Good morning … Chiefs lost, Trump wins, announces tariffs and no rest for the weary. A couple links to start the day / week off …

BLOOMBERG: Bond Market Gains Fade as Trump, Inflation Keep Yields High

Treasury supply worries ease, but policy questions persist

Strong labor market, elevated inflation keeping Fed on hold

CNBC: Trump to impose 25% tariffs on steel and aluminum — here are the likely biggest winners and losers

… I’ll skip any further pretense I’ve got something to add to aggressively UNCH bond market with dow FUTURES higher as it was a very late night and always an early morning, so …

… here is a snapshot OF USTs as of 723a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are slightly lower in quiet conditions, even as incremental tariff threats linger. Risk sentiment remains cautiously optimistic however, with S&P futures +27pts here at 7am. The desk has seen demand in intermediates from real$ accounts, helping drive a modest flattening earlier, which is reversing slightly into the US session on a slight increase in volumes. Commodities are bid-up in some inflationary sympathy, Crude +1.6%, Copper +0.8%, and Gold +1.5%, while CAD is -0.4%, and AUD flat.

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWKUS Market Open: Trump to announce 25% aluminium and steel tariffs; stocks gain and XAU makes a fresh ATH … USTs are flat, Bunds are a touch higher as tariff threat concerns weighs on the EZ outlook … USTs are essentially flat and with price action rangebound thus far, trading within a very narrow 109-02+ to 109-09 range; markets are digesting the jobs report on Friday as well as fresh tariff announcements from President Trump regarding 25% levies on all steel and aluminium coming into the US (more details on Monday). Today's docket sees the release of US employment trends and NY SCE.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

This note was one I thought would be delivered during the snow clean up (perpahps before) but was actually delivered AFTER the big game … still worth a look …

The sustained pickup in US labor demand suggests that Fed monetary policy is not restrictive. If this trend continues, we think it would significantly increase the risk of the FOMC needing to hike rates this year.

Our tariff framework suggests South Korea, Japan and Thailand as countries that Trump may target next.

We are well above consensus on the inflationary impact of tariffs and added a 2s10s flattener to our portfolio.

Good thing AFTER the BIG game, it’s USUALLY quiet …

The week after payrolls is usually quiet but due to the first Friday of the month being the latest it could possibly be this month, then we bump straight into US CPI (Wednesday) week, with PPI (Thursday) for an added bit of inflationary sparkle. Outside of this the main highlight will be Powell's semi-annual monetary policy testimony before the Senate Banking Committee (tomorrow) and the House Financial Services Committee (Wednesday). The latter comes after CPI which will possibly spread the interest level over the two appearances rather than most of the focus being on the first as per usual. Elsewhere in the US, watch out for the NY Fed inflation expectations series today after a stronger equivalent from the University of Michighan survey just before the weekend on Friday. After that we wait until this Friday for the other important US data, namely retail sales and industrial production…

Ever wonder what happened 25yrs ago?

DB: Mapping Markets: How did the dot com bubble burst? The definitive guide

Given the relentless rally in tech stocks over the last couple of years, there’s been a lot of parallels made with the dot com bubble, which grew rapidly in the late-1990s before bursting in early 2000.

With 25 years having passed since the bubble burst, we’re conscious that the events of that period took place before the careers of most market participants today. So we’ve put together this report running through what happened. The focus is mainly on how the selling played out and what caused the bubble to deflate.

Looking back, the most striking feature is that the initial selloff had no obvious driver. Once the selling began, it simply led to more selling, just like many bubbles through history. That's different to the other big selloffs of recent times, which were driven by a key shock, e.g. Covid in 2020 or bank failures in 2008.

