draw a straight line between liquidity and risk asset returns, mainly because their relationship is not consistent over time. Extend the analysis beyond the last few years, and the correlation drops to essentially zero.

Contrary to periods of active Fed QE, the latest expansion in bank reserves primarily stems from money market funds scaling back usage of the ON RRP. The traditional portfolio rebalancing channel of the Fed buying bonds (creating reserves in the process), crowding out investors into riskier assets and driving those prices higher is not evident. Money market funds participate in a wholly different market than most investors, and there is little substitutability between stocks and short-term risk-free investments like bills and repos that money market funds buy.

A more plausible explanation is that reserves and risk assets are both responding to a common external factor: changes in expectations of short-term interest rates. Anticipations of the Fed's policy path wield considerable influence over money market funds' choices to use the ON RRP. If money funds expect the Fed will hike more than the bill curve has priced, then they will invest in the ON RRP to participate in rising rates. If they think the Fed is done hiking, then deploying cash outside the bill curve might be the better strategy. These decisions directly alter the quantity of reserves. At the same time, market expectations of the stance of monetary policy affect the valuations of risk assets. In an environment defined by large money market fund AUMs and heightened sensitivity of risk to the Fed outlook, it’s unsurprising that reserves and asset prices share an increased correlation, although their correlation should not be mistaken for causality.

… Since it’s the start of December this morning, we’ll shortly be releasing our monthly performance review for November. Overall, it was a great month for markets after a run of three fairly weak ones, which has led to a big turnaround in some of the YTD numbers for 2023. In fact, it was the best month for global bonds since December 2008, the best month for US bonds since May 1985, as well as the strongest month for the S&P 500 this year. The full report will be in your inboxes shortly…

Goldilocks(Tony Pasquariello … markets / macro … offering because of how he begins)

I don’t often lead with a chart, but this one cuts immediately to the punch line:

the month of November saw the largest easing in US financial conditions of any single month in the past four decades:

beneath the hood, it was a clean sweep, and of significant magnitude: stocks up, rates down, dollar weaker, credit tighter…

Goldilocks: Core PCE Inflation Falls Further; Personal income and Initial Claims in Line With Expectations

BOTTOM LINE: Both personal spending and income increased by 0.2% in October, in line with consensus expectations. The saving rate edged up to 3.8% from an upwardly revised 3.7% in September. The October core PCE price index rose by 0.16% month over month, in line with expectations, and the year-over-year rate declined another 0.2pp to 3.5%. Core services prices excluding housing were soft, rising just 0.15% month over month. The consumption details of the October personal income and spending report were broadly consistent with our previous assumptions. We will update our GDP tracking estimates after the mid-morning data.

… The big news in today's data however, was PCE inflation. Core PCE inflation fell to 3.46% in October. That compares to the FOMC median projection of 3.9% for the full year (Q4/Q4) in their June projections, and the 3.7% full year projection in the FOMC's September projections. In our economic comment in last week's US Economics Weekly "Fed restrictive or higher for longer?" we expect the speed of this inflation improvement to drive changes in the FOMC communications at the December meeting, and we are already hearing in comments from participants this week of the increasing comfort that they have done enough with rate hikes. In the October data released this morning, core PCE prices over the last six months have risen just 2.48% at an annual rate… getting closer to the FOMC's 2.0% objective.

Core PCE inflation slips to 3.5%; Past 6 months at 2.5%…

Chicago PMI bounces in November The Chicago PMI moved up 11.8 points to 55.8 in November, besting consensus expectations of 46.0, and hitting the highest level since early 2022. That moved the index into expansionary territory for the first time in 14 months. Respondent firms noted slowing increases in prices paid, increasing new orders, and improved employment. Backlogs of work continued to contract, but at a slower rate. In general, today's release was significantly stronger than the recent Federal Reserve manufacturing surveys, which have been weak for an economic expansion, even though some have improved in recent months. Also, a production rebound related to the end of the UAW strike may have contributed to this month's bright reading from the Chicago chapter of the ISM.

