Good morning … it — HIMCOs Q3 ‘review and outlook — has arrived and … you guessed it, still bullish USTs. And ALWAYS worth a moment of your time.

In SHORT, he’s viewing global (US, UK, Japan, EZ and China) monetary policy as extremely tight and impacts yet to ripple through system and while Fed 50bps rate CUT was a start, there’s ‘significant lag’ between init FED policy move and any sort of meaningful boost of global growth.

HIMCO: Quarterly Review and Outlook Third Quarter 2024: The Rules of the Game

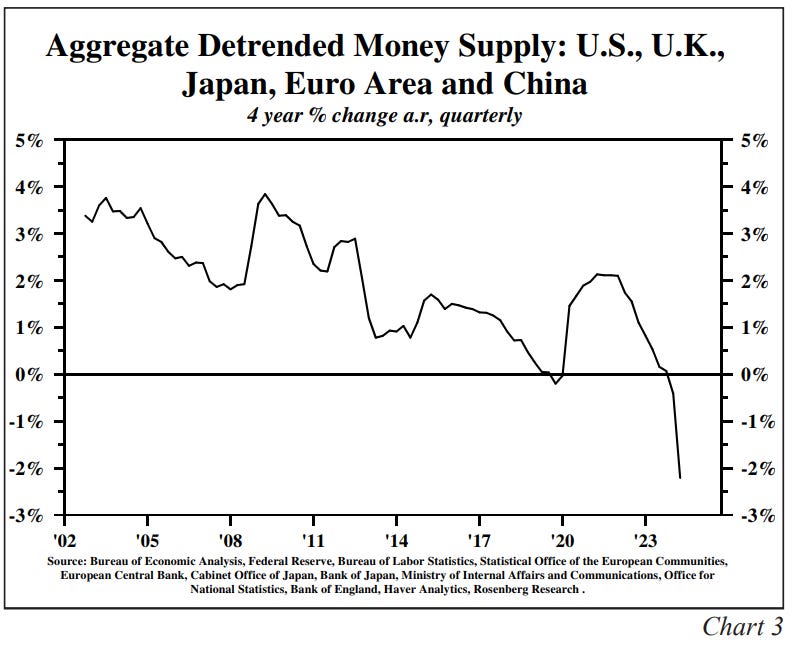

…A Single Globally Weighted Monetary Barometer The situation in these individual regions can be consolidated into a global directional indicator of monetary thrust that provides a comprehensive view of the monetary situation across these regions (Chart 3). This indicator is the most restrictive in the past twenty-two years, meaning that these five central banks, collectively, have significantly increased the risk of severe disinflation and poor economic performance. The combined detrended real M growth for these five economic regions is weighted by its contribution to world GDP. China's M is only available since 1998 and as four-year moving averages were employed, the series could only start in 2002. But it is critical to the value of the series to include China, because it is 19% of the global economy. Each country's yearly GDP, as measured by the World Bank, is weighted by its relative contribution to global economic output. Over this twenty-two year span, the four-year moving average of detrended global M has fallen to a record low in the latest reading. Although a limited sample period, it contains one extremely relevant comparison point. The slowdown in M growth during the Great Financial Crisis pales in comparison to the current situation.

…The Treasury Bond Market The headline and core inflation rates will continue to recede in an environment of more excess capacity combined with the monetary restraint of the past two years, which is still working its way into economic conditions (Chart 4). Accordingly, the Federal Reserve will have the latitude to lower the policy rate further. Moreover, additional cuts will be needed to reverse the multi-year decline in real detrended M growth. At the same time, long-term U.S. Treasury bond yields will follow the downward path in inflation. This pattern has been extensively researched and well-documented. The current evidence of the slow growth of real M globally and its impact on the world economy suggests the pressure for long term treasury yields to fall is increasing.

… This analysis is beyond solid and based on my personal experience, it’s worth reading this a couple / few times and letting it sink in. Furthermore, a couple / few more rate CUTS isn’t likely to help ones personal financial economic outlook before the election and one can only hope it will help overall situation within a year.

Now, as an offset TO Dr. Lacy Hunt, I’d urge one and all to read Rich Bernstein (RBA) note just below, “Tight Fed policy doesn’t always equate to tight liquidity” as it offers another and perhaps opposing view.