From today’s vantage point, it’s also clear there are several key differences with today. First, the NASDAQ’s ascent was much more rapid before the dot com bubble burst and, by its peak, the index had more than doubled over the previous year. Second, it deflated incredibly fast, with the NASDAQ down by over a third in little more than a month. And third, the dot com bubble burst into a wider economic downturn, culminating in a recession in 2001, unlike the broadly positive macro backdrop of steady growth we’re currently experiencing…

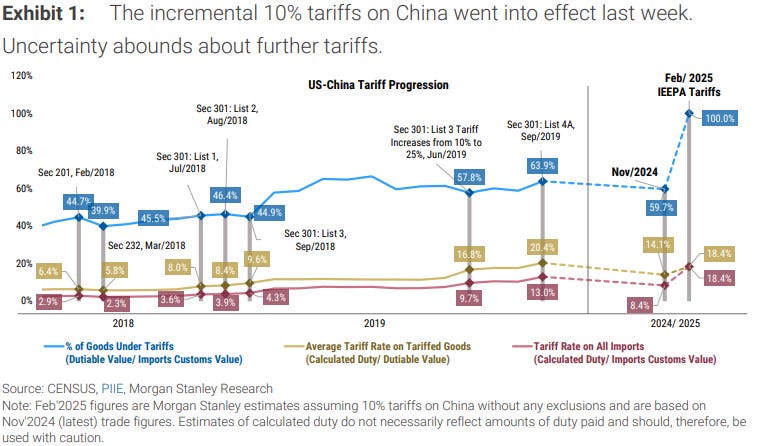

Tariff Man cometh backeth … providing narrative creators ample resources and plenty of job security …

MS Sunday Start | What's Next in Global Macro: Tariff Man and the Multipolar Plan

Tariff tactics matter, but don’t let them distract you from the larger strategic theme. Investors spent much of last week gripped by the “will he, won’t he” of whether President Trump would follow through with new tariffs. Friday’s news reintroduced the possibility of reciprocal tariffs, which he said would be announced next week. Earlier in the week, the US increased tariffs on China though tariffs on Mexico and Canada were avoided, at least for now. So far it’s lining up with our expectation for the US tariff path coming into the year: Tariffs on China and on key products out of Europe would go up gradually, consistent with US policy focused on supply chain security and reducing trade deficits. But it would be naive to deny that many paths from here, both more benign and severe, are possible….

…In fixed income markets, the pressure of this transition on growth that our economists cite is one key reason why US Treasury yields could buck the consensus for higher yields and move lower into year-end, as my colleague Matt Hornbach argues…

And on topic, given what’s occurred over past 24-48hrs …

The Global Macro Strategy team shares observations about rates and FX markets from Friday, January 31 through Monday, February 3. We learned that the marginal investor thinks tariffs raise near-term inflation, hurt real growth, and ultimately hurt nominal growth because they tie the Fed's hands.

Key takeaways

In rates, the repricing to a less dovish near-term Fed policy path occurred with a more dovish repricing of the trough policy rate – flattening the yield curve.

In G10 FX, GBP is finding a home as an issue-specific safe haven. JPY is the best haven against tariff threats and has emerged as an important asymmetric long.

In EM, Mexico appears to have a lot in the price already. The tariff impact would have been very negative, but Mexico performed in line with other EM markets.

Same shop with an equity note on week ahead …

MS US Equity Strategy: Weekly Warm-up: We Address Key Questions Around Tariffs, AI Adoption and Rates

Investors are focused on tariffs, AI adoption and back-end rates. We address key debates in the market, introduce a new industry framework focused on potential tariff exposure and highlight our top trade ideas—Long Quality, Financials, Software and Consumer Services over Consumer Goods.

The past week highlighted the uncertain outlook for policy. Tariffs on imports from China, Mexico, and Canada were announced, only to have tariffs on the latter two countries postponed for a month. Asset prices—especially equities and the dollar—did round trips as markets digested the news…

…For the US, we are anchored to the data, but the fact of earlier tariffs on China and greater risks led us to change our view to only one rate cut from the Fed this year. We see the Fed as inclined to cut rates very gradually so long as inflation trends down convincingly, and our forecasts for inflation have continued disinflation. We had thought two cuts in the first half of the year were possible. But in December, the Committee saw inflation risks as skewed to the upside, and the reality of the tariffs probably increases the upside risk for the Fed. So, we think the burden of proof for disinflation in the data is higher. In our forecast, the 12-month change in core PCE inflation will fall by almost a half percentage point by May. That amount of disinflation should be sufficient to overcome the doubt, leading to a cut in June. A cut in May is still possible, especially if there is no further escalation in tariffs and if the inflation data surprise to the downside, but the Fed’s caution has risen…

…What has not changed is our view that permanent tariffs on China will ramp to 60% by the beginning of 2026. And because almost 2/3 of US imports from China are capital goods or intermediate goods that go into manufacturing, we expect that escalation of tariffs to induce meaningful slowing in the US economy into next year. Consequently, the rate cuts that the Fed puts off this year, will likely come back late next year.

