while WE slept: Bonds mixed, USTs contained, Bunds to session lows; "How Long Will High Rates Last? Bond Markets Say Maybe Forever" -BBG; bonds signal stock correction -ASC

Good morning … A relatively quiet start to a summer week after a hotter than hot weekend here in the NE. With little insight ahead of this weeks ‘liquidity events’ (2s, 5s and 7s tomorrow, Wed and Thurs) and this weeks ending ‘flation report, I’m going to begin by checking in on 10s …

10yy DAILY: very definition OF why NOT to sell quiet markets and take a step back and note 2024 range (~ 4.70% - 3.79%) as we’re close to the middle (4.245%) with momentum nearer overBOUGHT … can / will be resolved by trading HIGHER OR simply time at a price)

… with this visual in mind and in the case you’ve not yet take a moment to review current setup, the latest MacroVoices with Rosie (Team Rate CUT) is worth your time.

NEWSQUAWK: US Market Open: Sentiment improves with equities on the front foot whilst Dollar slips ahead of Fed speak … Bonds are mixed with USTs contained, whilst Bunds slip to session lows … USTs are rangebound with a few fleeting ticks higher emerging on the German Ifo release but with just under 10 ticks to go to re-test Friday's pre-PMI best. Fed's Goolsbee & Daly are scheduled for later today, but this week's focus will reside on US PCE on Friday. USTs currently trading around 110'16.

Reuters Morning Bid: Transatlantic split reopens as half-year nears … Adding to the confusion, and perhaps the greater comfort that more interest rate cuts are coming in the second half, is the fact that the aggregate global economic surprise index has turned negative to the worst reading in almost a year …

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use … here’s SOME of what Global Wall St is sayin’ …

We expect US yields to remain range-bound and thus suggest positioning in trades that carry positively.

Ahead of the first round of voting in the French elections, we like hedging against further volatility in European assets.

We like selectively receiving EM rates as valuations have become stretched.

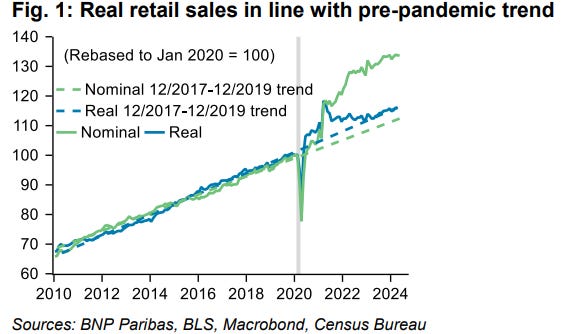

Although the US rates market has been whipsawed in recent weeks, the bottom line is that ranges have held. While US economic data has slowed of late, we view this as a cooling rather than deterioration and thus expect ranges to continue to hold for now. To be sure, the May retail sales report indicated some belt-tightening among consumers as downward revisions to the previous two months toned down a solid increase in control group sales. But big picture, the recent data shows personal consumption remains healthy, back to tracking its pre-pandemic trend in inflation-adjusted terms (Figure 1).

The recent moderation to trend from the robust pace in the wake of the Covid recession was expected and partly reflects the impact of monetary policy restriction. High interest rates and inflation disproportionately impact lower-income households, which mainly spend on goods. Conversely, higher-income households have pushed spending on services above the pre-pandemic trend, something we expect will continue to support growth in consumer spending this year. We thus estimate a solid pace of growth in personal spending (0.3% m/m) in the May PCE report to be released on Friday…

I am fond of the saying that the economy is not the stock market and the stock market is not the economy. Often, a strong economy is not good for stocks, while a soft one can drive a very bullish tape. This latter case is the classic 'late cycle' period in which we find ourselves, in our view. More specifically, when the economy is slowing from prior tightening by the Federal Reserve, the equity market often starts to get excited about the Fed reversing course and valuations rise in anticipation. With P/E multiples and other valuation metrics now in the top decile, the question is, “Will valuations begin to fall faster than earnings growth and lead to a meaningful correction?”

At the stock level, this is already happening, as illustrated by the extremely weak breadth ( Exhibit 1 ). Most stocks are seeing valuations fall more than earnings are rising – which is why stock picking has become so important for active investors this year. While this can create great long/short opportunities, the list of longs has become harder to find, and the momentum in a few stocks continues almost unabated…

… As highlighted in our most recent research, economic growth surprise indices have been trending lower all year, with the index making a new low this past week ( Exhibit 2 ). So far, the S&P 500 has taken the weaker data in its stride while treating bad economic data as still good for Large-Cap Quality stocks given expectations of Fed rate cuts. Meanwhile, several other indices have broken down, with some now negative on the year.

… The bottom line is that the ongoing policy mix of heavy fiscal spending and tight interest rate policy is crowding out many companies and consumers in way that is unsustainable, in our view.

This week has a lot of politics in it, and markets are rarely that good at pricing political risk. The US presidential debate may make investors pay attention to political risk earlier than is normal in the US political cycle. Because so much attention has focused on the suitability of the candidates for office (rather than their policy positions), this debate might actually matter.

Inflation is one real world issue that has had political resonance (the US personal consumer expenditure deflator is released later this week). Politically, inflation is an emotional issue not a rational issue—consumers focus on price levels of high frequency purchases. Reports of price discounting in food items profit-led inflation retreats are likely to impact political perceptions far more than official data…

… And from Global Wall Street inbox TO the WWW,

AllStarCharts: The Bond Market Points to a Stock Market Correction

Mark it, Dude.

We have another bearish divergence calling strike three on the stock market rally…

High-yield bonds $HYG versus US Treasuries $IEI.

