Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

Lacy Hunt, HIMCo, remains bullish and we’ve got some shorter-term risks over the next couple weeks but I dont think this matters to him … I noted his latest quarterly Friday before the day got going and the day came and went SO fast …

First UP lets deal with a couple / few things items from the week just passed (in other words, a couple snarky ZH links which contain visuals and info graphics helping tell the tale of markets — INCLUDING rates — which you may / may not have already stumbled upon) …

ZH: US Durable Goods Orders Revised Lower... Again! ZH: Dems Lose Faith As UMich Sentiment Expectations Dip In October

… and culminating in a recap worth a look …

ZH: Stocks Break Six-Week Win-Streak, Gold Hits Record High As 'Trump Trade' Takes Off

… NOW in the week ahead, there will be a double header of UST supply Monday with $69bb 2yy …

2yy DAILY: perhaps a bid is close at hand …

… at / near 4.12 which appears to have been resistance back at the turn of the year and now, as we revisit it from the other side, with momentum now overSOLD … but then …

5yy DAILY: similar setup where ‘support’ appears to be close by …

… again approaching support as momentum quite overSOLD is good, in as far as stability goes but then there’s all the macro in the coming couple weeks …

… Ok I’ll move on AND right TO the reason many / most are here … some WEEKLY NARRATIVES — SOME of THE VIEWS you might be able to use THIS WEEKEND, here a few things which stood out to ME from the inbox …

First up from THE bank of the land (clearly DODGERS fans … ugh) …

…US: The pop in rates in October was mostly about a Fed pivot and good data. Election sweeps are bear steepening risk; we like buying dips especially on mixed govt.

…US macro: good data + Fed pivot = last +20bp

…Duration dipper: we continue to encourage clients to buy the rate dip. We have argued for trading US duration tactically, believing near-term 10Y range will be 3.5-4.25%. We think it makes sense to tactically add duration exposure towards upper end of the range; our preferred duration point remains the belly (5Y). Our dip buying approach is based on the view that the Fed will not pivot again to hikes but will remain in cautious cutting mode for much of 2025, looking for opportunities to deliver a policy stance more aligned with the lower level of inflation risk …

…Bottom line: Early November with the US election, payrolls, Fed and refunding presents risk for long duration positions, particularly at the back end of the curve. Sweep outcomes likely to see market trade higher back-end yields on supply & fiscal concerns. We prefer to express this risk through short 30y spreads. Medium term, think that an election-related selloff would present a dip buying opportunity and real rates could be more compelling if inflation becomes an issue with higher tariff policies. We believe that the market will struggle to price less than 3 Fed cuts for the remaining cycle even in big selloff scenarios as inflation risk is generally lower and the Fed would still be restrictive at 4%.

BAML: US Economic Weekly Spotlight on trade policy

…Data preview: Distorted employment We forecast nonfarm payrolls rose by 100k in October. Although this is below consensus, we’d still view it as a solid print, since we estimate that Hurricane Milton and the Boeing strike lowered payrolls by about 50k. Note that Governor Waller pointed to a larger drag of ~100k in recent comments. The hurricane also likely lowered hours worked and, as a result, raised average hourly earnings growth. Meanwhile, the unemployment rate should move back up to 4.2%, partly due in part to hurricane distortions.

… More than a few NFP pre-caps and so, this one from France …

We look for a downshift in payroll growth to 120k in October and a steady unemployment rate (released 1 November).

We expect Fed officials to look through the weak number given negative storm and strike effects, which we estimate at 60-70k.

If the report proves surprisingly strong on all key dimensions though, we expect it would add to murmurs of a Fed pause as early as December. Even so, a near-term pivot could prove difficult given inflation progress and the consensus Fed view that policy rates are still restrictive.

Amid rising public debt and ongoing budget processes, the IMF calls for a fiscal pivot, which could have monetary implications. Beyond the fiscal, a potential Trump victory with an 'R-sweep' could be most consequential for the global economy. Next week, the focus is on US employment, European GDP and inflation, and the BoJ.

US Outlook Hurricane clouds to remain after payrolls Fedspeak during the lead-up to the blackout did not push back against expectations of a 25bp November cut, consistent with our baseline. Although next week's October employment data will likely give an initial sense of underlying labor market activity, the Fed is unlikely to take strong signals until November's release.

Fedspeak during the lead-up to the blackout period provided little cause to believe that the FOMC will pause in November. That said, even though our baseline continues to pencil in a December cut, the outcome for this meeting remains data-dependent, in our view.