After receiving the remaining surveys of November, we continue to expect the ISM manufacturing index moved up 2.8 points to 49.5 in November, the data released tomorrow, above the current consensus estimate of 47.8.

UBS (Donovan): Central banks keep tightening (involuntarily)

European and US inflation numbers again surprised the markets by coming in lower than expected. The ending of the 2021–22 transitory inflation was very rapid (in the US, durable goods inflation went from record high to deflation within nine months). It may be that the ending of profit-led inflation is similarly fast. This does, of course, mean that real central bank interest rates are rising more rapidly—and the full effect of past monetary tightening has yet to be felt….

Wells Fargo: Moderation in Personal Spending Amid More Cooling in Prices

Summary Today's personal income and spending report shows consumers are throttling back. Not only are households spending less, but also the composition of outlays is tilting in a way that suggests a more budget-conscious mindset even as income is holding up better than first reported.

… Meanwhile, the year-ago rate of core PCE inflation came down to 3.5% from 3.7% a month earlier (chart), which was expected. Headline inflation slowed to 3.0% from 3.4% the month prior, and this was a bit more of a cooling than was expected.

Wells Fargo: Revised GDP Data: Profit Growth Remained Robust in Q3-2023 (chart of GDI has ME at hello and so, while this is now OLD news, am still sharing … as it IS convincing to one for the HARD LANDING camp)

Summary

The sequential rate of real GDP growth in Q3-2023, which was originally reported as 4.9%, was revised up to 5.2%. Although growth in real PCE was tamped down a bit, growth in real fixed investment was not as weak as originally reported.

Today's release provided the first look at the income side of the National Income and Product Accounts. In that regard, real gross domestic income rose only 1.5% in the third quarter, marking the fourth consecutive quarter in which growth in real GDI has not kept pace with growth in real GDP. Wages and salaries continue to rise at a strong pace, at least in nominal terms, but elevated inflation is eroding the real value of those wage increases.

Despite weak growth in GDI, corporate profits rebounded in Q3. Pre-tax profits rose by the most in five quarters, leaving the level of profits only a stones-throw away from the recent cycle peak.

Economy-wide profit margins also improved during the quarter amid a sturdy level of end-demand offsetting a still-high cost environment.

Rebounding profits can be supportive of economic growth, but to the extent we see renewed pressure on margins in coming quarters, headcounts and thus broader growth may be at risk of slowing. Recession risks are elevated, but a downturn is far from a certain outcome particularly in an environment of rebounding profits growth.

… The second release of the National Income and Product Accounts (NIPA) for any quarter is important because it is the first time that analysts get to view income creation data in that quarter. In theory, the income side of the NIPA accounts should be equivalent to the spending side. That is, the act of spending creates an equivalent amount of income for somebody in the economy. In reality, however, the two sides rarely are identically equivalent due to data errors and omissions. In that regard, real gross domestic income (GDI) grew only 1.5% in the third quarter on a sequential basis. Indeed, growth in real GDI has lagged growth in real GDP for four consecutive quarters. On a year-over-year basis, real GDP is up 3.0% while real GDI is down 0.2% (chart). Growth in real consumer spending, which was up 2.3% on a year-ago basis in the third quarter, could eventually be at risk if growth in real income remains weak. Although nominal wages and salaries rose 5.6% (year-over-year) in Q3, high inflation is eroding growth in real purchasing power.

Stocks rallied today as October's PCED inflation rate continued to moderate. Most importantly, the inflation rate of PCED services excluding energy and housing is falling. It has been stuck around 5.0% in 2022 and earlier this year. But it was down to 3.9% y/y in October (chart). Fed Chair Jerome Powell and his colleagues have said that they are concerned about the stickiness of this "super-core" measure of inflation. Now, they should be less concerned as it seems to be coming unstuck.

