To begin this morning, here’s a visual of 3yy which, after Friday’s debacle of a NFP — I mean one which was so good it was terrible? No, it was GREAT … Rates are back down a touch … squint and you can see it

I’ve broken out a new crayon and gotten to work in effort to find some relevance on the DAILY charts … Momentum suggesting rates overSOLD but ahead of CPI with Friday’s upside surprise to the jobs report, well … that makes some amount of common sense.

… here is a snapshot OF USTs as of 705a:

… HEREis what another shop says be behind the price action, you know,

WHILE YOU SLEPT Treasuries are modestly higher and the curve a touch flatter with nothing on the calendar today save for the 3pm Treasury auction bidder classification details. CPI looms large on Wednesday. DXY is lower (-0.17%) while front WTI futures are too (-1%). Asian stocks were mixed/little-changed, EU and UK share markets are all higher (SX5E +0.9%, FTSE 100 +0.5%) while ES futures are showing +0.5% here at 6:50am. Our overnight US rates flows saw a front end-led dip to Friday's lows in the early Asian going before better buying from real$ emerged in 10's while fast$ sold the uptick. There also was some real$ interest to sell 30's and flatten 10s30s curve. Overnight Treasury volume was notably weak at ~70% of average overall (3yrs again seeing the highest relative average turnover among benchmarks at 94%).

… On the other hand, it will be interesting to see where TLT's trade today after Friday's close confirmed a break below its similarly-constructed bull trendline while next- up we show how Treasury 30yr yields linger near their trend support level. 30yr yields closed Friday right on their trendline, as you can see if you squint.

… and for some MORE of the news you can use » IGMs Press Picks for today (8 August) to help weed thru the noise (some of which can be found over here at Finviz).

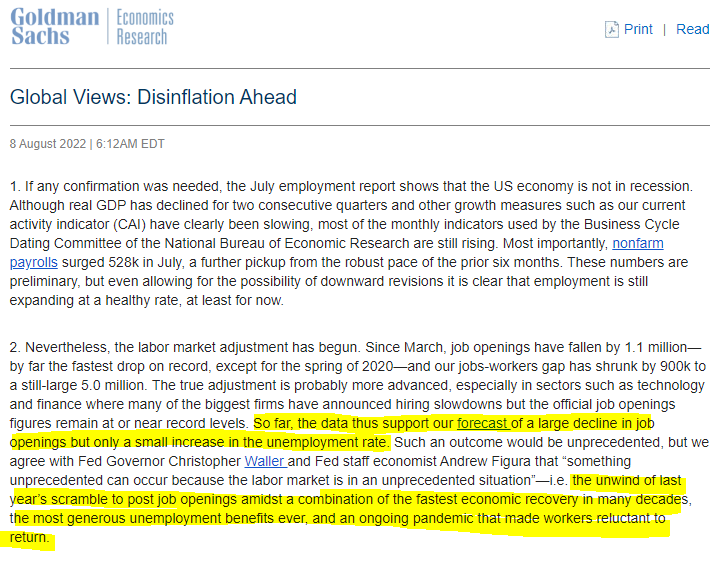

The first one just hitting inboxes across the land as those who are actually in this lovely Monday morning, will be greeted by THIS from Goldilocks

You need to make it all the way down to bullet #5 — thinking RATES,

5. The rates market sold off sharply on Friday’s jobs report and is now leaning toward another 75bp move at the September FOMC meeting. This may end up being correct, but we still think a downshift to 50bp is more likely if the next two CPI reports do show significant underlying disinflation. Beyond September, we expect two more 25bp hikes in November and December—consistent with the June SEP—before the committee goes on hold for an extended period at a 3¼-3½% funds rate. We don’t see additional hikes in 2023 because we expect growth to remain well below trend and inflation to come down steadily further, and we don’t expect cuts unless the economy looks close to entering a full-blown recession. That said, the risk to our forecast is that it will take a modestly higher terminal funds rate to put the economy on a sufficiently disinflationary path.

Barclays stating what I believe to be the obvious, in a general sense…

No backing down Solid economic data have undermined the narrative of a dovish pivot from central bankers

Last week’s robust US employment report underlined persistent inflation pressures. That implies a need for higher rates from the Fed, regardless of softer commodities or slowing growth. We see upside risk to our +50bp forecast for September. We also see one last hike of 25bp from the BoE next month, before a pause as a recession hits.

