Good morning … WELP, 1 outta 3 ain’t bad especially when that 1 GOOD liquidity event a bit further out the curve (and so, not related directly TO the FedFunds level, but rather only tied to yield curve / duration plays), well … ZH

… HEREis what another shop says be behind the price action, you know,

WHILE YOU SLEPT Treasuries are lower with the curve steeper out to 20yrs, correcting a decent share of yesterday's middle-session and 20yr-led flattening. What news we found is linked above, DXY is lower (-0.25%) while front WTI futures are higher (+1.45%). Asian stocks were mixed, EU and UK share markets are little changed-to-modestly lower and ES futures are showing -0.4% here at 7am. Our overnight US rates flows saw no reportable flows during Asian hours with volumes running quite weak (just $60mln 30's traded in Asian hours, only $700mln 10's in the screens then...).

… US News: Here's the KC Fed's agenda for the Jackson Hole sumposium: KCFed Institutional investors backing away from the 'overheated' US housing market BBG Historically, Jackson Hole hasn't been a big event for US stocks WSJ August on the verge of being tropical storm - free for only the third time in 60 years ZH

… it's another day and another slack-jawed update of German year-ahead power prices. We only beat this drum again because, to the surprise of nobody, the next chart is its analog.

… and for some MORE of the news you can use » IGMs Press Picks for today (26 Aug) to help weed thru the noise (some of which can be found over here at Finviz).

If there was little to add YESTERDAYjust ahead of the JHOLE CONFAB, there’s even less so today with NO UST supply and 10a speech by JPOW.

Here are a couple / few things to help you look busy and keep you fingers off the trading buttons.

First and foremost, what may be THE BIGGEST REASON to choose NOT to make a (buy / sell) CHOICE,

… The MOVE index of implied bond volatility -- at times seen as the Treasuries fear gauge -- has rarely been this high in late August. In fact, the only other times it was around or above current levels at this time of the year was in 1990, 2002-03 and 2009. In 2008, it would later move a lot higher, of course, as the global financial crisis struck.

It is noticeable that those prior occasions came either during or just after the Fed cut rates rapidly, rather than in the middle of steep hikes as is now the case.

With the strongest inflation in 40 years and central banks’ policy response threatening to tip the world into recession, investors are right to be nervous. But that doesn’t mean that potential outcomes from Jackson Hole have been fully priced in.

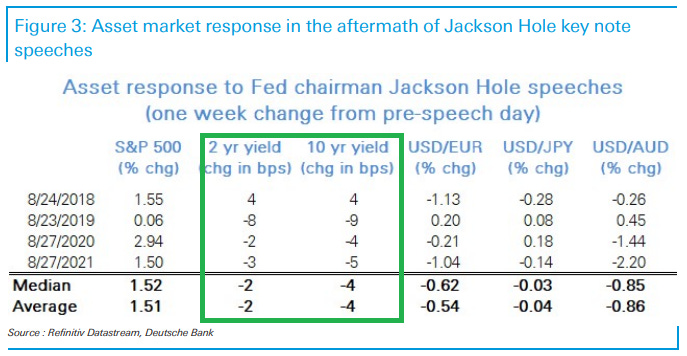

DB offers some context ahead of today’s JHOLE 10a speech by JPOW

… Irrespective of the leaning of Powell’s remarks, today is likely to mark a big divergence from the messages of recent years. It was only back in 2019 that Powell used his speech to comment that “Low inflation seems to be the problem of this era, not high inflation.” Then in 2020 as he discussed the Fed’s review of their monetary policy framework, he said that “The persistent undershoot of inflation from our 2 percent longer-run objective is a cause for concern.” And even in 2021 as inflation had risen above target, Powell discussed why the inflation spike was likely be temporary, citing factors such as the absence of broad-based price pressures. So we’ve come a long way since then.

DB also offers,

What not to expect from Powell, but to expect from markets

The macro backdrop for Powell's Jackson Hole speech is far more favorable than might have been feared a month or two back. The Fed is faced with a surprisingly robust labor market, evidence of a peaking in inflation, and financial conditions that have taken Fed tightening on the chin.

The experience of Jackson Hole 2021, will make the Fed Chair cautious in making the same error twice. That itself argues against his messaging looking too far forward, or, erring on the dovish side. Markets have however largely taken this on board, which risks a small, short-lived ‘buy the rumor, sell the fact’ technical bond rally, sell the USD, and relief equity trade.

