while WE slept: 'bonds reel' as '47 hits steel, QUIET (Japanese holiday); "NFIB vs Gravity - The headline index backed off in JAN (102.8 vs 105.1 prior)" -Citi; 10s higher 6 of last 7 Febs -BNP

Overall, small business owners remain optimistic regarding future business conditions, but uncertainty is on the rise. Hiring challenges continue to frustrate Main Street owners as they struggle to find qualified workers to fill their many open positions. Meanwhile, fewer plan capital investments as they prepare for the months ahead.

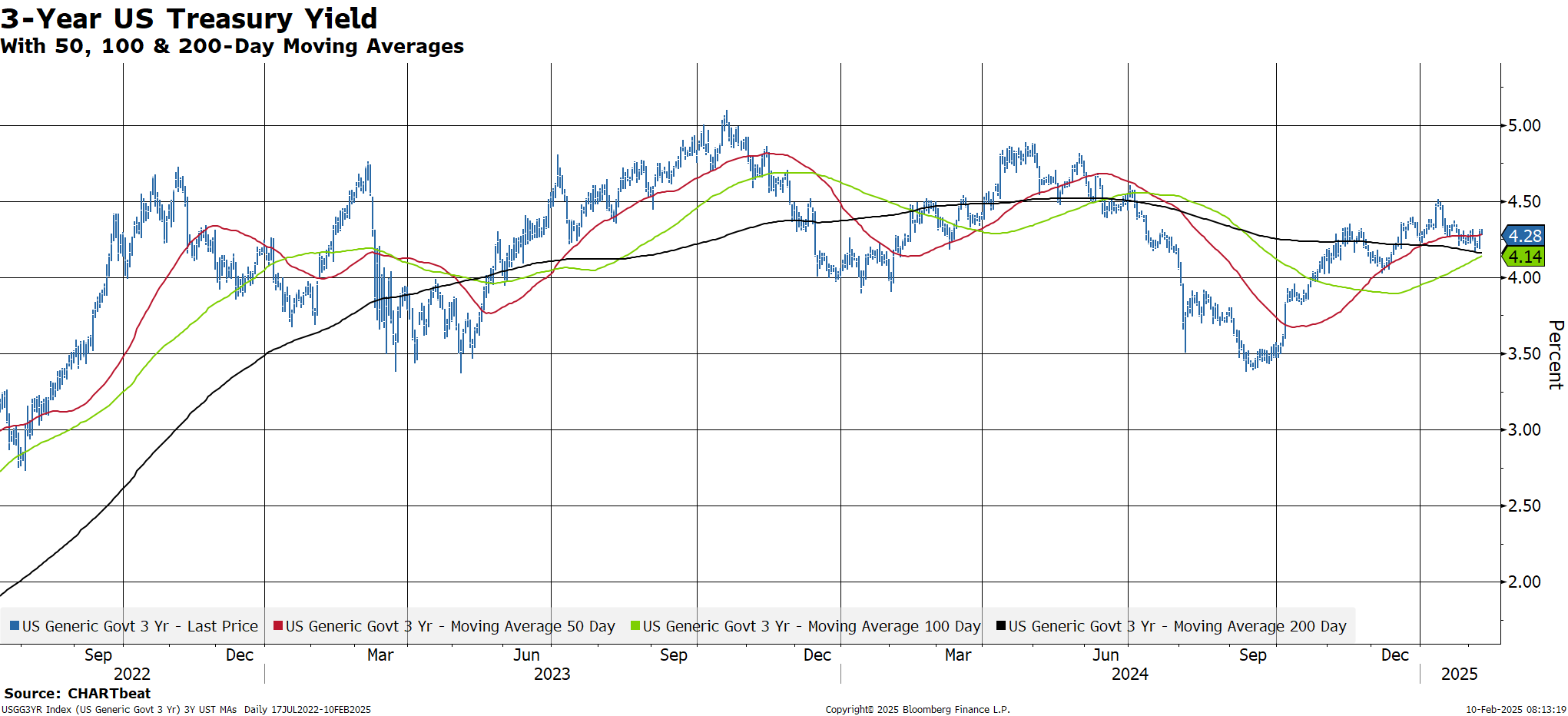

As the dust settles from the (not so)superbowl, there was euphoria despite / because of the newest iteration of ‘47s tariff efforts and oddly enough, ‘most things’ were bought … and with the reFUNding kicking off today with $58bb 3yr notes this afternoon, lets jump in and take a look of ‘most things’ included USTs …