Also cooling off is the growth rate of consumer spending. The Atlanta Fed's GDPNow tracking model shows that real consumer spending is rising at a 2.7% saar during Q4, that's down from Q3's 3.6% pace. Real GDP is tracking at a 1.8% pace down from 5.2% during Q3…

… And from Global Wall Street inbox TO the WWW,

Bloomberg: Battered stock bears got their Fed calls right: The Weekly Fix

An Annual Tradition It’s that time of year when everyone pokes fun at Wall Street strategists for their year-ahead targets that never came to fruition. There’s plenty of material to make hay with this time around: recall that heading into 2023, the average forecast called for the S&P 500 to decline, the first negative prediction since at least 1999. So naturally, the S&P 500 is sitting on 19% year-to-date gains.

But an interesting wrinkle is that the root cause of some of the most bearish fantasies was generally correct: the Federal Reserve was more aggressive than widely expected, and yields soared to eye-watering heights as a result. However, it was the follow-through from those higher rates that has yet to materialize: the widely heralded recession never came, corporate profits didn’t exactly crater and US consumers are still spending.

There’s a few potential reasons why. One, the US economy is less rate-sensitive compared to past cycles — a dynamic that Fed chair Jerome Powell acknowledged just last month. That’s resulted in longer and more variable lags.

Second, it turns out that the S&P 500’s heaviest hitters — the megacap technology companies — don’t necessarily have an adversarial relationship with higher rates. Rather, the tech companies that have powered index-level gains in the stock market this year are generally better equipped to deal with interest expenses and refinancing risks than their smaller brethren. Additionally, companies such as Alphabet Inc. and Tesla Inc. have actually profited from their massive cash hoards in recent quarters.

In sum, the 2023 Wall Street forecasting experience raises a question that this newsletter has asked before: even if you knew, what would you do? Having the proper information and starting point in hand is useful, but markets are under no obligation to behave. It’s a fun thought exercise.

“I think it’s fashionable to make fun of strategists when they’re wrong, but at the end of the day, if you have a process you can respect and understand what drove them to that decision, they can still be valuable,” Adam Parker, CEO of Trivariate Research and former Morgan Stanley chief US equity strategist, told Bloomberg’s Alexandra Semenova.