US President Trump has stated that tariffs on the EU are coming "pretty soon". We discuss what tariffs could be coming and the impact on the European economy and the EUR.

Key takeaways

Our base case includes gradual, targeted tariffs on the EU later in 2025, preceded by a reinstatement of the Sec. 232 steel and aluminum tariffs.

The overall economic impact will depend on how the EU responds. On that front, we think 2018 provides a good template.

We estimate that a general 10% US tariff on EU exports would lower European growth by 30bp to 60bp. We see the ECB cutting to 1% by 2026 in any case.

In FX Strategy, we still recommend long EUR/USD positions and think it could rise to 1.08 if tariff implementation is avoided or delayed after negotiations.

That said, we don't think enough risk premium is priced in EUR/USD for an adverse tariff scenario and think EUR/USD could test parity should this materialise.

US President Trump (temporarily) retreated from ending de minimis tariff exemptions. De minimis rules mean US consumers do not pay trade taxes on imports worth less than USD 800. This, alongside retreats from taxing Colombian, Mexican, and Canadian goods, emphasizes trade tax visibility. Consumers would notice the cost of these tariffs (affecting food and fuel prices, or the price of purchases from Temu), and would quickly realize that US consumers, not foreigners, pay tariffs. Highly visible tariffs lead to a quick retreat.

Taxing steel and aluminum is less visible to end-consumers. Taxing (bulk) imports from China is also less visible (imports from China tend to fall in price, so tariffs may mean less deflation, not price increases). Trade taxes in these areas are likely to be more enduring. They are still economically negative (a tax is a tax), but there are potentially fewer second-round effects…

…Trump suggested mega-donor Musk had found irregularities with “Treasuries”. Treasury officials clarified the US president’s apparent confusion, saying it referenced payments made by the Treasury not bonds.

The major stock market indexes are still up since Election Day despite recent turbulence caused by DeepSeek and Trump Tariffs 2.0 (chart). The former is weighing on the shares of AI companies. However, cloud giants Amazon, Microsoft, and Google remain committed to spending record sums this year to build out their AI capacity. Asked last week about the AI cost efficiencies represented by DeepSeek’s widely followed advances, Amazon CEO Andy Jassy echoed the sentiments of other tech leaders in saying that he expects the trend to increase overall AI demand.

Trump Tariffs 2.0 hit the stock market hard on Friday after President Donald Trump said he plans to announce reciprocal tariffs on many countries by Monday or Tuesday of this coming week, a major escalation of his offensive to tear up and reshape global trade relationships in the America's favor.

We view this as a positive development given that Trump previously planned to impose a uniform 10%-20% tariff on all US imports. The reciprocal approach leaves plenty of room for the US to negotiate tariff cuts with each of America's trading partners separately. They're Trump's "art of the tariff" deals!

Trump's reciprocal tariff threat also spooked the bond market on Friday (chart). That's because higher tariffs would cause at least a one-time spike in consumer prices which might trigger a renewed inflation cycle. Another possible reason for the backup in the bond yield on Friday is that the Bond Vigilantes figure that Trump's reciprocal approach to tariffs suggests that he may be abandoning the idea of a uniform tariff aimed at raising revenues.

The focus of the economic week ahead will be inflation. Businesses tend to raise prices at the beginning of the year; that could result in January CPI and PPI releases (Wed and Thu) that are hotter than expected even though both are seasonally adjusted. A few Fed officials recently worried out loud that tariffs could interrupt the progress toward the Fed's 2.0% inflation target. We expect Trump 2.0 will generate more noise than signal in the upcoming inflation news, as the economy is buffeted by four “D”s: deregulation, deportations, duties, and de-bureaucratization.

