while WE slept: FI down (OAT strength faded) USTs following; Q2 in review (DB); "Elections Have Consequences" (MS); "Fed’s Rate-Cut Delay Won’t Hold Back the Tide of Global Easing" (BBG)

Good morning … feeling as though I just hit SEND of a short weekend note, bit later than normal and I’m having quite a bit less than normal to say on a Monday morning.

Exaggerating this is the feeling is that in week ahead — interrupted by 4th of July festivities — we’ll have what most will enjoy as a 5d weekend ahead. Except for those working Friday (in office, remote?) managing PnL risks in / around NFP.

I’ll lead with a monthly look at 10s (in concert w/a monthly look at long bonds HERE)…

10yy: a definitively more BULLISH looking chart (relative to long bonds HERE) and in my view … momentum is bullish and while 2024 WAS defined by an uptrend AND rates were up something like 40bps in Q2, there may just be a new (down)trend developing (green) …

… and away we go with Q2 now firmly behind us, we all begin with (awaiting latest thoughts from Dr. Lacy Hunt / HIMCO) a clean slate and looking anxiously TO the day, week, month, quarter and half just ahead …

… here is a snapshot OF USTs as of 655a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Relief in Europe after the French 1st round has pared somewhat, ISM & Williams due … US Treasuries are directionally in-fitting with other core players; just off a 109-15 base but remain towards the low-end of a 10 tick range

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ … including some of the WEEKLY views which I may have missed …

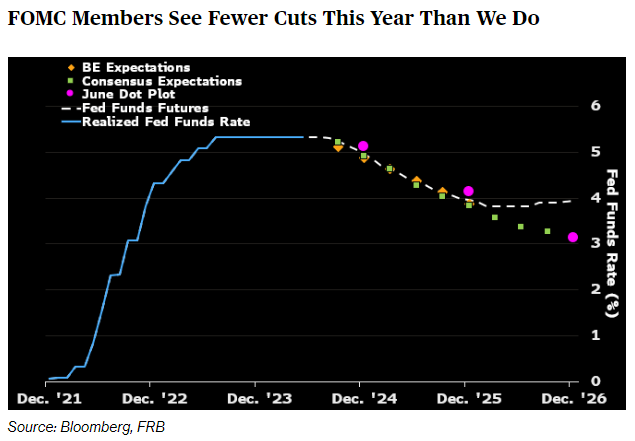

…US Rates – Stable forecasts & hedging risks Our US econ base case for a “cooling, but not cool” economy is consistent with our rate forecasts. We hold 4.25% 10y forecast through ’26 with Fed trough at 3.5-3.75%. Anticipate market to price larger election tail risk in coming weeks…

… Technicals

In line with our view, US10Y yield peaked by Memorial Day completing a countertrend 1H24. Reiterate buy dips / be long for H2.

We recap four scenarios: 1) Softer landing US10Y 3.50-3.22%. 2) Harder landing below 3%, maybe 2.67-2.11%. 3) No landing means repeating 2H22-1H23 with H2 choppy range. 4) Fast landing and fast recovery may mean +/- 3% then +/- 7%.

… The Biggest Picture: Biden & Trump responsible for 2 largest deficits of past 80 years (Chart 2); but inflation #1 issue for electorate, US govt spend -2% (rolling 12-month basis), fiscal excess wanes bigly in Year 1 new Presidential cycle (Chart 5); an election ”sweep” scenario bond -ve, but “split” scenario Congress bond +ve…latest probablities1 are Trump/split Congress 40%, Biden/split Congress 25%, Trump sweep 25%, Biden sweep 10%.

DB: June and Q2 2024 Performance Review (fan favorite monthly RECAP …)

Financial markets saw a pretty mixed performance in Q2, as investors focused on several risks to the outlook. On the positive side, equities continued to advance, and the S&P 500 reached a new all-time high thanks to further gains for the Magnificent 7. But the equity gains remained narrow, and the equal-weighted S&P 500 actually lost ground in Q2. Moreover, sovereign bonds struggled as investors priced in fewer rate cuts over the rest of the year, even as the ECB delivered their first rate cut since the pandemic. Geopolitical risk was also in focus, particularly around the Middle East in April. Then in June, French assets sold off after President Macron announced a snap legislative election. Towards the end of the quarter, there were also growing signs of weakness in global economic data…

Quarter in Review - The high-level macro overview … But despite the growing move towards rate cuts, sovereign bonds still struggled over Q2 as a whole, in part because investors were pricing in a more gradual cycle of rate cuts. For instance, at the end of Q1, 67bps of cuts were priced in by the Fed’s December meeting. But that was down to 44bps by the end of Q2. So sovereign bonds struggled to get much momentum, and the 10yr Treasury yield was up +20bps over the quarter to 4.40%.