I’ll trust you can make up your own mind (and I’ll offer I’m leaning heavily towards HIMCO at this point now) and I’ll head back to the here and now. Actually, a couple / few links helping detail what happened yesterday …

ZH: Continuing Jobless Claims Jump To 3 Year Highs ZH: "Firms Are Worried" - US Manufacturing Survey Signals 3rd Straight Month Of Contraction ZH: US New Home Sales Jumped In September As Rates Fell, But...

… here is a snapshot OF USTs as of 652a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US futures are bid & DXY is flat ahead of US data & Fed speak … USTs are flat but directionally in-fitting with the pressure seen in Bunds, sparked by strong German Ifo metrics … USTs are flat with specifics light so far and while USTs have been dragged to a 111-06 low by EGBs they are yet to convincingly slip into the red. Docket ahead has durables in addition to potential remarks from Fed’s Collins.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

… never too early for an NFP pre-cap …

BARCAP October employment preview: Riders on the storm

We expect hurricanes and strikes to slow job gains to 125k in October, with additional distortions to the workweek, hourly earnings, and the unemployment rate (+0.1pp, to 4.2%). With uncertainty about the magnitude of these effects likely to linger even after the release, we expect the FOMC to downweight the signal.

… with jobs in mind, a few words on markets …

BARCAP: Food for Thought: Risk Premia Diverge, Again

The latest leg of the rally saw multiples expand and gains broaden beyond Big Tech while Treasury yields spiked, causing the equity risk premium to narrow sharply. While a depressed ERP is nothing new, the last time it fell this low vs. IG option-adjusted spreads was just prior to the summer risk-off.

BARCAP Equity Market Review: Not too bothered by rates

Equities have so far shrugged off rates volatility, helped by better US data and okay-ish earnings. Despite bleak EU macro and dovish ECB repricing, bond proxies have been hit, as the Trump trade prevails. But beware of reversal risk into the election. Q3 results have mostly been clearing events for Cyclicals.

…The spike in rates is grabbing the headlines once again, but hasn't derailed the rising equity market, so far. As recent history showed us, the equities-rates relationship is not linear and varies depending on policy, growth and inflation expectations. So far, the latest move up in yields seems to be for 'good reasons', i.e. the rebound in US economic surprises, suggesting the summer soft patch is largely behind us …

… France calling, update on GDP incoming …

BNP: US Q3 GDP preview: Strength to reinforce trim to downside risks

KEY MESSAGES

We estimate annualized real GDP growth of 3.0% q/q saar in Q3 2024 (released 30 October), a result that could look even stronger beneath the surface.

Consumers continue to drive spending, buttressed by strong fundamentals and a healthy labor market.

Another strong print is unlikely to stop the Fed from continuing its rate-cutting cycle near term. Inflation and labor market data still argue for gradual normalization, though we note broader financial conditions have been increasingly supportive of the growth outlook.

Downside risks receding: Stronger US economic data have shifted the balance of risks around our soft-landing base case. Indeed, in our most recent Global Outlook we saw risks as skewed to the downside, and at the time looked for just 1.7% q/q annualized GDP growth in Q3. Though pockets of stress remain for some consumers and businesses, resilient retail spending and a bounce in job growth in September leaves us assessing those risks as more balanced…

US Michigan consumer sentiment is due, including the inflation expectations reading. Is this useful information? It is not. The data will be distorted by frequency bias (there is more to life than food and fuel for the family fleet of SUVs, but that is pretty much all US households focus on for inflation). Political bias will also distort the data—Republicans think they are living in Weimar Germany, Democrats think inflation is under control.

Does the headline sentiment data tell us anything about the forthcoming US elections? Almost certainly not. One of the few things that can be said about the elections with any certainty is that the opinion polls are likely to be wrong. That includes polls like Michigan consumer sentiment…

… finally … this …

Wells Fargo: The Economics of the 2024 World Series The Los Angeles Dodgers vs. the New York Yankees in a Coastal City Clash

Summary Two Storied Teams with One Goal in Mind The 120th edition of the World Series will get underway today. The matchup will feature the Los Angeles Dodgers and the New York Yankees, two storied franchises who have spared no expense in the pursuit of bringing home the Commissioner's Trophy. The Dodgers signed rising star Shohei Ohtani this offseason, adding a major offensive weapon to a team who ended the regular season with the highest winning percentage in the major leagues. The Yankees also have no shortage of big-time talent. Aaron Judge and Juan Soto will lead the star-studded squad in search of their 28th championship for the franchise, which would be more than other team in the league.