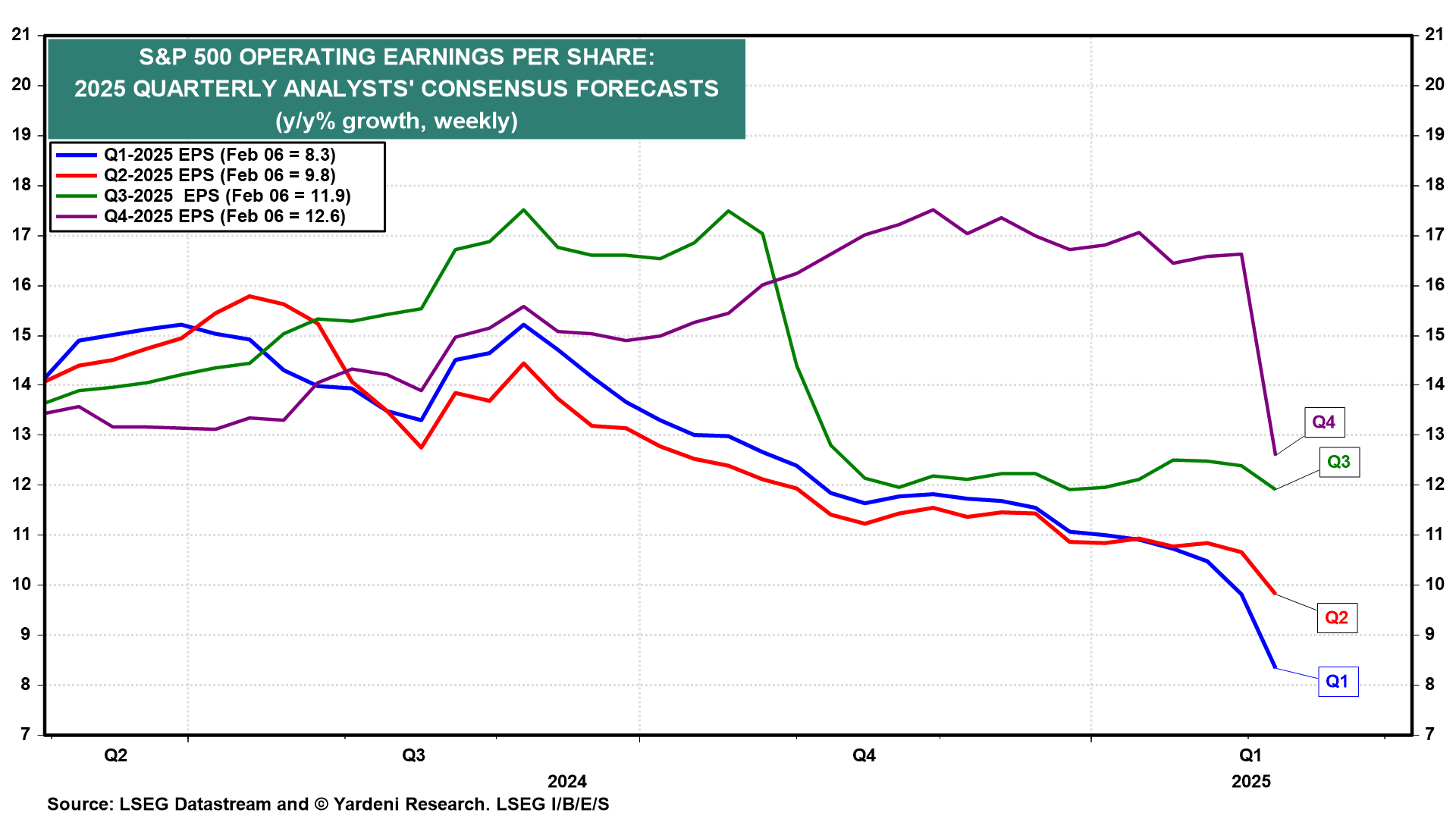

We believe that the economy's stellar performance will continue notwithstanding all the commotion coming out of Washington. On that note, Q4's earnings season is shaping up to beat even our very bullish expectations of 12.0% y/y EPS growth. Analysts entered earnings season expecting 8.2% y/y EPS growth; after big-tech earnings reports, that's now 13.3% (chart).