Incoming data remain consistent with solid growth momentum. We expect estimates in next week's advance estimates to place Q3 GDP growth at 3.0% q/q saar, the same as the Q2 pace, reflecting a robust 3.5% q/q saar increase in consumer spending. We expect December's estimates to show acceleration of the core PCE prices to 0.26% m/m (2.2% y/y).

Even with data showing that the post-hurricane spike in initial claims was short-lived, we expect the Fed's read on underlying activity to be clouded well past next week's report. Taken alongside the Boeing strike, our best judgment is that payrolls will slow to 125k and that the unemployment rate will jump to 4.2%, with additional fallout on the workweek and hourly earnings.

… and from best in (statEgery)biz, now long 10s on dip …

…On the data front, Tuesday’s JOLTS release will be closely watched for any further confirmation of the underlying strength of the jobs market seen via the September payrolls release. The consensus is for a modest downtick in Job Openings to 7.9 million from 8.04 million in August. We’ll be more focused on the Quits Rate, which recently printed at just 1.9% – below the bottom of the pre-pandemic range and a troubling sign for sentiment in the labor market. Investors will also get their first look at Q3 real GDP, which is anticipated to come in at an impressive 3.0%. Embedded within the quarterly annualized core-PCE figures will be the September move of the Fed’s favored inflation measure, although the monthly breakdown won’t be on offer until Thursday – the current forecast is for an uptick to +0.3% which would nonetheless be associated with a downtick in the yearly pace to 2.6%.

The marquee data release comes in the form of Friday’s payrolls figures for the month of October. In light of how influential the September data (NFP, CPI, Retail Sales) proved to be for the no-landing/Goldilocks narrative, we’re eager to see whether October reinforces or challenges the optimism. We’re wary of the potentially distortive impact from the hurricanes on the BLS series and suspect that the ‘not at work due to weather’ table within the report will once again be of particular interest as the market seeks clarity on the trajectory of the labor market. If nothing else, the setup for the week ahead points toward crosscurrents as the Presidential election reaches the final stretch…

In the attached Weekly we preview Wednesday’s release of advance third-quarter GDP data. We also provide some thoughts on the rise in yields that has followed the Fed’s 50-basis-point rate cut on September 18. We have added summary of upcoming macro events next week to the final page of this piece.

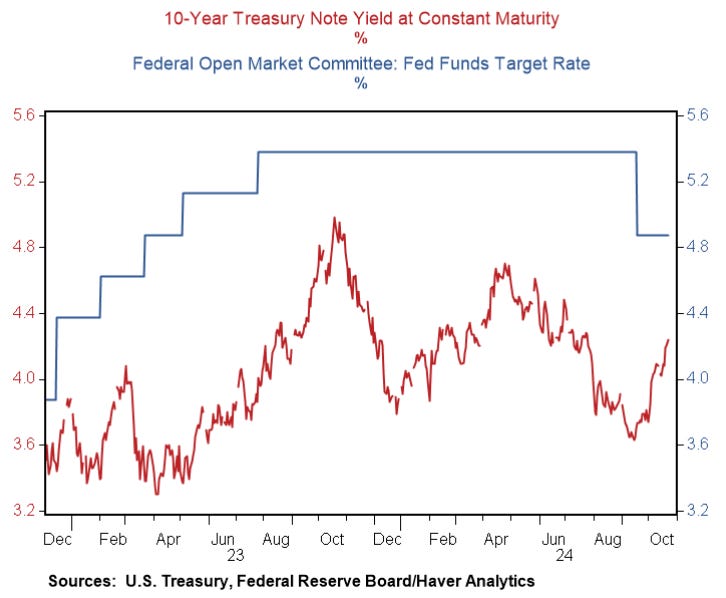

…The Fed and the Bond Market In 1774, William Cowper wrote his poem “God moves in a mysterious way,” which has become a fairly commonplace proverb, but substitute monetary policy for the word God and you have a basic thesis for the operation of monetary policy. There are numerous channels through which monetary policy can have an impact and most of them work, at least initially, through financial markets. The most obvious channel is the interest-rate channel—cut interest rates and interest-sensitive spending could be boosted as investment spending is increased. There is also the exchange-rate channel, which is particularly important for open economies, the wealth-effect channel, the liquidity- or quantity-channel, and the expectations channel, to name but a few. For a small open economy, the exchange-rate channel might be the dominant one and might actually tightly constrain monetary policy (think, for example, Switzerland, or the Netherlands before the creation of the Euro). A considerable body of academic theory since the Rational Expectations revolution focuses on the expectations channel. Monetarists in the tradition of Milton Friedman argued for the importance of the quantity of money. The truth of the matter is that we do not know exactly how monetary policy works but we do know that it can be extremely powerful.

