while WE slept: geopolitical risk premia removed, supply on tap, USTs under pressure; 'Recent bear steepening appears election-related' (BNP); AI says more dovish FOMC stmts (DB)

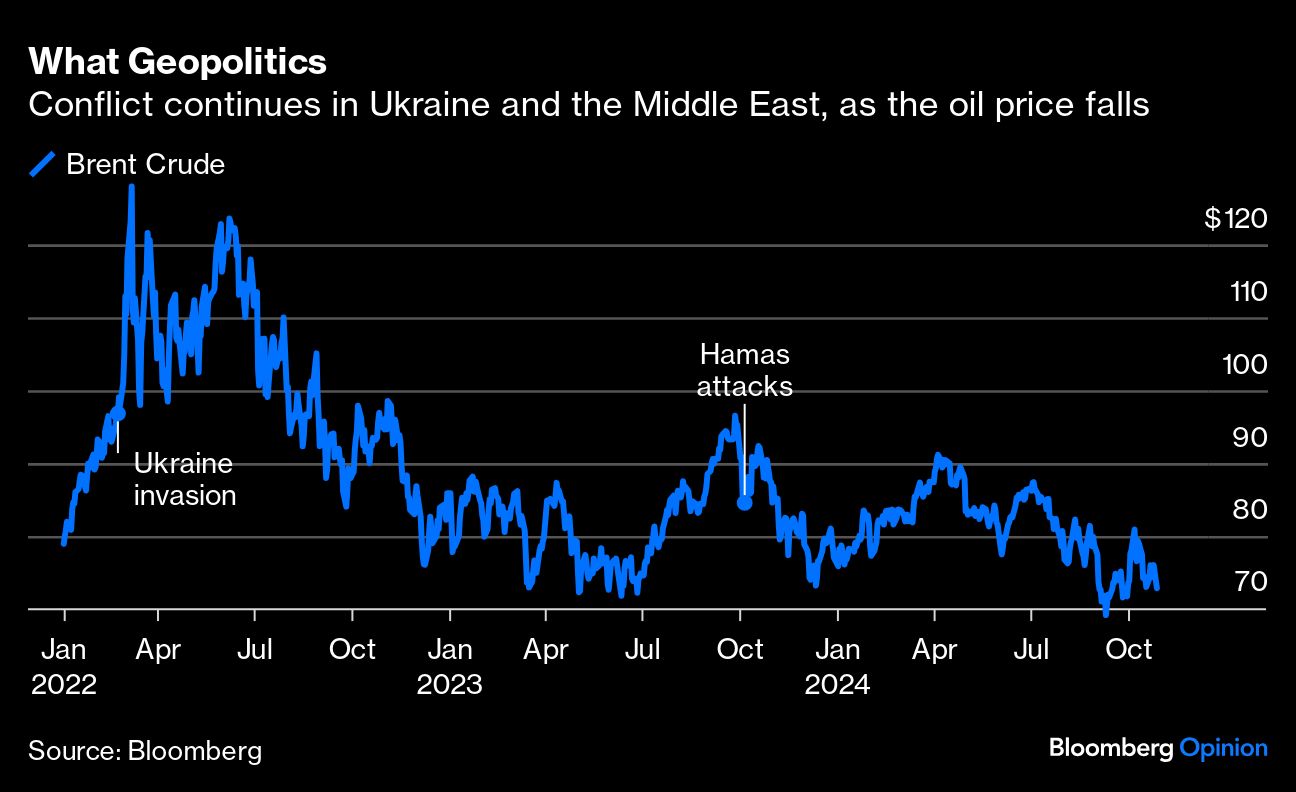

… and specifically on Israeli strikes being a relative ‘non-event’, oil, bonds, and gold gapped lower on the open as ‘risk’ (equity futures) edged higher as Israel targeting of Iranian military facilities on Saturday, avoided sensitive nuclear sites and so, was considered a non-escalatory attack.

Meanwhile, ALSO over the weekend …

CNBC: China’s industrial profits plunge at fastest pace since the pandemic

… added together, the aformentioned events of the weekend just past doesn’t seem to have helped the UST market which is staring at a double-header of liquidity events today (2s at 1130a and 5s at 1p) … a couple of now broken levels offered HERE.

