while WE slept: bonds rangebound ahead of confidence, supply and DESPITE Daly; BBB-3m TBILLS FLAT -DB; "On track for a soft landing" -UBS; "Deciphering the Disinflation Process" -FRBNY; bonds cheap

Good morning … Mary Daly (FOMC voting member)of the FRBSF made some comments late yesterday which apparently helped supply a bid for bonds …

RTRS: Fed's Daly: inflation not the only risk, policy must 'exhibit care'

… Reducing inflation further will likely require restraining demand, she said, and while so far the unemployment rate - now 4% - remains below long-run sustainable levels, "future labor market slowing could translate into higher unemployment." To avoid that, she said, the Fed must be both "vigilant and open."

… these comments also served to rob the bond market of what little concession might have been available, making this afternoons ‘liquidity event’ somewhat more challenging …

2yy: overBOUGHT and a touch HIGHER - concession - despite Daly

not unlike chart of 10yy (YEST), 2s are nearly in middle of this years trading range with momentum moving slowly from overBOUGHT to … less overbought and as is always the case, this can occur with yields moving higher and / or simply time at a price … this is what is happening at the moment …

… and while there were / are some curve machinations, it’s all quite contained and so I’ll skip ahead TO a snapshot OF USTs as of 630a:

(once again, didn’t feel like waiting for any on Global Wall especially not when I’ve little to add and markets are aggressively UNCH) … and SO, for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: NQ leads as NVDA gains pre-market, USD/USTs flat ahead of US supply, data & Fed speak … Bonds are contained awaiting impetus from US data and a 2yr auction … USTs are rangebound and essentially unchanged ahead of survey data, June's Consumer Confidence and then the beginning of the week's supply docket with a USD 69bln 2yr sale. USTs currently sits around 110-18.

The bond rally into end 23 forced us to become more tactical since our YA. We trade the 4-4.5% 10y UST range on the long side

We tweak our global rate forecasts. We are still bullish EUR rates, short UK real yields & expect higher JGB yield

We also provide updates on the front-end, spreads, inflation and volatility across regions.

… US Moderation ≠ meltdown, fade rate extremes

… Macro lessons learned in 1H '24: COVID catch up near done: the US economy appears in the late stages of post COVID normalization; US hiring is moderating, esp. in biggest catch-up sectors (i.e. healthcare). US inflation has eased: it will take a few more cool prints to start Fed cuts. Elections matter: French elections impacted EU stability / integration expectations, EM elections impacted carry trades, the US election could impact macro. US election: sweep => fiscal easing => higher rates, divided => stable / lower.

Rate lessons learned in 1H '24: Buy the dip: if Fed not hiking, we think investors should be dip buying. Since the '24 year ahead we had 2 recommendations to go long the 5y to fade sharp rate selloffs; clients should fade extremes. Duration is easier trade vs curve: the US curve has a high bar to out-steepen forwards; it requires a very well-timed call on either rapid Fed cuts or elusive bear steepening. Demand Qs persist: our cautiously optimistic view on UST demand in '24 was validated but large supply coming; we expect additional long end UST cheapening with supply / demand questions. Funding vol on rise: supply & dealer constraints => 2H '24 funding pressure. It should stabilize in 1H '25.

We translate these core lessons learned into our base case rate views for 2H '24:

Duration = trade 4-4.5% 5-10y rate rage tactically from the long side, add exposure >=4.5% & lighten exposure <=4%. Near term risks skew to lower rates as macro activity & inflation data moderate. We note: economic moderation ≠ economic meltdown. The labor market remains tight & higher end consumer may offset lower end consumer pullback. US 10y back to 3-3.5% or lower likely requires a Fed cutting down to 2-3% & U3 rate >=5%. We see this as unlikely near term…

…Bottom line: we hold our core views into 2H '24 = buy the dip in rates and fade any extreme rally, stay neutral on the curve, stay long 30Y B/ E but hedge with 1y1y inflation short, short 30Y swap spreads, and position for a steeper vol curve.

…Meanwhile in the US, a late rally saw the 10yr Treasury yield close -2.4bps lower on the day at 4.23% where it's stayed in Asia this morning. The rally was helped along by dovish-leaning comments from San Francisco Fed President Daly, who said that “Future labor market slowing could translate into higher unemployment”, adding “At this point, inflation is not the only risk we face”…

DB: Monthly Chartbook: Charts to make you go WOW! (one caught MY eye)

This chart book aims to make you think "WOW!!" as you look through many of the charts.

To ensure it's not a random series of charts we've structured it around a weaving narrative.

