Good morning … With bond markets closed in observance of Columbus Day and with Day 3 of middle east tensions flaring, I’ll be brief.

Given my career focus on the CASH bond markets, please forgive me if this look at FUTURES (per TradingView) is off a touch …

I’ve attempted to note NFP lows (108’28) to last nights opening HIGHS (111’18) as well as what appears to be a relative CALM in / around where long bonds settled after opening pop (~110’14 or about 5tics higher from close)…

… here is a snapshot OF USTs as of 705a:

… HERE is what this shop says be behind the price action overnight…

… WHILE YOU SLEPT

… and for some MORE of the news you can use » The Morning Hark - 9 Oct 2023 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

Before we jump in to the ‘news’, lets have a look at how it was said to be going in the ‘news’ from the WSJ on 9/11

WSJ: Biden Administration Takes Steps to Free Up $6 Billion in Iranian Funds in Prisoner-Swap Deal. U.S. waiver of some Iran sanctions would allow the release of frozen Iranian funds held in South Korea

… A State Department spokesman said Washington will have oversight on when and how the funds are used. “It is longstanding U.S. policy to ensure our sanctions do not prevent food, medicine, and other humanitarian goods and services from flowing to ordinary people, no matter how objectionable their government,” the spokesman said.

That was then and they claimed to have ‘oversight’ … am wondering then how we got from there to here, with a story just written and noted 10/8 (so, less than a month)

WSJ: Iran Helped Plot Attack on Israel Over Several Weeks. The Islamic Revolutionary Guard Corps gave the final go-ahead last Monday in Beirut

Moving from some of the news to some of THE VIEWS you might be able to use…in addition TO an updated WEEKLY compilation (noted over the weekend), here’s SOME of what Global Wall St is sayin’ (in a similar sorta way you’ll find content if you pay for ZH PREMIUM? except … they are SELLIN other folks data where as I’m just point it out and links provided — should work IF you have permission and should NOT work if you don’t … HOW can THEY do that?? askin’ for a friend as I never understood how they do it…)

BNP - Oil: Limited impact from conflict but price risks skewed upwards

We believe recent developments in the Middle East add a risk premium to crude prices, given risks of escalation and tighter enforcement of Iranian sanctions.

However, we consider the impact to remain limited unless there is a significant escalation. Key signposts in this respect would be the narrative on Iran’s involvement; tightening of sanctions enforcement on Iranian flows; and escalation of hostilities to neighbouring regions.

DB - Stagflation in the 1970s: Is history repeating itself in the 2020s?

This month marks 50 years since the 1973 oil shock. Although many events were responsible for the stagflation of the 1970s, that oil shock was arguably the single biggest event in perpetuating those conditions. It sent much of the Western world into recession, and it took many years before price stability returned.

As we look back at the 1970s today, there are a striking number of parallels with our own time: inflation remains above target across the major economies; we have witnessed severe spikes in energy prices over recent years; and there’s been growing industrial unrest. Over the weekend, the attacks on Israel showed how geopolitical risk can return unexpectedly. And we are also seeing an El Niño event this year, which echoes a similar event in the early 1970s that put upward pressure on food prices.

We published separate reports on the 1970s back in 2021 and 2022. Since then, there have been several positive signs that we aren’t heading back for a repeat of that decade. For instance, central banks have launched their biggest series of rate hikes in a generation, most of the post-pandemic supply chains issues have been resolved, and there’s been a substantial fall in commodity prices over the last year.

But now is not a time to get complacent and there are very strong reasons for caution. Inflation is still above target in every G7 country, and the 1970s showed how unexpected shocks could rapidly send inflation higher once again. History also suggests that the last phase of returning inflation to target is the hardest. And given inflation has already been above target for the last two years, a fresh inflationary spike could well lead expectations to become unanchored…

… Conclusion Over the past 18 months, there have been a lot of promising signs that a return to the 1970s can be avoided. We've seen central banks deliver the fastest cycle of rate hikes in a generation. On the supply side, the post-pandemic supply-chain issues have broadly healed and commodity prices have come down noticeably from their peaks. Meanwhile, both consumer and market-based expectations of inflation remain impressively well-anchored.