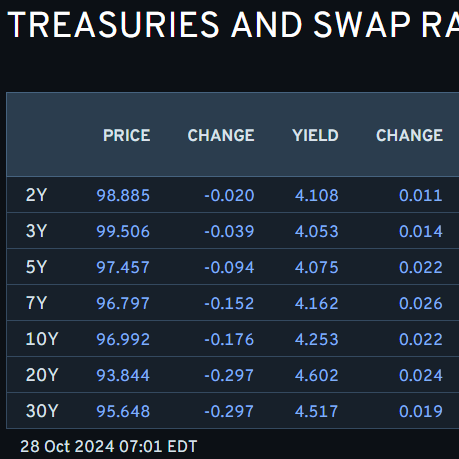

Interesting to note 5yy traded right to their 200dMA (4.118%) and are holding. For now.

5yy DAILY: will “X” mark the spot (ie a dipORtunity)?

… doesn’t seem too convincing of a bid, at least not just yet and so … as always, feel free to choose your own ending as the news was either GOOD (risk ON) or bad …

Meanwhile, back at the ranch … here is a snapshot OF USTs as of 701a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: Equities lifted and oil sinks as traders digest Israel’s limited strike on Iran … Bonds are pressured by the removal of geopolitical risk premia, but have lifted off lows in recent trade given the continued pressure in oil prices … USTs are pressured by the removal of geopolitical risk premia though also find themselves off lows as the pullback in energy prices begins to weigh on yields and exert upward pressure on benchmarks; though, still very much in the red. US docket is front-loaded on account of the Fed, with 2yr & 5yr supply today serving as another bearish factor and likely explaining the relative.USTs are currently trading around 110-25 and off the lows of 110-18+.

Reuters Morning Bid: Oil and yen drop on MidEast restraint, Japan indecision

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

… the French are gettin’ nervous and lookin’ at how to hedge DJT …

We believe US yields and the USD can continue to push higher into the US election.

In contrast, we like tactically owning Bunds, which we think have become unduly oversold…

…US yields and the USD have moved steadily higher in recent weeks on the back of both stronger US economic data and increasing market expectations that Donald Trump will win the US election (see Figure 1). We see scope for these moves to continue this week. Indeed, we think that macro markets are likely to react asymmetrically to upcoming US economic data releases, and that there is also scope for more portfolio hedging of Trump risk.

Why do we say this? Because we think only the last leg higher in yields has been election-related, suggesting that there remains a significant number of investors who still have not adjusted their portfolios to account for election risk. Specifically, we looked at the relationship between level and curve since the 10y UST yield bottomed on 16 September. The movement in 2s10s UST has had three regimes: bear steepening from 16 to 25 September, bear flattening until 7 October, and bear steepening since then. We would attribute the first regime to the Fed cutting by 50bp to attempt to stay ahead of the curve and preserve a soft landing; the second to improving economic data including the September NFP report and the third regime to rising Trump odds (Figure 2). In other words, we think that only the last 20bp rise in 10y UST yields appears election-related…

… a visual from DBs artificial intel department and a recap of week ahead …

DBDaily - US payrolls this week; Can Europe skirt '24 recession?

…Fedwatching with AI. Matt Luzzetti applies DB's AI tool to Chair Powell's prepared remarks at the past four years of FOMC meetings to create an objective Hawk-Dove scale. The results align with Matt's subjective assessment over the period, but there is some sensitivity to two potential sources of variation – across prompts and time – though less than Matt anticipated ex ante. From this start, there is more to do here: ideally, the tool could provide similarly insightful scores of alternative and less structured forms of Fed communication across more nuanced periods …

…For markets, the positive mood that dominated so far this autumn saw a mini-scare last week, as the S&P 500 fell for the first time in six weeks, while the bond sell-off continued apace. There’ll be plenty to test the market nerves with this week'sbumper set of data releases, including US payrolls on Friday, and earnings reports, with five of the Magnificent 7 reporting. Meanwhile, the tight US election campaign will enter its final stretch.

One market fear that has eased over the weekend is escalation risks in the Middle East. This comes as overnight into Saturday Israel carried out retaliatory strikes against Iran, but with these targeting military facilities and avoiding oil or nuclear installations. The targeted scope of the attack and the absence of an immediate retaliation signal have seen markets price out some of the geopolitical risk premium. Brent crude is down around -4.5% lower to below $73/bbl in Asia trading, reversing last week’s 4% rise. Gold is down -0.60% from Friday’s record high, while US equity futures are posting decent gains with those on S&P 500 and NASDAQ +0.50% and +0.65% higher, respectively.

