US equities and US Treasury bond prices tumbled this morning following a report by the new Fed whisperer himself - WSJ's Nick Timiraos - suggesting The Fed's inflation-fighting stance means 75bps is very much on the table for September's FOMC meeting. While careful not to leak any inside scoop, the mere fact that Timiraos is reporting this story - after his CPI/75bps move earlier in the year is enough to spook traders.

Federal Reserve Chairman Jerome Powell’s public pledge to reduce inflation even if it increases unemployment appears to have put the central bank on a path to raise interest rates by 0.75 percentage point rather than 0.50 point this month.

Fed officials have done little to push back against market expectations of a third consecutive 0.75-point rate rise in recent public statements and interviews ahead of their Sept. 20-21 policy meeting.

“We will keep at it until we are confident the job is done,” Powell said in Jackson Hole.

Mr. Powell’s speech showed he “very much did not want to leave the impression that the Fed would fall short on fighting inflation,” said Tim Duy, chief U.S. economist at research firm SGH Macro Advisors.

Specifically, Timiraos notes that Fed officials have been uncomfortable by how markets rallied - easing financial conditions - following their July 26-27 meeting, when Mr. Powell at a news conference signaled the central bank would at some point slow its rate rises. The rally risked undoing some of the Fed’s work to slow the economy.

And so today's story by a well-known Fed whisperer seems well-timed to front-run any attempted short-squeeze higher in stocks ahead of the Fed meeting.

The market's odds of a 75bps hike surged to 90%...

Which then sent stocks AND (shorter-dated)bonds LOWER … until, of course, the Feds Beige Book was released ….

That was then and this is now, and so, here is a snapshot OF USTs as of 7a:

… HEREis what another shop says be behind the “Low Conviction Conditions”

… WHILE YOU SLEPT Treasuries are modestly flatter and richer save the 2y point, a rather quiet overnight session seeing a jolt of bullish-tilted volumes after the RBA’s Lowe served up some dovish commentary (3y AGBs -16.4bps): “All else equal, the case for a slower pace of increase in interest rates becomes stronger as the level of the cash rate rises,” Lowe said in Sydney. In response, AUS STIRTs now price just quarter-point moves for the rest of 2022. Better Japan GDP data helped some local risk-asset performance (NKY +2.3%), but the risk-asset picture is mixed with SHCOMP -0.3%, DAX futures showing -0.5% and SPX futures showing -0.1% here at 6:30am. Energy space remains on the back-foot, Crude futures -0.2%, NG -0.3% and EU electricity prices lower by 4-6% depending on locale. In USTs, 2s10s is 2bps flatter (further inverted), 5s still outperforming on curve (2s5s10s -2.2bps). Flows overnight showed sociable better buying of short-end paper and light RM selling in long-end. Volumes are running ~95% across the term-structure (30d ave).

… and for some MORE of the news you can use » IGMs Press Picks for today (8 Sep) to help weed thru the noise (some of which can be found over here at Finviz).

As important a note as was MSs Mike Wilson — updated and lowered stock jockey fcast HERE just the other day, THIS from Goldilocks, hit inoboxes overnight, and will likely be a key to navigating the water cooler discussions ‘round Global Wall Street break rooms

We are raising our Fed forecast to include a 75bp rate hike in September (vs. 50bp previously) and a 50bp hike in November (vs. 25bp previously). We continue to expect a 25bp hike in December, which would take the funds rate to 3.75-4% by the end of 2022.

At the July FOMC meeting, Chair Powell laid out a case for slowing the pace of tightening. Since then, the data have on net come in roughly as expected or even a bit more supportive than expected of the case for slowing down. But Fed officials have sounded hawkish recently and have seemed to imply that progress toward taming inflation has not been as uniform or as rapid as they would like. And today, the Wall Street Journal reported that the FOMC “appears to be on a path to raise interest rates by another 0.75 percentage point this month,” a likely hint from the Fed leadership that a 75bp hike is coming at the September meeting. We therefore now think the FOMC will delay its plan to slow down.