Historically, the market responses on the day of the Jackson Hole key note speech have been restrained (see Figure 1). Even in the short term, Powell's speech will likely lack specifics on the 50bps vs 75bps next FOMC call that remains 'data dependent'. Next Friday's NFP, rather than this Friday is the real vol event.

The S&P above 4000 has likely fully priced a yield curve mix of a 3.5%+ fed funds and a 3%+ 10y yield. It is likely that over time the Fed will have to go beyond what is priced, on the assumption that the inflation impact of supply side improvements will need to be supplemented by greater demand restraint for the Fed to come close to reaching its inflation target on a desired timetable.

… As to the immediate market reaction a short-lived ‘buy the rumor, sell the fact’ technical bond rally, sell the USD, and relief equity trade, is most likely, even if the multi-week/month messaging is the reverse - one of a Fed seeking tighter and not easier financial conditions, if it is to reach its 2% inflation target.

The Federal Reserve’s Jackson Hole summer camp has a speech by Fed Chair Powell. Powell has three problems. First, as Powell has trashed forward guidance, specific signals for the September policy decision cannot be believed.

Second, Powell is not an economist. Greenspan, Bernanke, and Yellen delivered speeches outlining the Fed’s philosophy around structural change and the theories they supported. Powell lacks the background to do that. Third, many US citizens do not know who Powell is and the overwhelming majority will not hear a word Powell says today. A gallon of gasoline has far, far more impact on inflation expectations than anything Powell says today. Powell should offer a brief apology for the June policy errors and go back to toasting marshmallows…

Gotta say that JPOW isn’t an economist isn’t really a problem. At least not in MY eyes. Economists led ME to believe the idea of TRANSITORY and furthermore, it’s not as if JPOW is down in the basement of the Eccles building, running quantametric models. He’s got like 10s of econ geek staff who truly are to … blame?

Moving right along and watching for whatever ECB has to say over the weekend (SCHNABEL?)

Wells: Pipelines & Lifelines: Implications of Russia's Gas Supply Disruption If Russia were to shut off the flow of natural gas into Germany, it would impart a negative shock to the German economy, and by extension Europe. The United States has ramped up its natural gas export capability in recent years. But lacking the proper import facilities at present, Germany is not yet ready to take full advantage of U.S. natural gas, although many other parts of Europe already are. The actions of the U.S. and other countries would be insufficient in the near-term to replace an ongoing reduction in European gas supplies from Russia.