But for the time being at least, it is too early to sound the all clear. After all, inflation is still above target in every G7 country, even if it has come down from its peak. We saw in the 1970s how fresh shocks can lead to expectations becoming unanchored, particularly if they already follow a period where inflation has been above target. At the same time, growth remains sluggish in several countries, and relative to recent years, policymakers face more constraints when stimulating the economy

Goldilocks - The Risks of a Higher Rate Regime (risks are all significant alone but not large enough to trigger recession … unless they all hit together … )

Interest rates have risen across the curve in recent months even as the hiking cycle has increasingly looked finished. Rates have risen moderately at the front end as it has become less clear whether falling inflation will be enough to prompt cuts anytime soon. And rates have risen sharply further out the curve as investors have inferred from the economy’s strong performance at a 5%+ fed funds rate that the neutral or equilibrium interest rate might be much higher than was widely assumed last cycle, when markets embraced the secular stagnation hypothesis.

The main implication of the further tightening in financial conditions led by rising rates is that the drag on GDP growth will last longer. We now estimate a roughly -½pp hit to growth over the next year, meaningful but much less than last year and too small to threaten recession.

The move to a higher rate regime poses other risks too. Last cycle, the belief that real rates would remain close to zero in the future helped to rationalize a few major economic trends that would otherwise have looked more questionable: elevated valuations of risky assets in financial markets, the surprising survival of persistently unprofitable firms in the corporate sector, and wide deficits that added to an already historically large federal debt in the public sector. We explore what the economic consequences might be if these trends were to begin to unwind…

… We think it is unlikely that concern about debt sustainability will lead to a deficit reduction agreement anytime soon. But if it does happen eventually, an agreement similar in magnitude to the 1993 fiscal adjustment would imply a hit to GDP growth in the neighborhood of as much as ½pp per year for a number of years.

While these risks are significant, they are probably not large enough individually to trigger a recession unless they occur abruptly and aggressively or simultaneously. And in those scenarios, we think that the Fed would likely deliver rate cuts that would offset much of the impact….

Goldilocks - Oil Comment: Early Thoughts on Potential Oil Market Effects from Attacks in Israel (both of which I think I could have figured out on my very own…)

Recognizing the elevated uncertainty and incomplete information at this early stage, we note that there has been no impact to current global oil production, and that we see as unlikely any immediate large effect on the near-term supply-demand balance and near-term oil inventories, which tend to be the main fundamental driver of oil prices. We thus continue to forecast that the Brent oil price rises from $85/bbl as of Friday to $100/bbl by June 2024. That said, we identify two potential implications of Saturday’s shocking attacks that may weigh on global oil supply over time.

1. Reduced probability of Saudi-Israeli normalization and associated boost to Saudi production…

2. Downside risks to Iranian oil production…

MS - Weekly Warm-up: When Uncertainty Is High, Price Reigns...Which Side Are You On?

Fiscal constraints limit policy response at a time when cyclical risks persist. Market breadth reflects this dynamic as the S&P 500 defends key technical support. We share takeaways from our roundtable with industry analysts, our latest consumer survey and our Dividend Playbook report.

… With the US Treasury in the process of issuing close to $2T in new supply in the second half of the year, the bond market has taken notice and demanded a higher rate of return to fund that issuance. While front end interest rates have been generally stable over the past several months on the expectation the Fed is close to ending its rate hikes, the longer end of the Treasury market continues to trade poorly with 10-year yields hovering near 5%. With inflation expectations relatively stable and economic growth showing limited signs of reaccelerating, it appears this move in yields is, in part, related to our earlier question—has the US government pushed the limit of its ability to spend without proper long term fiscal discipline and funding in place?