The series begins at Dodger Stadium in Los Angeles. The Los Angeles metro economy has struggled to regain momentum following the pandemic. However, greenshoots are sprouting now that population growth appears to be turning around, tourism is picking up and the World Cup and Olympics are in the not-too-distant future. The series will then move to Yankee Stadium in the Bronx, New York City for at least game three and game four. Although the New York City metro economy still bears the scars from the pandemic, the city is starting to liven now that Manhattan foot traffic is recovering, payrolls are growing at a healthy clip and population flows are normalizing.

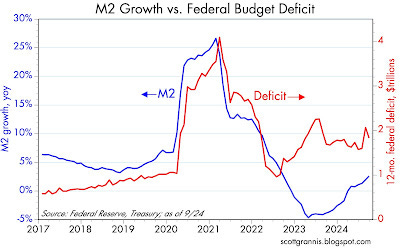

…Regardless, it is still vitally important to monitor money supply and demand. So far, nothing out of the ordinary seems to be happening, and that implies no unpleasant inflation surprises for the foreseeable future. The following charts include M2 as of the end of September, and my estimate for Q3/24 GDP.

Chart #1

Chart #1 shows how the surge in the federal deficit was mirrored by an increase in M2 growth. The link between the two dissolved in the latter half of 2022, with the result that ongoing deficits, though still quite large, are no longer being monetized.

… NOT from Dr. Vigilante BUT rather a former (popular kid and) BAML economist …

The heyday of the bond market vigilantes was during the Clinton presidency (1993-2001). During that period both Treasury Secretary Ruben and Fed Chair Greenspan argued that budget deficits created so much pressure on bond yields that reducing the deficit might actually stimulate the economy. This argument seemed a bit overdone to me, but it reflected the reality of bond market dynamics at the time.

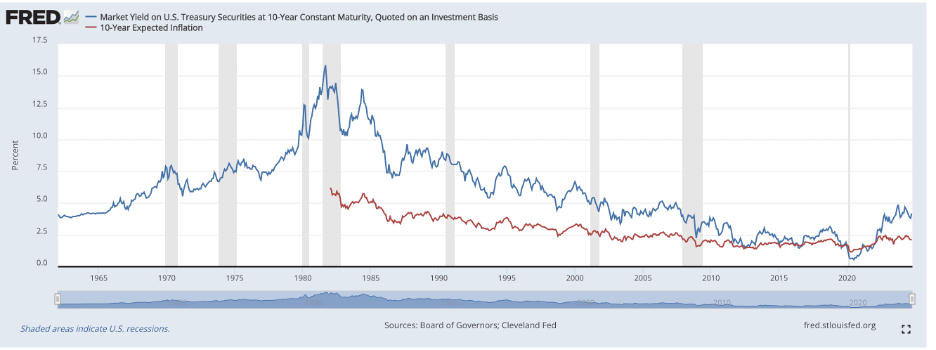

Over the decades, bond vigilantes have been beaten into submission like the moles in a game of wack-a-mole. Coming out of the 1965-80 Great Inflation bond yields were very high as investors demanded a large inflation risk premium. This could be seen in both market pricing and in surveys of household inflation expectations (chart). However, as the Fed continued to chip away at inflation and committed fully to a 2% target, inflation expectations and the inflation risk premium dropped. Indeed, prior to the Pandemic inflation expectations were starting to settle to below the Fed’s 2% target.

Long-run inflation expectations are from the MIchigan survey

Other developments reinforced the downward trend in bond yields particularly in the last two decades. First, interest rates have been even lower in other developed market economies, including near-zero yields in Japan. Second, the 2007-9 Great Financial Crisis was followed by a long “rehab recovery.” Even with near-zero policy rates and bond buying programs by the major central banks it took a long time for the US and global economy to recover. Yields finally hit bottom in 2020 when COVID crushed the economy and briefly caused a further drop in inflation.

What, me worry?

The upshot was that a generation of investors has learned that it is dangerous to short the bond market. With brief interruptions, bond yields fell from a peak of about 16% in 1981 to below 1% in 2020 (chart). I think this seemingly relentless trend is a big reason the markets have become oblivious to the budget outlook…

… Rip Van 10-year

In recent decades, one of the most common questions I’ve gotten from clients is: if the bond market can sleep through all of that, what will it take to wake it up? A corollary question is: when will the dollar lose its reserve currency status? My answer has always been a bit of a dodge: There is no obvious alternative to the dollar and US treasury market as the center of global capital markets. Hence, I don’t really know when the disaster will happen, but not soon…

…Direction of travel clear; timing uncertain

Like most economists, I’m not comfortable making short term market calls. The fundamental policy and economic backdrop matters in the medium term but can be easily overwhelmed by other market drivers in the near term. However, I think there is a good fundamental case for bond yields trending higher. Four things stand out:

· The 10-year yield has been on a choppy upward climb for more than four years now, marking the longest “bond bear market” since the 1970s. Could investors decide rising yields is more of the norm than the exception?