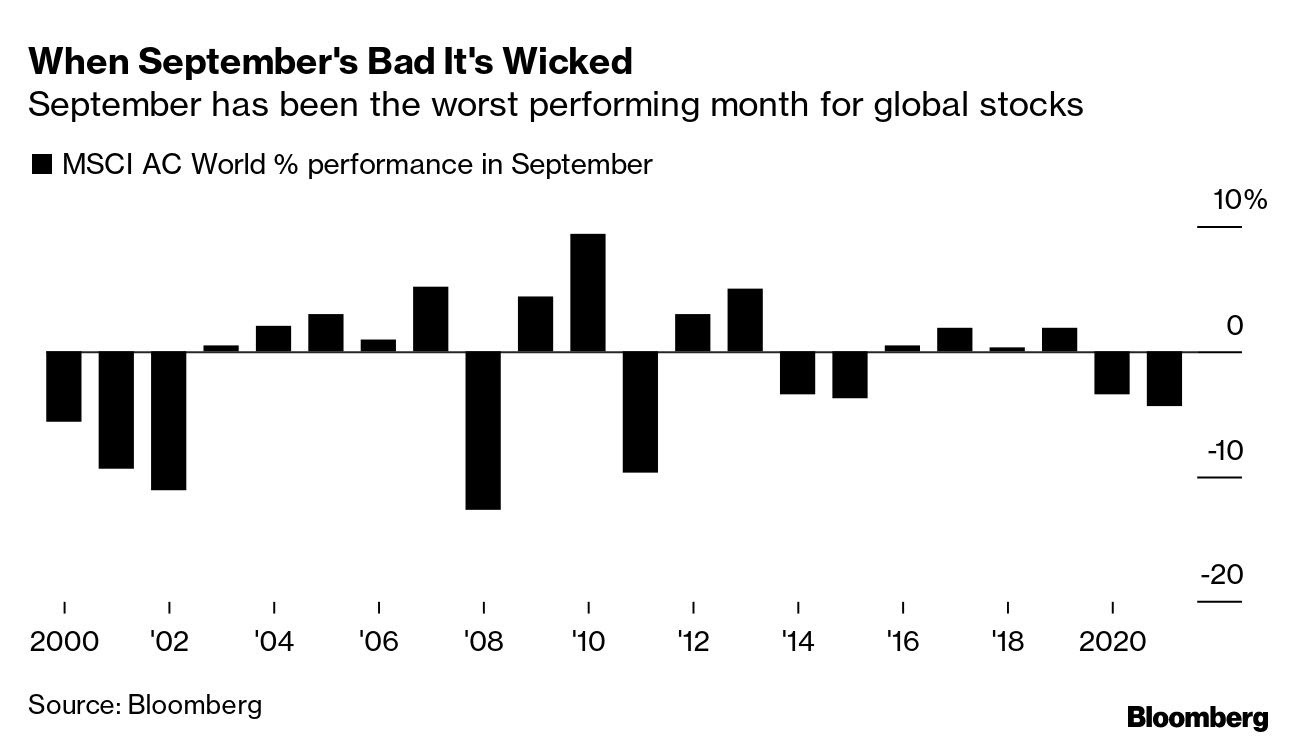

HERE is a tidbit on what to expect in SEPTEMBER with regards to equities and seasonality,

Lovers of horoscopes, tarot cards and stock-market seasonality, look away now. We're about to enter the worst month of the year for global shares. While seasonality is rightly criticized regarding stock moves, it's hard not to notice that when September is bad, it's wicked. In the nine down years since 2000, the average decline in the MSCI AC World Index has been a whopping 7%. Average gains for up years come in around 3%, but it's more like 2% if you take away the near double-digit jump in stocks in 2010. There are lots of reasons why stocks can fall next month -- more signs on the data front that global growth is slipping and an increasing realization of the threat a winter energy crisis could pose to the world economy. Bulls will point to the ongoing resilience of corporate earnings and the hope that central bankers can engineer a soft landing in their fight against inflation. Whatever happens, the dog days of summer are over and a lot of fund managers have just a little over three months left to make or break their year, given many shut up shop around the end of November. That should concentrate a few minds as a potentially volatile winter looms.