On the interest-rate channel, in his 1936 General Theory, Keynes wrote “the rate of investment will be pushed to the point on the investment demand-schedule where the marginal efficiency of capital in general is equal to the market rate of interest.” However, he discussed circumstances in which the channel was short-circuited by the failure of market interest rates to decline noting “The short-term rate of interest is easily controlled by the monetary authority, both because it is not difficult to produce a conviction that its policy will not greatly change in the very near future, and also because the possible loss is small compared with the running yield…But the long-term rate may be more recalcitrant when once it has fallen to a level which, on the basis of past experience and present expectations of future monetary policy, it is considered ‘unsafe’ by representative opinion.” So what has happened to longterm interest rates since the Fed cut the funds rate by 50 basis points on September 18? On September 17, the 10-year Treasury yield ended the day at 3.65% but now stands at 4.21%, so the representative long-term interest rate has risen 56 basis points even as the Fed has lowered the short-term interest rate by 50 basis points. The long-term interest rate paid by companies has also risen with the Moody’s Baa yield rising from 5.33% to 5.78% over the same period—an increase of 45 basis points. Judged by market interest rates, we have the situation described by Keynes, and it raises the question: is the current level of short-term interest rates in some sense unsafe?

Ever since the introduction of TIPS in January 1997, bond investors have been able to largely insulate themselves from the ravages of inflation (we say largely because for taxable investors, the inflation compensation component of the yield is taxable) and bond traders have been able to express their view on what is driving yields (inflation or real rates). On September 17, the 10-year TIP yielded 1.54% but this has risen to 1.90%, which is an increase of 36 basis points. Over the same period, the 10-year inflation breakeven has risen from 2.11% to 2.29%, which is an increase of 18 basis points. The rise in yields, therefore, has been divided between higher real yields and higher inflation breakevens in the ratio of 2:1. We argued at the end of 2021, when the real 10-year yield stood at -1.1% that real yields would be the primary driver of nominal yields as the Fed renormalizes monetary policy and, as the chart below shows, this remains the case…

…Part of the message in the higher inflation breakevens, and perhaps also in the rise in the price of gold to new record highs after the 50-basis-point rate cut, may be that markets are pricing in some risk of materially higher inflation if the Fed cuts interest rates too aggressively.

uch a rise in interest rates after the first cut in the fed funds rate is not without precedent. The Fed cut the funds rate by 25 basis points on July 6, 1995, having doubled the funds rate from 3% to 6% from February 1994 to February 1995. In the 28 trading days that followed that rate cut, 10-year yields rose 52 basis points from 6.05% to 6.57%, and the economy did not sink into recession following a far more aggressive monetary tightening episode than most had expected. Greenspan & Co had only to lower the fed funds rate by 75 basis points from July 1995 to January 1996 to pull off the clearest example of a soft landing in the modern history of the Fed. What is clear is the market appears at odds with the Fed’s longer-term policy indications even as futures price in rate cuts to below 3½% by the end of 2025 and we see this as further support for our view that yields going forward are likely to be about 4%.

… a note on positioning and flows …

DB: Investor Positioning and Flows - The Cross Asset Ramp Up In Volatility Premiums

We noted last week that implied volatility premiums have ramped up across asset classes in the face of a plethora of catalysts (growth concerns, earnings, geopolitical risks, elections, Fed uncertainty) (Taking Stock Of The Five Catalysts, Oct 18 2024). In equities, the VIX is about 10 points above realized vol, putting the vol premium more than 1sd above average or in the 91st percentile since 2010. The implied vol premium is also similarly elevated in FX. The vol premium in oil has risen but modestly so. The real standout is in bonds, where the implied vol premium is running a massive 2.5sd above average and near the highest on record (99th percentile), notable even relative to the heightened vol of the last 2 1/2 years.

What happens if implied vol declines from these elevated levels, especially post the US elections?

…In bonds there is no clear directional pattern historically. In the current context, bond yields have been going up along with vol and the correlation has been largely positive for the last 4 years. While better-than-expected growth data has been a driver recently, the US election is also playing a role with fears centered around rising fiscal deficits. However, as our rates strategists have pointed out, in their reading a Trump sweep without enacting tariffs is the only election outcome that would lead bond term premia to increase from current levels while the other scenarios would see them fall (Fixed Income Chart Of The Day: Term premia under election scenarios, Oct 22 2024). Will an unwinding of elevated vol post elections then see bond yields decline regardless of the outcome?