3yy: TLINES, and 50dMA converging in / around 4.30% …

… as the price action for 3yr money converges and triangulates its worth noting DAILY momentum has moved from overBOUGHT to somewhat less so (not yet overSOLD) and a bit more outright concession might help with this afternoons liquidity event

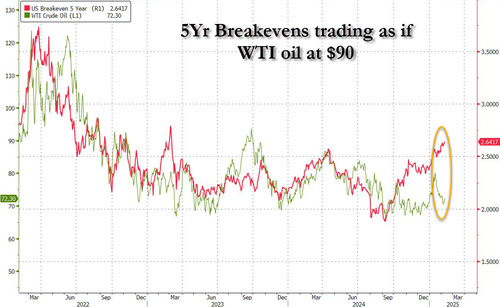

…But, despite the 'normalizing' inflation expectation, breakevens started to breakout - especially at the short-end....

Source: Bloomberg

...at the long-end, Treasury yields are lower, decoupling from the rising BEs...

…...Breakevens imply a $90-plus price...

… here is a snapshot OF USTs as of 720a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are bear-steepening into NY hours with EGB under-performance seen overnight (10y OATs +10bps) after solid French employment figures and heavy supply from the Netherlands, the UK and Italy (and France 30y tomorrow). Tokyo is out on holiday, so lighter volumes are presiding over jumpy moves, with Trump announcing 25% universal metal levies for next month. The desk has seen selling out the curve from CBs and other real$ accounts in 10s-30s. Fast$ accounts continue to express steepening interest in 5s/10s and 5s/30s, and we've also seen some interest in beta-weighted steepeners pre-supply. S&P futures are showing -15pts here at 7am, Crude Oil +1.25%, XAU flat, and DXY flat as well…

… NFIB vs Gravity - The headline index backed off in JAN (102.8 vs 105.1 prior) after a 13.5pt lurch higher from last NOV, on par with the first ‘Trump bump’, worth 11.8pts in the NFIB index in 2016-17. So a bit of mean reversion can be expected as tariff news and volatility in equity markets filters through the data. The hiring index was released early last week and ticked down from 19 to 18. This morning’s update saw the uncertainty index rise 14pts to 100 - the third highest recorded reading - after two months of decline. The net % expecting the economy to improve fell 5pts to a net 47%. Reports of higher nominal sales in the past three months dropped 1pt from December and the net % expecting higher real sales fell 2pts from December’s high-water mark (since JAN 2020) to a net 20%. Holistically, this small business confidence erosion may speak to the weakness already in soft-survey surprises (CESI soft at -3.1 from JAN peak of 35), marking the transition of tariff-related uncertainty from tailwind for hiring and imports to headwind for manufacturing / temp service / public sector employment…

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK: US equity futures & Bonds lower as markets digest Trump tariffs, Fed Chair Powell due … Bonds reel as Trump hits steel, BoE's Bailey and Fed's Powell are set to speak; crude gains whilst metals take a hit … A slightly constrained start to the session on account of a Japanese holiday and as such there was no overnight cash UST trade. Nonetheless, the bias is bearish as participants digest and assess the inflation implications of Trump’s latest measures and commitments to respond from Canada and the EU. Action which has weighed on USTs to a 109-01+ trough, a tick below Monday’s base but just above the 109-01 low from Friday. Trump is set to sign an executive order at 15:00 EST, with commentary via Fed Chair Powell also due at that time.

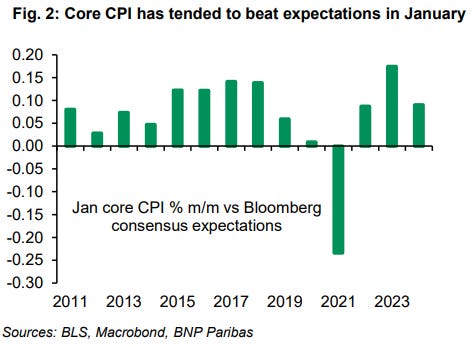

Since the pandemic, US core CPI inflation has consistently run stronger in January–February than in the rest of the year, suggesting ‘residual’ seasonality in the data.