On the other hand, analysts have been very quick to get pessimistic on 2025 earnings growth (chart). We think they are overcompensating in reaction to either tariff worries or a possible slowdown in the Magnificent-7’s capital spending, or both. We're expecting Q1 EPS growth of at least 10.0% y/y.

While the economy has been doing very well, this week's data might suggest it is cooling. Retail sales and industrial production (both Fri) are likely to slow from December’s growth rates. We caution against interpreting this as a reaction to Trump 2.0 or the start of a broad-based slowdown, but we recognize that it may weigh on stock prices while boosting bond prices.

Here's more:

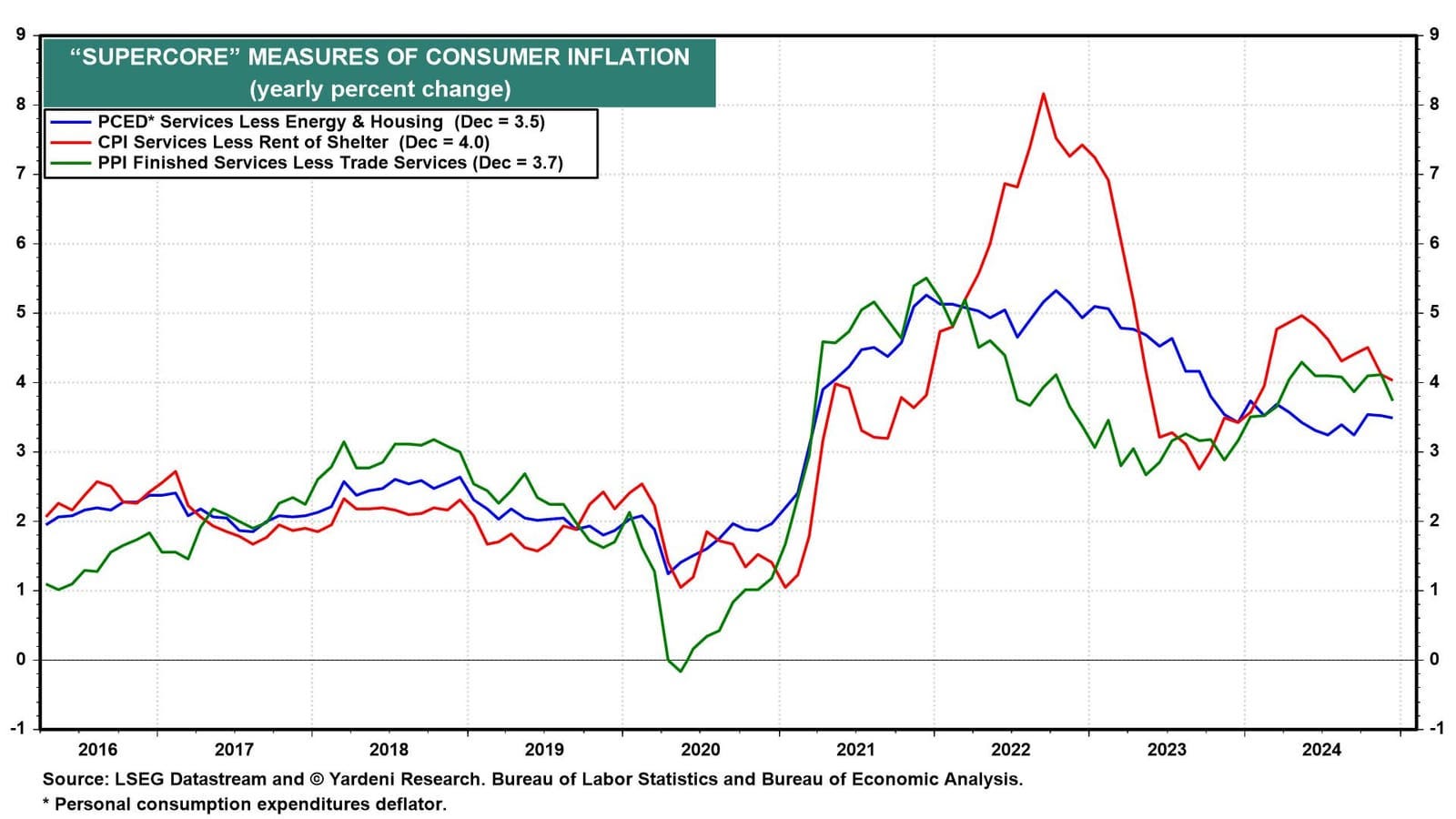

(1) Inflation. The Cleveland Fed's Inflation Nowcast projects January's headline and core CPI (Tue) rose 0.24% and 0.27% m/m, respectively. That would put the y/y readings at 2.85% and 3.10%. We're watching supercore (core services ex-housing) in both the CPI and PPI (chart). A continued deceleration would likely lower bond yields and boost stock prices. A reversal in last month's progress would likely have the opposite effect.

(2) Expected inflation. January's New York Fed consumer survey (Mon) will likely show inflation expectations are rising, ostensibly due to tariff worries, just as the University of Michigan's survey did last week (chart). That said, essentially all of the increase was due to respondents who identify as Democrats, whereas Republicans' expectations fell. Partisanship is infecting these consumer surveys and, along with low response rates, may be rendering them less useful.

(3) Small businesses. December's NFIB Small Business Survey showed owners are very bullish on Trump 2.0, expecting sales to increase and raising their plans to hire and invest (chart). January's survey (Tue) is likely to be a bit less upbeat on tariff worries.

