Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…and my apologies for late delivery as futures are open and so, without further delay and in light of monthly charts being updated / ready for consumption …

30yy MONTHLY … see what you wanna see … bearish UPtrend OR a bullish cross of momentum …

… as always, it’s the WHAT NEXT which matters and after this weekend I’m not sure I’m seeing things to sway ME one way or another (sorry, not sorry) and so, a couple / few things items from Friday …

CalculatedRISK: Personal Income increased 0.5% in May; Spending increased 0.2% CalculatedRISK: PCE Measure of Shelter Slows to 5.5% YoY in May

ZH: 'SuperCore' Inflation Rises For 49th Straight Month As Spending Disappoints

… All told by days, weeks, month, quarter and H1 end, here’s how the cookie crumbling, at least as detailed (not badly) by some snarkists ‘out there’ …

ZH: S&P Surges To Best Election Year H1 Since 1976As Rate-Cut Hopes & Macro Data Collapse

… But away from politics (and today), US Macro data serially disappointed in the first half of the year, crashing to its ugliest since 2016. This was the worst start to a year for macro surprises since 2018 (and second worst since 2012)...

But, despite all this 'bad news', rate-cut expectations have plunged YTD, with 2024 starting the year with 160bps priced in and ending H1 with just 45bps priced in. 2025 expectations did pick up modestly, from around 70bps to 87bps...

… Ok I’ll move on AND right TO the reason many / most are here … some WEEKLY NARRATIVES … some of THE VIEWS you might be able to use.

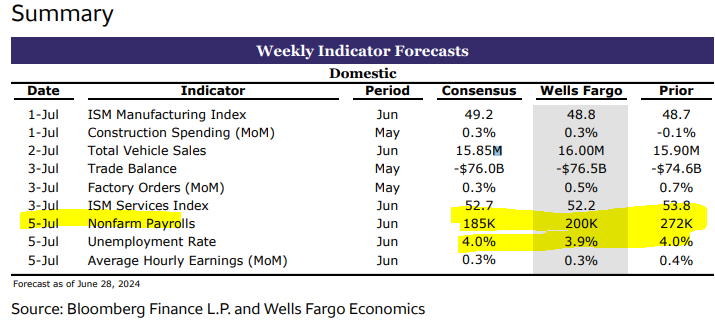

THIS WEEKEND, a couple / few things which stood out to ME this more of a laundry list / link-fest (reach out if links don’t work OR you’d like a note here / there) and as has been the case past few days, there are more than a couple NFP guess-timates…

BARCAP May PCE: Spending fundamentals remain on strong footing

Real PCE rose more than expected, up 0.3% m/m, following a decline in the prior month. This is in line with our lack of conviction that consumers are losing steam, given the still-low saving rate, strong household fundamentals, and income gains.

Core PCE price inflation was only 0.08% m/m in May, bringing the annual rate lower to 2.6% (from 2.8%). As expected, the slowing was broad-based across goods and services and supports our baseline call that the FOMC will deliver one rate cut this year, in September at the earliest.

… US Outlook Mistaking moderation for deterioration Intensified pessimism about aggregate demand remains unwarranted, in our view. Although underlying growth has slowed from its unsustainable pace in H2 23, data appear to be aligning for a soft landing, with underlying fundamentals still posing upside risks to growth and inflation. We retain our September cut baseline.

BMO: Questionable Payrolls? (entering 2s10s flattener and got short 5yr ‘breaks’)

…The divergence between the household and establishment surveys in May triggered a surprisingly active debate on the accuracy of the headline NFP figures, as did the comparison between the QCEW (quarterly) and the CES (monthly) pace of payrolls growth. This isn’t to suggest that investors are questioning the quality of the data in outright terms – instead there is simply a collective acknowledgement of the limitations of the surveys in accurately reflecting the realities of the real economy. It strikes us that this is consistent with an inflection point for investor sentiment, and we anticipate that any data showing a softer employment market will trigger sharper price action than confirmation of its ongoing resilience…

While the far-right Rassemblement National won strong support in the first round of the French parliamentary elections, we think its chances of securing an absolute majority look somewhat diminished compared with some opinion polls in recent days.

Extremely high voter turnout has paved the way for an unusually large number of three-way votes in the second round of 7 July, making alliances formed in coming days particularly important, and raising the prospect of a hung parliament.

Although the situation remains fluid, the result of the first round will probably be taken as marginally positive by markets, which had begun to price in a higher chance of an absolute majority for the far-right in recent days.

Rates: Risk premia have room to unwind a bit further, in our view, but the newsflow over the next two days will be key for the move to extend more meaningfully.

Equities: We expect a relief rally in French-election-sensitive high-beta stocks, and the CAC could rebound by around 2% over the next few days. We also see VSTOXX moving lower on Monday, though we expect this to retain its value.

Credit: We consider the diminished risk of a far-left majority a marginal positive for European credit.

FX: EUR is likely to rally on Monday, but we remain bearish.

BNP US rates: Front-end asymmetry returns into payrolls

We see value to front-end flatteners as risks to rates heading into hard activity data remain skewed to the downside. A deterioration in the labor market would force markets to price a lower Fed terminal rate, in our view.