Meanwhile, Treasuries are extending their recent decline. 10yr yields are +3.2bps higher to 4.27% as I type, their highest level since July, having now risen by 65bps from their September lows. This rise has come amid both rising term premia, partly driven by concerns about US fiscal deficits, and growing skepticism that the Fed will deliver rapid rate cuts given solid US data. Indeed, Fed funds futures for end-25 are up to 3.53% this morning, having priced out three 25bps cuts over the past six weeks.

With the Fed now in the blackout period ahead of next Thursday’s meeting, the data will be doing the talking this week, with the marquee release being the October payrolls report on Friday. Our US economists foresee a sizeable slowing in headline (+100k forecast vs. 254k previously) and private (+75k vs. 223k) payrolls. However, this envisages a nearly -70k drag due to striking workers (mostly Boeing) and the weather impact of Hurricane Milton. The weather effect may also push up average hourly earnings (+0.6% vs. +0.4%). DB expects unemployment to tick up a tenth to 4.2% amid rising labour force participation, but the risk is that it remains at 4.1%. Given the likely noise in the payrolls, the market may pay extra attention to Tuesday’s JOLTS report for September. Given the strong September payrolls, the hiring rate may pick up from the historically low 3.3% in August. The last JOLTS print also saw the quits rate, one of the best leading indicators of wage growth, fall to 2.1%, its weakest since 2015 if one excludes the first few months of Covid. Other labour market data will include the Q3 Employment Cost Index reading (DBe: +0.9% vs. +0.9%), which is the Fed's preferred measure of wage growth…

… ‘bout the oncoming election where ZH already detailed and offers somewhat more color … the source …

MS: Sunday Start | What's Next in Global Macro: Squaring the Circle

The outcome of the US elections, now just over a week away, has been at the center of every discussion we have had in the last several days. While the latest opinion polls show that the presidential race has tightened and is neck-and-neck in key swing states with poll numbers within the margin of error, in recent weeks some prediction markets have shifted meaningfully toward the Republicans in the contests for the presidency and control of Congress.

Capital markets have broadly aligned with the prediction markets. As reflected in the Republican (MSZZREP) and Democratic (MSZZDEM) baskets we track, stocks exposed to Republican win outcomes have risen.The baskets listed above were originated by Sales & Trading and are not products of Morgan Stanley Research. No investment recommendation is made with respect to any of the baskets referenced herein. Investors should conduct their own due diligence in making investment decisions with respect to those baskets….

…In the bond markets, while US Treasury yields have risen notably, factors beyond the prediction markets’ implied election outcomes have contributed to Treasury market action. Strong incoming data on payrolls and retail sales have certainly played a key role, especially in the first two weeks of the month. That said, more recent moves likely have been driven by the prediction markets. Many investors see the "Republican sweep" outcome as most bearish for US Treasuries, based on the 2016 election, when 2-year Treasury yields rose 50bp and 10-year yields widened 80bp over the month following a Republican sweep.

Matt Hornbach, our head of global macro strategy, points to meaningful differences between the Fed’s monetary policy today and the pre-election period in 2016, suggesting that any rise in Treasury yields would be more contained this time. In contrast to the current market expectation of about 135bp in rate cuts over the next 12 months, markets were pricing about 30bp in hikes back then. Furthermore, in the year after the 2016 election, expectations for the target fed funds rate rose by nearly 125bp. A similar rise in expectations for Fed policy would require market participants to expect the Fed to stop cutting rates immediately and refrain from further cuts through 2025, seemingly a remote possibility even under a "Republican sweep" election scenario.

… adding the middle east TO all of the coming days ‘event risks’ …

UBS: Global risk radar: Global Risk Radar: Israel responds

Israel carried out strikes against military installations in Iran this weekend, in response to Iran’s missile attack on Israel in early October. Based on the current state of affairs, Israel seems to have chosen a path that markets will likely interpret as a subdued course of action.

In our base case, we expect global markets to be occasionally affected by the escalation in the Middle East but do not assume the conflict will expand to an all-out war between Israel and Iran, including their respective allies. But the likelihood for such a risk case remains high, bearing the possibility of direct US involvement and disruptions to energy supply.

• We highlight the importance of diversified portfolios to limit the exposure to individual risks, but recommend staying invested given the overall supportive macroeconomic backdrop elsewhere. Oil and gold can help account for geopolitical risks.