· As discussed above, not only are policy proposals pointing to higher bond yields, but I think investors are beginning to care. Look out if one party sweeps and is able to enact a lot of its campaign proposals.

· I still think the market is underpricing the neutral funds rate. The consensus seems to have shifted up from about 2.5% to about 3%, but I still think 4% makes more sense. A good starting point for thinking about the neutral rate is that it should be correlated with the 4% or so trend growth in nominal GDP (Chart above). More important, market and economic resilience suggests that current Fed policy is not nearly as tight as the consensus and Fed believe.

· While the Fed is winning the war on inflation, there are likely some more lasting effects. Inflation expectations seem to have risen from below-target to slightly-above-target. And nominal wage growth could remain high as workers demand payback for a period of weak real wages.

Even Rip Van Wrinkle woke up after 20 years.

… ever ask if someone could make inflation simple? WELP today’s your lucky day … actually YESTERDAY was …

FirstTrust: Three on Thursday - Inflation Simplified

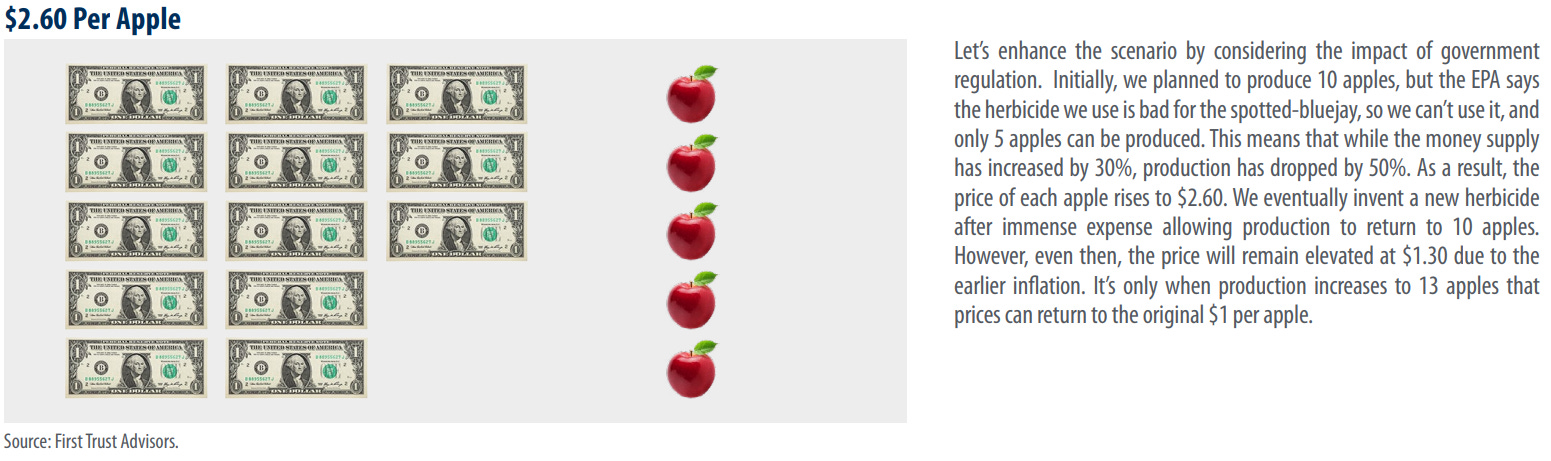

Contrary to popular belief, inflation doesn’t stem from rising wages, greedy businesses, government deficits, or even rapid economic growth—it results from the excessive printing of money. In this week’s “Three on Thursday,” we break down inflation in the simplest terms.

Milton Friedman famously stated, “Inflation is always and everywhere a monetary phenomenon, in the sense that it is and can only be caused by a more rapid increase in the quantity of money than in output.” Contrary to popular belief, inflation doesn’t stem from rising wages, greedy businesses, government deficits, or even rapid economic growth—it results from the excessive printing of money. In this week’s “Three on Thursday,” we break down inflation in the simplest terms. This is especially relevant today, as many people attribute the significant inflation of recent years solely to massive government spending or supply chain disruptions. However, these factors alone weren’t the root cause. For a deeper dive, explore the three graphics below.