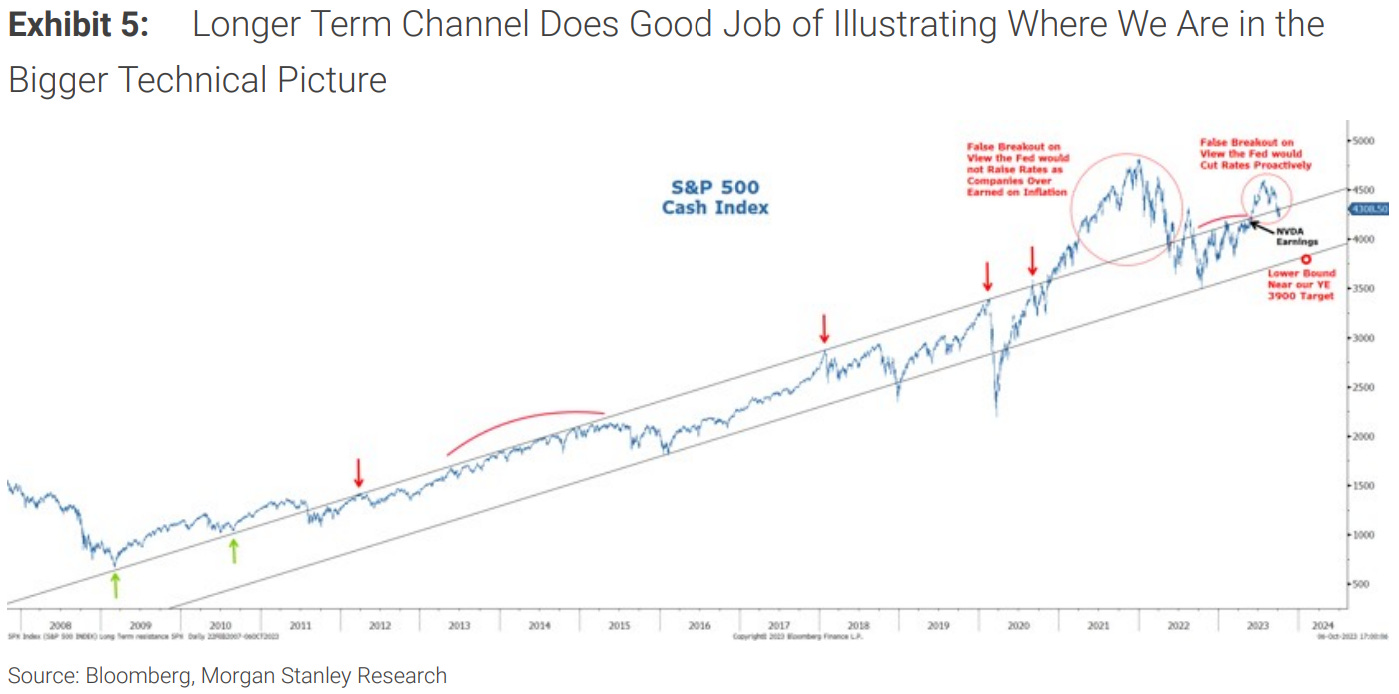

… From a technical perspective, many traders and investors alike have been laser focused on the 200-day moving average as a spot the "market" (i.e., the S&P 500) would likely defend before a 4Q rally commences. This was one of the more consensus calls in recent memory. While the current futures contract broke the 200-day and then was unable to get back above it until Friday's rally, the cash index and rolling futures contract never got there. It's no small coincidence that these levels many were focused on also coincided with the uptrends from October which only further supported the call/view that a move higher off these levels would present the buying opportunity many were expecting; though the context for this move—the hot jobs number—may not be good news in the end because it adds fuel to the higher for longer case. On the other hand, stocks often bottom on bad news assuming this is as elevated as it gets for back-end rates. Once again, it's hard to be definitively conclusive in today's late cycle backdrop, so price action is likely to continue dictating views in the short term.

… The correction of the past few months has been driven by a couple of factors, in our view. First, the Fed may not be done hiking rates but more importantly it's not likely to cut them anytime soon. This 'higher for longer' implication along with the dynamics discussed earlier in the note have fueled the move higher we have seen in rates which has been a headwind for equity valuation. We've also seen some of the mega cap tech winners underperform for this first time this year amid the rate move and as investors digest timelines around AI adoption and the subsequent proximity to revenue/margin/productivity benefits. Finally, consumer cyclicals have experienced a further leg of underperformance amid the recent move higher in gas prices, the exhaustion of excess savings and the resumption of student loan payments. In our view, the combination of higher rates and cyclical uncertainty will continue to weigh on the "market" multiple into year end. We find it instructive that the bottom end of the channel in Exhibit 5 coincides with our year end 3900 price target for the S&P 500.