… for some longer-term perspective and dart throwing …

JPM: Introducing the 29th edition of Long-Term Capital Market Assumptions

…Grounding ourselves in the solid fundamentals

Despite lower return assumptions, the global economy’s resilience has surprised to the upside. Here are some of the positives:

The “misery index,” which is the sum of YoY CPI (2.4%) and the unemployment rate (4.1%), stands at 6.5%—that’s lower than it’s been 85% of the time in the last 50 years.

The “misery index” is lower than it’s been 85% of the time in the last 50 years

Inflation seems like it was a cyclical event driven by the pandemic. The LTCMAs’ marked down U.S. long-term inflation from 2.5% to 2.4%.

Global central banks are easing policy, which should support growth and valuations; G7 nominal growth expectations have risen for the fifth year in a row.

Lower inflation and stronger economic growth create a favorable investing backdrop that lends itself to opportunities across asset classes.

… what else can one say when the days ahead are so important … stay NEUTRAL on duration and … well …

MS: 11 Days and 1 Payrolls To Go | Global Macro Strategist

The US general election takes place in 11 days. Before then, investors have to deal with a noisy nonfarm payroll report. We remain neutral on US duration and curve shape as well as the US dollar. We don't think the recent rise in US yields reflects much election risk, but rather reflects the data…

…Interest Rate Strategy United States 10y Treasury yields rose about 50bp over the past month, and the market-implied trough Fed policy rate rose about 60bp. We investigated how much US economic data surprises and changes in the price of a Trump victory in Polymarket explain these moves (and moves in other US rates). US economic data surprises explain the largest portion of changes in yields over the past month.

What does our analysis mean for the US rates markets around the US election? Heading into the election, rates markets should move most on US economic data surprises – unless prediction markets move in a way more clearly tied to race fundamentals instead of market technicals (like what occurred at Polymarket, reportedly).

We think the US rates markets are probably reflecting outcome probabilities closer to what swing-state polling suggests, i.e., a ~50% probability of a Trump or Harris presidency. Note: A Trump presidency on Polymarket priced near 50% before the recent swings in prediction markets, which according to media reports may have been influenced more by technicals. After investors digest the outcome of the election, they should go back to watching the US economic data.

The coming week should see relative calm before the pre-election action-packed week – which will include a nonfarm payroll print, the US presidential election, and an FOMC meeting. We suggest clients use this opportunity to position for relative value and mean reversion, while not taking directional risk. Specifically, we like paying fixed in the belly of the 7s10s30s PCA neutral risk-weighted butterfly.

… AND a few words on QT …

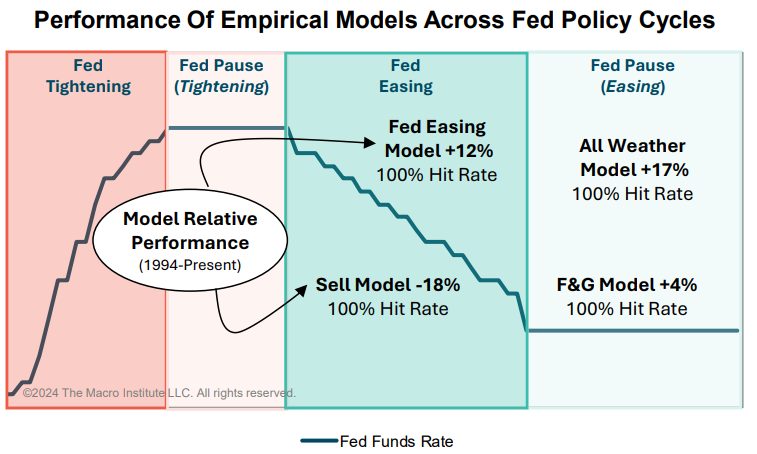

Trahan Macro: The Most Helpful Empirical Tools For The Fed Easing Cycle

This is perhaps one of the most important statistics for equity investors right now: the average Fed easing cycle over the last 50 years has lasted about 18 months! In that context, if we are facing an “average” episode then we are still in the first inning of this thing. This is where the opportunity lies, in our opinion, as there are many repeatable patterns in past Fed easing cycles. At the end of the day, humans make investment decisions and history teaches us that human behavior does not change much from one easing cycle to the next. This helps explain why the “Fed Easing Portfolio” has worked, but it goes well beyond a few factors and sectors.