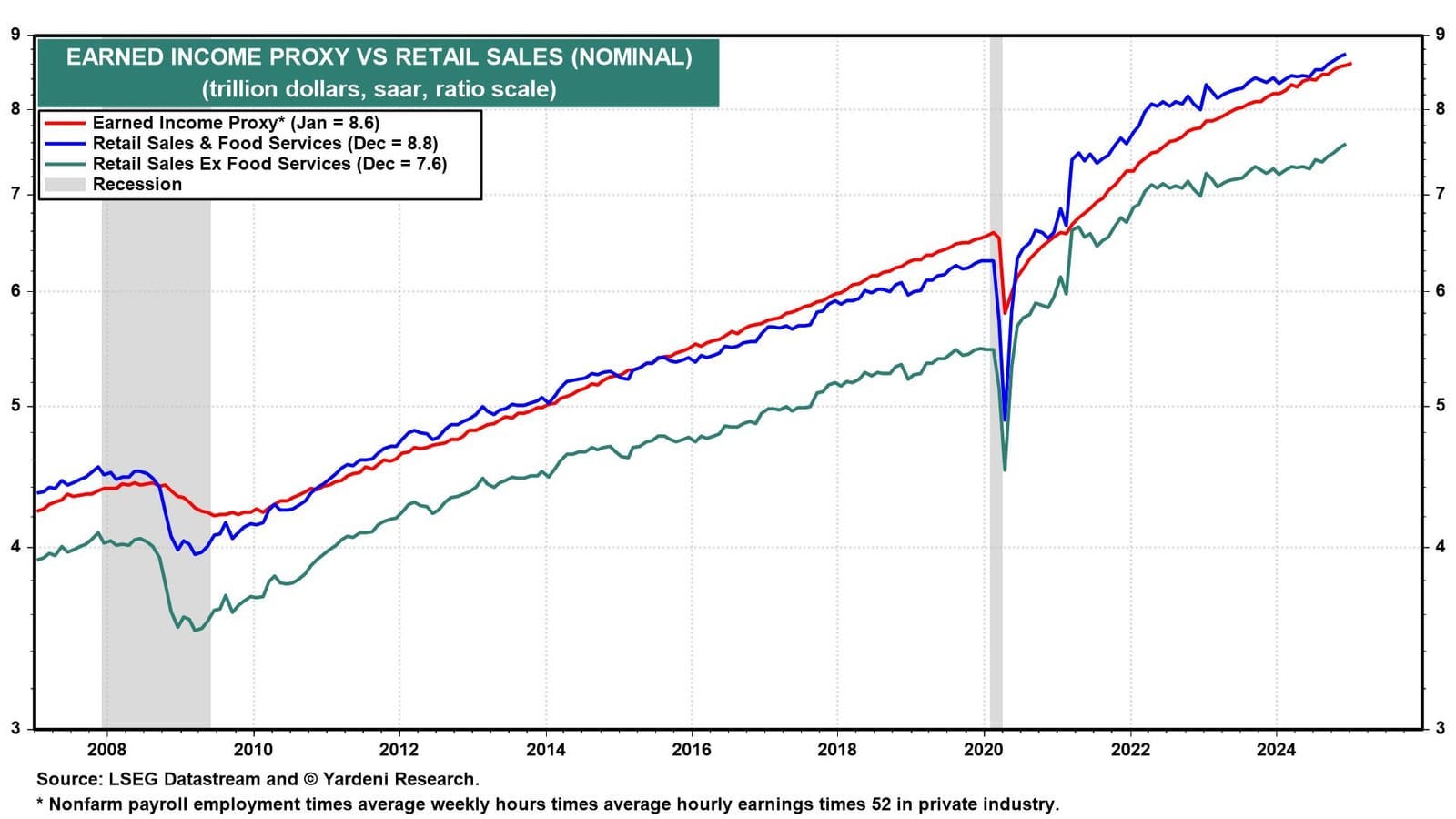

(4) Retail sales. Our Earned Income Proxy rose 0.3% m/m in January. We're expecting real retail sales rose around 0.2% m/m, as the California fires may have reduced hours worked in the economy but not actually dented consumer spending much (chart).