MS - The Weekly Worldview: Deciphering Inventories (not only hard to measure they are equally EASY to spin however you’d like …)

While Inventories are hard to measure, they are still relevant in the process of deciphering economic slowdowns and accelerations. Globally, inventory cycles are currently asynchronous, which is complicating the outlook.

… What do the data tell us? They suggest that the inventory cycles are asynchronous across regions. The US seems to be in consolidation mode, albeit a mild de-stocking. In the aggregate, inventory-to-sales ratios are a touch above the trend, which when combined with our expectations for slowing in consumer spending in the fourth quarter implies a mildly negative impulse from inventories. The opportunity for a restocking likely only comes in 2024. Meanwhile Europe is still feeling its way around a bottom. Exhibit 1 and Exhibit 3 show just how far Europe has detached from the US and China in this cycle. What is particularly interesting is that the PMI indicator for finished goods (Exhibit 4), shows that it is the US that has de-stocked the most on the manufacturing side…

… What is particularly interesting is that the PMI indicator for finished goods ( Exhibit 4 ), shows that it is the US that has de-stocked the most on the manufacturing side.

Hamas’ attacks in Israel weakened the shekel and increased oil prices. The Bank of Israel pledged to intervene in the foreign exchange markets and provide dollar liquidity to domestic banks. There is little sign of a broad safe-haven bid for the dollar, at this stage. Investors’ concerns about an escalation of the conflict to include Iran have prompted oil price moves.

… And from Global Wall Street inbox TO the WWW,

Hedgeopia - Equity Bulls Put Foot Down, Reflex Rally Due; Potential Catalysts Include 3Q Earnings And 10-Year T-Yield

… In the second half of this August, bond bears (on price) went after the October high at least three times – all unsuccessfully. In September, there were again several attempts. The resistance held firm – until the 21st. The breakout came on the heels of a hawkish message from the Fed post-conclusion of FOMC meeting that Wednesday.

After that breakout, the 10-year continued to rally, tagging 4.89 percent intraday Friday. This was the highest yield since August 2007; back then, the 10-year was on its way down from June’s high of 5.32 percent.

Rates have clearly come a long way, rallying to multi-year highs. Bond bears, who are sitting on boatloads of paper profit, can get tempted to lock in their gains. In fact, they failed to hold on to all of Friday’s gains in yields, closing at 4.78 percent, leaving behind – in a sign of fatigue – a shooting star.

If the 10-year experienced a genuine breakout on the 21st, the next time mid-4.30s get tested, which looks imminent, bond bears should be willing to add to positions. Else, the latest move higher post-4.30s breakout will simply qualify as having resulted from stop orders getting taken out.

Similarly, the vast majority of outstanding mortgages have a locked-in rate that’s lower than the current market rate. So for many consumers, the financing cost of their largest liability has been unchanged.