Early-year price hikes may be an adaption to a high-inflation environment – behavior we think is likely persisting in 2025, potentially with some moderation.

While the BLS’ annual model-based seasonal adjustment update may somewhat reduce Q1 strength, the agency has not signaled any intention to update its procedure more forcefully.

We think excess strength in January-February core CPI this year could run at about half the rate seen over 2022-24, and pencil that into our 2025 baseline.

We think early-year residual seasonality has been well flagged to the market, and see risks skewed towards lower 10y yields should the January and February CPI prints surprise to the downside.

…US rates: An unsurprising surprise? Yield impact: With January core inflation consistently beating expectations over the past decade (see Figure 2), February has increasingly, and unsurprisingly, seen rising Treasury yields – 10y yields have been higher in six of the last seven Februaries. We think this likely reflects the heightened focus on inflation over recent years.

No surprises? However, we think there is a good chance that, even with an upside January ‘surprise’, Treasury yields may not rise and the curve may not steepen.

We find that most investors have been preparing for seasonality and have taken heed of comments from Federal Reserve Chair Jerome Powell who noted the risk of residual seasonality affecting upcoming inflation data and encouraged markets to look at 12- month trends rather than each month’s print.

We think the market could react asymmetrically to the 12 February CPI print, and see a risk of lower yields – where an upside print may be viewed as a usual January distortion, but a downside print may be considered good news on inflation, particularly in the context of recent January upside surprises.

Grey swans are events recognized as possible but considered unlikely to materialize: these are not our base-case scenarios, but they would have significant market impacts if they happened.

Here we analyse 10 possible grey swans.

US equities: A tech crash

The Fed: Powell is fired

US Treasuries: A Liz Truss moment

Oil: OPEC+ unity is dissolved

Eurozone economy: GDP grows faster than 2% in 2025

Brazil: Politics drives a bull market

China equities: A flow-driven bull market

US commercial real estate: Losses drive up bank NPLs

Private debt: A first-ever default cycle

US economy: An AI productivity boom

Our analysis covers risks which are positive and negative, macro and micro, covering EM and DM, and ranging across asset classes (including private credit).

The analytical value-add of this note is to quantify what would need to happen for the risks to materialize – a road to the event – and identify related market opportunities.

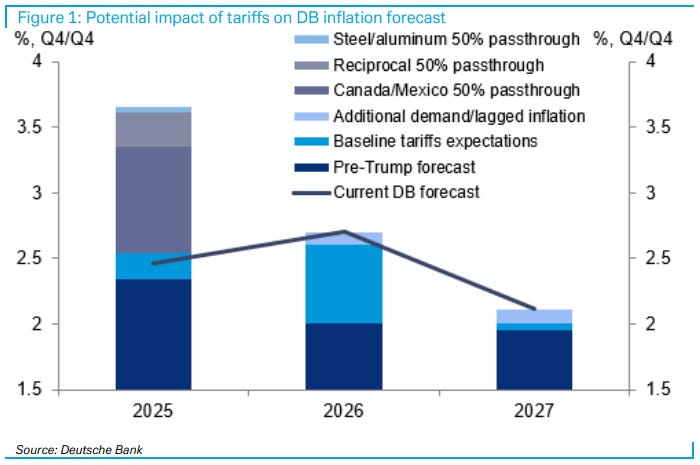

Germany on what steel / aluminum tariffs might mean for firms ‘flation f’casta AND US (vs ROW)equities …

DB: What reciprocal and steel/aluminum tariffs would mean for our inflation forecast

Recent newsflow suggests that the Trump administration is considering “reciprocal” tariffs, as well as a 25% tariff on all steel and aluminum imports.

If sustained, these tariffs could increase core PCE in 2025 by an additional 30-40bps, depending on the ultimate passthrough to consumer prices. If the delayed Canada and Mexico tariffs were to ultimately go into effect as well, inflation in 2025 could be above 3.5%, though the tariffs would have limited impact beyond this year.