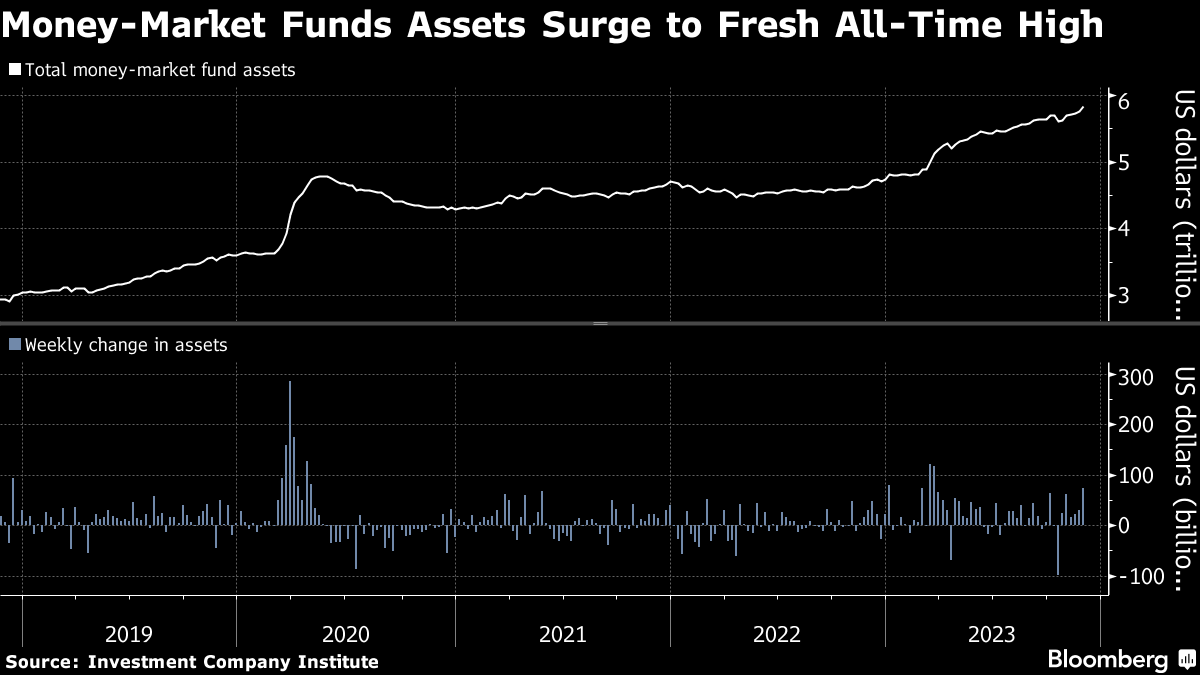

Cash is (Still) King A defining feature of 2022 was cash’s outperformance in a year when everything went wrong. In 2023, demand intensified further. Heading into 2024, that momentum is still building.

Assets in money-market funds soared to yet another record high of $5.8 trillion in the week through Nov. 29, according to Investment Company Institute data. A $73 billion inflow pushed it to those fresh heights — the largest weekly haul since March, when tremors in the US financial system drove depositors out of banks.

All told, more than a trillion dollars have been added to money-market funds so far in 2023. Lofty yields on the shortest-dated paper means that cash is attractive beyond its traditional role as a safe-haven asset. Meanwhile, depositors — rattled by March’s events, and frustrated by banks not passing on higher rates quickly enough — have flocked to money-market funds as well.

In the eyes of Federated Hermes’ Deborah Cunningham, another trillion dollars is in the offing. Next year should be “another banner year” for money-market funds, she said, given that the massive inflows thus far have primarily been from retail investors.

“What hasn’t really started in earnest yet is the institutional movers,” Cunningham, the firm’s chief investment officer for global liquidity markets, said in a Bloomberg Television interview. “Those institutional movers generally wait until interest rates have peaked or plateaued, and then they really start to come into the product once rates start to go back down again.”