We start by looking at the most astonishing large-cap equity market rise in history, namely Nvidia. Never has the overall market been so exposed to the performance of one stock. We then expand this analysis to the wider tech sector and the Mag-7 more generally. In recent months it's hard to underestimate the impact this very concentrated rise has had on financial conditions. Given how tough it is to value companies battling for supremacy in AI, especially with most of the spoils well into the future, this does make the macro world a high beta play on the Mag-7. That creates opportunities and risks in both directions.

We then look optimistically on AI from a societal and productivity point of view, and highlight how such gains are desperately needed given the huge problems we have with debt ratios, deficits and demographics. On a similar theme, we also show how many countries have been, or will soon be, relying on migration to ensure their populations don't fall. Incredibly, Germany has had a higher death than birth rate every year since 1972. Given the current political sensitivity to migration across many countries, this is a theme that’s likely to stay in the spotlight over the years ahead.

…Meanwhile, US credit is as sanguine as it has been in history. Over the last 100 plus years, BBB yields have rarely been as low relative to T-bills. The curve is almost flat.

The final segue moves into housing, where years of under investment in the volume of the housing stock is causing its own problem in terms of valuation and affordability.

… San Francisco Federal Reserve President Daly demonstrated the King Canute problem, urging technology companies to become less competitive and force workers back to offices. Structural change revolutionizes working practices, and the reaction is often the dangerous idea of restorative nostalgia (believing everything will be OK if only we just return to a mythical past). Recognizing change and adapting to it is more productive.

US data is meager and survey based. Only six economists forecast the Richmond Fed manufacturing sentiment survey, and now is not the time to start giving the figures any attention. The Conference Board consumer sentiment poll will be distorted by political polarization…

We maintain our view that the US economy is headed for a soft landing.

More moderate growth in consumer spending should help to keep inflation on a downward trend.

We expect the Fed to initiate a rate-cutting cycle in September.

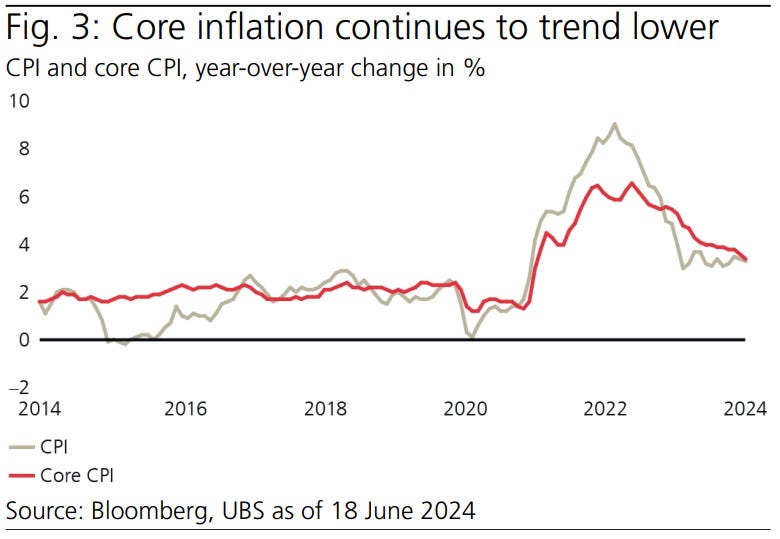

… Inflation Core CPI, which excludes food and energy prices, surprised to the downside in May, rising 0.16% month-over-month, the smallest monthly increase since August 2021. As shown in Fig. 3, in year-over-year terms, the core inflation rate continues to trend lower although it is still well above its pre-pandemic level. Goods inflation has turned negative as household spending shifts toward services. However, the relatively strong demand for services is contributing to some ongoing inflationary pressure. Shelter inflation in particular has remained stickier than we expected, but we still view a slowdown in the months ahead as inevitable given more timely information on new rental leases. Businesses are reporting that consumers are pushing back against price increases, and there have been more anecdotes about price cuts, especially at stores catering to lower-income households. We therefore expect the downward trend in core inflation to continue.

Policy The Fed left its policy unchanged at the FOMC meeting on 12 June, in line with market expectations. As shown in Fig. 4, the median “dot” now indicates only one 25 basis point rate cut by year-end, versus the three cuts projected back in March, suggesting that they may stay on hold until December. However, it is important to keep in mind that the Fed’s economic projections are strong relative to both our own expectations and consensus, helping to justify a later start to rate cuts. We maintain our base case that the Fed will be in a position to cut rates in September as it receives softer data on growth, the labor market, and inflation. We see risks as skewed toward the Fed staying on hold for longer than in our base case, but we still see additional rate hikes as unlikely. As suggested by the dots, once the Fed starts to cut, additional cuts are likely to follow. On the fiscal side, we do not expect significant policy changes until after the election.