Check out the HYG/IEI ratio (dark blue line) overlaid with the S&P 500 ETF $SPY:

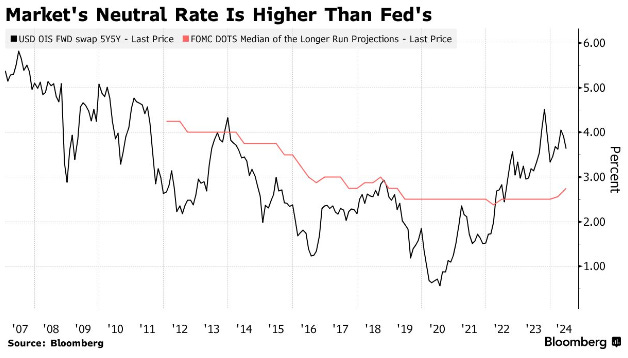

Apollo: The Neutral Interest Rate Is Higher than the Fed Thinks

The FOMC has started to revise higher its estimate of where the fed funds rate will be in the long run. This is likely driven by upward pressures on inflation and rates from deglobalization, the energy transition, more restrictions on immigration, more defense spending, and higher levels of government debt.

Bloomberg: How Long Will High Rates Last? Bond Markets Say Maybe Forever

Traders bet on a higher long-term funds rate than Fed

Neutral rate shift sets up a limit to gains in Treasury bonds

… “The significance is that when the economy inevitably decelerates, there will be fewer rate cuts and interest rates over the next ten years or so could be higher than they were over the last ten years,” said Troy Ludtka, senior US economist at SMBC Nikko Securities America, Inc.

Forward contracts referencing the five-year interest rate in the next five years — a proxy for the market’s view of where US rates might end up — have stalled at 3.6%. While that’s down from last year’s peak of 4.5%, it’s still more than one full percentage higher than the average over the past decade and above the Fed’s own estimate of 2.75%.

This matters because it means the market is pricing in a much more elevated floor for yields. The practical implication is that there are potential limits to how far bonds can run. This should be a concern for investors gearing up for the kind of epic bond rally that rescued them late last year.

For now, the mood among investors is growing more and more upbeat. A Bloomberg gauge of Treasury returns was down just 0.3% in 2024 as of Friday after having lost as much as 3.4% for the year at its low point. Benchmark yields are down about half a percentage point from their year-to-date peak in April.

… But if the market is right that the neutral rate – which cannot be observed in real time because it’s subject to too many forces – has permanently climbed, then the Fed’s current benchmark rate of more than 5% may be not as restrictive as perceived. Indeed, a Bloomberg gauge suggests financial conditions are relatively easy.

… The true level of the neutral rate, or R-Star as it is also known, has become the subject of hot debate. Reasons for a possible upward shift, which would mark a reversal from a decades-long downward drift, include expectations for large and protracted government budget deficits and increased investment for battling climate change.

Sam Ro from TKer: Warren Buffett: 'It takes just a few winners to work wonders'

… Buffett, CEO of Berkshire Hathaway, is often praised as history’s greatest investor. His legendary knack for picking stocks for Berkshire’ equity portfolio helps explain why the company’s shares have massively outperformed the S&P 500 over the years.

However, returns have not been evenly distributed across Berkshire’s stock holdings.

“Over the years, I have made many mistakes,” Buffett explained in his annual letter published in 2023 (emphasis added). “Our satisfactory results have been the product of about a dozen truly good decisions — that would be about one every five years.“

At the time, he walked through examples including Coca-Cola and American Express, which multiplied in value many times over while returning massive cash dividends. Read more about it here.

“The lesson for investors: The weeds wither away in significance as the flowers bloom,” Buffett said. “Over time, it takes just a few winners to work wonders.”

In his annual letter published this past February, he discussed those positions again, saying (emphasis added): “Patience pays, and one wonderful business can offset the many mediocre decisions that are inevitable.”

Is what’s happening today so different from history?

The chart below from Bespoke Investment Group shows how the “Magnificent 7” tech names have been responsible for nearly half of the S&P 500’s returns since the beginning of the bull market in October 2022.

The non-Magnificent names haven’t exactly been mediocre. But it’s clear that the strength of a few stocks have mattered…

… On Monday, Citi’s Scott Chronert raised his year-end target for the S&P 500 to 5,600 from 5,100. This was his first revision from his initial target.

“The weighting effect of the mega-cap growth cohort is exerting an outsized influence on index price action,” he said.

On Friday, Capital Economics’ Thomas Mathews raised his year-end target to 6,000 from 5,500. This was his first revision as well…

ZH: Fragility In A One Stock, Stock "Market" By Peter Tchir of Academy Securities

Ok, calling this a “one stock” stock “market” seems a bit extreme, but is it? On Thursday when stocks rolled over (the Nasdaq 100 started higher at the open and then dropped almost 300 points from there), virtually everyone I spoke to pointed to NVDA shares reversing as the main weight on the overall indices. Throughout much of Thursday and Friday, I was receiving many more notes on support/resistance related to NVDA than the indices, Treasuries, or anything else that could be whipping markets around. Yes, Friday was “triple witching,” which likely added to the volatility, but there was one stock that dominated all market conversation…

AND … something more specific relating TO 2yy tomorrow ahead of the auction but … THAT is all for now. Off to the day job…

I'm haunted by Rosie's quote on MarcoVoices-"soon bonds will be producing stock-like returns". It's gonna take more than his predicted 75 bps cuts in 2024 to achieve THAT :( IMHO

I'm haunted by Rosie's quote on MarcoVoices-"soon bonds will be producing stock-like returns". It's gonna take more than his predicted 75 bps cuts in 2024 to achieve THAT :( IMHO