These tariffs represent additional upside risks to the inflation outlook for the Fed. While our baseline is that they would prefer to “look through” the price level impact by keeping rates steady, their ability to do so could be constrained if inflation expectations begin to rise and / or the labor market reemerges as an additional source of inflationary pressure. Recent data suggest both these outcomes cannot be fully discounted.

DB: Falling equities could possibly spark some serious outflows from the US

US equities haven't done all that well recently - barely up since the post-election jump, while the equal-weighted index and small caps are actually down a bit. Our colleagues note a few headwinds: tariff headlines, higher rates vol, and elevated positioning (especially in tech), plus there's been the threat from Deepseek. It's possible a ramp-up in headwinds leads to material downside in equities, given the starting point of exceptionally high valuations, both compared to the peer group and the US’s own history (PE of 22x, vs 14x for RoW - Figure 1). What might that mean for the dollar?

It would likely be negative, via the channel of equity outflows (and thus a risk to our bullish dollar view). Foreign investors have amassed huge exposure to US equities over 15 years of marked outperformance (Figure 2). It's true they haven’t bought any additional equities in recent years – net equity flows are around zero (Figure 3). But that’s bullish in an of itself, because usually investors look to re-balance away from outperforming asset classes. That trend is visible across the rest of G10 - UK & New Zealand equities have lagged so they’ve seen firmer flows, while the Nordics are at the other extreme (Figure 4). But the US is the huge outlier - it's odd to have seen no outflows.

With a current account deficit around the important (at least historically) threshold of 4%, equity outflows amounting to even a couple of percent could pose a challenge for the dollar. And that's not a huge size - almost half of G10 has seen something like this over the past year. On the other side, it'd be a great environment for yen, which has tended to benefit from lower equities/lower yields.

Given the unique nature of today's housing market, we turned to Morgan Stanley's AlphaWise to conduct a consumer survey to gather clues on homebuying intentions. We found that affordability challenges remain a hurdle, but lower rates could help.

Key takeaways

46% of our survey respondents are considering buying a home in the next five years, while only 32% of consumers are considering selling.

If mortgage rates fell to 5.5%, 91% of people considering buying in the next 6 months would be more likely to, as would 85% considering over the next 2 years.

Consumer sentiment and reported reaction function support our view of growth in existing home sales in 2025, which we see climbing 5% relative to 2024 levels.

We find a significant relationship between home sales and durables spending; higher sales this year support our call for relatively strong goods consumption.

Elevated home prices and equity have, and should continue to, support spending. Baby Boomers accumulated the most wealth; prices are a hurdle to younger buying.

… The lack of forced selling has kept home prices protected in this cycle, which, combined with stubbornly high mortgage rates, has left affordability close to its most challenged levels in decades (Exhibit 4). The combination of low inventory and affordability pressures has driven turnover in the housing market – defined below as existing home sales as a share of owned inventory – to its lowest levels since 1981 (Exhibit 5).

There’s always an exception to a rule, right? One firm suggestin time to plead for ‘em (and some notes on tariffs and inflation expectations …)

US President Trump stated there will be no exceptions to aggressively taxing US buyers of foreign metals (due to start on 4 March, giving time for US companies to plead for exceptions). If there is no retreat, this will reduce US steel consumers’ competitiveness via higher import and domestic costs (if domestic metal producers raise prices under cover of the tariff). Retail consumers are less likely to notice the tax, unless job losses are explicitly linked to it.

The US January NFIB small business sentiment survey surveys a sample of NFIB members. There may be selection bias as NFIB members might, possibly, skew strongly Republican. That might hint at Republican business owners’ views of various proposed trade tax increases (and the realization that they, not foreigners, would pay)…

…For the US, the economic effects are likely to be small We see very small aggregate economic effects. Even though steel and aluminium are widely used as inputs into production, the total quantities of imports are small relative to the size of the economy. Imports of iron & steel (HST 72) and aluminium (HST 76) were ~$60 billion in 2024, ~1.8% of total imports. If we include articles of iron and steel too (HST 73), this would rise to $109 billion or 3.3% of total imports. As a share of the $29trn US economy, this would be between 0.2-0.4% depending on the breadth of imports covered by the new tariffs, implying a negligible impact on GDP. Instead, the effects could be felt more acutely in those who supply the US — note that Canada is the top supplier of US steel and aluminium imports and Mexico is third. In terms of the potential inflation impacts steel and aluminium imports are ~0.3% of the~$20trn level of nominal PCE and if we assume a 60% pass through, given these imports are intermediate goods, would imply a 7.5bp impact on PCE prices from a 25% tariff (25% x 0.005 x 0.6), with movements in exchange rates potentially reducing the inflationary impact. Given the lack of detail though, these are rough estimates.