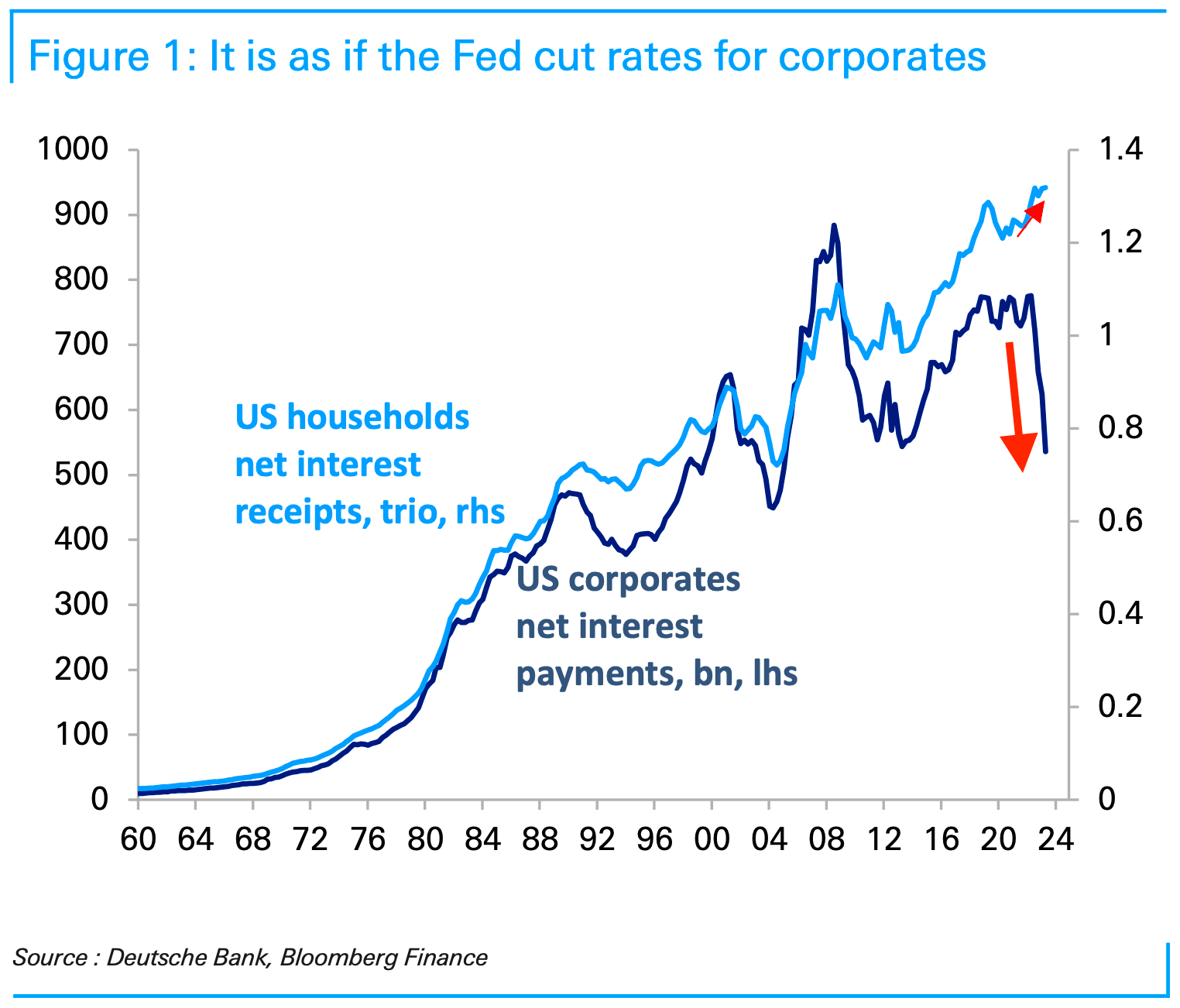

Second, many companies and consumers have quite a bit of cash. And higher interest rates means they’re earning more interest income. From Deutsche Bank’s George Saravelos on Monday:

“… It is effectively as if the Fed cut rates. Why? Because corporates took advantage of QE to term out borrowing at record-low rates and are now earning 5%+ interest on their cash. A similar dynamic can be seen with households: US aggregate household net interest receipts are still where they were before this hiking cycle started as the interest earned on cash has matched payments on borrowings.“

It’s counterintuitive but as Saravelos’ chart shows, the net interest corporations have been paying has actually declined as interest rates have risen thanks to the higher interest income.

… The bottom line: Rising interest rates are currently having a limited negative impact on businesses and consumers as a whole. For many, it’s actually been a net positive.\

https://www.barchart.com/story/news/20948239/2-federal-reserve-officials-say-spike-in-bond-yields-may-allow-central-bank-to-leave-rates-alone

Music to my ears !!!!!!!!!!

Excellent Article !!!

Will be fascinating to watch the FI market's response...Deflationary or Inflationary ???

I believe GAZA, will be changed perhaps forever. It's not feasible to have Hamas living there, any longer.

A complete takeover of GAZA is coming...and I have to support that.

The Palestinians have proven that can't gov't themselves or be a good neighbor.

This was the last straw....times up....

The Palestinians need to find some where else to live.....maybe Iran ???

I won't go into how the Biden Admin has financially supported the terrorist families, that Trump cut off.

I won't go into how Biden has not enforced the Oil Sanctions against Iran...

But the Obama/Biden Policies have been very counterproductive to ME Peace and for the State

of Israel....