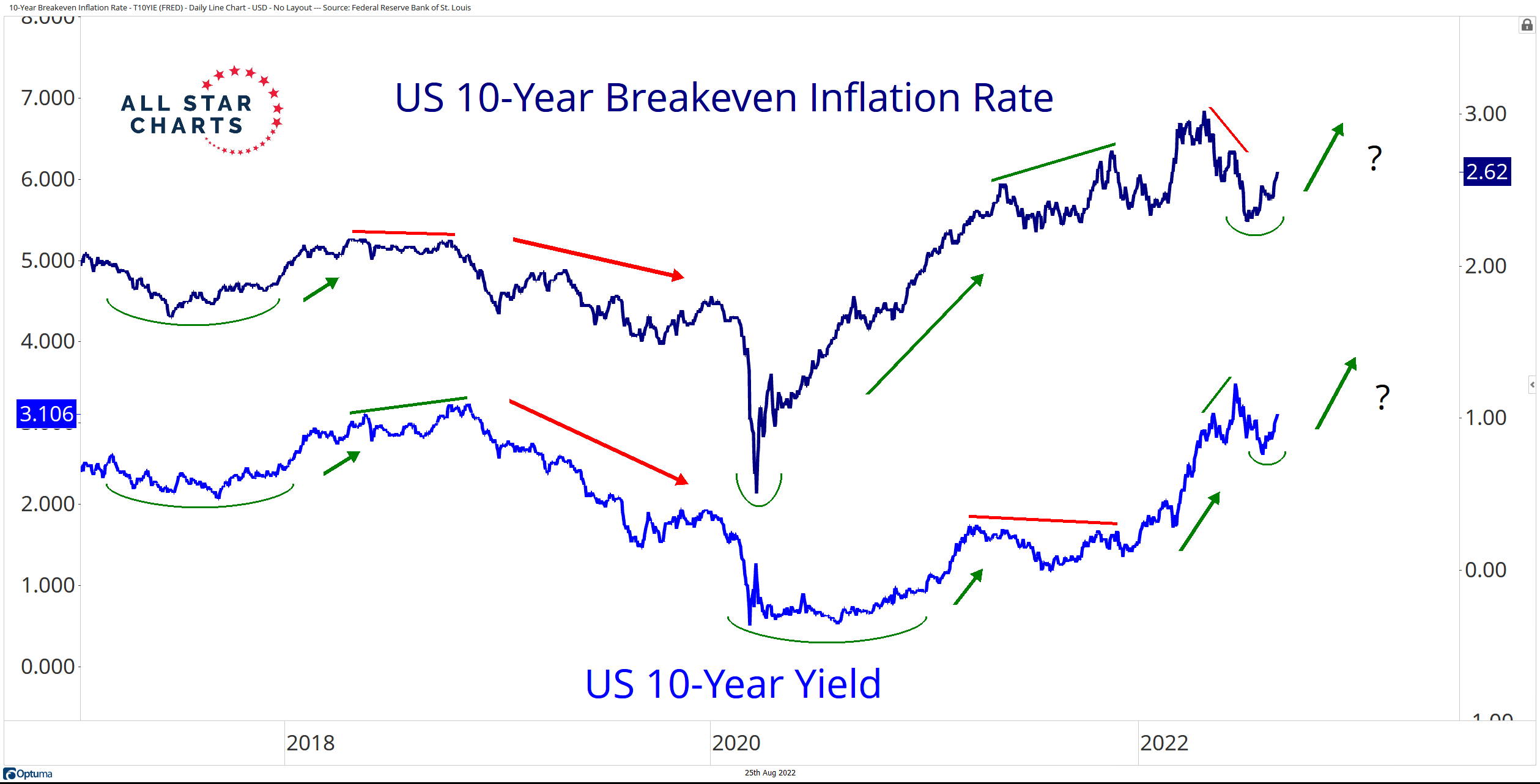

And here’s one from the (AllStar)CHARTS department

… When I think of the most critical trends to date, my mind immediately goes to interest rates. Rising rates and inflation have been the key drivers for two years now.

First, we have an overlay chart of the US 10-year breakeven inflation rate and the US 10-year yield:

As you would imagine, yields and inflation rates tend to follow one another over time. Rising rates and inflation go hand in hand. But oftentimes, these charts will highlight valuable divergences.

Most recently, the 10-year breakevens made a lower high after peaking in April as the US benchmark rate continued to catch higher. This turned out to be a poignant heads-up as both corrected lower into the summer.

Over the past few weeks, US yields and inflation rates have been rising together again. It appears the recent correction was nothing more than a countertrend move. With the primary uptrends assuring us they are still intact, we want to lean on the areas of the market that benefit most when rates are on the rise.

That’s right, cyclicals!

Finally, from some of the very best techAmentalists out there,

And as far as JPOW goes, 10a speech may or may not be definitive as far as the outlook goes and it’s going to be the rest of the team as well as all the papers released which will determine if we’ve got another 6mo of winter. Bloombergs Weekly FIX

The relief rallies that followed a softer-than-expected July US CPI print are a distant memory indeed. Federal Reserve officials and their global counterparts are clear they will do whatever it takes in the way of interest-rate hikes to tame inflation. As the clock ticks down to Fed Chair Jerome Powell’s opening speech this Friday, the Treasuries market has rarely been this fearful with the MOVE index of implied volatility remaining elevated.

Hedge funds set their latest big short in anticipation an ultra-hawkish Powell will send rate-hike bets soaring. The potential for central bank aggression was highlighted by news that the boards of the the St. Louis and Minneapolis Fed branches voted in July for a full percentage point increase in the discount rate — a measure that governs banks’ cost to borrow from the Fed and which was ultimately raised three-quarters of a point along with the US central bank’s main rate. With bonds, stocks and commodities moving in near lockstep, the potential for market shocks is high. That’s not even taking into account the dangers for assets as the Fed shrinks its bloated balance sheet, something Bridgewater reckons could send bonds and stocks down 25%.

The global outlook is similarly tense. Traders ramped up bets on European and UK tightening to stop the spike in energy costs from entrenching inflationary expectations. Adding to the European Central Bank’s burden, it looks like even a jumbo rate hike won’t get the euro back above parity. New Zealand’s Reserve Bank — a pioneer more than 30 years ago of inflation targeting — signaled a willingness to go above 4% with its cash rate. Around the globe, from Iceland to Israel , the hiking trails are aiming to make consumer spending fall back down the mountain.

Dangerous Trade

The strongest inflation in a generation continues to make bonds a dangerous trade. Shocking as it may seem against that backdrop, debt securities designed to protect against consumer-price gains are the worst performers this year. Linkers have been “stinkers” as Morgan Stanley notes — turns out commodities were a much better hedge against inflation.

Meanwhile a number of the world’s biggest bond investors are saying even the central-bank induced pain of steep hikes may not deliver a long-term win in the war against inflation. Instead, stagflation may be the watchword as slumping business activity worldwide feeds recession concerns. Guggenheim Partners Chief Investment Officer Scott Minerd is warning investors away from junk bonds too, and stocks, because of that dire economic outlook…