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

First up from The Terminal, a view (with couple interesting graphics) …

BLOOMBERG: Trump Derangement Syndrome comes for the US consumer

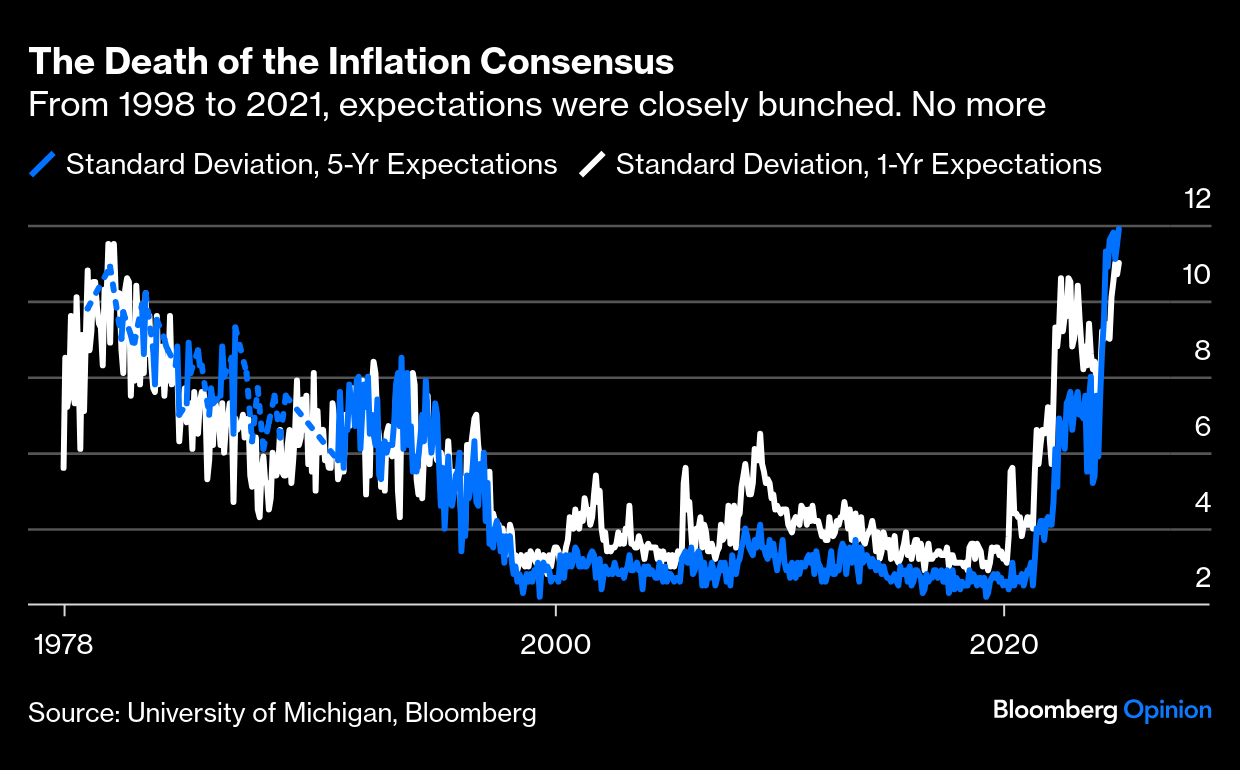

…Partisanship is probably the principal factor behind the total breakdown in consensus among consumers. Michigan has recorded the standard deviation — the basic statistical unit for measuring how much a variable wandersfrom its mean — since 1978. On this measure, views have never been so dispersed, even in the late 1970s when high inflation made the full range of possibilities look much wider:

With bifurcation like this, can we gauge expectations at all? Logically, expectations matter; it’s one of the things on which monetarists and Keynesians agree. If people expect higher inflation in future, they will buy more now, and negotiate far more aggressively for wage rises. That will tend to make inflation a self-fulfilling prophecy. But are expectations so clear-cut that they act as a discrete driving force, and should monetary policy aim to contain them? In 2021, the Fed economist Jeremy Rudd published a paper on whether expectations matter, and if we should care about them. His answer appeared to be “no”: The belief that expectations were a key determinant of inflation, he said, “rests on extremely shaky foundations, and a case is made that adhering to it uncritically could easily lead to serious policy errors.”…

…Consumer Resilience Isn’t Eternal Amid the talk of sentiment and expectations, the reality of a distressed consumer doesn’t get enough attention. Last December, US consumer debt outstanding unexpectedly surged by the most on record, reflecting massive increases in credit-card balances and non-revolving credit, according to the Fed. Total credit, which is not inflation-adjusted, shot up $40.8 billion following a revised $5.4 billion decrease a month earlier. Both revolving and non-revolving credit advanced:

These visible signs of stress justify consumers’ concern about tariffs and their impact on inflation. A recent study by the Tax Foundation estimates that the average household may pay over $800 in taxes if the initial tariffs imposed on Canada, Mexico, and China are permanently placed through 2034. In several instances, tariffs have raised prices and reduced output and employment, producing a net negative impact for the US. Ultimately, such an outcome would traduce Trump’s Make America Great Again mandate. Or does the end really justify means? As Gavekal Research’s Thomas Gatley explains, Trump seems less interested in reshaping global supply chains than in securing political victories and public attention. Yet a world of constantly threatened US tariffs is still a different one.

For now, a resilient labor market is buoying consumers. January’s jobs report pointing to a slight dip gave little reason for concern given recent wildfires and snow storms. Meanwhile, upward revisions to the previous two months showed resilience. Bank of America’s Shruti Mishra argues that the consumer fundamentals are robust with the three-, six- and 12-month nonfarm payrolls averages all showing steady, and possibly increasing, job growth which “bolsters our confidence that the Fed cutting cycle is over.”

With inflation also stuck above target (and expectations in the University of Michigan survey uncomfortably elevated), we see much more evidence of a higher neutral rate, and much less need to cut further.

Powell has admitted that elevated inflation has little to do with the labor market, and Wednesday’s CPI print provides further evidence of how much of a fight the central bank has to put up. One aspect of the report is very unwelcome — wage growth is rising again, and remains well above pre-pandemic levels; great for workers, but not for central bankers:

AND finally, an astute observation from the BIG game …

Appreciate it!