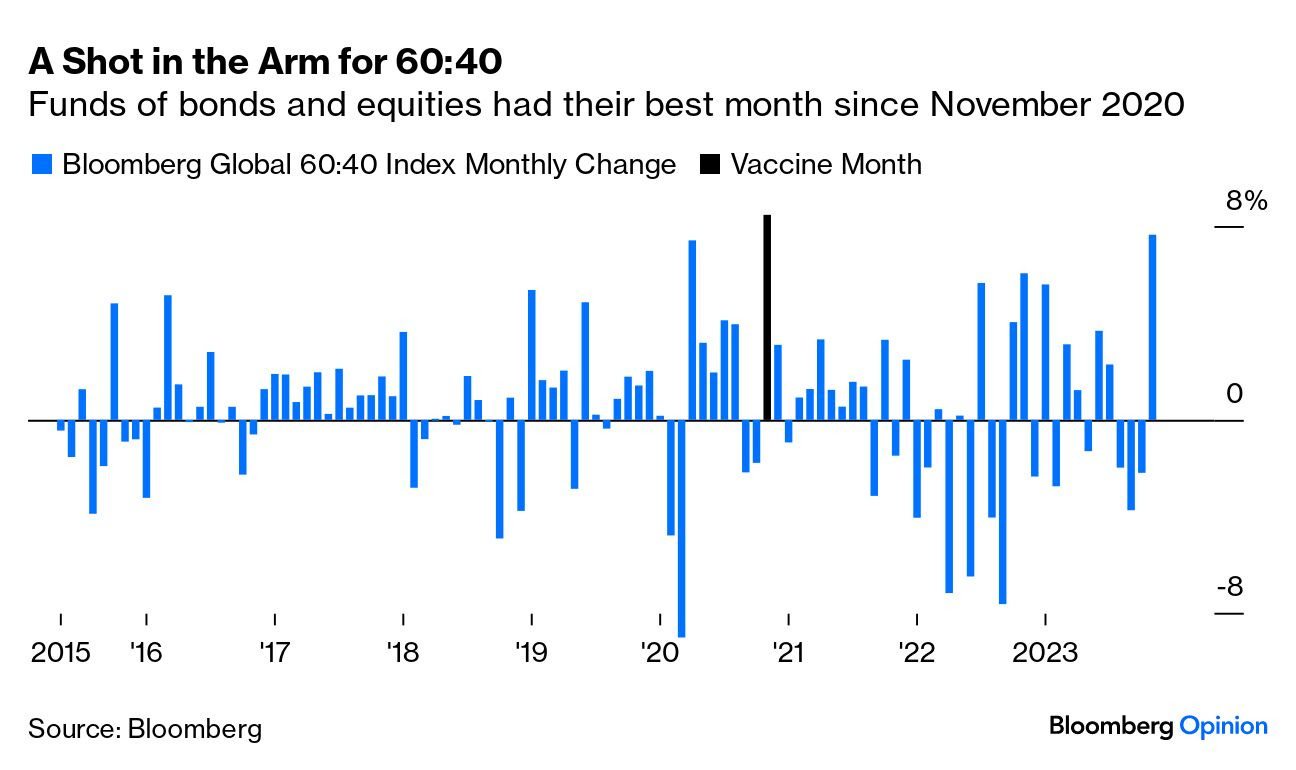

Bloomberg: Coming down inflation is no walk on Table Mountain (Authers OpED on 60/40 mention AND on 2yy BREAKS vs Earl…)

… It's undeniable that the descent has gone far better than expected for the last few months, which explains the startlingly strong performance of both US bonds and stocks this month. Bloomberg’s own index for a global 60% stocks 40% bonds portfolio is up 8% for the month, only marginally behind November 2020, the month when surprisingly successful Covid-19 vaccine tests sparked a relief rally:

It’s questionable whether this month’s news on prices really justifies a market reappraisal on the scale of that one. As with hikers on Table Mountain, it’s well not to take this too lightly. But it’s easy to understand that investors now want to convince central banks that a Matterhorn-style descent might be better after all…

… the long established relationship between oil prices and market inflation breakevens hasn’t had much effect of late. In theory, higher oil prices should reduce expectations for future inflation by creating a higher base. In practice, higher oil prices in the present tend to translate directly into higher inflation expectations, in large part because inflation traders tend to use oil futures as a hedge. What’s interesting is that the rise and fall of the oil price over the last few months has passed with minimal impact on US short-term inflation breakevens:

At a time when two separate conflicts are raging, both with the potential to bring supply of fuel down sharply, this may seem surprising. But as it stands, the oil market isn’t scared of OPEC+, and other markets aren’t scared of oil.

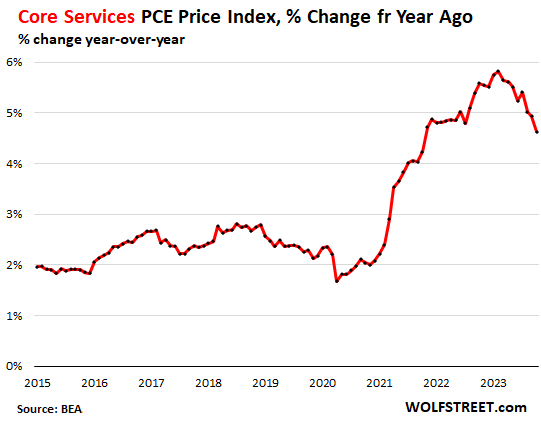

WolfST: Beneath the Skin of the PCE Price Index: Inflation in Services

Gasoline plunged, durable goods fell. Inflation still hot in services: housing, insurance, healthcare, transportation (incl. auto services). Food inflation simmers.