…Israel’s military strikes against Iran over the weekend focused on military targets. This has allowed oil prices to drop (as oil capacity was unaffected). Iranian leader Khamenei has seemingly signaled a measured response, supporting hopes that the situation will not escalate.

… AND for those looking for some FED related illumination …

Wells Fargo: November Flashlight for the FOMC Blackout Period

Summary

The FOMC started its nascent easing cycle with a bang, opting to reduce the fed funds target range by 50 bps to 4.75%-5.00% at its last meeting on September 18. But further policy easing seems set to proceed at a slower pace. We look for the FOMC to reduce the fed funds rate by 25 bps at its upcoming meeting on November 7.

Since the Committee last met, U.S. economic activity has generally surprised to the upside and suggested ongoing resilience. Concerns about rapid softening in the labor market were allayed by the September jobs report showing a much stronger pace of hiring the past three months and the unemployment rate falling to a four-month low. Solid retail sales and upward revisions to income suggest consumer spending remains on a firm footing. Consumer price inflation also came in a bit stronger than expected in September.

The FOMC's September dot plot, the recent string of stronger-than-expected data and policymakers' comments give no reason to expect another 50 bps cut at the Committee's upcoming meeting. We expect the FOMC will continue to reduce its policy rate with a smaller 25 bps cut as the real fed funds rate remains elevated relative to the past expansion and Committee members' estimates of "neutral." Therefore, there seems to remain scope to "recalibrate" policy further to avoid the labor market cooling beyond the point of comfort without rekindling inflation.

Yet given the recent run of data along with some officials' prior reluctance to cut much further, if at all, this year, we would not be surprised to see another dissent at the November 7 meeting, and view the risks to our expectation for a 25 bps cut skewed toward the FOMC leaving rates unchanged rather than opting for another 50 bps cut.

Recent signs of funding pressures lead us to expect the FOMC will discuss the current pace of quantitative tightening (QT) at its November meeting. The secured overnight financing rate (SOFR) traded above the top end of the fed funds target range at the end of Q3, suggesting bank liquidity has become less ample. While we do not anticipate any changes to QT at this meeting, the recent stress will likely lead to an in-depth discussion about the timeline for the cessation of balance sheet runoff. We currently expect QT to cease at the end of Q1-2025.

As the leaves start to change color, retailers move out the back-to-school merchandise as they deck the aisles with everything from 12-foot evergreens to human-size nutcrackers earlier and earlier each year. While our official tally of holiday sales does not kick off until November 1, anyone who has been in a home improvement store recently is reminded the holidays are fast approaching. In a year when sustained consumer spending propelled growth and helped the economy skirt recession, we're actually calling for a fairly modest holiday sales season to close out 2024.

Back by popular demand, some themes made the holiday menu again this year—holiday shopping continues to get pulled forward with less happening during the traditional period spanning from Black Friday to Christmas, still-high prices and less support propping up purchasing power means continued competition for consumer dollars, and online retailers continue to be the king of the dance when it comes to commanding the most holiday-sales dollars.

Yet, there is also a scent of, dare-we-say, “normal” in the air this year. Consumers' purchasing power has once again become dependent on income growth, as unique pandemic-era spending sources have faded. Despite consumer momentum helping sustain the economic expansion this year, through September the retailers included in our holiday sales metric have seen the slowest year-to-date sales growth in seven years. Momentum isn't a huge lift factor this year, as it has been in the years since the pandemic.

Both traditional brick-and-mortar and online retailers are growing flexible in catering to the early and late shopper, but with competition for consumers' dollars as fierce as ever, households are on the hunt for value this year and will likely spend less on traditional retail than in years past.

All told, we forecast holiday sales to rise 'just' 3.3% in November and December compared to the same period last year. If realized, that means we expect the 2024 holiday sales season to not only be weaker than last year's sales season, but also less robust than the long-run average of 4.3%.

While we're expecting a more modest end to the year for retailers, the fact is consumers are spending more throughout the year instead of waiting for Christmas. On that basis a soft finish to retail spending in 2024 need not set off major concerns about the sustainability of spending in 2025.

…We define holiday sales as total retail spending excluding sales at auto & parts dealers, gasoline stations and bars & restaurants that occurs in the months of November and December. By that measure, we forecast holiday sales to rise 3.3% compared to the same period last year. That would be weaker than last year's sales season and also well below the long-run average of 4.3% annual growth (Figure 1). Despite it being a year characterized by solid consumer spending that helped the economy sidestep a recession, we look for a fairly modest holiday sales season.