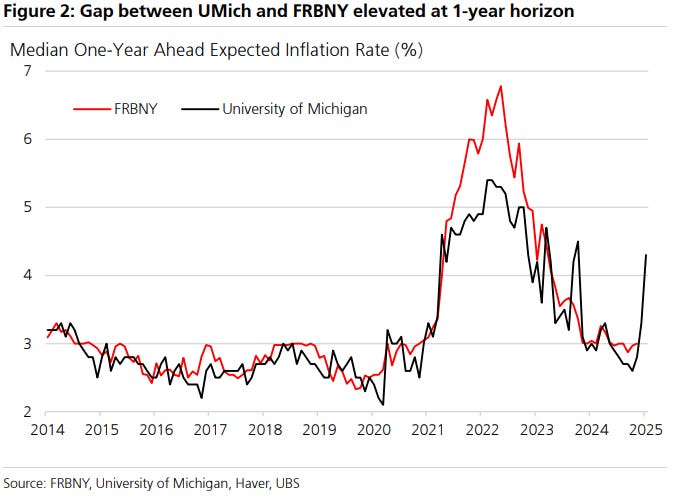

Inflation expectations warrant watching We are all watching inflation expectations for signs of becoming unhinged after the high inflation episode of the pandemic and the recent stickiness in core inflation. The recent tariff threats pose another risk. Plus, FOMC members continue to point to well anchored inflation expectations.

Friday, the University of Michigan survey data's longer-run measure did not do anything different from its behaviour a month ago, but the one-year ahead median inflation expectation jumped. Today, the FRB of New York survey reported the one and three-year ahead median inflation expectation in their Survey of Consumer Expectations were unchanged at 3.0% in January.

…Interestingly, the University of Michigan published a figure showing the rolling 7-day average of year ahead inflation expectations in recent weeks and noted the shift higher particularly around the announcements January 31 of potential tariff on goods imports from Canada, Mexico and China. The difference between the two could potentially be driven by timing differences in the surveys, one picked up the tariff threats and one may not yet have done so. Plus recent spikes in the Michigan measure have tended to fall back toward the FRB of NY measure, but we will know better later this month. Again, this warrants watching as policy announcements from the new administration continue.

Bearish stock market narratives have been pervasive since early 2022. They are becoming more so now with each headline coming out of Washington. Duties, deportations, duties, and de-bureaucratization (the four "Ds") can have a shock-and-awe effect. But financial markets broadly have been unperturbed because the US economy continues to be rock solid.

Then again, reining in the budget deficit and trade deficit is no easy task. President Donald Trump has even acknowledged that the cost of doing so may be some short-term pain. But we remain optimistic on the economy and therefore bullish on the stock market. Notwithstanding all the commotion in Washington, including frequent shifts in fiscal and monetary policies, the US economy's resilience speaks for itself. Currently, we see signs that not only is growth strong but it might be getting stronger.

Here are a few charts to illustrate this point:

(1) Manufacturing. After contracting for nearly the entire post-pandemic period, the ISM M-PMI suggests that the manufacturing sector is starting to expand (chart).