In the US, we continue to recommend positioning for more anchoring of long-term rates, even as the Fed is priced to hike more aggressively. We hold on to our 2s10s30s long in Europe, where the market remains torn between fears over inflation and growth. In the UK the weak outlook makes rate cuts in 2023 more probable and we recommend Dec 22/Dec 23 MPC OIS flatteners…

Whether or not MARKETS need to (re)PRICE this news is, as always, most important part of the equation …

… I’ll leave it to you to provide the appropriate markets-related caption …

HERE is one from a large German bank touching on a topic I’ve been most curious about …

… Harsh hedging costs. There’s also a lot of discussion about rising hedging costs (thanks to DM rate hikes) deterring Japanese investors - as existing FX hedges roll off, they simply repatriate the money. With the Fed at the vanguard of hiking, the resulting higher hedge costs have made the hedged yield on US bonds negative for a Japanese investor - a huge drop from the 1½% yield on offer last year (figure 4). Consistent with this, the majority of Japanese selling has been of US bonds, with little move in European holdings where the hedged yields are still positive (figure 5).

And for your inner stock jockey, the latest from Mike Wilson (alluded to last night HERE)

Operating Leverage Cuts Both Ways as Inflation Peak Signals Margin Risk The rise in inflation and the Fed's reaction to it has been a real headwind for valuations this year. However, it's also been a tailwind for earnings. Now, we are on the other side of that mountain, and operating leverage is rolling over likely more than the consensus expects.

Be careful what you wish for…Inflation has likely peaked and will probably fall faster than the market currently expects. That's good for multiples and is why we have seen rates fall and P/Es expand sharply over the last 1-2 months. Now, however, we see falling inflation weighing on profits as operating leverage starts to reverse. Just like most underestimated the positive effects of inflation on operating leverage, we think they are underestimating the negative effects from inflation falling…

… Earnings season...signs of negative operating leverage emerging...Second quarter earnings are tracking at +7% YOY for the S&P 500 with about half of sectors seeing positive earnings growth.Topline growth is tracking at +14% YOY for the S&P 500 with Energy once again the key contributor to index level growth. Most sectors are seeing revenue growth in the mid teens.That said, the majority of sectors are experiencing negative operating leverage, meaning that sales growth exceeds EPS growth—a dynamic that is evident at the index level. Despite signs of margin compression this quarter amid this operating leverage dynamic, bottoms up consensus is still calling for margin expansion into 2023, a development that we find unrealistic due to sticky cost pressures (particularly in labor) and receding demand…

So while prices to the end consumer are still rising at a rapid clip, prices for producers are rising at double the pace. That spells trouble for margins over the next several quarters …

The rally in stocks has been powerful, and has many investors believing the bear market is over. However, we think it’s premature to sound the all-clear simply because inflation has peaked. The next leg lower may have to wait until September when our negative operating leverage thesis is more reflected in earnings estimates. However, with valuations this stretched, we think the best part of the rally is over…

IF you desire somewhat MORE and a bit of a nostalgic walk down memory lane with some principles applied to markets of HERE AND NOW, this weekends Barrons,

Dr. Doom offers a few words on JPOW relative TO Volcker,

… the central bank’s approach is starkly different, Kaufman observes. The current monetary authorities prefer to deal incrementally, as opposed to the bold action taken by the Volcker Fed, starting in 1979. In particular, today’s Fed didn’t act swiftly to reduce liquidity by shrinking its balance sheet. Instead, it continued to buy Treasury and agency mortgage-backed securities when inflationary pressures were building last year, notably in the housing market.

“Today, you have a man of much milder behavior who is not an aggressive mover on monetary policy,” Kaufman says, referring to Fed Chairman Jerome Powell.

The character of the policy-setting Federal Open Market Committee also has become less confrontational, with few dissents, he further notes, in contrast to the disagreements seen during the chairmanships of Paul Volcker and his successor, Alan Greenspan. Kaufman also speculates about the influence of Treasury Secretary Janet Yellen, Powell’s predecessor as Fed leader. Trained as a labor economist, she is more predisposed to an easier policy to support jobs than to a tougher one to curb inflation, he says…

As far as inflation (CPI Wed) and interest rates,

… Kaufman expresses little confidence that the central bank will quickly get back to its previous 2% inflation target. Instead, he suggests, the monetary authorities may equivocate before reaching that goal. In other words, if 1982 was the beginning of the end of the inflation fight, we’re not even at the Churchillian end of the beginning now.

How, then, to explain Treasury bond yields under 3%, with the trailing 12-month CPI over 9%? Kaufman attributes this to feelings that the impacts of high oil prices and the war in Ukraine could resolve themselves.

He also points to the short-term mind-set of institutional investors. They have a trading orientation based on what he calls the illusion of the high degree of marketability of their holdings when they want to sell. That assumption was sorely tested during the pandemic-precipitated upheavals of March 2020. Furthermore, he adds, credit quality has deteriorated during the market cycles of the past decades…

{kind=link}

Good Work - Thank You!