It’s not a coincidence that the Healthcare and Consumer Staples sectors have outperformed in each of the last four Fed easing cycles. Now, this doesn’t mean that everyone should buy those ETFs blindly, but there is a message from the markets embedded in this statistic – Defensives tend to be in favor as the Fed eases policy. This should not be surprising since the Fed is typically dovish when the economy is losing steam, and that happens to be when Defensives are in favor.

The same dynamic can be found at the factor level as we have shown countless times this year with the Fed easing portfolio. It is simply an amalgamation of five factors that have generated alpha in past easing cycles and that combination happens to be working in recent months as well. In this week’s report, we take this analogy further and try to home in on which empirical models tend to work best as the Fed eases policy. There are a few surprises and plenty of great insights for today’s backdrop…

Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW

Apollo: Visits to the Statue of Liberty Continue at 2023 Levels, No Signs of a Slowdown

The US consumer is not slowing down. Visits to the Statue of Liberty continue at 2023 levels. Consumer spending remains healthy with air travel strong, hotel spending robust, and Broadway show attendance solid. Retail sales for September were strong at 1.7% year-over-year, and continue to be supported by strength in weekly same-store retail sales data. The US consumer continues to do well, driven by solid job growth, strong wage growth, and high stock prices and home prices.

See our chart book with daily and weekly indicators for the US economy.

…The rise in US bond yields has also been driven by improving US macro data (as well as Chinese stimulus). As fig 3 shows, yields have risen as the US Citi economic surprise index has picked up. Rising TIPS yields also correlate with reduced rate cut expectations (on the back of that better than expected macro data).

Fig 3: US 10 year bond yields vs. the US Citi economic surprise index

… inflation RISK somehow to mean more rate cuts? I dunno but anyways … inflation signaling out there …

…10-Year Treasury yields diverge from macro conditions, signaling inflation risk

…What the chart shows This chart consists of two panels, each offering a perspective on the relationship between US 10-year Treasury (UST) yields and macroeconomic conditions. The bottom panel tracks the "Qi Fair Value Gap.” The grey horizontal line separates periods where UST yields are either "too high" (above) or "too low" (below) compared to fair value based on macroeconomic inputs. The chart highlights how the 10-year UST yield has stayed mostly below its fair value until recently, indicating that yields are now above macroeconomic expectations.

The top panel compares the actual UST 10-year yield with the Quant Insight (Qi) model value, which represents the expected yield based on macroeconomic factors. Grey boxes highlight instances where the yield "catches up" to macro conditions. Recent data shows that UST 10-year yields are at their highest divergence compared to what macro conditions would suggest, signaling that current yields may be overextended relative to fundamentals…

… a bloodletting it has been …

WolfST: Treasury Buybacks: Update on the Bond Market Bloodletting

Among the jewels: Treasury Dept. paid 88 cents on the dollar to buy back 10-year Treasury notes sold at auction Aug. 2020 at a record-low yield of 0.677%.

… Some buyback technicalities.

Buybacks are not new. The Treasury Department was buying back older Treasury securities in 2000 through 2002, and on a minuscule scale once or twice a year from 2014 onward, with amounts such as $25 million a year, just to test the plumbing.

Treasury cites some reasons for the buybacks, such as to help manage its cash after tax season when it’s drowning in cash; and creating liquidity in an end of the market that lacks it. The effect – and the real reason for them – would be slightly lower yields in that end of the market.

Buybacks are supposed to ease a liquidity problem. The problem in the Treasury market is that older “off-the-run” Treasury securities are hard to sell because there is little trading in them, and sellers have to accept a (small-ish) haircut when they do find a buyer. The US Treasury market is the most liquid bond market in the world, but it’s not that liquid for older Treasury securities. So Treasury stepped in as buyer of “off-the-run” securities. Recently issued “on-the-run” securities, however, are easy to sell without haircut.

Buybacks are not QE. QE involved money creation – buying bonds with newly created money. That’s what the Fed did until 2022. Treasury cannot create money. It can only get money from collecting taxes and from borrowing – huge amounts of borrowing – which means that the Treasury Department issues new securities that add to the debt; the cash proceeds get spent on budget items and servicing the existing debt, and a small portion of those cash proceeds is now used to buy back off-the-run Treasury securities. Treasury cancels the securities it bought back and they cease to exist. In other words, with these buybacks, Treasury is swapping older bonds for brand new bonds.

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.