… Which assets saw the biggest gains in Q2? The Magnificent 7: It was a very strong quarter for the Magnificent 7, which rose +16.9% in total return terms. Nvidia (+36.7%) advanced for a 7th consecutive quarter…

MS: US Equity Strategy: Weekly Warm-up: Elections Have Consequences (yes, yes they do … for more — or really quite a bit less — see Time Magazine cover image below …)

Investor focus has turned to the election following last week's debate. Industry performance on Friday appeared to follow the 2016 playbook, though we note some important differences relative to this period. Bottom line, election outcomes remain uncertain, and we stick with our quality bias.

… How problematic is inflation for the average American? Neel Kashkari, President of the Federal Reserve Bank of Minneapolis, recently said that "the American people...and maybe people in Europe, equally...really hate high inflation." He went on to discuss a conversation he had with a labor leader who works with lower income workers, quoting her as saying "inflation is worse than a recession." Another sign that inflation remains a concern for many Americans came via the latest University of Michigan Consumer Sentiment Index which showed that longer run inflation expectations remain elevated (Exhibit 1). This is consistent with our latest Alphawise Consumer Survey which shows that "coping with inflation" remains consumers' top concern (Exhibit 2; more on this in the section below). In our view, these dynamics further the case that inflation is going to play a major role in this year's upcoming US election much like it is having an impact globally.

Housing prices have been rising globally. In the US, these are a reflection of the mortgage lock-ins, and do not indicate that monetary policy is less effective.

Is UST market liquidity worsening? The large size of the bill auctions and the continuation of the Fed’s QT are gradually putting upward pressure on repo rates. SOFR has moved 3bp higher this week as we approach the quarter-end (Graph 13). The volume-weighted 99th percentile of SOFR has moved as high as 5.5%, the rate offered at the Fed’s Standing Repo Facility. The increased demand for USD which originated in the French turmoil two weeks ago, is exhibiting itself in slightly higher repo rates, narrower swap spreads, and a wider cross-currency basis. We expect the immediate pressure to ease after the quarter-end.

We are still far from the extreme liquidity conditions of March 2020 or September 2019, but you wouldn’t know that from Bloomberg’s UST illiquidity index. This month the index has spiked higher than it ever was in 2020 (Graph 6). The index shows the “equally-weighted average yield error” of all USTs with maturities of >1y based on a fitted curve. We do not view the current extreme level of the Bloomberg index as a good measure of prevailing liquidity conditions. The measure has departed from the MOVE index, which shows declining rates volatility this year. Spreads between off and on-the-runs, while increasing moderately in recent weeks, are not at extreme levels. If one adjusts the Bloomberg illiquidity index for the average level of rates across the curve, it shows a much more moderate increase this month (Graph 14). While the average yield errors from Bloomberg’s fitted curve are undoubtedly larger than in 2020, they are not larger relative to the level of rates. Finally, Société Générale tracks the UST futures market’s liquidity by measuring the ratio of volume available to be traded at the best bid and ask vs the total volume traded each day. This indicator shows improving liquidity in UST futures since March 2023 (Graph 15).

TD Global Rates Weekly: Everybody Wants to Rule the World

UBS: The trouble with three-ways (France, you degenerates … FRENCH elections reference … nothing more, nothing less…)

The first round of the French elections produced results broadly in line with opinion polls (as to the popular vote). An unusually large number of second-round votes could be three-way contests. That makes the final outcome harder to predict. In the past, there has been a “front républicain” with third-placed moderate candidates withdrawing to increase the chances of defeating a more extreme party (in this election, the Rassemblement National). It is not clear how many constituencies will follow such a strategy.