Although another solid NFP print is likely, we believe market risks are asymmetrically skewed in the event of a weaker number.

We like Z4/Z5 flatteners into a data-packed week in the US.

We advocate positioning in trades that would benefit from a “worse than expected” outcome of the French election’s first round this weekend, but can also perform for fundamental reasons outside of French politics.

More Evidence that Disinflation Has Not Stalled … The Dallas Fed’s trimmed mean PCE prices measure slowed to 2.8% on a 12-month basis in May from 2.9% in April. Though not yet consistent with the Fed’s inflation objective, this 12-month inflation rate has moderated in every month since April 2023 and in 19 of the last 21 months.

MS Friday Finish: Higher Rates Aren't Stoking Inflation (so, Team Rate CUT or the other guys? def Team Rate CUTS)

The idea that the interest earned on savings is adding fuel to spending and creating upside inflation risks is misguided, missing the full picture of the aggregate household. On balance, net interest payments have been rising, dampening buying power – especially among lower-income cohorts.

… Liquidity is falling, net interest payments are rising, and by income group, the lowest quintile is feeling the heat. Our tracking of the data suggests that the narrative for the consumer has not changed. The low-income household has been in recession for some time and their burden is growing. A post-earnings season check-in with our equity analysis confirms that the middle- and middle-to-upper-income groups are trading down in price, while upper-income groups continue to spend. Putting it all together, real consumption is tracking 1.7% Q/Q annualized growth in 2Q24 (2.4%Y) compared with 3.1% Q/Q in 4Q24 (2.7%Y). Interest rates are restrictive – their effects continue to move through the economy and deepen.

MS: Time To Enter UST Steepeners | Global Macro Strategist

After having adopted a neutral stance on the US yield curve for much of the past year, we believe now is the time to enter US Treasury curve steepeners. Heightened risks and uncertainty during election season, coupled with Fed rate cuts, should help the curve steepen finally and convincingly.

… Overall, we suggest adding 2s20s curve steepeners, expecting both a pathway to more cuts as well as markets adding more term premiums in the long-end. We chose the 20y point over the 30y point given the recent richness of the 20y point over the 10s20s30s butterfly (see Exhibit 15). The key risk to the trade is rise in probability of president Biden, or stronger economic data …

MS: Sunday Start | What's Next in Global Macro: Growth versus Inflation

… Markets do have a lot to consider though. Soft landings are rare historically, so a recession is surely a risk. And slowing real GDP growth combined with falling inflation means that nominal earnings are likely to slow even more, at least on average. The slowdown may feel rougher than a soft landing…

… Part of our slowdown for this year, and a huge dose of uncertainty for next year, comes from fiscal policy. The ramp up in spending contributed to rapid growth last year; this year, spending is still flowing, but not at an increasing rate, so the fiscal contribution to growth has gone away. Again, a slowdown without a crash. But the fact of the election in November means the range of fiscal policy outcomes is wide. And any gridlock that leads to contractionary policy like the Budget Control Act last decade could cause a slump. Worse still, as we have noted, tariffs are disruptive to economic activity and could lead to a sharp slowdown. But the market focus is on the here and now, and we do not think the slowing in the data amounts to a material risk.

June payrolls slow to 210k because of softening demand for and supply of labor. We forecast no change in the unemployment rate at 4.0%; if weaker demand dominates, unemployment instead rises to 4.1%; if weaker supply, it could fall to 3.9%. AHE rises 0.3%M, slowing to 3.9%Y.

Q1: What does the US election mean for markets? Stick to the playbook Uncertainty is high for election results and the macro impacts of key policy choices – as a result, investors should prepare for more noise than signal. To weather these uncertainties, we suggest sticking to the cross-asset playbook that favours carry, convexity and cheap optionality. Policy choices also have reliable impacts on equity sectors, hence opportunities exist in those with a positive skew across outcomes (e.g., industrials and telecom)…

… Q5: Why Are We Still Bullish On Copper After Its 10%+ Rally Year To Date? Because Of Supply Tightness

NWM: US Weekly Economic and Strategy Brief (all eyes on jobs Fri aft mkts closed Thurs and so …)

…Jobs preview: We forecast 200,000 payrolls; 4.0% unemployment; 0.2% earnings

… Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW

ING: US inflation relief and consumer cooldown boosts chances of rate cuts

The Federal Reserve's favoured measure of inflation came in at just 0.1% MoM, offering hope that the first quarter "hot" prints are firmly in the rear-view mirror. US consumer spending is also slowing with first quarter growth set to come in at less than half the rate recorded in second half 2023. This combination boosts the chances of Fed easing policy

WolfST: Fed’s Wait-and-See on Rate Cuts Makes Sense amid Whiplash Data: Still Worst 6-Month “Core” PCE Inflation since mid-2023 but Freak Plunge in Durable Goods

Housing inflation was hot and accelerated in May, amid crazy whiplash-data in other services.

ZH: 4 In 10 Americans Will Stay Put This Summer As Money Is Tight

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

Excellent article...as usual.

Given Mr. Biden's poor debate performance, I'm looking for a blowout

NFP number, delivered by our politically unbiased BLS....Gotta change the negative headlines, somehow???