U.S. inflation surged in the early post-COVID period, driven by economic shocks such as supply chain disruptions and labor supply constraints. Following its peak at 6.6 percent in September 2022, core consumer price index (CPI) inflation has come down rapidly over the last two years, falling to 3.6 percent recently. The authors argue that the same forces that drove the nonlinear rise in inflation in 2021 have worked in reverse since late 2022, accelerating the disinflationary process.

… Conclusion This post has argued that the combined shock to imported inputs and labor supply may have amplified the inflation surge in the early post-COVID period. As the shock has dissipated, our model suggests that the same mechanism has worked in reverse and accelerated the decline in inflation. The amplification effect may be one explanation for the faster than expected disinflation over the last two years.

We do not expect the supply-side shocks to fully explain the rise and fall of inflation due to the important role played by demand-side factors, such as government transfers during the pandemic. Importantly, these demand-side factors could partially be responsible for the supply-side factors we observe.

Going forward, in light of our model results we expect the downward pressure on inflation due to the amplification forces highlighted here to diminish since supply chain conditions have returned to normal, limiting the disinflation from the interaction with the labor market.

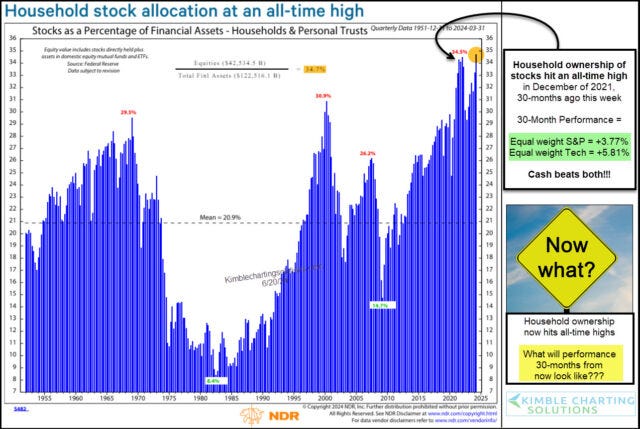

Kimble: Household Ownership of Equities At All-Time High; Should Investors Be Concerned?

… Looking at two important “equal weight” index ETFs – RSP (S&P 500) and QQEW (Nasdaq 100) – we can see that they have risen just 3.77% and 5.81% respectively over the past for 30 months. Even cash has outperformed!

Fast forward to today. Household ownership is now higher than it was 30 months ago (the highest in history). Do we have another crowded trade in equities? What will stock performance look like 30 months from now?

… 5. Yield Curving: The other issue is some of the traditional cycle indicators are at peak cycle-maturity levels, and turning the corner. So again, we need to keep vigilant on this because things could turn faster and for reasons other than any of us expect.

“These 3 lines all measure the same thing – the maturity of the business cycle (**and turning points**). On all 3 counts they say the cycle is long in the tooth, and turning.”