The market is now pricing roughly a 75-50-25 path for the next three meetings, and our financial conditions index has tightened meaningfully on the hawkish shift in expectations. This should be enough to keep growth on a solidly below-potential path in the second half of 2022. How the drag from tighter financial conditions will net out with other key growth impulses in 2023 is more uncertain, and we could imagine the hiking cycle extending beyond this year.

And just as Goldilocks reducing it’s FED forecast, a large British operation is cutting it’s CHINA GROWTH f’cast,

We further reduce our 2022 and 2023 GDP forecasts to 2.6% and 4.5% respectively in view of a deeper and longer property contraction exacerbated by mortgage boycotts. Intensified COVID lockdowns ahead of the Party Congress, slowing external demand and power shortages add to the near-term headwinds.

HERE are a few thoughts from Rareview Macro — getting LONG DURATION as they suggest its, TIME TO FIGHT THE FED

… Based on the critical signals received recently in our proprietary framework, we believe the bond market is undeniably in Regime 4. That is, real yields are rising, and breakevens are falling.

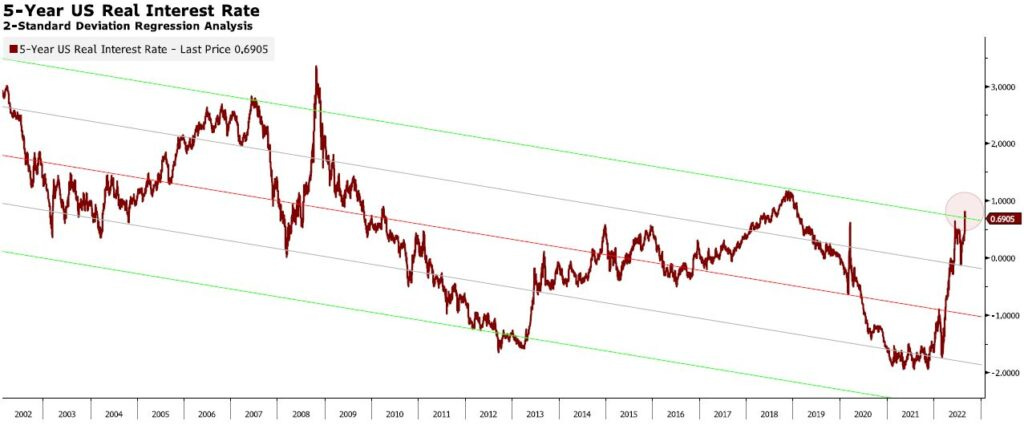

Last week, the 5-year US real interest rate closed at 0.72%. Note that the move higher in real yields last Friday surpassed the cycle high recorded in June (i.e., 0.70%). Notably, this occurred on a “monthly” closing basis, which we believe has more validity for a thematic portfolio than a “weekly” or “daily” close.