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

An informed VIEW …

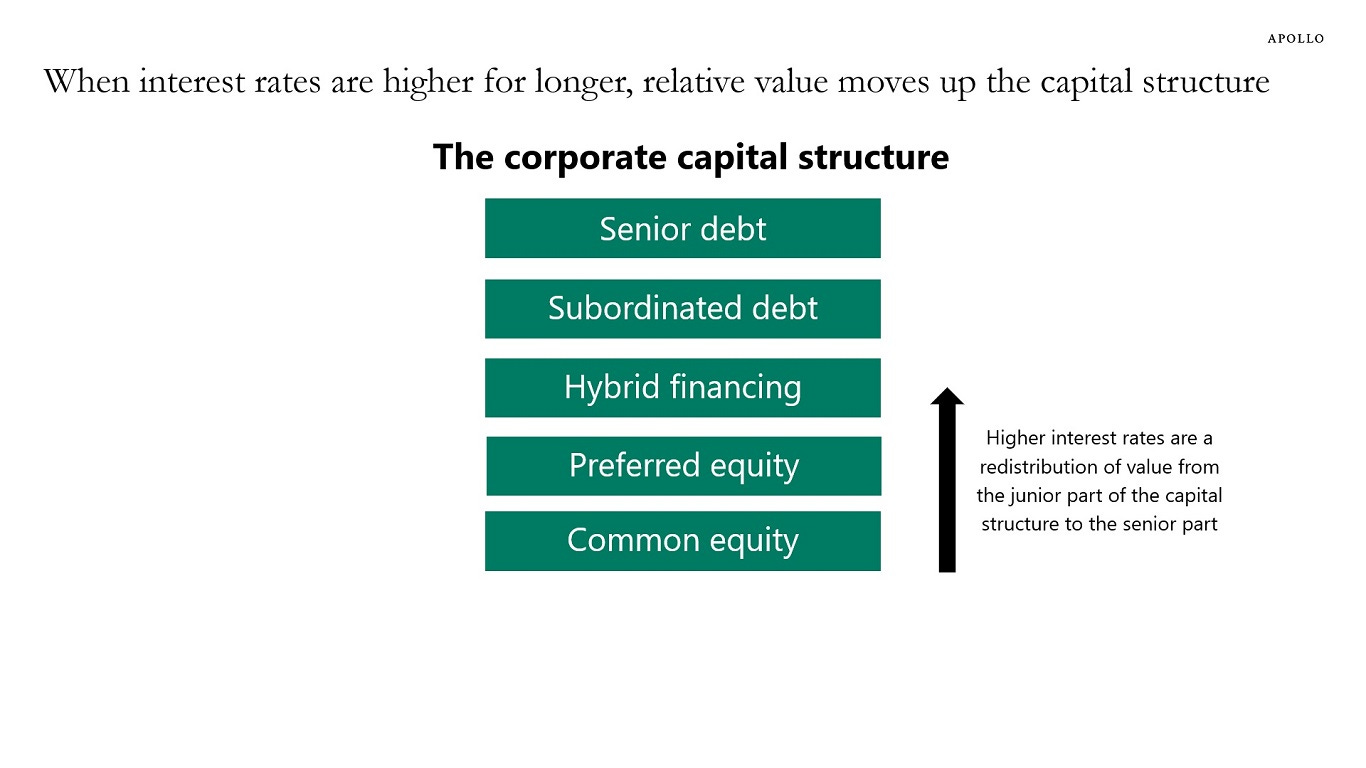

APOLLO: The Impact of Rates Higher for Longer on the Capital Structure

The transmission mechanism of monetary policy works through higher costs of capital that lowers demand for capex and hiring but also raises return requirements for equity to pay the debtholders in the company.

Higher interest rates are a redistribution of value from the junior parts of the capital structure to the senior parts, see chart below. Someone has to pay the higher level of interest rates in corporate capital structures, and it is not the Fed, it is the equity holder.

In short, companies with no earnings, no cash flow, and no revenue will continue to struggle simply because they cannot pay the higher debt servicing costs. In other words, when interest rates are higher for longer, companies with earnings tend to outperform because companies with earnings are able to pay higher debt servicing costs. The purpose with higher interest rates is to slow growth, which makes value more attractive than growth.

In fact, this is the entire idea from the Fed with raising interest rates—to discourage too much risk taking, such as investments in companies and capital structures with no earnings, no revenue, and no cash flow. Examples of unattractive sectors are growth, software, and venture capital.

One for the inner chartEgerists out there …

Hedgopia: Major Equity Indices Draw Sellers At Technical Resistance, Even As Options Market Reflects Intense Bullish Optimism