…. finally, a look at the economic week ahead (incl a graphic of econ surprises and 10yy…)

Yardeni: The Economic Week Ahead: October 28 - Nov 1

The week ahead is jampacked with key indicators for the labor market, economic growth, and inflation, as well as more Q3 S&P 500 earnings. The first estimate of Q3 GDP will be followed by the September PCED inflation rate and October payroll employment. We're expecting continued strong growth and disinflation, though we anticipate that employment was muddled by one-time factors and that some components of the Fed's preferred PCED inflation rate remained sticky. Additional strong economic data, stickier inflation, and more-than-expected Treasury financing needs could raise the 10-year Treasury yield into the 4.25% to 4.50% range (chart). That could unsettle the stock market.

… And from Global Wall Street inbox TO the WWW …

Starting off is a commentary ‘bout all that ‘cash on the sidelines …

Apollo: A Lot of Money on the Sidelines Coming Out

US households are savvy. When the Fed funds rates was zero, the number of households with a TreasuryDirect account, where you can buy and sell US government bonds, was about 700,000, see chart below. But once the Fed started raising interest rates, the number of households with a TreasuryDirect account increased to 4 million. Even before the Fed started cutting, the number of accounts started declining.

Combined with the $6.5 trillion currently in money market funds, the key question is what households will do with their Treasury holdings and money market holdings as the Fed continues to cut interest rates.

The most likely outcome is a steeper curve whereby households will withdraw money from the front end of the curve and put it into credit and other higher-yielding fixed income assets.

… and while Japan surprise was a big deal, so too was the lack of news from middle east …

Bloomberg: Japan's stability gets a monster October Surprise Weakened leader Ishiba may struggle to form a majority outside the LDP’s usual comfort zone.

… Oil Is Calm Another big event since markets last traded: Israel’s missile attacks on Iran. It wasn’t unexpected, but the reaction of the oil market in Asian trading has been a little counterintuitive. Crude prices dropped more than 5%. Israel opted not to attack the oil industry directly, a possibility once widely canvassed, and Iran swiftly confirmed that its production was unaffected. That continued a trend. This is how the price of Brent crude has moved in the last two years:

Despite initial appearances, the short-term move downward makes sense. Not only was oil production unaffected, but both sides seem to lack appetite for another round of escalation. Peter Tchir of Academy Securities pointed to rival claims by Israel, who hope to have minimized Iran’s ability to deal with any future attacks, and Iran, which says the attack had little impact:

At this stage, the outcome is likely not much different regardless of which side is telling the truth (or if the truth is somewhere in between), as neither side seems intent on escalating further. Yes, there have been some comments out of Iran calling for preparations for war, but does either side really want to escalate at the moment? Look for this to revert back to proxies and for oil prices to decline on the back of this controlled retaliation that is unlikely to provoke a direct response from Iran.

If the response to the latest round of hostilities makes sense, however, the broader message from the oil market seems totally discordant with many other current assumptions. Hard landing for the US economy is now thought highly unlikely, inflation breakevens have started to edge up again, and China has launched an attempted stimulus. A Trump victory would mean more tax cuts in the US, which should be expansionary. And yet the oil market is behaving as though demand is doomed. Eric Robertsenof Standard Chartered Plc puts it as follows:

Oil is trading as if downside economic risks are all that matter and geopolitical risk is non-existent... Even with the escalation of military conflict in the Middle East, Brent oil has struggled to sustain prices above $80/barrel since Aug. 1. Furthermore, the oil market appears to be ignoring both recent signs of better-than-feared US economic activity and China’s significant stimulus announcements. In other words, oil is trading as if the macroeconomic backdrop has deteriorated over the last three months, while we would argue that the backdrop is marginally better than feared.

Early Monday’s sharp fall in response to the news from Iran suggests that there was indeed some political risk written into the oil price, and that it has now been removed. Traders’ perception of the economy was even weaker than it appeared. That ties in to the unavoidable topic of the moment.

… AND on the tsunami of USTs coming …

WolfST: Treasury Yield Curve Un-Inversion Hits Milestone on Inflation Fears, Tsunami of Supply, QT. Mortgage Rates Near 7%

The 10-year yield surged by 60 basis points in five weeks but may run out of steam by about right now.

… and given the event-risk in the week just ahead, from the best in the strategy biz is a LINKthru TO this calendar …