…Growing concerns over rising U.S. deficits and who will win the White House next month may also be behind the advance in yields. Betting market odds for a former President Trump victory in November are tracking very closely to 10-year Treasury yields. In contrast, the odds for Vice President Harris to win are moving in the opposite direction of rates.

What’s Behind Higher Yields?

…What would a breakout above resistance mean for stocks? As highlighted in the bottom panel of the chart below, the last two sustained moves above the 4.25%-4.30% range created headwinds for equity markets. The start of the S&P 500 correction last fall and its pullback this spring both overlapped with a breakout in yields above this resistance range.

Yields Approach an Important Inflection Point

… BeachBoys weigh in …

PIMCO Macro Signposts | Fed Cuts and Market Responses: History Lessons Macro Signposts | 23 October 2024

Since 17 September – the day before the Federal Reserve cut its policy rate by 50 basis points (bps) – the yield on the 10-year U.S. Treasury has climbed roughly 55 bps to 4.2%. This seemingly counterintuitive trend over the past several weeks has spurred questions around the extent to which the current Fed easing cycle will potentially deliver positive returns for bond investors, as has happened in past cycles.

While historical patterns are complex and not definitive, an analysis of previous Fed easing cycles suggests that bond market price action in the first month after the Fed begins cutting interest rates does not tend to be a good predictor of either 1) the broader macroeconomic outcome that ensues over the next year and beyond, or 2) the extent to which high quality bonds are able to deliver positive returns.

Indeed, historical analysis of bond total returns across Fed cutting cycles – both recessionary and non-recessionary – reveals that bond returns have tended to be positive, and in excess of the overnight funding rate, across a range of cycles and macroeconomic environments.

Equity market performance directly subsequent to the first cut has a similarly poor record of foreshadowing the ultimate macroeconomic outcomes, although equity performance at longer time horizons has been much more divergent and dependent on how the economy lands.

Rates markets are far from a crystal ball We would caution investors from reading too much into the recent rise in bond yields. Over the past six major Fed rate-cutting cycles,1 the change in the 10-year Treasury yield a month after the first cut has not provided a consistent signal about the magnitude of further cuts or whether the U.S. economy falls into recession. In fact, yields rose in the month after the first cut more often than not (see Figure 1).

Figure 1: Yield on 10-year U.S. Treasury before and after initiation of major Federal Reserve easing cycles

Consider two quick facts:

In four out of the last six rate-cutting cycles (1984, 1995, 2001, and 2007), 10-year Treasury yields were higher by up to 32 bps one month after the first cut, versus the 38 bps increase in the first month during the current episode.

Comparing the specific cycles that began in September 2007 and July 1995 is particularly revealing. Despite the wildly different macroeconomic trends that ensued in the year after each first Fed rate cut, in both cases, 10-year Treasury yields rose 20 bps – 25 bps one month after that first cut. The 2007 cut came before the global financial crisis and more than 10 years of policy rates hovering at the zero lower bound, while the 1995 cut was a 50-bp one-and-done adjustment ahead of a multi-year productivity boom.

What about the equity market?…

…Investment takeaways Although uncertainty surrounds the outlook for the U.S. economy – the upcoming U.S. election could be a major turning point for policy – recent U.S. macro data have been robust, and futures market now price approximately seven 25-bp Fed rate cuts in the first year of this easing cycle.

If we see a similar outcome to the soft-landing episode of 1995, then history suggests a portfolio of high quality core bonds has potential to generate a positive outright and total return. More importantly, however, in the event the U.S. economy is unable to stick the soft landing despite apparent recent strength, then past cycles suggest that total returns for fixed income markets could be even more positive.

History indicates that starting yields have been a good predictor of 5-year returns. The Bloomberg US Aggregate Index is yielding 4.5% currently, and with and the extra benefit of the negative correlation between daily bond returns and equities returning as inflation has normalized this cycle, one could argue that the bond market is effectively paying investors to diversify.