It now seems less likely that one group will have a majority after the second round, but investors would be unwise to place too much confidence in that. A weaker minority government is unlikely to tackle France’s fiscal situation (although a Truss-style crisis can probably be avoided). The elections remind investors that economic structural upheaval encourages prejudice politics, and this will be more evident in more countries…

… And from Global Wall Street inbox TO the WWW,

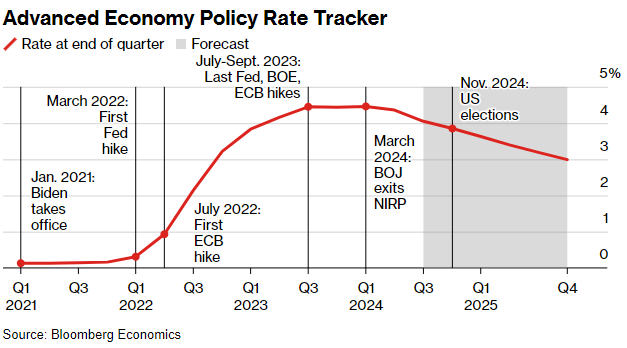

Bloomberg: Fed’s Rate-Cut Delay Won’t Hold Back the Tide of Global Easing

Almost all major central banks are now on a path to rate cuts

Easing may not be swift or synchronized, but it’s happening

Global policymakers aren’t about to let the Federal Reserve’s delay in cutting interest rates distract them too much from their own easing efforts.

Among the 23 of the world’s top central banks featured in Bloomberg’s quarterly guide, only the Bank of Japan won’t end up lowering borrowing costs within the next 18 months. Most are already set to do so this year.

In total, 155 basis points will be removed from an aggregate benchmark global rate compiled by Bloomberg Economics by the end of 2025. Even the Fed itself, whose plans for cuts in borrowing costs went awry in the face of stubborn US inflation, will still end up delivering a couple of moves this year, the forecasts show…

… What is clear by now is that prospects are dwindling for a swift removal of the unprecedented global tightening delivered during the post-pandemic cost-of-living crisis.

In tandem with the caution of their US peers, central bankers worried about lingering consumer-price pressures are seen adopting a far gentler trajectory downwards for rates than they did on the way up…

Bloomberg: ‘Non!’ to Macron opens longest week in politics (Authers’ OpED)

Biden, UK also face destiny as Le Pen’s far right takes pole position in France, though markets seem unperturbed — so far.

… How Can Markets Possibly Be This Healthy? With the first half of the year now over, the MSCI All-World index is up 10.3%. Nothing wrong with that. True, there’s a big imbalance between the US (up 14.8%) and the rest of the world (4%), but this still is far stronger than we would expect if markets were seriously alarmed. The strength can ultimately be attributed to two factors:

Disinflation

The single biggest reason for this strength, the hidden necessary condition,is an assumption that inflation is beaten. Concerns over how long it will take to get year-on-year price rises down to 2%, or to restore living standards for poorer people worst hit by the price spike of 2022, aren’t really so relevant. The important point is that inflation won’t go back up, so rates won’t need to rise. If that’s right, all things become possible. And the latest Personal Consumption Expenditure deflator figures for May, published Friday, confirm that the Federal Reserve’s favored inflation gauge is steadily declining. Both the core PCE — excluding particularly variable items — and the trimmed mean produced by the Dallas Fed, which excludes outliers and takes the average of the rest, are now below 3%. They remain above target, but the direction of travel seems clear:

rt

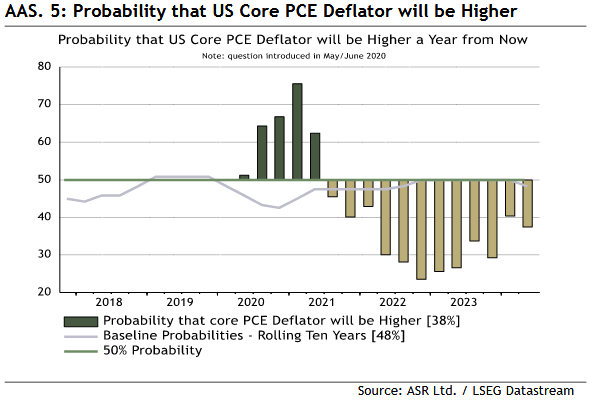

There’s room for much argument about exactly how fast the Fed can cut rates from here, but very little case for a hike. That’s what matters. If rates are reducing, then it’s safe to buy risk assets now, and that’s what asset allocators are doing. The latest quarterly survey of allocators by Absolute Strategy Research shows this clearly. Confidence that the PCE will be lower still a year from now remains very strong:

That translates into strong confidence that the era of monetary tightening is over. It’s possible that rates will remain on a plateau for a while, but there’s confidence that policy will ease from here, and not tighten:

What’s strange about this is that the confidence is not broadly shared. Last week saw the latest updates of surveys of inflation expectations conducted by the Cleveland Fed among company managers and the University of Michigan among consumers. Over the next 12 months, consumers think inflation will continue at roughly the level it is now. Companies are bracing for an increase. If inflation really is at nearly 4% this time next year, as companies predict, rate hikes will be back on the agenda:

The consumer survey conceals a growing split over how bad future price rises could be. The most commonly cited figure is the median, but Michigan also publishes a mean, which is generally higher (very, very few people expect negative inflation, after all). The way the mean and median have parted company over the last year is spectacular. This chart shows the mean and median consumer expectations for inflation over the next five years:

If the average American consumer expects inflation to run at more than 5% for the next five years, that implies that expectations have veered out of control. With the median below 3%, a significant body of people must be braced for double-figure price rises. That’s incompatible with policy easing, and would throw a wrench into more or less any positive scenario for the economy. It’s possible that a coterie of ideological conservatives have convinced themselves that hyperinflation lies ahead, but even then it’s bizarre that their forecasts are higher now than two years ago when inflation was at its peak.

These expectations matter because they can be self-fulfilling. If companies and a significant chunk of the population are bracing for higher prices ahead, that will affect their behavior. And if they’re right, many of the world’s most important asset allocators are wrong.

… with this little in mind, a quick look at week ahead where I’d point out how jam-packed WEDNESDAY is

… (1) Payroll employment. We expect that June's employment report (Fri) will show payrolls rose by 150,000 to 200,000, and that wage inflation continued to moderate. We've previously observed that payroll employment is highly correlated with S&P 500 forward earnings, which climbed to a record high in June (chart). That makes sense, since profitable companies tend to expand their payrolls. while unprofitable ones are forced to pare their payrolls.

(2) Household employment. We will be having a close look at the household measure of employment, which fell 408,000 during May, led by a 474,000 drop in 20-24 year-old workers (chart). We suspect that was a seasonal issue related to college students. If so, then both these series should have rebounded during June.

(3) Unemployment rate. Everyone seems to be expecting that the next surprise in the labor market will be a jump in the unemployment rate (Fri). It rose to 4.0% in May, the highest reading since January 2022. We think that uptick was related to the seasonal issue among college students. If so, then the unemployment rate should have remained at, or fell back below, 4.0% during June. The jobs-hard-to-get series confirms our expectation (chart).

… Finally a couple visuals to consider …

… AND …

… AND, and … happy … happy …

(for those not aware OF what I’m referring to … HERE is ESPN LINK and … THAT is all for now. Off to the day job…

Bobby Bonilla Day, what a gold mine deal he struck for himself, thanks for the smile that story brings!

Most excellent today, great inflation analysis love all the charts!

Since you went there, and I am a Degenerate :), Never trust a woman if she offers a 3-way scenario. About the only thing I still agree w/Howard Stern on (finally outgrew him in 2017 I wonder why....) is it's a Loyalty-Sh!t test for a man. Don't fail it!

Bond Yields have jumped the last few days, is this mainly due to

Quarter End/Mid-Year Rebalancing ???

Bobby Bonilla Day, what a gold mine deal he struck for himself, thanks for the smile that story brings!

Most excellent today, great inflation analysis love all the charts!

Since you went there, and I am a Degenerate :), Never trust a woman if she offers a 3-way scenario. About the only thing I still agree w/Howard Stern on (finally outgrew him in 2017 I wonder why....) is it's a Loyalty-Sh!t test for a man. Don't fail it!