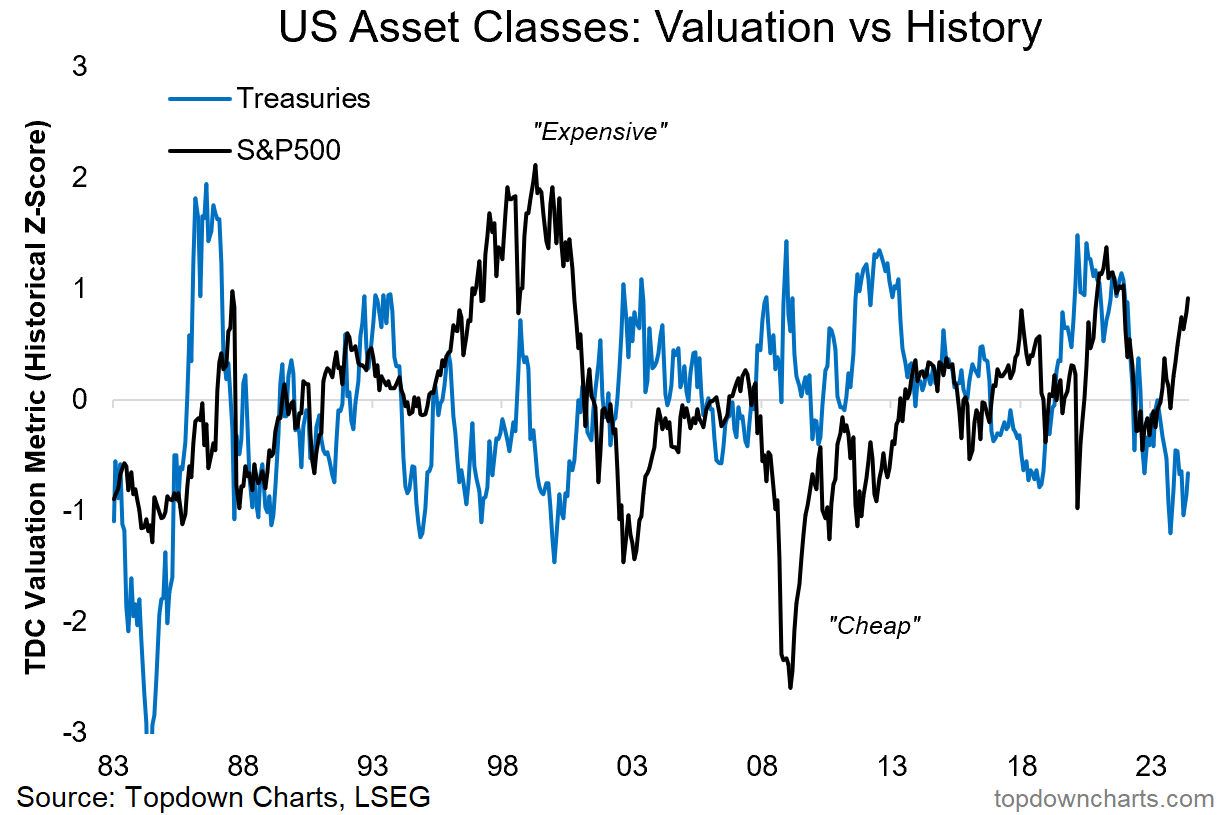

6. Bond Bargain: Bonds are cheap, stocks are not.

“As such, and while things have moved a lot since the brief 5% reading for the US 10-year treasury yield in October last year, government bond valuations are still cheap, and the macro downside risk scenario I outline here is bond bullish. It won’t be a straight line, but bonds likely see further upside in the coming year following one of their worst bear markets in recent history.

Stocks are a different matter though…”

ZH: $50 Billion In Quarter-End Pension Selling On Deck: JPM

… Here is the analysis the author of JPM's Flows and Liquidity newsletter does to calculate how much quarter-end selling is on deck:

When we look at the universe of US defined benefit pension funds, private and public funds together have just over $9tr of assets. If we assume they were fully rebalanced at the end of December and taking into account the QTD performance of US equities and bonds, we estimate that the pending equity rebalancing flow by US defined benefit pension fund plans into quarter-end could see net selling of equities of just under $80bn.

However, as noted recently, the caveat in this calculation is that pension funds overall tend to be less strict in terms of rebalancing than balanced mutual funds or other pension fund related entities such as Norges Bank/GPIF, and as a result JPM has typically estimated that around a third of the estimated pension fund rebalancing flow would take place in the same quarter. This implies net selling in 2Q24 of around $26bn.

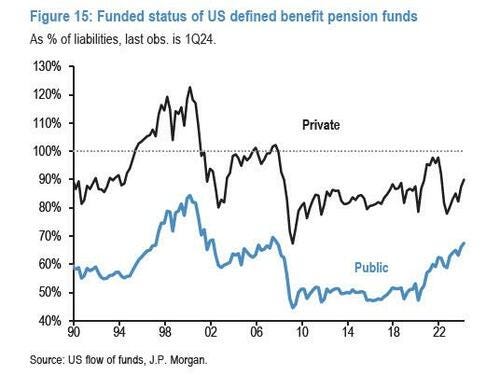

… Panigirtzoglou next looks at private and public funds separately, and finds that for both quarters taken together the net equity selling amounted to around half of the pending rebalancing estimate, while for public funds this was around a quarter. This is consistent with the idea that public defined benefit pension funds, with a lower funded status and a higher equity allocation, have tended to be slower at rebalancing. That said, with the funded status for public pension funds having improved from below 50% in early 2020 to just under 70% in 1Q24, its highest level since 3Q07, the gap in rebalancing behavior between private and public funds could narrow over time.

Finally, in addition to US defined benefit pension funds, when JPM looks at the rebalancing demand from balanced mutual funds - who tend to balance monthly - a relatively small gap between equity and bond returns since the start of June, implies a modest net selling equity selling of around $10bn.

… This implies combined net equity sales of around $24bn for these investors, or a total of around $50bn when combined with US defined benefit pension funds.