Not a bad outcome given the uncertain path ahead…

… tight or loose? YES (choose your ending?) …

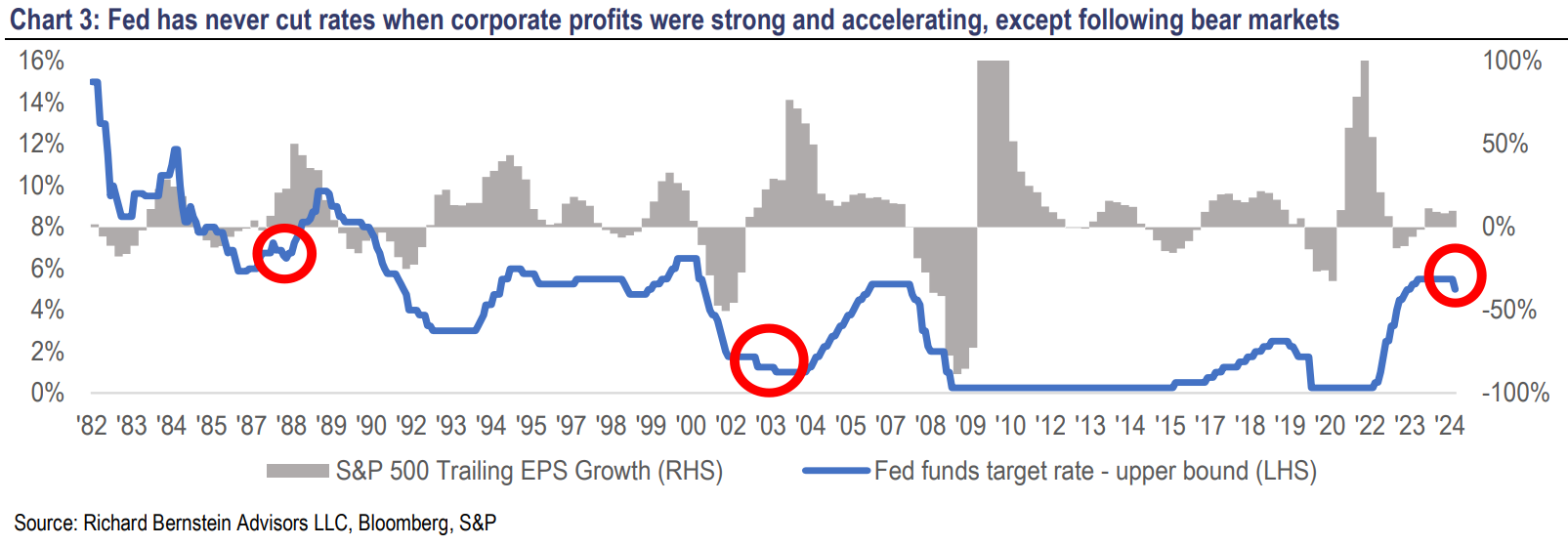

RBA: Navigating the tight policy, loose liquidity paradox

Tight Fed policy doesn’t always equate to tight liquidity The Federal Reserve's dual mandate is to maintain stable inflation and maximize employment. With inflation having fallen significantly and the post-pandemic extreme labor market tightness having subsided, the Fed believes its policies are now too restrictive, hence the aggressive start to its easing cycle. While the Fed’s policy stance appears tight on a variety of metrics (Chart 1), liquidity conditions tell a different story. The Fed manages liquidity through its policy tools, but it's crucial to remember that the Fed is just one source of liquidity among several. The Fed acts like a coxswain on a rowing team, steering the liquidity boat, but the rowers (factors like capital markets, fiscal policy, banks and foreign capital) aren't always in sync. Despite the Fed's efforts to tighten liquidity over the past year, other forces have moved in the opposite direction, keeping financial conditions relatively loose. Even banks, which have been tightening lending standards, have slowed their pace of tightening over the past year, contributing to an environment of easy liquidity compared to historical norms (Chart 2).

Could the Fed be adding fuel to the fire? This is the first time in history that the Fed has ever cut interest rates when corporate profits were strong (currently ~10% y/y) and accelerating, except in the wake of the 1987 and 2002 bear markets (Chart 3). Easing into an economy with ample liquidity and accelerating corporate profits could reignite inflationary pressures, particularly when key components such as food, health care, education and autos are already stabilizing or accelerating. Persistently higher inflation could eventually force the Fed into another round of tightening, potentially choking off growth. But in the meantime, faster nominal growth could benefit certain segments of the market, including US small caps, deep cyclical sectors (such as industrials, energy, and materials), and non-China emerging markets, all of which appear to be in the early stages of earnings recoveries.

AND somewhat more over the weekend but … THAT is all for now. Off to the day job…