… Year-over-year, the core services PCE price index decelerated to 4.6%. We’ll get into the major components of core services in a moment.

ZH: Q3 GDP Revised Higher To 5.2% As Soaring Government Spending Offsets Lower Private Consumption (following up on GDP given I was out and MARKETS seem to be celebrating just about EVERYTHING, good or LESS good)

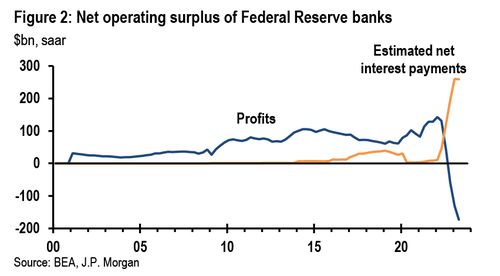

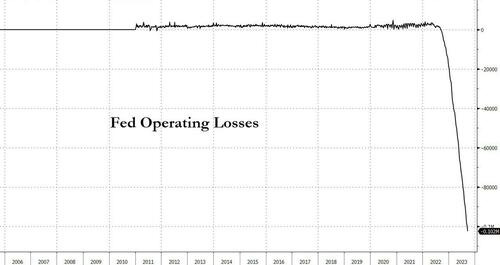

ZH: What's Behind The Record Divergence Between GDP and GDI, And Why Tomorrow The US Economy Will Be Revised Sharply Lower (did someone say GDI? outstanding!!)

… And while we discussed all this and more previously, a key question some may ask is what is the reason behind the massive divergence between GDP and GDI?

For the answer we go to a recent note from JPM chief economist Michael Feroli who correctly notes that one dark cloud hanging over the US economic outlook all year has been the very weak performance of real gross domestic income (GDI), which has contracted 0.5% over the past four quarters.

As noted before, GDI should equate with GDP, and past research has indicated that averaging GDI with GDP (also called GDO, or gross domestic output) provides a better measure of the underlying growth of economic activity than either measure viewed in isolation. Obviously, incorporating GDI clearly sends a more downbeat message about the economy’s recent performance, and suggests that the surge in the US Dollar and 10Y yields are just huge headfakes, and once the revised data is released we could see a brutal mean reversion in both the greenback and US Treasuries.

But going back to the key question - what is behind the record difference between GDP and GDI - Feroli answers that this is the result of previously omitted net interest payments by the Federal Reserve, which will be corrected by tomorrow's data revision, thereby boosting GDI. By itself this revision would close about half of the gap between these two broadest measures of the size of the economy.

As Feroli explains next, "consistent with their legal status, the National Income and Product Accounts (NIPAs) consider the Federal Reserve banks to be financial corporate businesses." Their contribution to GDI has so far been in corporate profits, which track closely to the net income of the Federal Reserve system. Recently, the profits of the Federal Reserve banks have rapidly deteriorated, contributing to the weakness in GDI.

This deterioration has been the result of ballooning interest payments on the Fed’s liabilities as short-term interest rates have increased (this would also explain the confusion experienced by Albert Edwards recently when he looked at a variation of this chart to conclude that it was "The Maddest Macro Chart I Have Seen In Many Years").

So to address the unprecedented collapse in Fed profits as a result of soaring interest rates...

All work and no play makes Jack an angry boy :)

I saw that PMI number and I thought it looked strangely high.

Strike-end effect sounds plausible.

Heard Jim Bianco saying that the 10 yr Bond might go to 5.5%,

next year.

I usually give a lot of credence

to what he says....but that seems

less and less likely to happen.

Really amazing to watch the effect

of 1.5 - 2T in Gov't deficit spending

on the Economy and in the Economic numbers.

John Maynard Keynes and John Kenneth Galbreath would be

Thrilled !!!