sellside observations (NFP recaps / victory laps), a couple FUNduhMENTAL economic calendars and "...statistically indistinguishable from zero ..." (the IRA which has passed)

Good afternoon … HERE are a few OBSERVATIONS from the Sellside … There is very little research or analysis on The Inflation Reduction Act which has recently been pushed through.

Keeping in mind whatever the ultimate impact MAY be, the financial world was coming to an end in ‘08 and the TARP (Troubled Asset Relief Program) failed before it was also pushed through.

$700bb in DC seems to be the magical number and I have not read the bill and only have some suspicions about it’s impact. I’ve got some links for somewhat more in a bit but for now …

… There are many ways to measure liquidity or "money" in the financial system, and all have strengths and weaknesses.

One lesser known but important measure is called "other deposit liabilities," which essentially measures all deposits in the banking system but excludes the large time-deposits like "CDs" that are not readily spendable.

Adjusting this deposit measure by the CPI for a "real" metric allows us to compare liquidity growth across time and across periods of high and low inflation.

From 1950 until 2008, this liquidity measure, "real ODL," increased by roughly 2.0% per annum. Over this same period, the velocity of money increased at a 0.2% annualized rate, very stable.

After the financial crisis, real ODL increased at a 5.1% annualized pace. Despite money growth of 2.5x the historical average, inflation never leaked into consumer prices.

Why?

Since 2008, the velocity of money declined at a 3.6% annualized rate, completely neutralizing the 3.1% excess money growth.

The Federal Reserve is on track to reverse the excess liquidity by the middle of 2023 if they continue raising rates and reducing the size of its balance sheet.

Pausing interest rate hikes at ~3.5% is not problematic, particularly as the QT operations continue to withdraw liquidity.

If the Fed stays on track, liquidity will return to the pre-COVID 5.1% trend, which is still above the long-term rate.

However, the conditions that have caused the persistent decline in velocity, namely excessive debt, are still operative, so this is likely sufficient to bring inflation back into an acceptable range.

If the velocity of money stabilizes, then further liquidity drains will be necessary, but without an improvement in the productivity of debt, velocity will grind lower and offset the excess liquidity as it pertains to an increase in consumer prices.

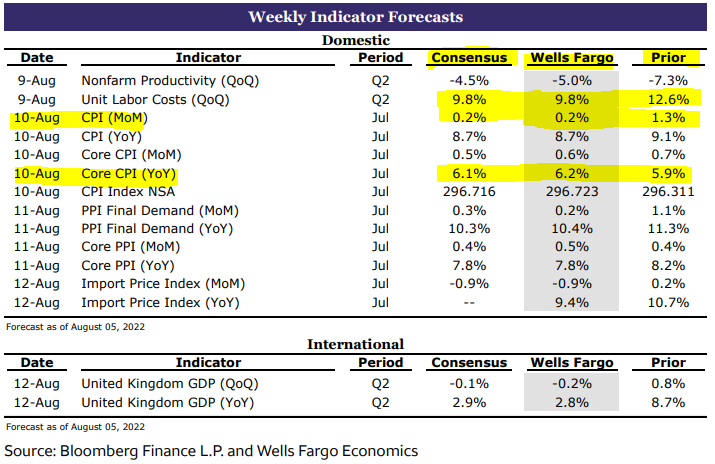

AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

Finally, given there’s an interesting weekend vote shaping up in DC where topic of debate and soon to be increased taxes and rules/regulations coming to a theater near you and me soon — you know — that which is being sold / billed as the INFLATION REDUCTION ACT, I thought I’d leave this here — some from UPENN / Wharton thoughts

{kind=link}