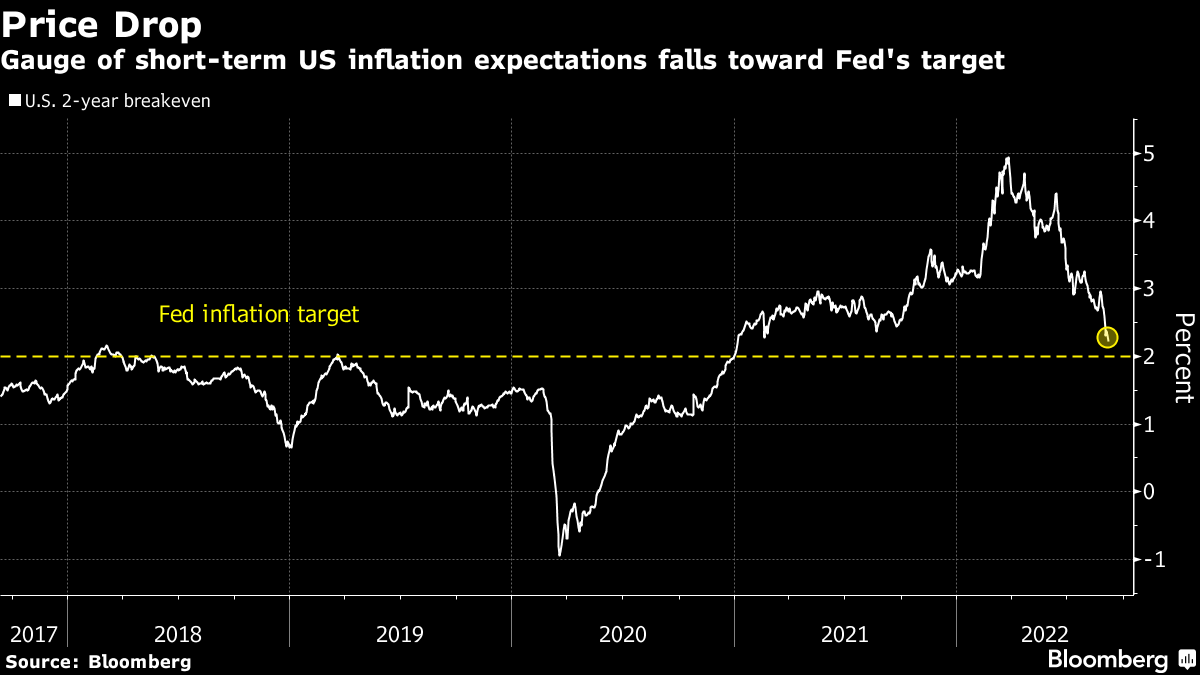

Concurrently, the 5-year US breakeven interest rate closed at 2.60%, below the January-February range. Inflation expectations are now near their lowest point of the interest rate hiking cycle.

Collectively, these charts show the Fed is tightening financial conditions and winning the battle against inflation expectations. That happens when you raise interest from 0.25% to 4.25% in six months. Note that the Fed has raised rates to 2.50% in the spot market and 4.25% in the futures market.

To further demonstrate the “blunt” force of the Fed’s hand, below is a daily chart of the 2-standard deviation regression of the 5-year US nominal interest rate minus the 5-year US breakeven interest rate dating back to 2002. As you can see, US real interest rates are now the driving force of financial conditions to the degree that they are trading outside the 2-standard deviation band.

… TIME TO FIGHT THE FED

Extend Duration

When the Fed reaches the point of “breaking the market” in Regime 4, counterintuitively, the most positive response is in long-duration assets. Why? Because once this stage is reached, the subsequent policy response is to cut interest rates within 6.5 months on average.

Therefore, as we reach the average point above the neutral rate this month or surpass the extreme overshoot of the neutral rate by December, the significant fixed income portfolio construction change is to extend the duration.

We have started that process in the products we manage…

Harkster.com offers a few notes/links thru to FURTHER READING ahead of the ECB

Powell may be causing restless nights for investors across the world, but he’s likely sleeping a little more soundly, at least if he is following signals from the bond market. There, expectations for future inflation look to be falling nicely in line with the Fed’s aims, seen most clearly in so-called breakevens, which track the difference between yields on inflation-protected securities and regular Treasuries.

Two-year breakevens have tumbled from just under 5% in March to 2.2% Wednesday, within shouting distance of the Fed's 2% target. Longer-dated equivalents are also retreating. Inflation is showing signs of decelerating, the central bank said in its latest Beige Book report, and the recent slump in the oil price will give officials some comfort. But what brings relief to policy makers will not necessarily do the same for investors. The Fed seems committed to keep interest rates higher for longer. And a continued slide in inflation expectations is just as likely to signal bets on a recession, which would keep the pressure on risk assets like stocks and credit.

With this chart in mind, a couple MORE visuals for those who, like me, are visual learners.

… 4. Zooming Out: The long-term bond Price [n.b. we’ve been switching back and forth between charts of price and yields, which as you should know - move inversely] is at a critical juncture here, very real risk of breaking down and a new wave of pain for bonds (equally though, this would be a convenient place to bottom).